Document Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

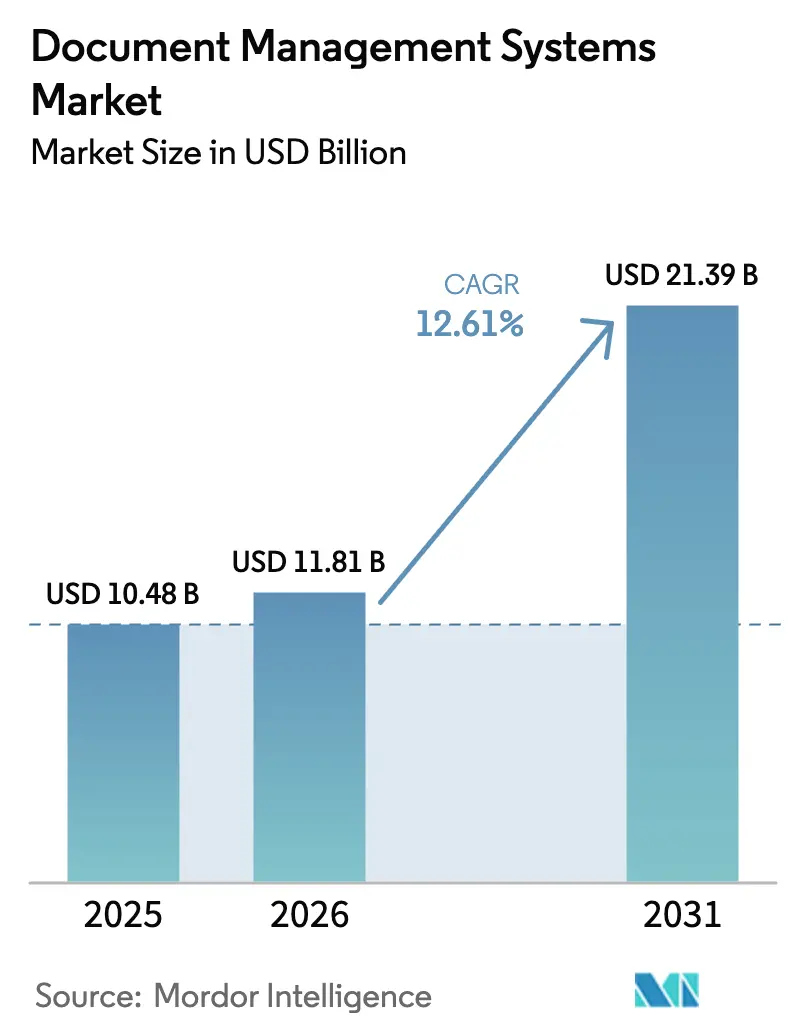

| Market Size (2026) | USD 11.81 Billion |

| Market Size (2031) | USD 21.39 Billion |

| Growth Rate (2026 - 2031) | 12.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Document Management Systems Market Analysis by Mordor Intelligence

The Document Management Systems Market size is projected to expand from USD 10.48 billion in 2025 and USD 11.81 billion in 2026 to USD 21.39 billion by 2031, registering a CAGR of 12.61% between 2026 to 2031. Rapid growth stems from enterprises retiring legacy repositories in favor of cloud-native platforms that embed AI copilots inside everyday collaboration tools. At the same time, data-sovereignty laws in Europe and Asia Pacific obligate vendors to stand up in-region hosting with end-to-end encryption, broadening the customer base even as it fragments infrastructure footprints. Competitive heat is intensifying as hyperscalers bundle storage into collaboration suites, compressing standalone software pricing and steering pure-play providers toward vertical templates that slash deployment time. Buyers overwhelmingly favor cloud deployment for elastic capacity and automatic upgrades, yet air-gapped on-premise systems endure in defense and other sovereign sectors.

