Dynamic Application Security Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 8.63 Billion |

| Growth Rate (2026 - 2031) | 15.59% CAGR |

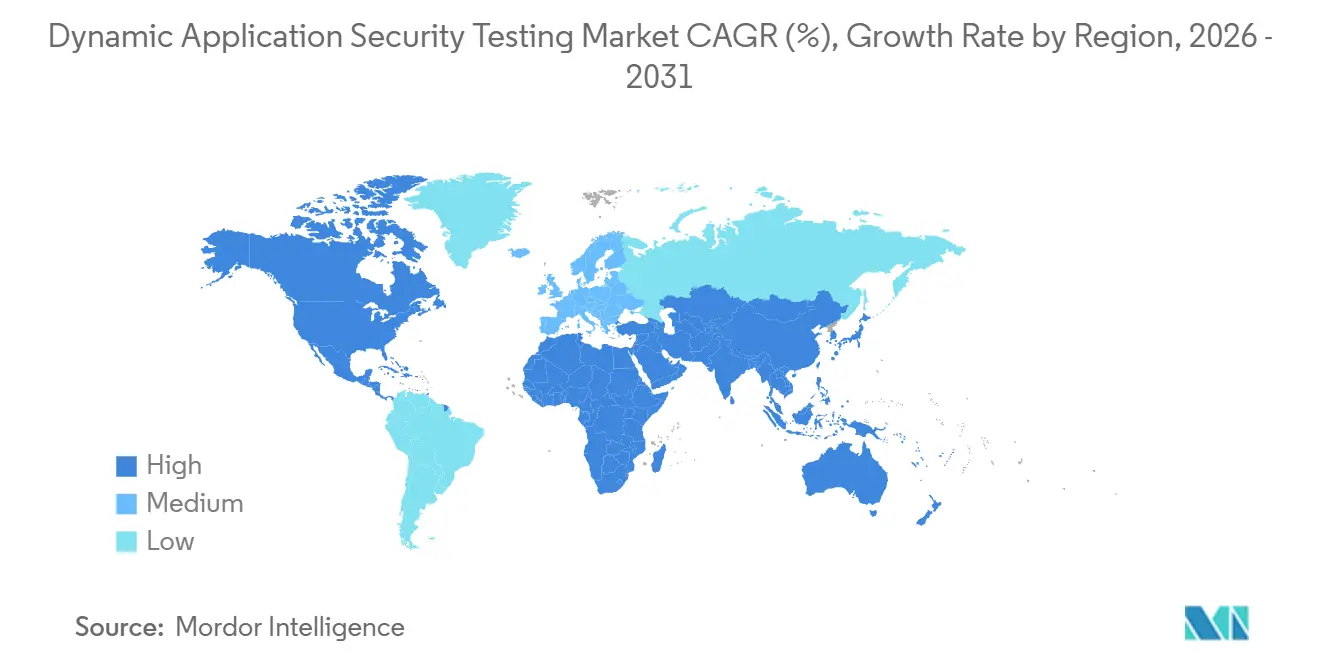

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dynamic Application Security Testing Market Analysis by Mordor Intelligence

