| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 53.46 Billion |

| Market Size (2030) | USD 57.84 Billion |

| CAGR (2025 - 2030) | 1.59 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

District Heating Market Analysis

The District Heating Market size is estimated at USD 53.46 billion in 2025, and is expected to reach USD 57.84 billion by 2030, at a CAGR of 1.59% during the forecast period (2025-2030).

The district heating industry is undergoing a significant technological transformation with the emergence of fourth-generation systems that operate at lower temperatures of 50-60 degrees Celsius. This advancement represents a crucial shift in operational efficiency, as these modern systems substantially reduce heat loss within the district heating infrastructure while maintaining the traditional advantages of centralized heating infrastructure. The integration of digital technologies and machine learning capabilities has enabled predictive heat load management based on customer data, operational metrics, and weather forecasts. This technological evolution has proven particularly impactful in the European Union, where district heating currently serves approximately 60 million citizens, with an additional 140 million people residing in cities equipped with at least one district heating system.

The industry is witnessing a pronounced shift toward sustainable and renewable energy sources, driven by aggressive climate objectives set by global economies. A notable development in this direction is the June 2024 strategic partnership between Swedish SMR project developer Kärnfull Next and Finnish counterpart Steady Energy to introduce Small Modular Reactors (SMRs) for district heating in Sweden. The integration of electrically powered heat pumps in district heating supply networks has enabled higher renewable energy utilization for thermal purposes, creating a balanced synergy between various energy systems. This transition has demonstrated remarkable environmental benefits, with industrial conversions to district heating systems achieving a significant reduction in electricity usage by 11% and fossil fuel consumption by 40%.

The market is experiencing rapid advancement in operational efficiency through digitalization and data analytics. Utilities are increasingly implementing fully integrated data systems to identify and resolve inefficiencies promptly, while intelligent algorithms are being deployed for fault detection, including the identification of leakages, inefficient heating systems, and component failures. This digital transformation has enabled utilities to better understand client heat usage patterns, implement new control strategies, and personalize demand management for specific customer groups. The integration of these technologies has facilitated more effective district heating operation and management, contributing to the industry's overall modernization.

The industrial application of district heating systems continues to evolve, despite varying heat load requirements across different industries and processes. Through the implementation of district heating networks, significant environmental impacts have been achieved, with industrial conversions leading to a reduction of global carbon dioxide emissions by 112,000 tons annually. The industry's infrastructure continues to expand, particularly in the European Union, where district heating networks currently meet 11-12% of the EU's heat demand through approximately 6,000 district heating and district cooling networks. This expansion demonstrates the growing recognition of district heating as a viable solution for industrial energy needs, despite the challenges posed by diverse industrial requirements and processes.

District Heating Market Trends

Augmented Demand for Energy-Efficient and Cost-Effective Heating Systems

The growing emphasis on energy efficiency and cost optimization in heating systems is driving significant market growth in the district heating sector. According to EuroHeat, district heating and district cooling systems demonstrate substantial environmental benefits, with the potential to help avoid 9.3% of all European CO2 emissions and achieve 40-50 million metric tons of annual CO2 reductions through district cooling implementations. This efficiency is particularly important as heating equipment in residential spaces constitutes a major portion of energy consumption, making centralized district heating systems an attractive alternative to individual heating solutions. The technology's ability to utilize industrial waste heat from power plants, industrial processes, and renewable energy sources further enhances its appeal as an energy-efficient solution.

The cost-effectiveness of district heating systems is demonstrated through their ability to serve large populations efficiently. Currently, approximately 60 million EU citizens are served by district heating, with an additional 140 million people living in cities with at least one district heating system. The transition to fourth-generation district heating systems, which operate at lower temperatures (50-60 degrees), has further improved efficiency by reducing heat loss within the network, resulting in additional cost savings. This evolution in technology, combined with the integration of renewable energy sources and waste heat recovery, makes district heating an increasingly attractive option for both residential and commercial applications, particularly in densely populated urban areas where the infrastructure can be optimally utilized.

