| Study Period | 2021 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 6.36 Billion |

| Market Size (2030) | USD 7.77 Billion |

| CAGR (2025 - 2030) | 4.09 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Dry Eye Disease Market Analysis

The Dry Eye Disease Market size is estimated at USD 6.36 billion in 2025, and is expected to reach USD 7.77 billion by 2030, at a CAGR of 4.09% during the forecast period (2025-2030).

Beyond Simple Lubrication: The New Treatment Paradigm

The dry eye disease treatment landscape has evolved well beyond simply squirting artificial tears into irritated eyes. The doctors are increasingly focused on tackling specific inflammatory pathways rather than just soothing symptoms. Look at the recent GOBI and MOJAVE studies for Bausch + Lomb's new solution; they enrolled over 1,200 patients and showed meaningful improvements by week 8. It's revolutionizing how doctors approach dry eye treatment from the ground up. Patients with stubborn cases who've tried everything now have legitimate options. And for companies and clinics. The message couldn't be more precise: invest in treatments that address the root causes or risk being left behind. The market is rewarding those who understand that treating the underlying pathophysiology—not just temporarily relieving symptoms—creates both better outcomes and stronger business models in this increasingly crowded space.

The Digital Transformation of Dry Eye Diagnostics

Digital health tech is completely changing how we handle dry eye disease. The latest diagnostic platforms use AI to spot subtle changes in meibomian gland dysfunction that even trained specialists might miss. These tools don't just make diagnosis more accurate; they're transforming how researchers evaluate whether new treatments actually work. Beyond the clinic, this digital revolution is speeding up R&D by giving companies access to real-world patient data they never had before. Back in 2022, we already knew that medications like Lifitegrast (Xiidra) 5% were indicated for treating dry eye symptoms. Now, these digital tools are helping doctors determine exactly which patients will respond best to which treatments. In a market increasingly defined by precision approaches, the digital laggards risk getting left in the dust.

Patient Experience as Market Driver: The Convenience Revolution

The dry eye market is increasingly being shaped by what patients want, not just what doctors prescribe. The days of patients simply accepting whatever treatment regimen was handed to them are fading fast. Telehealth for dry eye care has exploded, too, with initial consultations and follow-ups happening from the comfort of patients' homes. People simply stick with treatments that fit into their lives without hassle—and abandon those that don't. This convenience factor is opening up market opportunities well beyond traditional medical settings. Remember how Lifitegrast (Xiidra) established itself for dry eye treatment. The next competitive edge isn't just developing effective eye drops—it's making them incredibly easy to get and use. Companies that get this aren't just adding convenience as a bonus feature; they're building their entire approach around it. And they're the ones grabbing bigger slices of this competitive market.

Dry Eye Disease Market Trends

Growing Crisis: The Expanding Impact of Dry Eye Disease

Dry eye disease has grown from a simple clinical issue into a significant public health challenge in many countries. In the United States alone, this condition affects more than 38 million Americans, with about nine in ten patients experiencing the evaporative form. This high number of cases has put pressure on healthcare systems while creating new opportunities for companies that can provide effective and affordable treatment solutions. For healthcare providers and pharmaceutical companies, this means focusing on complete care solutions rather than individual products—combining diagnosis, treatment, and ongoing care into streamlined patient programs. The effects of this growing patient population are changing workforce needs in eye care. Recent analysis of United States Department of Health and Human Services data shows that demand for ophthalmologists will increase by 5,150 full-time positions—a 24% increase from 2020 to 2035—which will worsen the already existing shortage of eye care specialists. This workforce gap creates an urgent need for better diagnostic tools, automated screening, and care models that don't require a specialist for every patient with dry eye syndrome. Companies that develop solutions to optimize the workforce can gain market advantage while helping solve a critical healthcare access problem.