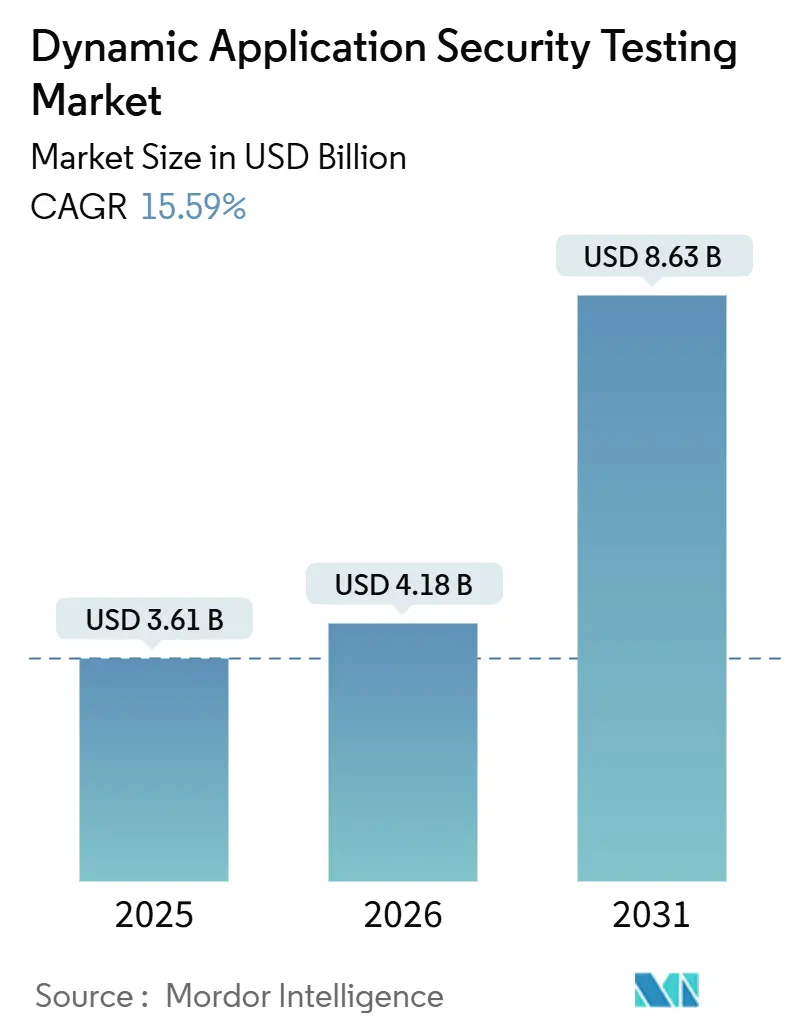

The dynamic application security testing market size is projected to be USD 3.61 billion in 2025, USD 4.18 billion in 2026, and reach USD 8.63 billion by 2031, growing at a CAGR of 15.59% from 2026 to 2031. Escalating API-centric attack volumes, regulatory mandates that insist on runtime validation, and rapidly falling exploit-creation costs together accelerate demand for dynamic testing that can exercise live applications instead of reviewing static code. Vendors are embedding artificial-intelligence engines that generate boundary-condition test cases, while buyers increasingly favor platforms that integrate with continuous integration pipelines so that every build triggers a scan. Cloud-native delivery dominates because scanners must follow containerized workloads that redeploy dozens of times per day. Competitive pressure pivots on false-positive reduction, proven API coverage, and support for modern protocols such as GraphQL and gRPC, all of which influence procurement decisions for large enterprises and small businesses alike.