Understand The Key Trends Shaping This Market

Download PDF

Rising Urbanization and Industrialization

The rapid pace of urbanization and industrialization is creating substantial opportunities for district heating system implementations worldwide. According to OECD projections, countries like India and China are expected to see a sevenfold increase in per capita income by 2060, driving massive urban development and industrial growth. This economic expansion, coupled with increasing energy demands in urban centers, is pushing the adoption of centralized heating solutions. The trend is particularly evident in Germany, where recent data from BDH shows approximately 790,500 gas heating systems were sold in 2023, with over 696,500 utilizing advanced condensing boiler technology, demonstrating the growing sophistication of heating infrastructure in urbanized areas.

The industrialization trend is also driving the integration of district heating systems with industrial processes, creating efficient energy ecosystems in urban-industrial zones. Major industrial parks and commercial centers are increasingly adopting district heating solutions to optimize energy usage and reduce operational costs. For instance, in Southeast Asian countries, where rapid industrialization is occurring alongside urbanization, district heating solutions are being implemented to address both industrial heating needs and environmental concerns related to air pollution. The systems' ability to utilize industrial waste heat and incorporate renewable energy sources makes them particularly valuable in industrial zones, where they can serve both industrial processes and nearby urban developments, creating synergistic energy efficiency benefits.