Key Report Takeaways

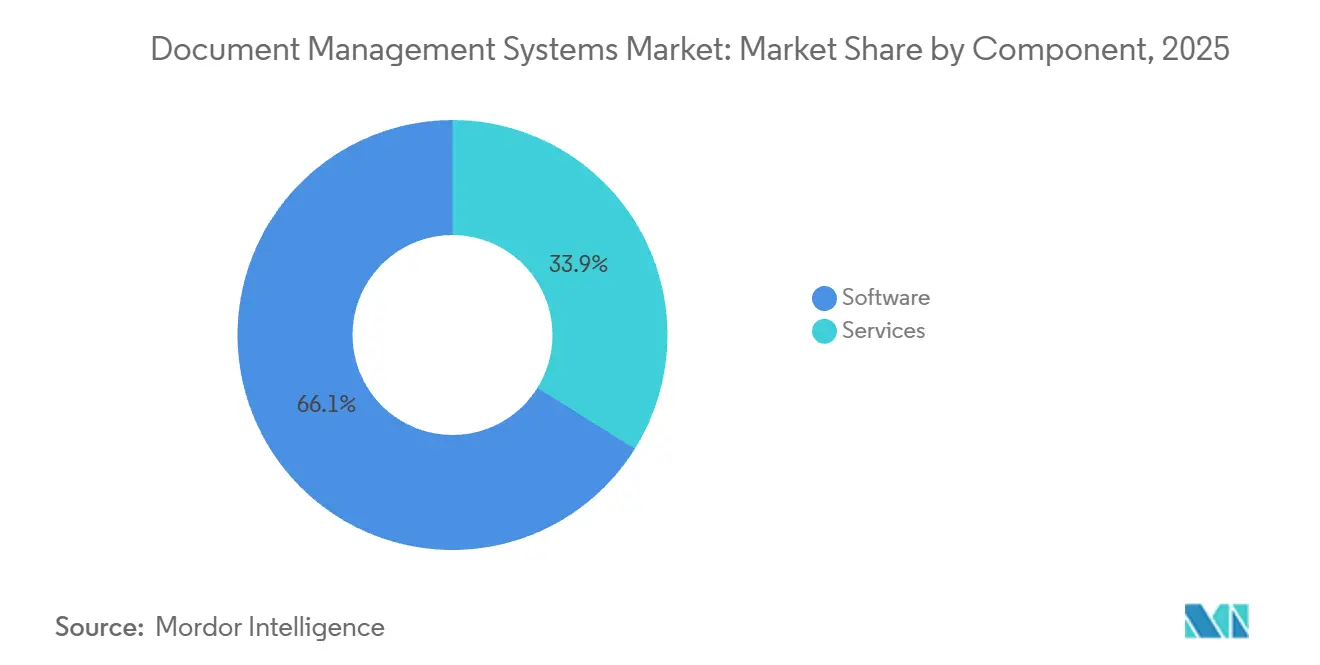

- By component, software licenses held a 66.12% market share in document management systems in 2025, while services are set to expand at a 17.21% CAGR to 2031.

- By deployment mode, cloud captured 70.34% of 2025 revenue and is advancing at an 18.34% CAGR, far outpacing on-premise installations.