Key Report Takeaways

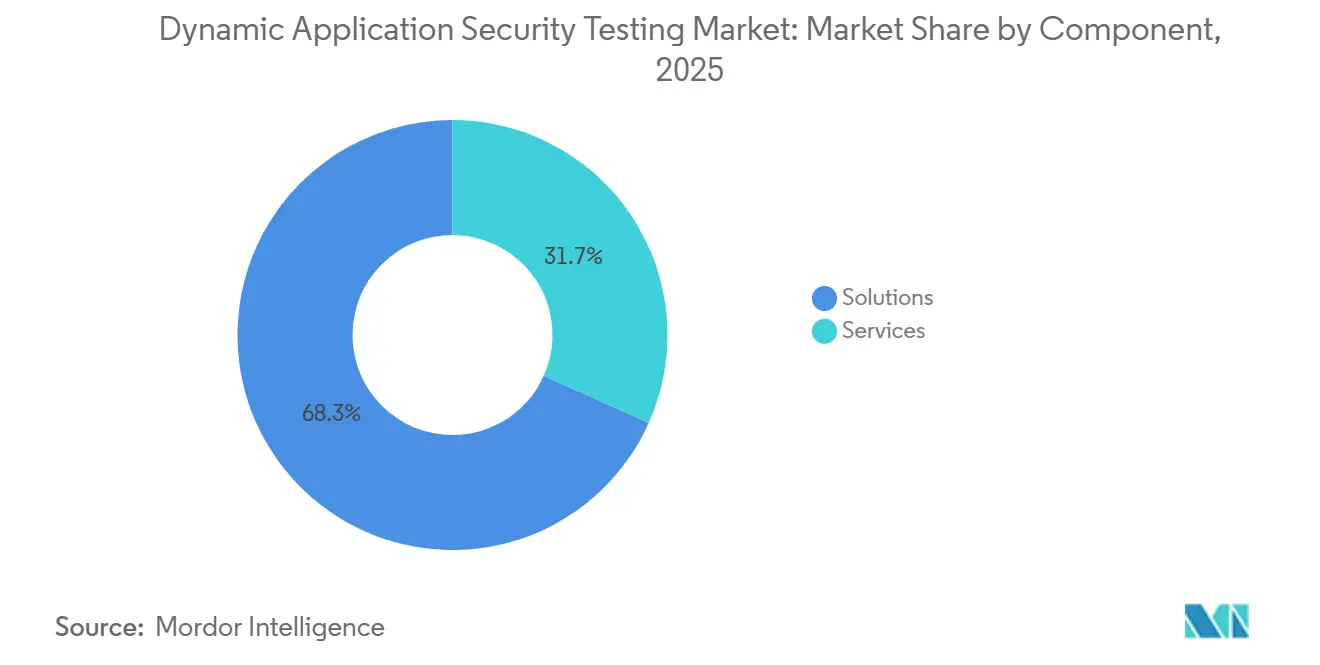

- By component, solutions held a 68.30% share of the dynamic application security testing market in 2025, whereas services are advancing at a 15.62% CAGR through 2031.

- By deployment mode, cloud-based platforms accounted for 73.50% of the dynamic application security testing market size in 2025 and are projected to expand at a 15.76% CAGR through 2031.