Segment Analysis: By Plant Type

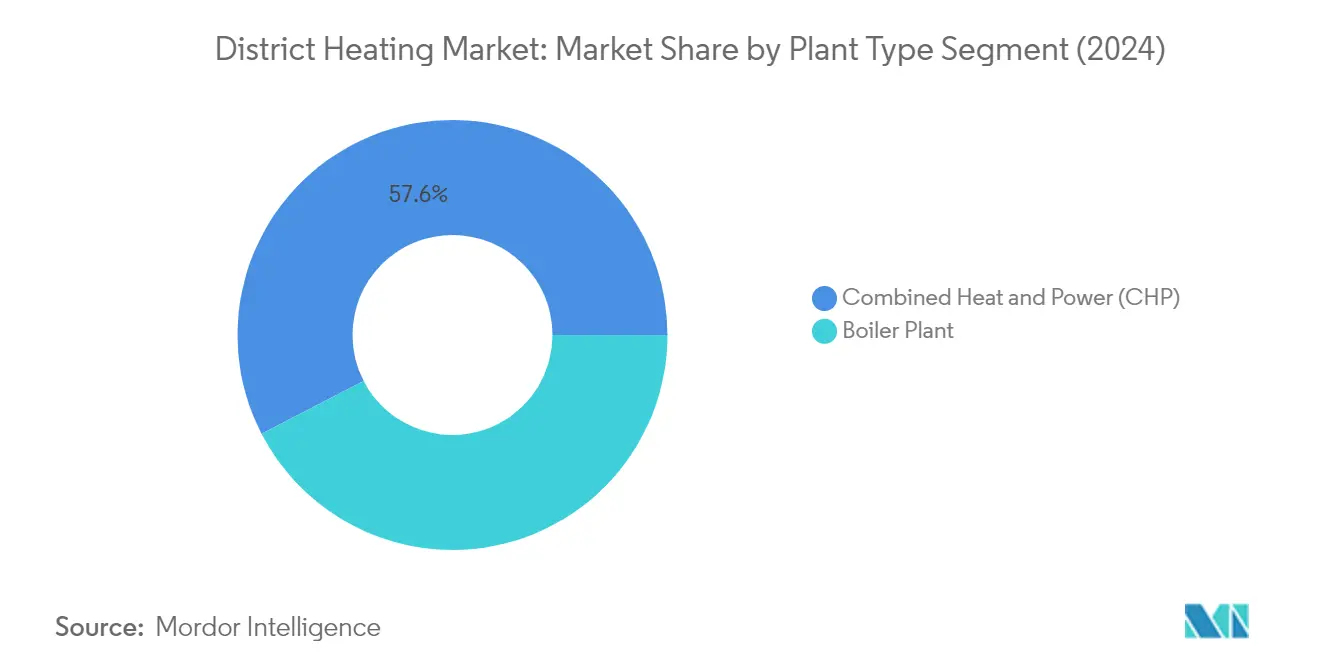

Combined Heat and Power (CHP) Segment in District Heating Market

The combined heat and power (CHP) segment dominates the global district heating market, holding approximately 58% market share in 2024. This dominance is driven by its superior efficiency in simultaneously generating electricity and heat. Unlike traditional heating plant systems, CHP technology recovers waste heat from electricity production, achieving total energy conversion efficiencies ranging from 60% to 80%. The segment's prominence is further strengthened by government incentives and programs, particularly in Organization for Economic Cooperation and Development countries, where many nations have established tax incentives and CHP power generation targets. Gas-fired CHP has emerged as a well-established technology scalable to different sizes, while direct biomass CHP has proven technically and economically viable for large-scale plants above 10-20 MW. The segment is projected to maintain its market leadership and demonstrate robust growth at nearly 3% CAGR from 2024 to 2029, supported by increasing adoption of gasification and ORC (Organic Rankine Cycle) technologies that enable smaller plants to operate from biomass. The combined heat and power market is expected to see significant advancements as these technologies evolve.

Boiler Plant Segment in District Heating Market

The boiler plant segment represents a crucial component of the district heating market, offering dedicated thermal energy generation through various fuel sources, including fossil fuels, renewable-sourced fuels, and solid waste incineration. Modern boiler plants have achieved remarkable efficiency improvements, with manufacturers capable of increasing conversion efficiencies above 97% based on lower heating value, which can exceed 100% when flue gas condensation is utilized. This segment is particularly significant in regions transitioning to more sustainable energy sources, as biomass-fired heating plants gain prominence, especially within the European Union. The technology's centralized layout enables more efficient removal of pollutants compared to individual decentralized systems, while the ability to combine different fuel types within a district heating scheme helps avoid dependence on a single energy source. The segment continues to evolve with innovations in condensing boiler technology and integration of renewable fuel sources, maintaining its essential role in the district heating infrastructure.

Segment Analysis: By Heat Source

Natural Gas Segment in District Heating Market

Natural gas maintains its dominant position in the district heating market, commanding approximately 39% market share in 2024, valued at around USD 20.48 billion. The segment's leadership is primarily driven by the cost-effectiveness and environmental advantages of natural gas plants compared to traditional fossil fuel alternatives. Natural gas-based district heating systems have gained significant traction, particularly in Europe, where countries like Germany and the Netherlands rely heavily on this energy source, with more than 90% of their heat being supplied by natural gas. The segment's growth is further supported by the increasing exploration activities worldwide and the relatively lower environmental impact compared to coal-based systems. Additionally, the integration of natural gas in trigeneration systems, which provide electricity, heating, and cooling simultaneously, has enhanced its adoption in various commercial and industrial applications.

Renewables Segment in District Heating Market

The renewables segment is experiencing remarkable growth in the district heating market, with an expected CAGR of approximately 15% during the forecast period 2024-2029. This substantial growth is driven by increasing government initiatives promoting renewable energy adoption in district heating systems and growing environmental consciousness. The segment encompasses various renewable sources, including biomass, solar thermal, geothermal, and waste heat recovery systems. The transition towards low-temperature district heating systems, particularly the fourth-generation systems operating at 50-60 degrees, has significantly enhanced the integration capabilities of renewable energy sources. Furthermore, several European countries have achieved notable success in renewable energy integration, with at least eight countries reaching over 40% renewable energy share in their district heating supply, setting a precedent for other regions to follow.

Remaining Segments in Heat Source Segmentation

The coal and oil & petroleum products segments continue to play significant roles in the district heating market, though their importance is gradually diminishing due to environmental concerns and regulatory pressures. The coal segment, while still substantial in regions like China where it accounts for a significant portion of district heating production, is facing increasing pressure from decarbonization initiatives and environmental regulations. The oil and petroleum products segment represents the smallest share of the market, primarily due to ongoing global efforts to phase out oil-based heating systems. Many countries, particularly in Europe, are implementing policies to transition away from these traditional fossil fuel sources towards more sustainable alternatives, reflecting a broader industry shift towards cleaner energy sources.