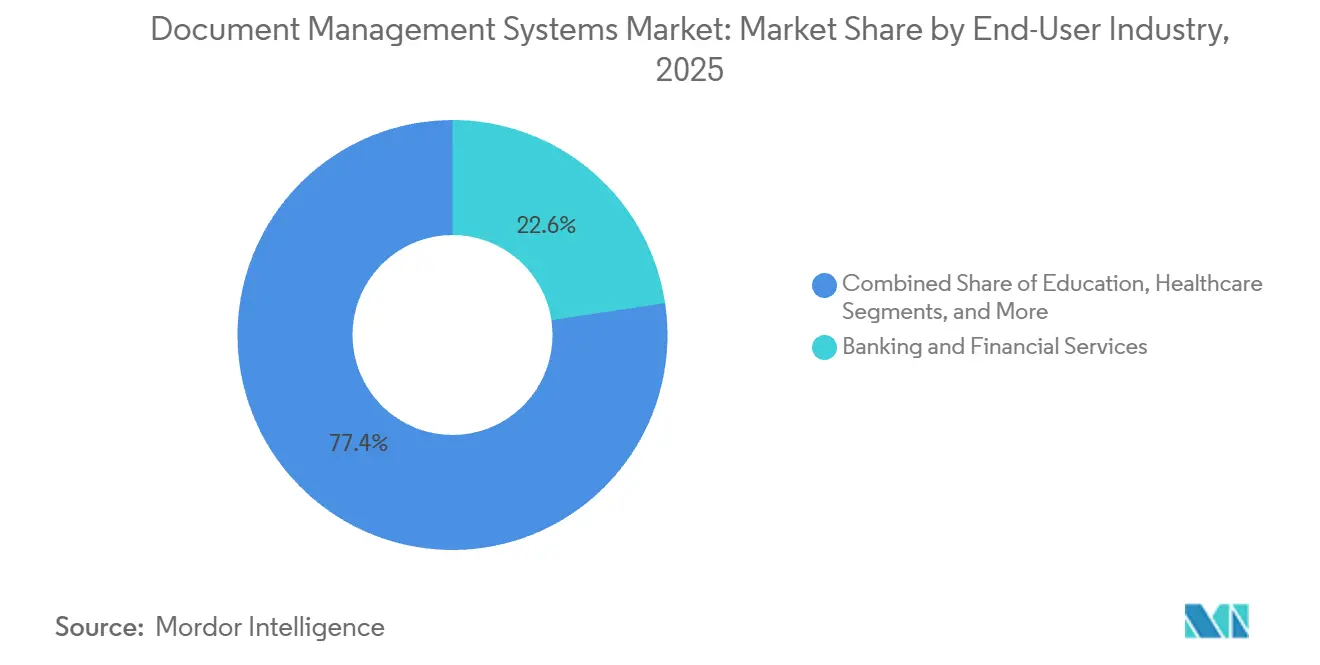

- By end-user industry, banking and financial services led with 22.63% revenue share in 2025, whereas healthcare is forecast to rise at a 17.69% CAGR through 2031.