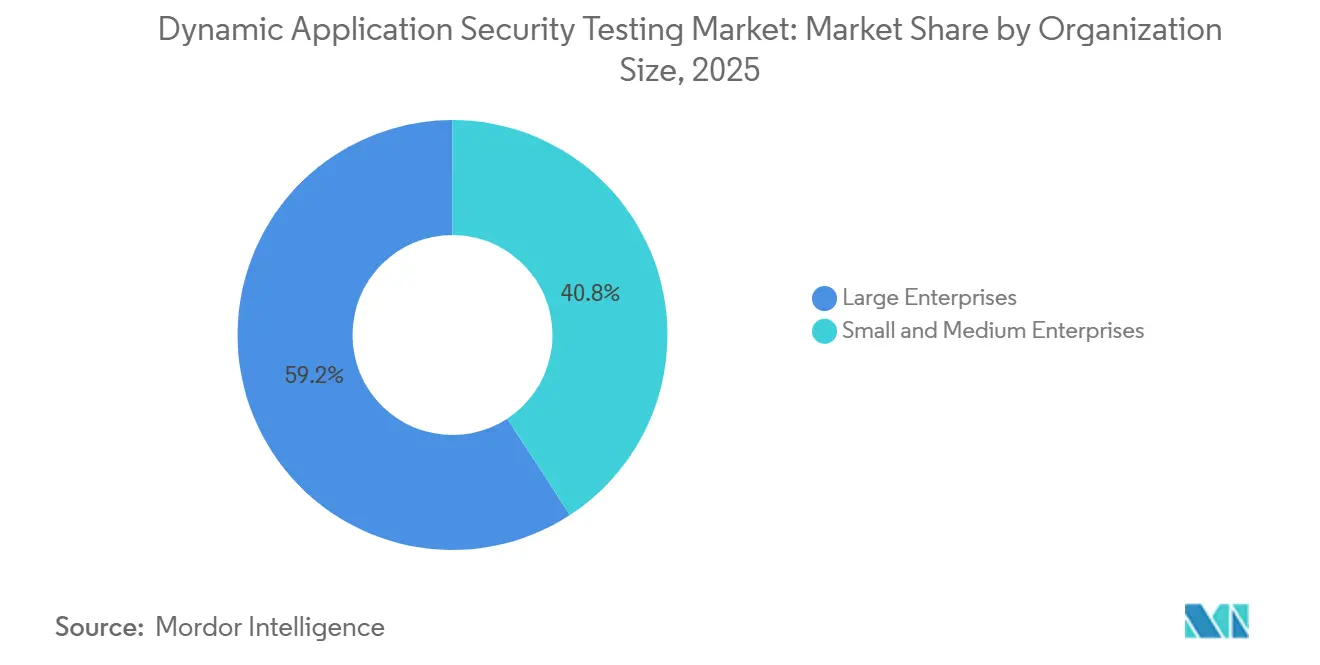

- By organization size, large enterprises captured 59.20% of the dynamic application security testing market share in 2025, while small and medium enterprises are growing at a 16.99% CAGR.

- By end-user vertical, BFSI commanded 24.20% of 2025 revenue, yet retail and e-commerce is the fastest riser at an 18.65% CAGR to 2031.

- By geography, North America led with 42.80% share in 2025, whereas Asia-Pacific is forecast to grow at a 17.10% CAGR, the highest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dynamic Application Security Testing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of API-Centric Attacks | +3.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Shift-Left DevSecOps Adoption | +3.0% | Global, led by North America and Europe | Medium term (2-4 years) |

| Mandatory SBOM and Supply-Chain Rules | +2.5% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Exploit Automation | +2.2% | Global, R and D hubs in North America and Asia-Pacific | Long term (≥ 4 years) |

| Low-Code/No-Code Proliferation | +1.8% | Global, strong in mature citizen-developer markets | Medium term (2-4 years) |

| Pay-Per-Scan Pricing Disrupting TCO | +1.5% | Global, strongest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Volume of API-Centric Attacks

API endpoints generated 48% of all web-application attacks in 2024, equal to 150 billion events that Akamai traced across its global network.[1]Source: Akamai, “State of the Internet Security Report 2024,” akamai.com Wallarm cataloged 1,602 unique API vulnerabilities in Q3 2025, a 20% sequential rise, dominated by broken object-level authorization and excessive data exposure flaws. The shift to microservices means a modern commerce application now surfaces 200-500 APIs, magnifying the runtime surface that only the dynamic application security testing market can probe effectively. Traceable AI reported that 57% of organizations suffered an API breach in the prior year, yet just 34% deployed API-specific defenses.[2]Source: Traceable AI, “2024 API Security Survey,” traceable.ai Regulatory pressure compounds the urgency, as PSD2 and open-banking rules enforce third-party access that must be validated for authorization integrity.

Shift-Left DevSecOps Adoption

GitLab’s 2024 survey showed 58% of developers already run dynamic tests during development pipelines, up from 41% two years earlier. Despite this progress, only one-third include dedicated API scans, largely because authentication credentials and ephemeral test environments complicate automation. Datadog found that 15% of live services still contained vulnerabilities cataloged in CISA’s Known Exploited list, reinforcing the need for earlier discovery. Incremental scanners that test changed endpoints in five-minute cycles now align with sub-10-minute build targets, encouraging broader adoption.

Mandatory SBOM and Supply-Chain Disclosure Rules

CISA expanded SBOM minimum elements in August 2025 to include provenance, license, and vulnerability status, but also stated that disclosed components must undergo runtime validation.[3]Source: CISA, “Software Bill of Materials,” cisa.gov The EU Cyber Resilience Act imposes EUR 15 million or 2.5% turnover penalties for non-conformance, pushing manufacturers to prove exploitability rather than merely list components. Medical devices face similar proof requirements under FDA guidance issued in 2024. Each mandate elevates the dynamic application security testing market because runtime probing confirms whether a vulnerable library is reachable in production.