Innovation Breakthrough: New Technologies Transforming Dry Eye Diagnosis and Care

Diagnosis of dry eye disease is moving from simply asking about symptoms to using precise measurements that enable targeted treatments. New clinical tools are showing real improvements in patient outcomes, as seen in a phase 2 trial for AZR-MD-001 that showed significant improvements in meibomian gland function and ocular surface health. The technology not only improved clinical measures but also provided practical benefits, with contact lens wearers able to wear their lenses up to 192 minutes longer—a real-world improvement that patients notice in their daily lives. For companies in this field, this means successful products must deliver both clinical results and everyday benefits that patients can clearly recognize. Advanced diagnostic tools are creating new treatment possibilities by allowing early detection and personalized therapy. These tools are especially valuable for challenging cases such as contact lens wearers, patients who've had eye surgery, and those with autoimmune-related dry eye syndrome. By providing detailed information about the specific causes of each patient's condition, these tools help doctors match treatments to individual needs rather than using a one-size-fits-all approach. Leading manufacturers are now building diagnostic features directly into their treatment systems, creating integrated solutions that can measure how well treatment is working and adjust accordingly—potentially improving outcomes while reducing the time doctors need to spend managing each case.

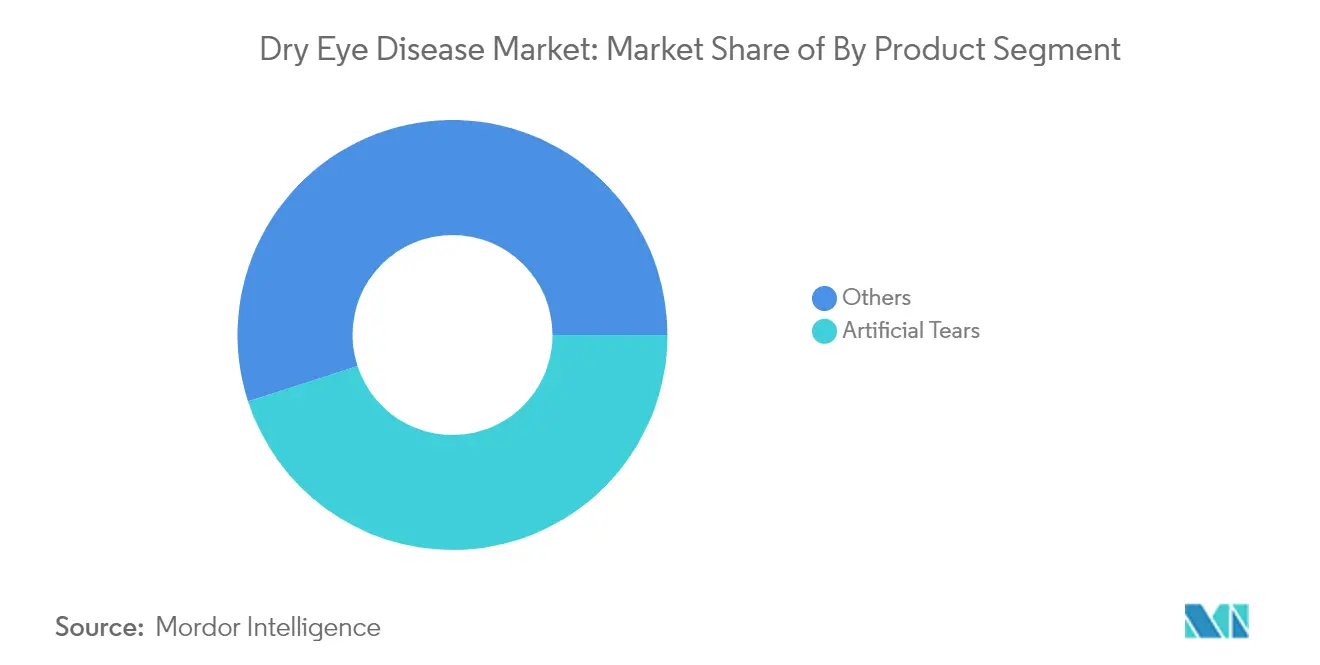

Segment Analysis: By Product

Anti-inflammatory Powerhouses: The Dominant & Fast-Growing Force

Anti-inflammatory drugs have established themselves as the cornerstone of dry eye disease treatment, commanding 37.9% of the market in 2025. These medications address the underlying inflammation that drives chronic dry eye symptoms rather than just providing temporary relief. Cyclosporine formulations, in particular, have proven effective in restoring natural tear production. The segment is even more notable is its growth rate—advancing at 18.74% CAGR, far outpacing other treatments. Recent regulatory approvals, expanded uses, and new delivery methods have accelerated market adoption, creating opportunities for previously underserved patients. The key takeaway is clear: pharmaceutical companies with strong anti-inflammatory portfolios and active development in this area are best positioned to capture value in the dry eye disease market.