Segment Analysis: By Application

Residential Segment in District Heating Market

The residential segment dominates the district heating market, accounting for approximately 50% of the total market share in 2024. This significant market position is driven by the widespread adoption of district heating systems in single-family houses, multi-family houses, high-rise buildings, and mega townships, primarily for space heating and water heating applications. The segment's dominance is particularly pronounced in cold climate countries like Denmark, Iceland, and other EU nations, where district heating networks powered by renewable sources have resulted in significant emission reductions. The implementation of various state-level incentives and programs has further strengthened the residential segment's position, with many countries offering grants, subsidies, and energy taxes to increase the share of renewables in heat production. The segment's strong performance is also attributed to the growing awareness of energy efficiency and the cost-effectiveness of district heating solutions compared to individual building apparatus.

Commercial and Industrial Segment in District Heating Market

The commercial and industrial segment is projected to exhibit the highest growth rate of approximately 2% during the forecast period 2024-2029. This growth is primarily driven by the increasing adoption of sustainable building protocols imposed by regulatory bodies and technological advancements in combined heat and power systems. The segment's expansion is further supported by the growing investments in new commercial establishments and the integration of district heating solutions in industrial processes. The push toward renewable energy establishments and the extraction of sensible heat for industrial and commercial applications continues to positively influence the segment's growth trajectory. Additionally, the rising focus on energy efficiency and the implementation of smart building technology has created new opportunities for district heating solutions in commercial spaces, particularly in regions experiencing rapid urbanization and industrialization.