AI-Enabled Exploit Automation

Research on LLM agents showcased their ability to autonomously exploit up to 51% of tested CVEs, achieving this feat at costs under USD 4 and significantly reducing manual effort by two orders of magnitude. This advancement highlights the growing efficiency of automated systems in cybersecurity. In 2024, Datadog noted a substantial reduction in the median time-to-exploit, which dropped to just seven days. This shift is primarily attributed to the adoption of automated payload generation, which has streamlined the exploitation process. Vendors are now actively integrating generative models capable of creating test cases directly from API schemas, enhancing their ability to identify vulnerabilities. At the same time, attackers are leveraging similar agents to exploit weaknesses, igniting an arms race in cybersecurity. This ongoing competition is driving a continuous and heightened demand for more intelligent and advanced dynamic scanning solutions to stay ahead of emerging threats.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Signal-to-Noise (False-Positive) Fatigue | -2.0% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Scarcity of AppSec Skill-Sets | -1.8% | Global, most severe in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Limited Runtime and Business-Logic Coverage | -1.2% | Global, high in complex microservices deployments | Medium term (2-4 years) |

| Fragmented Standards across Jurisdictions | -0.9% | Multinationals operating in multiple regulatory regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Signal-to-Noise (False-Positive) Fatigue

Security teams face a significant challenge in managing the overwhelming volume of alerts generated by their systems, with 70-90% of these alerts being false positives. This high rate of irrelevant alerts forces teams to spend considerable time and resources triaging thousands of notifications just to identify the critical 10-30% that genuinely require attention. Over time, developers tend to disregard alerts due to the persistent noise, which ultimately compromises the achievement of essential security objectives. To address this issue, instrumented proof-based scanning solutions offered by vendors like Invicti have proven effective in reducing irrelevant findings by up to 60%. This improvement not only enhances efficiency but also allows security teams to focus on actionable insights. As a result, buyers are increasingly emphasizing precision as a critical requirement, often listing it as a mandatory feature in their requests for proposals.

Scarcity of AppSec Skill-Sets

In 2024, ISC2 identified a significant global cybersecurity talent shortfall of 4.8 million professionals, with a particularly pronounced scarcity in dynamic testing expertise. This gap underscores the growing demand for specialized skills in the cybersecurity market. The average time required to fill these critical roles now exceeds six months, creating substantial challenges for organizations seeking to secure their systems. Additionally, salary premiums for these roles have surged to 40%, making it increasingly difficult for many small enterprises to attract and retain such talent. However, advancements in technology have provided alternative solutions. Firms can now leverage managed services and security-as-code APIs, which simplify the process of conducting advanced testing. These tools enable organizations to access critical testing outcomes without the need to hire and onboard these rare and highly sought-after specialists, thereby addressing some of the challenges posed by the talent gap.

Segment Analysis

By Component: Services Scale Faster Than Software

Solutions generated 68.30% of 2025 revenue, showing that enterprises still license full-featured platforms to cover broad asset inventories. Yet the services slice is growing at 15.62% CAGR, faster than the overall dynamic application security testing market. Providers integrate scanners with CI/CD systems, tune authentication flows, and interpret findings for business units. Global consultancies, including Accenture, expanded application-security headcount through 2025 to meet this demand.

Services also appeal to organizations that struggle with false positives; a managed team validates exploitability before escalating, trimming alert queues. As a result, the dynamic application security testing market size attached to services is projected to expand steadily through 2031. Vendors respond by bundling onboarding, custom policy creation, and regular health checks inside subscription tiers, aligning economic incentives with customer outcomes.

By Deployment Mode: Cloud-Based Delivery Dominates

In 2025, spending on cloud-hosted scanners accounted for 73.50%, and they continue to outpace on-premise solutions, growing at a rate of 15.76% CAGR. Cloud engines possess the capability to discover and test containerized microservices and serverless functions, which are redeployed dozens of times daily, in near real-time. This ability to handle frequent redeployments efficiently is a key factor driving the adoption of cloud-hosted solutions. The extension of Amazon Inspector to Lambda and container workloads further highlights the growing preference of buyers for fully managed offerings, as these solutions reduce operational overhead and enhance scalability.