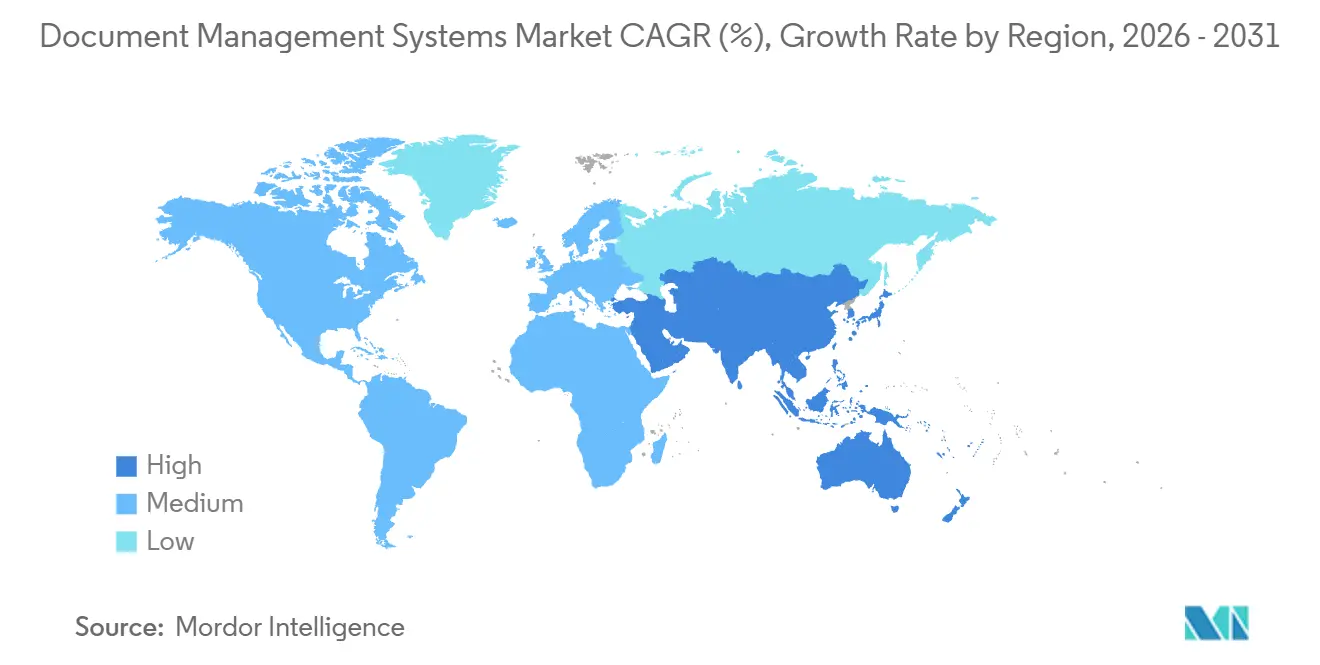

- By geography, North America commanded 37.53% of the document management systems market size in 2025, whereas Asia Pacific is expected to post the highest regional CAGR of 18.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Document Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Paper-Free Processes | +2.8% | Global, with early momentum in North America and Europe | Medium term (2-4 years) |

| Cloud-Native DMS Platforms Bundled Inside Collaboration Suites | +3.1% | North America and Europe core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Surge in AI-Enhanced Search and Auto-Classification Accuracy | +2.4% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Strict Data-Sovereignty Rules Driving Compliant Roll-Outs | +2.6% | Europe (GDPR), Asia Pacific (China, India), Middle East | Long term (≥ 4 years) |

| Rise of Industry-Specific Templates Shortening Deployment Cycles | +2.2% | Global, with vertical concentration in BFSI, Healthcare, Manufacturing | Medium term (2-4 years) |

| Generative-AI Copilots Unlocking Content-in-Context Workflows | +2.3% | North America and Europe early adopters, Asia Pacific following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Paper-Free Processes

Government mandates are accelerating digital conversion far faster than voluntary sustainability initiatives. The U.S. National Archives requires every federal agency to digitize permanent records by December 2026.[1]First-name Last-name, “Electronic Records Archives 2.0,” National Archives and Records Administration, archives.gov Japan’s Digital Agency ordered all prefectures to adopt paperless workflows by April 2025, triggering a 35% jump in procurements. Canon processed 18 billion pages through its cloud-scanning service in 2025, up 22% from 2024, illustrating the flood of analog content entering repositories. Rising capture volumes trim storage costs but inflate metadata-tagging labor, a trade-off that favors AI-driven auto-classification over manual indexing. Enterprises therefore prioritize platforms with built-in machine-learning enrichers that satisfy compliance while slashing operating expense.

Cloud-Native DMS Platforms Bundled Inside Collaboration Suites

Hyperscalers now embed repositories directly in collaboration tools, bypassing lengthy procurement. Microsoft launched SharePoint Embedded in March 2024; by January 2025, more than 200 ISVs had adopted the service. Box deepened integration with Google Workspace in June 2025, and pilot clients recorded 40% fewer version-control errors. Bundled offerings command 15-20% price premiums because they deliver seamless interoperability, forcing pure-play vendors to compete on vertical depth rather than horizontal features.

Surge in AI-Enhanced Search and Auto-Classification Accuracy

Large language models now cut metadata entry labor by up to 70%, yet regulated sectors still demand near-perfect precision. Microsoft 365 Copilot trimmed manual tagging by 65% for 500 pilot enterprises. IBM’s partnership with Unstructured.io pushed domain-specific accuracy to 97%, narrowing the gap to compliance thresholds.[2]First-name Last-name, “Content Assistant Partnership,” IBM Corporation, ibm.com Most organizations run hybrid workflows where AI proposes tags and humans approve them, balancing productivity gains with risk controls.