District Heating Market Geography Segment Analysis

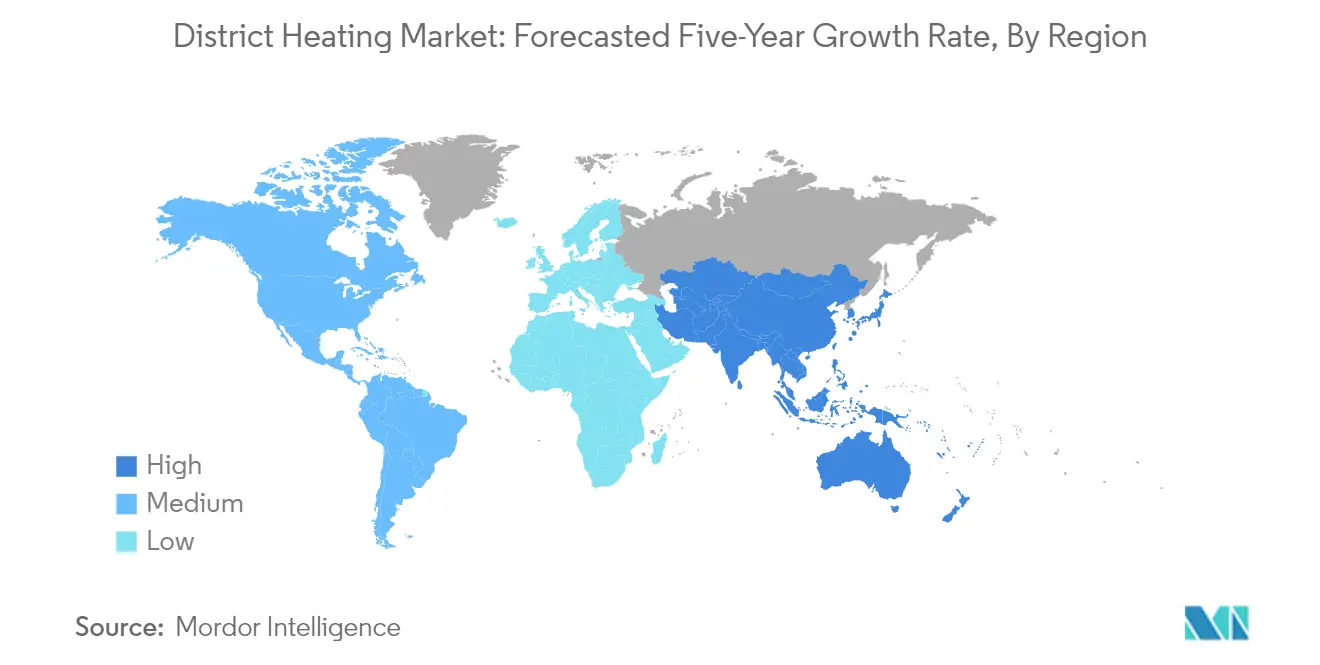

District Heating Market in North America

The North American district heating market maintains approximately 5% of the global market share in 2024, primarily driven by institutional and urban systems across the United States and Canada. The market structure in this region is characterized by three distinct types of systems: municipal or not-for-profit urban systems, investor-owned urban systems, and institutional systems. The institutional segment has shown particularly strong growth, benefiting from less regulatory oversight and tax exemptions. Life science and biomedical sectors are increasingly embracing district energy technology due to its reliability and resiliency, especially for critical facilities like medical centers and hospitals where consistent heating, humidification, cooling, and equipment sterilization are crucial for patient care. The region's market is further characterized by significant geographical variations, with northern cities like Milwaukee, Minneapolis, and Detroit showing higher adoption rates due to their colder climates. Canadian markets have evolved significantly, with district energy systems becoming increasingly efficient and utilizing various alternative energy sources, including biomass, solar, deep-water cooling, and solid waste to produce lower emissions.

District Heating Market in Europe

The European district heating market has demonstrated steady growth at approximately 0.5% annually from 2019 to 2024, reflecting the mature nature of the market and its established infrastructure. The region's market is particularly strong in Scandinavian and Central European countries, where district heating remains the principal method for providing space and water heating in urban areas. Germany stands as one of the largest markets, with district heating being more prevalent in the eastern regions due to historical policy influences. The market's development is strongly supported by comprehensive national legislation, particularly in countries like Denmark and Germany, where policies encompass federal support, specific targets, connection obligations, and customer protection measures. The region's commitment to sustainability is evident in its push toward fourth-generation district heating systems, which operate at lower temperatures and achieve greater efficiency. Market dynamics are further shaped by the EU's ambitious climate goals and the increasing integration of renewable energy sources into district heating networks.

District Heating Market in Asia-Pacific

The Asia-Pacific district heating market is projected to grow at approximately 3% annually from 2024 to 2029, establishing itself as the most dynamic region in the global market. China leads the regional market with rapid expansion of centralized systems, particularly in its northern regions where heating demand is substantial. The market's growth is driven by increasing urbanization, rising disposable incomes, and growing environmental consciousness across the region. Japan's market is evolving in response to its energy diversification goals and carbon emission reduction targets, while South Korea is advancing its zero-energy building initiatives through various energy efficiency policies. The region's district heating infrastructure is increasingly incorporating advanced technologies and smart systems, particularly in new urban developments. Market expansion is further supported by strong government initiatives, particularly in China where policies actively promote clean heating technologies and sustainable urban development.

District Heating Market in Rest of the World

The Rest of the World market, encompassing regions such as Latin America, the Middle East, and Africa, represents an emerging frontier for district heating solutions. Countries like Brazil, Mexico, and South Africa are showing increasing interest in district heating and district cooling systems, driven by rapid urbanization and growing energy demands in their commercial and residential sectors. The Middle East and North Africa (MENA) region, despite having lower heating requirements compared to other regions, is witnessing growing demand due to expanding building infrastructure and population growth. The market in these regions is characterized by a strong focus on district cooling applications, particularly in commercial developments and high-rise buildings where natural ventilation is limited. The development of district heating systems in these regions is closely tied to broader urban development initiatives and sustainability goals, with many countries implementing new energy efficiency standards and exploring renewable energy integration into their district heating systems.