In industries with stringent regulations, on-premise deployment remains a critical requirement due to data sovereignty policies that limit external processing. These policies ensure sensitive data remains within controlled environments, making on-premise solutions indispensable for compliance. As a result, hybrid architectures are emerging as a practical solution: the scan engine operates in the vendor's cloud, but credentials and other sensitive data are securely stored on the customer's hardware. This setup ensures compliance requirements are met without compromising the breadth of security coverage. Such a mixed model underscores the adaptability and flexibility required in the dynamic application security testing market, enabling it to cater to both cloud-centric developers seeking innovation and risk-averse incumbents prioritizing regulatory compliance and data security.

By Organization Size: SMEs Narrow the Adoption Gap

In 2025, large enterprises commanded a dominant 59.20% share of the revenue, driven by their expansive application portfolios and stringent audit mandates. These organizations manage extensive application estates, which require robust security measures to comply with regulatory standards and ensure operational efficiency. In contrast, SMEs are rapidly gaining ground, boasting a robust 16.99% CAGR, thanks to the shift from hefty upfront licenses to usage-based pricing models. This pricing approach significantly reduces the financial burden on smaller organizations, enabling them to adopt advanced security solutions. A case in point is StackHawk, which offers a free tier for open-source projects and charges per-scan for commercial workloads, catering to budget-conscious teams and fostering wider adoption among SMEs.

While SMEs grapple with expertise limitations, managed dynamic scanning services have emerged as a practical and cost-effective solution. These services address the skill gaps in smaller organizations by providing specialized expertise and continuous monitoring. Indian outsourcing firms, leveraging regional security operation centers, provide continuous testing services at competitive rates, bolstering their foothold in emerging markets. These firms enable SMEs to access high-quality security testing without the need for significant in-house resources. As a result, SMEs' share in the dynamic application security testing market is poised for a steady ascent in the coming years, driven by increasing adoption of managed services and the growing need for robust security measures in a rapidly evolving digital landscape.

By End-User Vertical: Retail and E-Commerce Accelerate Post-Breach

Thanks to its open-banking exposure and hefty regulatory fines, the BFSI sector held a commanding 24.20% share of the 2025 market value. This dominance highlights the sector's critical role in driving the adoption of advanced security measures. Yet, in the wake of the Ticketmaster and Santander breaches, which compromised 560 million records, retail and e-commerce expenditures have been on a robust ascent, boasting an 18.65% CAGR. These incidents have underscored the vulnerabilities in data security, prompting businesses to prioritize investments in protective measures. With PCI DSS 4.0 now mandating continuous runtime validation for systems handling cardholder data, the necessity for dynamic testing has never been clearer. This regulatory shift emphasizes the importance of proactive security strategies to mitigate risks and ensure compliance.

Guided by FDA device-security directives, the healthcare sector is ramping up its security measures to address emerging threats. The sector's increasing reliance on connected devices has made robust security protocols indispensable. Simultaneously, the energy, utilities, and manufacturing sectors are turning to dynamic testing to fortify their industrial IoT interfaces. These industries face unique challenges due to the critical nature of their operations, making the adoption of advanced security solutions a priority. The pattern is consistent across all sectors: the combination of live, externally-facing APIs and the potential for financial and reputational harm fuels ongoing investments in the dynamic application security testing market. This sustained investment reflects the growing awareness of the need for comprehensive security frameworks to protect sensitive data and maintain operational integrity.

Geography Analysis

North America led with 42.80% of 2025 revenue because Executive Order 14028 forces federal contractors to demonstrate runtime vulnerability validation. Adoption depth is highest, but teams also experience the greatest alert fatigue, spurring premium demand for proof-based scanning and AI triage. Canada’s Critical Cyber Systems Protection Act, enacted in 2024, widened mandatory testing to provincially regulated utilities, adding incremental demand.