Beyond Inflammation: The Diverse Ecosystem of Complementary Treatments

Beyond anti-inflammatories, the dry eye market includes a diverse range of complementary approaches addressing different aspects of the condition. Artificial tears remain a foundation of initial therapy, with innovations focused on better retention and compatibility. Products like the ADVALUBE PG formulation, with its precise 0.4% Polyethylene Glycol and 0.3% Propylene Glycol composition, demonstrate the attention to detail in premium offerings. Punctal plugs offer a device-based solution for tear retention, particularly valuable for patients with aqueous-deficient dry eye who don't respond well to topical treatments. Secretagogues work by stimulating natural tear production, while technologies like the Moist Heat Mask, which provides precisely 10 minutes of thermal therapy, specifically target meibomian gland dysfunction. This diversity highlights an important reality: successful companies need expertise across multiple treatment approaches to address the varied nature of dry eye disease and provide personalized care based on specific patient needs.

Segment Analysis: By Distribution Channel

Community Trust Centers: Why Retail Pharmacies Lead the Way

Independent pharmacies and drug stores dominate the distribution landscape for dry eye syndrome treatment, controlling 52.2% of the market in 2025. Their strength comes from combining easy access with personal consultation—a powerful combination for managing chronic conditions like dry eye disease. These community outlets excel at building patient relationships through face-to-face interactions, allowing pharmacists to recommend specific products based on individual symptoms and treatment history. Products with patient-friendly features, such as the HYLO delivery system that provides 300 preservative-free drops with extended sterility, find strong support in this channel. For manufacturers, the message is clear: developing strong relationships with independent pharmacies through education programs, streamlined inventory systems, and pharmacy-exclusive products offers the most direct path to market success in the dry eye treatment space.

Digital Revolution: Online Pharmacies' Rapid Rise

Online pharmacies have emerged as the growth engine for dry eye syndrome distribution, expanding at 10.41% CAGR. This rapid growth reflects changing consumer buying habits, with more patients comfortable managing chronic conditions through digital platforms. The appeal goes beyond convenience, including price comparison, automatic refills, and access to specialized formulations that local stores might not carry. Digital platforms excel at using patient data to create personalized recommendations and reminder programs that improve outcomes and build loyalty. Products designed with extended stability, such as preservative-free formulations that stay sterile for over three months, are particularly well-suited for e-commerce. For manufacturers, this means adapting: optimizing packaging for shipping, creating digital education materials, and building direct-to-consumer engagement capabilities, which have become essential for capturing growth in the evolving dry eye market.

Clinical Gateways: Hospital Pharmacies' Strategic Role

Hospital pharmacies play a specialized but influential role in the dry eye disease treatment landscape, serving as entry points for advanced therapies and newly diagnosed patients. Their connection with ophthalmology departments creates unique opportunities for introducing sophisticated treatments immediately after diagnosis or procedures when patients are most receptive to new therapies. These settings are well-equipped to handle complex formulations and devices that require detailed education or special storage. The clinical environment also enables important feedback between doctors and pharmacists, allowing for quick adjustments to treatment plans. The standard 10mL packaging format common in professionally dispensed eye drops shows how products are often designed with institutional settings in mind. For manufacturers, success in this channel requires a different approach focused on clinical evidence, key opinion leader relationships, and integration into institutional protocols rather than consumer marketing. Companies that develop specialized hospital teams with eye care expertise can establish their products at the critical initial treatment stage, creating prescription patterns that often continue as patients move to community-based care.