Strict Data-Sovereignty Rules Driving Compliant Roll-Outs

The European Union’s Data Governance Act prohibits most cross-border transfers of public-sector data. China’s Personal Information Protection Law imposes similar constraints on critical-infrastructure operators. Anticipated Indian legislation is expected to follow suit. Hyperscalers can absorb the capital cost of multiple regional clouds, but mid-tier vendors must partner locally or exit, splitting the market between global platforms and single-country specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent User-Change Resistance in Regulated Back-Office Functions | -1.4% | Global, acute in Europe and North America legacy enterprises | Medium term (2-4 years) |

| High E-Discovery Costs From Poor Metadata Hygiene | -1.2% | North America and Europe litigation-intensive sectors | Long term (≥ 4 years) |

| Cyber-Insurance Premiums Rising After DMS-Centred Ransomware Events | -0.9% | Global, concentrated in Healthcare and BFSI | Short term (≤ 2 years) |

| Vendor Lock-In Concerns Slowing Migration From Legacy ECMs | -1.1% | Global, particularly North America and Europe mid-market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent User-Change Resistance in Regulated Back-Office Functions

Deloitte found that 38% of financial-services compliance staff still print filings for manual review, doubting the evidentiary strength of digital signatures. Civil-law jurisdictions that require notarized deeds maintain hybrid processes, prolonging change-management programs to two years and inflating training budgets to USD 0.5-2 million per enterprise. Resistance delays ROI and moderates cloud-migration momentum.

High E-Discovery Costs From Poor Metadata Hygiene

Thomson Reuters valued U.S. e-discovery at USD 18,000 per gigabyte in 2024. A Fortune 500 manufacturer spent USD 12 million reviewing 8 terabytes for one dispute, a burden attributable to untagged legacy files. AI enrichment tools promise relief, but retrofitting tags to petabyte-scale archives remains a multi-year endeavor that tempers immediate savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| User-change resistance in regulated functions | -1.70% | Global; higher in traditional industries | Medium term (2-4 years) |

| High e-discovery costs from poor metadata | -1.20% | North America, Europe | Short term (≤ 2 years) |

| Rising cyber-insurance premiums post-ransomware | -0.90% | Global; higher in North America and Europe | Medium term (2-4 years) |

| Vendor lock-in concerns | -1.10% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Edge Ahead as Complexity Escalates

Services are growing at a 17.21% CAGR because migration complexity, AI tuning, and compliance mapping outstrip in-house skills. KnowledgeLake migrated 450 million federal documents to SharePoint Online in six weeks, remapping retention policies on the fly. EY and Adobe deliver Basel III audit trails in only 12 weeks through a bundled advisory and e-signature package. Software licenses held a 66.12% market share in 2025. Software remains indispensable, yet license fees fall 10-15% annually under hyperscaler price pressure.

As buyers seek turnkey outcomes, vendors with strong consulting arms, such as IBM, Hyland, and OpenText, capture stickier revenue. Managed services likewise appeal to mid-market firms lacking 24-hour IT coverage; DocuWare’s cloud service bundles backup and patching to cut the total cost of ownership by 30%. Consequently, the document management systems market size for services is expanding faster than license revenue and reshaping vendor business models.

By Deployment Mode: Cloud Dominates, Hybrid Gains Regulatory Traction

Cloud deployments generated 70.34% of 2025 revenue and are advancing at 18.34% through 2031, propelled by elastic storage and continuous feature releases. Azure-hosted SharePoint processed more than 1 trillion files in 2025, showcasing scale that on-premise systems struggle to match. Enterprises also value built-in disaster recovery and global accessibility, especially for distributed teams. Still, sovereign sectors retain on-premise instances for air-gapped networks, sustaining a sizable legacy footprint.

Hybrid is emerging as a compliance bridge. Hyland’s OnBase Hybrid Cloud synchronizes metadata to Azure for AI search while holding binaries on customer servers, satisfying data-residency laws without sacrificing modern features. Similar architectures are poised to spread across defense, healthcare, and public-sector accounts, ensuring the document management systems market continues to accommodate multiple deployment choices.

By End-User Industry: Healthcare Accelerates on Telehealth Mandates

Banking and financial services commanded 22.63% revenue in 2025, driven by know-your-customer, anti-money-laundering, and Basel III reporting. However, healthcare is on track to be the fastest-growing vertical at a 17.69% CAGR, propelled by telehealth expansion and electronic health record integration. The Centers for Medicare and Medicaid Services link reimbursements to digital interoperability, pushing hospitals to embed repositories inside Epic and Cerner workflows. Consequently, the document management systems market size tied to healthcare use cases is projected to double in five years.