Europe contributed roughly 29% of spending in 2025, propelled by the progressive rollout of NIS2, DORA, and the Cyber Resilience Act. German and French financial institutions extend scans to every third-party API, aligning with 24-hour incident-report deadlines. Post-Brexit divergence obliges United Kingdom firms that serve EU clients to follow both regulation sets, inflating test volume and complexity.

Asia-Pacific is the fastest growing region at a 17.10% CAGR. China’s Multi-Level Protection Scheme 2.0 now mandates dynamic assessments for Level 3 systems or higher, covering most enterprise applications. India’s Digital Personal Data Protection Act enforces fines up to INR 2.5 billion (USD 30 million) for breaches, encouraging exporters to certify security posture to global customers. Japan, South Korea, Australia, and New Zealand together make sizeable contributions where breach-notification laws tighten annually.

Competitive Landscape

The dynamic application security testing market remains moderately fragmented; the top ten suppliers control about 45-50% of revenue. Incumbents such as Invicti Security, PortSwigger, and Qualys compete on breadth, layering API, compliance, and proof-based engines into unified dashboards. New entrants, including Bright Security and Probely, focus on developer experience by integrating directly with GitLab or GitHub workflows.

AI-assisted triage and test-case generation dominate patent filings, underscoring vendor recognition that false-positive fatigue jeopardizes renewals more than raw detection rates. Invicti’s acquisition of API Fortress in January 2026 signals consolidation aimed at protocol depth, while PortSwigger’s automated multi-factor authentication handling released in December 2025 exemplifies niche capability leap-frogging.

White-space persists in business-logic flaw detection and in reliably scanning protocols such as GraphQL, gRPC, and WebSocket. Providers that blend generative AI with behavioral instrumentation to close these gaps are positioned to capture future share as the dynamic application security testing market matures.

Dynamic Application Security Testing Industry Leaders

IBM Corporation

Synopsys Inc.

Veracode Inc.

Checkmarx Ltd.

OpenText Corporation (Fortify)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Invicti Security acquired API Fortress to bolster GraphQL, gRPC, and WebSocket coverage.

- December 2025: PortSwigger released Burp Suite Enterprise 2025.4, adding automated multi-factor authentication workflows.

- November 2025: Qualys launched TotalCloud DAST, correlating runtime findings with cloud misconfigurations.

- October 2025: StackHawk raised USD 60 million in Series C funding led by Sapphire Ventures.

Global Dynamic Application Security Testing Market Report Scope

Dynamic Application Security Testing is a program in which the application is tested in a production-like environment from the outside, unlike SAST. As DAST tools don't have access to the application's source code, they detect vulnerabilities by performing actual attacks on the web app, mobile app, and APIs, similar to a real hacker. The report includes an in-depth analysis of solutions and services offered by various vendors for mobile and web-based application security for large enterprises and SMEs across the globe.

The Dynamic Application Security Testing Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud-Based, and On-Premise), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defence, Retail and E-Commerce, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud-Based |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defence |

| Retail and E-Commerce |

| Energy and Utilities |

| Manufacturing |

| Other End-User Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Vertical | BFSI | ||

| Healthcare | |||

| IT and Telecom | |||

| Industrial and Defence | |||

| Retail and E-Commerce | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Other End-User Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on dynamic application security testing expected to grow through 2031?

Industry revenue is projected to climb at a 15.59% CAGR between 2026 and 2031, rising from USD 4.18 billion in 2026 to USD 8.63 billion by 2031.

Which deployment approach attracts the most investment today?

Cloud-based scanners already account for 73.50% of 2025 spending because they can track containerized and serverless endpoints that redeploy frequently.

Why are retailers ramping up dynamic testing budgets?

Breaches that exposed 560 million records in 2024 highlighted API authentication gaps, prompting retail and e-commerce firms to boost outlays at an 18.65% CAGR.

What creates the biggest hurdle to wider adoption inside small companies?

A shortage of application-security expertise and historically high license costs slow uptake, though usage-based pricing and managed-service options are closing the gap.