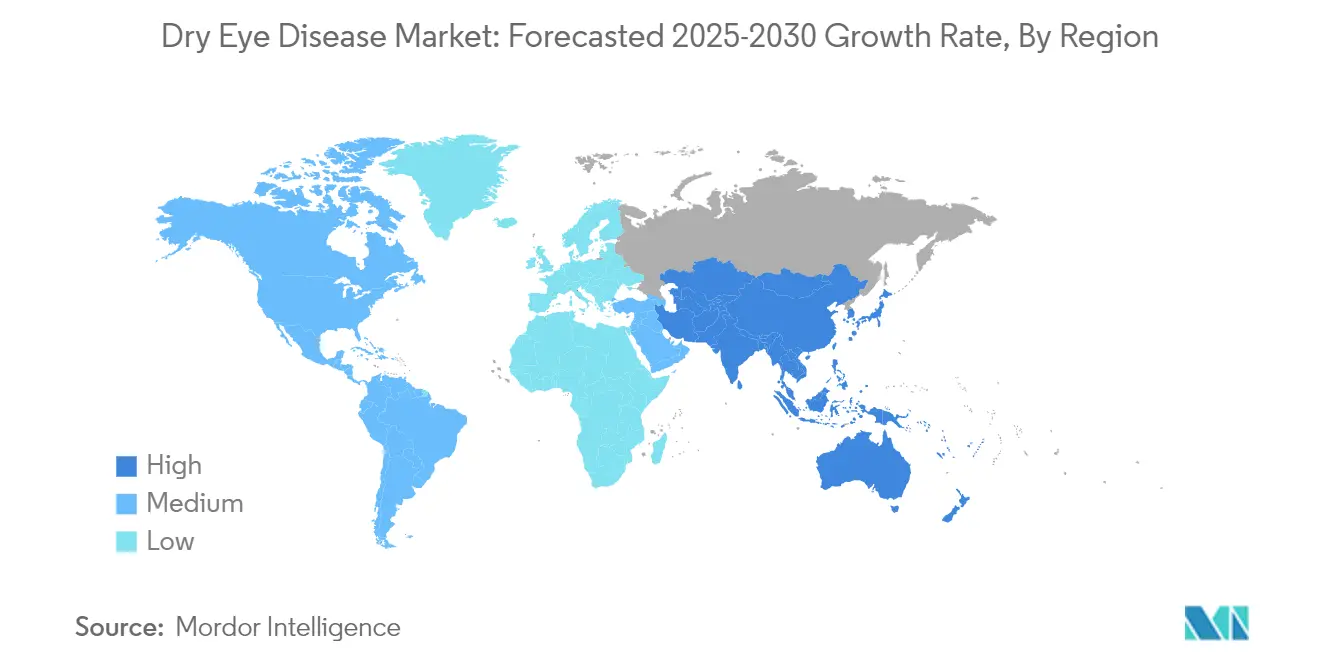

Geography Analysis

North America: Leading the Charge in Dry Eye Innovation

North America is the dominant region in the dry eye disease market, with a 73.2% share in 2025. The region's leadership stems from high disease prevalence, strong healthcare infrastructure, and substantial R&D investments. The FDA plays a crucial role in advancing treatments, with companies focusing on innovative therapies and improved delivery systems. This market dominance creates a competitive landscape where pharmaceutical companies must differentiate through either clinical efficacy advantages or patient access programs to capture market share. Healthcare providers in this region increasingly adopt comprehensive approaches that address both symptoms and underlying causes of dry eye disease.

United States: Where Market Leadership Meets Innovation

The United States dominates the North American dry eye disease market, accounting for the most significant market share percentage in the region. High disease awareness, substantial insurance coverage, and quick adoption of new treatments drive this leadership position. The regulatory environment continues to support innovation, as seen with the FDA's review timeline for Aldeyra Therapeutics' reproxalap, a first-in-class treatment for dry eye symptoms. Market access strategies have evolved to prioritize patient affordability, with programs like MIEBO's offering eligible commercial patients copays as low as USD 0. For companies looking to succeed in this competitive landscape, combining clinical innovation with patient-centered access programs has become essential for gaining and maintaining market share.

Mexico: The Emerging Growth Story

Mexico represents the fastest-growing segment within the North American dry eye disease region, with the highest CAGR percentage. This growth comes from expanding healthcare access, increasing screen time among urban populations, and raising awareness about eye health. International pharmaceutical companies are extending their reach through local partnerships and distribution networks. The market is seeing increased adoption of both prescription and over-the-counter solutions, with pricing strategies adjusted to fit the local economy. Mexico's emerging role as a medical tourism destination for specialized eye care is creating new opportunities for market expansion and innovative service delivery models that bridge traditional treatment gaps.