Manufacturing, construction, education, and retail are also scaling adoption. Autodesk’s ISO 19650-certified template shortens BIM documentation from nine months to six weeks, while Walmart processes 500,000 supplier invoices weekly through an AI-enabled repository. Such vertical depth illustrates how domain-specific templates unlock new budget pools and reduce deployment risk across diverse industries.

Geography Analysis

North America delivered 37.53% of 2025 revenue, helped by U.S. federal digitization deadlines and a Canadian directive that all federal departments move to cloud repositories by March 2027. High Microsoft 365 penetration speeds deployment, yet growth moderates as enterprises stretch platform life cycles and focus on AI add-ons rather than replacements.

Asia Pacific will grow at 18.43% through 2031. India’s Digital India program earmarked INR 14,903 crore (USD 1.8 billion) for e-governance in its 2025-2026 budget.[3]First-name Last-name, “Digital India Programme,” Government of India, digitalindia.gov.in China’s Digital Silk Road funds state-enterprise deployments to standardize cross-border trade documents. Japan mandated paperless prefectures by April 2025, spurring a 35% order increase. Australia’s amended Privacy Act requires breach notification within 72 hours, pushing organizations toward real-time audit trails.

Europe, the Middle East, and Africa form a patchwork shaped by GDPR and localization rules. The EU Data Governance Act obliges vendors to run regional data centers. Germany’s cybersecurity agency advises on-premise or hybrid deployments for critical infrastructure. Gulf smart-city programs such as Dubai Smart 2030 embed repositories into e-government services. South Africa’s POPIA drives banks and telecoms toward consent-managed archives.

Competitive Landscape

The document management systems market is moderately concentrated, with the top five suppliers controlling 45% of 2025 revenue. Microsoft leverages Teams and SharePoint to embed repositories in day-to-day workflows; over 200 ISVs integrated SharePoint Embedded within a year of launch, widening Microsoft’s reach into vertical software. Box defends share by offering multi-cloud flexibility across AWS, Google Cloud, and IBM Cloud, appealing to organizations wary of single-vendor lock-in.

Adobe partners with EY to bundle Acrobat Sign with compliance advisory, giving regulated banks a turnkey path to Basel III documentation. OpenText’s Micro Focus acquisition enlarged its portfolio but stretched integration resources, allowing nimble rivals such as M-Files and Laserfiche to win mid-market deals. Vertical specialists enhance differentiation: Autodesk dominates construction BIM workflows following ISO 19650 certification, while Thomson Reuters leads legal case management through embedded Federal Rules processes.

Technology roadmaps now converge on generative AI copilots that surface relevant documents within transactions, cutting the 20-30% search tax knowledge workers shoulder. Vendors that blend AI innovation with strict compliance controls are best placed to secure long-term contracts, while pure-play laggards risk relegation to tactical niches. Acquisition pipelines remain active as software-only firms buy consulting practices to deliver full-stack offerings, accelerating consolidation yet preserving space for specialists that solve high-value vertical pain points.

Document Management Systems Industry Leaders

Microsoft Corporation

OpenText Corporation

IBM Corporation

Hyland Software Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Autodesk obtained ISO 19650 certification for Construction Cloud, trimming BIM deployment cycles from nine months to six weeks.

- October 2025: IBM partnered with Unstructured.io, raising Content Assistant accuracy to 97% on domain vocabularies.

- June 2025: Box extended Google Workspace integration, cutting version-control errors by 40% during pilots.

- January 2025: EY and Adobe launched a bundle that delivers Basel III audit trails in 12 weeks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Document Management Systems (DMS) market as the worldwide demand for software and associated services that capture, store, retrieve, and govern digital documents, PDFs, text files, images, e-forms, and scanned records throughout their life cycle, whether deployed on-premise or in the cloud according to Mordor Intelligence analysts.