Get Analysis on Important Geographic Markets

Download PDF

District Heating Industry Overview

Top Companies in District Heating Market

The district heating market features established players like Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, and Logstor AS, among others, who are actively shaping the industry landscape. These district heating companies are increasingly focusing on product innovation, particularly in developing fourth-generation low-temperature district heating systems and smart energy solutions that integrate renewable sources. Operational agility is demonstrated through investments in digitalization, network optimization, and improved asset management systems. Strategic partnerships and collaborations, especially with government bodies and technology providers, have become crucial for expanding market presence. Companies are also pursuing geographical expansion through both organic growth and acquisitions, with particular emphasis on emerging markets in Asia-Pacific and modernization projects in Europe. The industry is witnessing a clear shift towards sustainable solutions, with major players investing in renewable energy integration and carbon reduction initiatives for their district heating networks.

Market Structure Shows Regional Leadership Patterns

The district heating market exhibits a mix of global conglomerates and regional specialists, with market leadership often determined by geographical presence and technological capabilities. Large multinational corporations like Vattenfall and Engie leverage their diverse energy portfolios and financial strength to maintain market positions, while regional specialists such as Göteborg Energi and FVB Energy excel in their respective territories through deep local market understanding and specialized expertise. The market shows moderate consolidation, with established players holding significant market share in their core regions, particularly in the Nordic countries and Western Europe. These companies often operate as integrated energy providers, offering district heating as part of their broader energy solutions portfolio.

The industry is characterized by active merger and acquisition activity, driven by the need to acquire new technologies, enter high-growth markets, and achieve operational synergies. Companies are increasingly pursuing strategic acquisitions to strengthen their position in specific regions or to acquire complementary capabilities, particularly in renewable energy integration and smart grid technologies. Private equity firms are also showing growing interest in the sector, particularly in acquiring and modernizing existing district heating infrastructure. This trend is especially prominent in emerging markets where urbanization and environmental regulations are driving demand for efficient heating solutions.

Innovation and Sustainability Drive Future Success

Success in the district heating market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and environmental sustainability. Incumbent players are focusing on modernizing existing infrastructure, implementing smart technologies for district heating distribution optimization, and increasing the share of renewable energy sources in their heating mix. Market leaders are investing heavily in research and development to improve system efficiency and reduce heat losses, while also developing new business models that address changing customer needs and regulatory requirements. The ability to integrate various heat sources, including industrial waste heat and geothermal energy, while maintaining reliable service has become a critical differentiator.

For contenders looking to gain market share, success factors include developing specialized expertise in specific market segments or technologies, building strong relationships with local authorities and stakeholders, and offering innovative financing solutions. The market faces moderate substitution risk from individual heating solutions and heat pumps, driving companies to enhance their value proposition through improved service quality and competitive pricing. Regulatory frameworks, particularly regarding carbon emissions and renewable energy requirements, continue to shape market dynamics and investment decisions. Companies that can effectively navigate these regulatory requirements while maintaining operational efficiency and customer satisfaction are better positioned for long-term success.

District Heating Market Leaders

-

Vattenfall AB

-

Danfoss Group

-

SP Group

-

Engie

-

NRG Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

District Heating Market News

- April 2023: Danfoss Group announced the new options for OEMs as it expands the Z-design range of Micro Plate Heat Exchangers; where The latest addition to the range C262L-EZD is a dual-circuit evaporator that's ideal for scroll chillers. These robust and reliable units extend the range's capability with cooling capacities now covering up to 300 kW in single circuits and up to 800 kW in dual circuits.

- October 2022: ENGIE announced it acquired a 6 GW portfolio of solar, paired and stand-alone battery storage development projects from Belltown Power U.S. The transaction included 33 projects comprising some 2.7 GW of Solar with 0.7 GW of paired storage and 2.6 GW of stand-alone battery storage. The projects across ERCOT, PJM, MISO and WECC1 and ENGIE will increase grid stability and resilience by integrating green power generation with paired and stand-alone storage.

District Heating Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

- 4.5 Government Initiatives and Programs on District Heating Transition

- 4.6 Key Trends and Innovations in District Heating

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

-

5.2 Market Restraints

- 5.2.1 High Infrastructure Cost

6. MARKET SEGMENTATION

-

6.1 By Plant Type

- 6.1.1 Boiler

- 6.1.2 Combined Heat and Power (CHP)

-

6.2 By Heat Source

- 6.2.1 Coal

- 6.2.2 Natural Gas

- 6.2.3 Renewables

- 6.2.4 Oil and Petroleum Products

-

6.3 By Application

- 6.3.1 Residential

- 6.3.2 Commercial and Industrial

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Vattenfall AB

- 7.1.2 SP Group

- 7.1.3 Danfoss Group

- 7.1.4 Engie

- 7.1.5 NRG Energy Inc.

- 7.1.6 Statkraft AS

- 7.1.7 Logstor AS

- 7.1.8 Shinryo Corporation

- 7.1.9 Vital Energi Ltd

- 7.1.10 Gteborg Energi

- 7.1.11 Alfa Laval AB

- 7.1.12 Ramboll Group AS

- 7.1.13 Keppel Corporation Limited

- 7.1.14 FVB Energy

8. INVESTMENT ANALYSIS

9. FUTURE OPPORTUNITIES

**Subject to Availability

*** In the Final Report Asia, Australia and New Zealand will be Studied Together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

District Heating Industry Segmentation

District heating (also recognized as heat networks or teleheating) is a system for distributing heat produced in a centralized place through insulated pipes for domestic and commercial heating necessities, such as water heating and space heating. The district heating system comprises a high-powered central boiler, well-insulated pipes hidden under the streets, a heat exchanger, and an added system (heat pump, solar power, boiler, etc.) to generate hot water separately in the summertime.

The district heating market is segmented by plant type (boiler plant, combined heat and power (CHP)), heat source (coal, natural gas, renewables, oil, and petroleum products), by application (residential, commercial, and industrial), and by geography (North America, Europe, Asia Pacific, Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| By Plant Type | Boiler |

| Combined Heat and Power (CHP) | |

| By Heat Source | Coal |

| Natural Gas | |

| Renewables | |

| Oil and Petroleum Products | |

| By Application | Residential |

| Commercial and Industrial | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

District Heating Market Research FAQs

How big is the District Heating Market?

The District Heating Market size is expected to reach USD 53.46 billion in 2025 and grow at a CAGR of 1.59% to reach USD 57.84 billion by 2030.

What is the current District Heating Market size?

In 2025, the District Heating Market size is expected to reach USD 53.46 billion.

Who are the key players in District Heating Market?

Vattenfall AB, Danfoss Group, SP Group, Engie and NRG Energy Inc. are the major companies operating in the District Heating Market.

Which is the fastest growing region in District Heating Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in District Heating Market?

In 2025, the Asia-Pacific accounts for the largest market share in District Heating Market.

What years does this District Heating Market cover, and what was the market size in 2024?

In 2024, the District Heating Market size was estimated at USD 52.61 billion. The report covers the District Heating Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the District Heating Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

District Heating Market Research

Mordor Intelligence provides a comprehensive analysis of the district heating industry. We leverage our extensive experience in researching thermal energy networks. Our latest report examines the evolving landscape of communal heating systems. It includes combined heat and power technologies, district cooling solutions, and innovative thermal storage applications. The analysis covers various heating sources, such as geothermal district heating, biomass district heating, and solar district heating installations. We provide detailed insights into district heating companies and their technological innovations.

Our detailed report is available in an easy-to-read PDF download format. It offers stakeholders crucial insights into district heating infrastructure developments and heat network expansion strategies. The analysis covers district heating pipeline systems, industrial waste heat utilization, and emerging municipal heating trends. With in-depth coverage of the district heating market size and growth projections, the report helps stakeholders understand network heating dynamics and district energy opportunities. The research focuses particularly on advancements in thermal energy networks and district heating distribution systems. It provides valuable insights for industry participants looking to optimize their market positioning and strategic planning.