Canada: Balanced Approach to Dry Eye Management

Canada's dry eye syndrome treatment market offers a balanced approach between the innovation-focused U.S. market and Mexico's rapidly evolving landscape. The public healthcare system provides stable treatment access, while private insurance covers specialized therapies. Canadian healthcare providers increasingly use integrated care models combining pharmaceuticals, devices, and lifestyle modifications. Market strategies often focus on education campaigns targeting both providers and patients, emphasizing early intervention. The country's cold, dry climate in many regions naturally predisposes residents to dry eye symptoms, creating consistent year-round demand rather than the seasonal patterns seen elsewhere. This environmental factor has prompted healthcare systems to develop specialized protocols for managing climate-associated ocular surface conditions.

Europe: Strategic Innovation Within Cost Constraints

Europe represents a critical market in the dry eye disease treatment landscape, with healthcare systems that emphasize cost-effective treatments. The aging population and increasing screen time drive market growth, with treatments like Evotears priced at approximately EURO 30 for a one-month supply. European regulators typically require robust long-term efficacy data, shaping how products are developed and marketed. The region increasingly incorporates lifestyle and environmental factors into treatment approaches, creating opportunities for comprehensive management protocols. Research institutions across Europe continue to advance the understanding of ocular surface diseases, establishing partnerships that connect academic research with commercial applications.

Germany: Research Excellence Driving Market Leadership

Germany holds the most significant market share percentage within the European dry eye disease market, serving as the foundation of regional development. This leadership position comes from a strong healthcare infrastructure, favorable reimbursement policies, and significant pharmaceutical manufacturing capabilities. German clinical research excellence is demonstrated by studies like the VEVYE trial that enrolled 1,369 patients with dry eye disease. Medical practitioners in Germany have pioneered integrated treatment approaches combining pharmaceutical and device-based therapies. The comprehensive healthcare coverage for dry eye treatments reduces financial barriers for patients, driving higher treatment rates and creating a model market for new product introductions.

United Kingdom: Post-Brexit Acceleration

The United Kingdom represents the fastest-growing segment within the European dry eye syndrome market, recording the highest CAGR percentage. This growth coincides with NHS efforts to reimagine approaches to chronic eye conditions, with greater emphasis on early intervention. The United Kingdom market is expanding through increased awareness and more diverse access channels beyond traditional prescriptions. Digital health solutions are gaining traction, with telemedicine platforms offering remote diagnosis and treatment recommendations. The post-Brexit regulatory environment has created the potential for faster approval of innovative treatments, potentially reducing time-to-market. United Kingdom research institutions are advancing the understanding of how environmental and lifestyle factors affect dry eye prevalence, informing more targeted treatment approaches.

Rest of Europe: Diverse Healthcare Systems, Unified Challenges

The remaining European countries form a diverse dry eye syndrome treatment market landscape, each with unique healthcare approaches. France emphasizes pharmaceutical solutions with strong reimbursement policies for prescribed treatments. Italy shows a growing preference for preservative-free formulations, reflecting concerns about long-term ocular surface health. Spain has increased the adoption of advanced diagnostic technologies that enable more targeted treatment approaches. Distribution channels vary across the region, with different levels of pharmacist autonomy affecting how products reach patients. These markets share a growing trend toward integrated treatment protocols that combine pharmaceuticals, devices, and environmental modifications, recognizing dry eye disease's complex nature and the need for personalized treatment strategies.

Asia-Pacific: Where Growth Meets Opportunity

The Asia-Pacific region represents the fastest-growing territory in the global dry eye disease market, advancing at a CAGR of approximately 5.74%. This growth comes from multiple factors: rapid urbanization, increasing screen time, worsening air quality in cities, and aging populations in developed economies like Japan and South Korea. The region presents an interesting contrast of high-risk factors alongside historically lower diagnosis rates. Clinical research is expanding rapidly, as shown by studies in India where rebamipide ophthalmic suspension demonstrated 68.75% improvement in severe dry eye symptoms compared to 28.57% in control groups. Companies entering this market need strategies that address the unique combination of economic factors, healthcare infrastructure limitations, and cultural approaches to eye care.

Middle East and Africa: Unique Challenges, Custom Solutions

The Middle East and Africa region presents a complex landscape in the dry eye disease market, with stark contrasts in healthcare infrastructure and treatment access. The arid conditions throughout much of the Middle East naturally increase the risk for dry eye symptoms, yet diagnosis and treatment rates have traditionally lagged behind other regions. GCC countries are driving regional growth through healthcare investments, specialized eye care centers, and improved insurance coverage for ocular treatments. Many parts of Africa face fundamental healthcare access challenges, creating opportunities for simplified treatment options and innovative distribution approaches. The region's diverse climates and genetic factors contribute to unique presentation patterns of dry eye disease, often requiring tailored therapeutic strategies that consider local conditions and resource availability.

South America: Building Momentum Through Accessibility

South America shows balanced development in the dry eye syndrome market, with significant urban-rural gaps in disease awareness and treatment access. Brazil leads the region with its healthcare system, increasingly recognizing dry eye disease as a priority condition. The tropical climate creates unique challenges compared to the temperate areas, affecting both symptom patterns and treatment adherence. South American markets have shown strong interest in combination therapies that address multiple aspects of dry eye pathophysiology. Generic medications play a more significant role here than in other regions, making competitive pricing crucial for market success. Healthcare providers are increasingly adopting standardized diagnostic criteria, improving identification rates, and creating more consistent treatment pathways for patients across diverse geographic and economic settings.

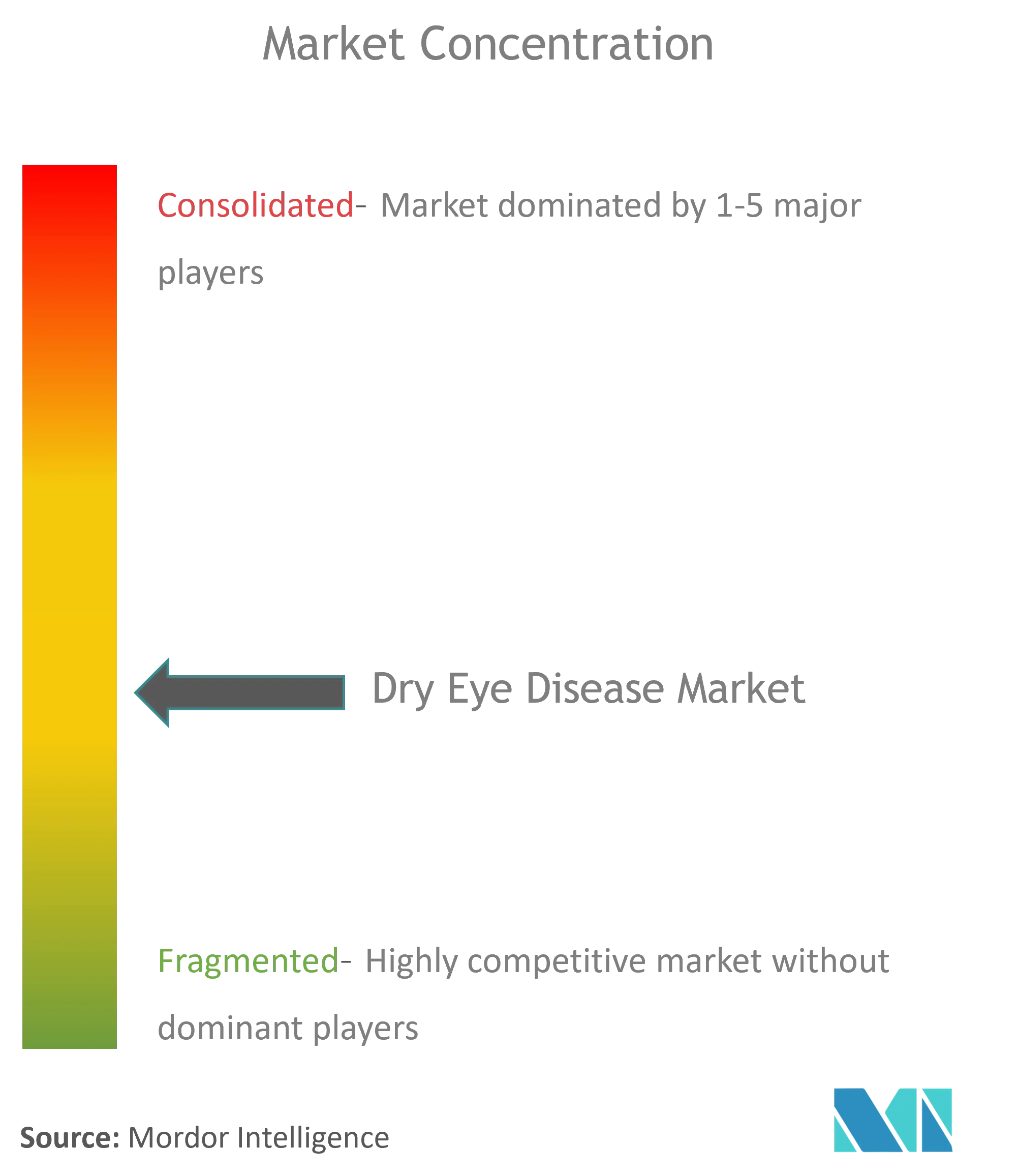

Dry Eye Disease Industry Overview

Innovation Arms Race: R&D Investment Reshaping Competitive Hierarchies

In the dry eye disease market, companies are now competing through focused R&D investments rather than just battling for market share. This approach is evident in the anti-inflammatory drugs segment, which leads with 37.9% of the market while growing at an impressive 18.74% annually. Bausch + Lomb showed the power of this strategy when they secured FDA approval for MIEBO in 2023, backed by strong results from two Phase 3 clinical trials. Other major players like AbbVie and Novartis are following suit by developing targeted treatments for specific dry eye disease mechanisms instead of creating me-too products. This innovation focus lets companies charge premium prices and creates barriers that smaller competitors struggle to overcome. Companies that invest in novel delivery systems and treatments that work in multiple ways will win favor, with both doctors looking for better results and insurers willing to pay for treatments that actually work better.

Channel Champions: Distribution Strategy as a Competitive Edge

Beyond having great products, success in the dry eye syndrome treatment market now depends heavily on innovative distribution strategies. While traditional pharmacies still dominate with 52.2% of distribution, forward-thinking companies are expanding into online channels that are growing at 10.41% annually—almost twice as fast as the overall market. Johnson & Johnson and Santen Pharmaceutical are leading this change by creating seamless experiences that combine virtual doctor visits with home delivery options. This approach recognizes a key market truth: for chronic conditions requiring ongoing treatment, how patients access medication matters as much as the medication itself. Companies in the severe dry eye market that build strong relationships with patients through direct education and specialized pharmacy partnerships gain a lasting advantage. The winners will be those who perfect their distribution networks while gathering valuable real-world data on how patients actually use their products.

Regional Playbooks: Adapting Strategies to Geographic Realities

The dry eye syndrome market shows significant geographic differences that create strategic opportunities for adaptable companies. While North America holds 73.2% of the market, Asia-Pacific's 5.74% growth rate points to untapped potential that requires customized approaches. Smart players like Alcon and Sun Pharmaceutical are creating region-specific pricing and products that address unique environmental factors in high-potential markets like China and India. This approach recognizes a practical reality: increasing screen time, pollution, and aging populations in developing regions are creating new dry eye disease patients with different needs and expectations. Companies that build local manufacturing, regulatory expertise, and distribution partnerships will gain early advantages in these growing markets. Success in the global dry eye market size competition will come to companies that empower regional teams to make quick decisions based on local conditions rather than forcing one-size-fits-all strategies across different healthcare systems.

Dry Eye Disease Market Leaders

-

Santen Pharmaceutical Co. Ltd

-

OASIS Medical

-

Alcon Inc.

-

Bausch Health Companies Inc.

-

AbbVie Inc. (Allergan PLC)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Dry Eye Disease Market News

- October 2022: Aldeyra Therapeutics, Inc. completed the phase 3 clinical trial of 0.25% reproxalap ophthalmic solution, an investigational new drug candidate, for treating allergic conjunctivitis. The company presented the clinical data from the trial at the American Academy of Optometry 2022 Annual Meeting.

- January 2022: NovaBay Pharmaceuticals launched Avenova lubricating eye drops to treat dry eye symptoms.

Dry Eye Disease Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Rising Burden of Dry Eye Disease

- 4.2.2 Technological Advancements and Emergence of Novel Diagnostic Tools

-

4.3 Market Restraints

- 4.3.1 High Cost of Specialty Dry Eye Products with Complex Reimbursement Scenario

- 4.3.2 Availability of Alternative Therapies

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Product

- 5.1.1 Artificial Tears

- 5.1.2 Anti-inflammatory Drugs

- 5.1.2.1 Cyclosporine

- 5.1.2.2 Corticosteroid

- 5.1.2.3 Other Anti-inflammatory Drugs

- 5.1.3 Punctal Plugs

- 5.1.4 Secretagogues

- 5.1.5 Other Products

-

5.2 By Distribution Channel

- 5.2.1 Hospital Pharmacies

- 5.2.2 Independent Pharmacies and Drug Stores

- 5.2.3 Online Pharmacies

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 AbbVie Inc. (Allergan PLC)

- 6.1.2 AFT Pharmaceuticals

- 6.1.3 Akorn

- 6.1.4 Alcon Inc.

- 6.1.5 Bausch Health Companies Inc.

- 6.1.6 Horus Pharma

- 6.1.7 Johnson & Johnson

- 6.1.8 Mitotech

- 6.1.9 Novaliq GmbH

- 6.1.10 OASIS Medical

- 6.1.11 Otsuka Pharmaceutical Co. Ltd

- 6.1.12 Prestige Consumer Healthcare

- 6.1.13 Santen Pharmaceutical Co. Ltd

- 6.1.14 Sentiss Pharma Pvt. Ltd

- 6.1.15 Sun Pharmaceutical Industries Ltd

- 6.1.16 VISUfarma

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Dry Eye Disease Industry Segmentation

As per the scope of the report, dry eye disease refers to the disturbance of the lacrimal functional unit, which comprises the lacrimal glands, ocular surface (cornea, conjunctiva, and meibomian glands), and lids, along with the sensory and motor nerves that connect them. The Dry Eye Disease Market is Segmented by Product, Artificial Tears, Anti-inflammatory Drugs (Cyclosporine, Corticosteroid, and Other Anti-inflammatory Drugs), Punctal Plugs, Secretagogues, and Other Products, Distribution Channels (Hospital Pharmacies, Independent Pharmacies, and Drug Stores, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). Several dry eye treatment products are used for various ocular manifestations. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD million for the above segments.

| By Product | Artificial Tears | ||

| Anti-inflammatory Drugs | Cyclosporine | ||

| Corticosteroid | |||

| Other Anti-inflammatory Drugs | |||

| Punctal Plugs | |||

| Secretagogues | |||

| Other Products | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Independent Pharmacies and Drug Stores | |||

| Online Pharmacies | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Dry Eye Disease Market Research Faqs

How big is the Dry Eye Disease Market?

The Dry Eye Disease Market size is expected to reach USD 6.36 billion in 2025 and grow at a CAGR of 4.09% to reach USD 7.77 billion by 2030.

What is the current Dry Eye Disease Market size?

In 2025, the Dry Eye Disease Market size is expected to reach USD 6.36 billion.

Which is the fastest growing region in Dry Eye Disease Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Dry Eye Disease Market?

In 2025, the North America accounts for the largest market share in Dry Eye Disease Market.

What years does this Dry Eye Disease Market cover, and what was the market size in 2024?

In 2024, the Dry Eye Disease Market size was estimated at USD 6.10 billion. The report covers the Dry Eye Disease Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Dry Eye Disease Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Dry Eye Disease Industry Report

The Global Intellectual Property Management Software Market Report is segmented by deployment, solution, type, end-user industry, and geography, providing a comprehensive market analysis. The market is driven by the increasing volume of patents, trademarks, and copyrights, necessitating efficient management solutions. Cloud deployments and the IT & telecom sector are pivotal in market expansion. The rising demand for streamlined administrative processes and strict enforcement of intellectual property laws are key growth drivers. However, the market faces challenges such as the complexity of global intellectual property laws and high initial costs.

The Asia Pacific region, led by technological innovations and a high number of filings, is a major contributor to the market's expansion. Market trends indicate a shift towards collaborations and strategic partnerships to enhance software functionality and user experience, addressing the diverse legal needs across different regions. The intellectual property market size is set to expand, with software solutions playing a crucial role in managing and protecting intellectual property assets efficiently.

For detailed statistics on the intellectual property management software market share, size, and revenue growth rate, consult the Mordor Intelligence™ Industry Reports. Get a comprehensive market forecast outlook and historical overview by downloading a free report PDF sample from their website. This industry analysis highlights the importance of market trends, industry overview, and market research in understanding the market value and market segmentation. The market report provides insights into market growth, market data, and market review, helping identify market leaders and industry statistics. The industry reports and research companies offer an in-depth industry outlook and market predictions essential for understanding industry size and industry sales.