Scope exclusion: solutions that serve only as generic file-sync repositories or pure web-content management tools without a dedicated document governance module are not counted.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By End-User Industry

- Banking and Financial Services

- Manufacturing and Construction

- Education

- Healthcare

- Retail

- Legal

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed technology buyers in BFSI, healthcare, manufacturing, and the public sector across North America, Europe, and Asia-Pacific, along with cloud integrators and cybersecurity auditors. Their inputs on license utilization, typical renewal discounts, and audit frequencies validated price curves and revealed region-specific adoption triggers that desk material alone cannot surface.

Desk Research

We first mapped publicly available statistics from trusted bodies such as NIST's Cybersecurity Insights, Eurostat's cloud-computing use files, the U.S. Bureau of Labor paper-consumption series, and industry submissions to AIIM and ARMA. Regulatory texts (HIPAA, GDPR, SEC 17a-4) and patent analytics from Questel helped us size compliance-driven refresh cycles, while 10-K filings and investor decks of major office-product vendors clarified average selling prices. News and financial feeds retrieved from Dow Jones Factiva, supported by D&B Hoovers revenue snapshots, anchored vendor share splits.

These secondary sources create the baseline vocabulary, installed base, seat penetration, and migration rates, yet they remain only part of the puzzle; many other open datasets and trade releases were reviewed to cross-check and supplement the figures mentioned here.

Market-Sizing & Forecasting

A blended top-down production and trade reconstruction is applied, starting with national enterprise counts, average seats per firm, and prevailing seat-price brackets. These results are corroborated through selective bottom-up checks, supplier roll-ups and channel feedback, to fine-tune outliers. Key model variables include:

1. Cloud DMS penetration among enterprises,

2. Average annual spend per employee on document software,

3. Share of regulated records subject to retention mandates,

4. Document digitization rates in paper-intensive verticals, and

5. Currency-adjusted license price erosion.

A multivariate regression with ARIMA overlay forecasts the five drivers, letting us simulate moderate, conservative, and aggressive demand arcs before locking the base case.

Gaps in bottom-up evidence are bridged by regional elasticity factors derived from primary interviews.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance screens against external market signals, and peer audits. We refresh models yearly and trigger interim updates when policy changes, cybersecurity incidents, or material M&A events alter market physics. A final pass is executed just before report publication so clients always receive the newest view.

Why Mordor's Document Management System Baseline Inspires Confidence

Published estimates often differ because firms choose unequal scopes, price ladders, and refresh cadences. Independent publications place 2024 global values between USD 7.16 billion and USD 7.68 billion.

Key gap drivers include whether services revenue is bundled, how free-tier users are counted, currency conversion dates, and if forecasts assume full AI-driven price premiums or tempered competitive discounting. Mordor's study reports USD 10.51 billion for 2025 after excluding generic file-sync tools and rechecking vendor ASPs quarterly, whereas others may lift earlier 2024 data without these adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.51 B (2025) | Mordor Intelligence | - |

| USD 7.68 B (2024) | Global Consultancy A | Older base year and narrower service capture |

| USD 7.16 B (2024) | Regional Consultancy B | Excludes hybrid deployment revenue |

| USD 8.96 B (2024) | Trade Journal C | Uses list prices without regional discount factors |

In sum, by tying every assumption to auditable variables, refreshing data annually, and filtering out unrelated content management spend, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the document management systems market?

The global market stands at USD 11.81 billion in 2026.

How fast is the document management systems market expected to grow?

It is forecast to expand at a 12.61% CAGR, reaching USD 21.39 billion by 2031.

Why are services growing faster than software in this space?

Migration complexity, AI configuration, and compliance mapping require specialized expertise, driving a 17.21% CAGR for services versus slower license growth.

Which deployment mode is gaining the most traction?

Cloud dominates with 70.34% of 2025 revenue and an 18.34% CAGR, though hybrid models are rising in regulated sectors.

Which industry will be the fastest adopter over the next five years?

Healthcare is projected to rise at a 17.69% CAGR due to telehealth documentation mandates and EHR integration.

Who are the leading vendors in the field?

Microsoft, OpenText, IBM, Hyland, and Oracle collectively control about 45% of global revenue, with Box and Adobe also holding notable positions.

Page last updated on: