Direct-to-Consumer Laboratory Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.62 Billion |

| Market Size (2030) | USD 5.92 Billion |

| Growth Rate (2025 - 2030) | 10.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

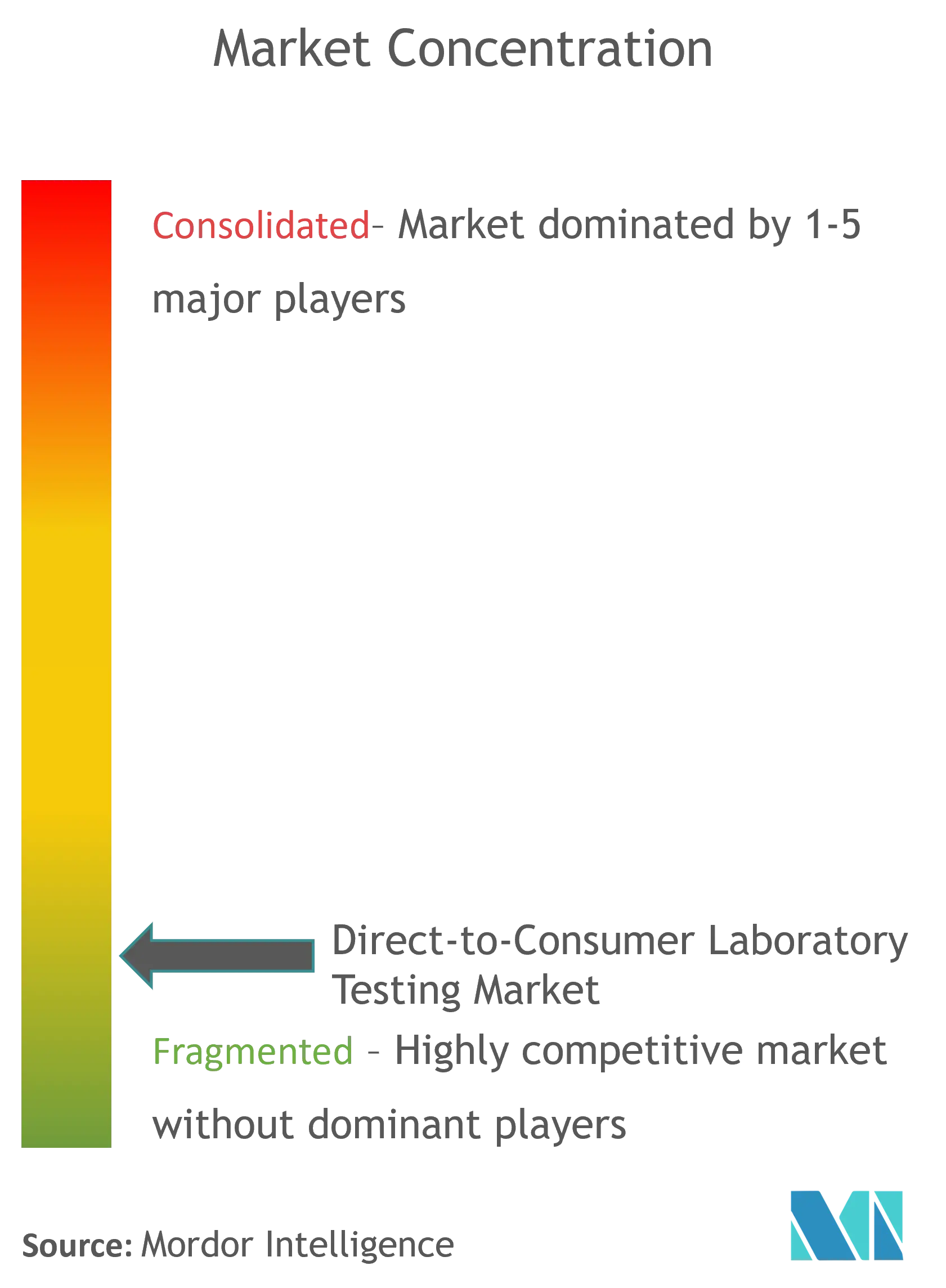

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Direct-to-Consumer Laboratory Testing Market Analysis by Mordor Intelligence

The Direct to Consumer Laboratory Testing market generated USD 3.62 billion in 2025 and is forecast to reach USD 5.92 billion by 2030, reflecting a healthy 10.35% CAGR over the period. Growth is underpinned by permanent shifts toward at-home care, cost-efficient telehealth integrations, and rapid declines in sequencing and assay prices. New FDA rules now clarify compliance pathways, spurring capital investment even as they raise short-term operating costs. Corporate wellness subsidies, privacy-centric data custody solutions, and micro-device blood collection technologies are widening the addressable patient base. Meanwhile, recent consolidations—most notably LetsGetChecked–Truepill and Hims & Hers–Trybe Labs—are redrawing competitive boundaries and accelerating vertical integration.

Key Report Takeaways

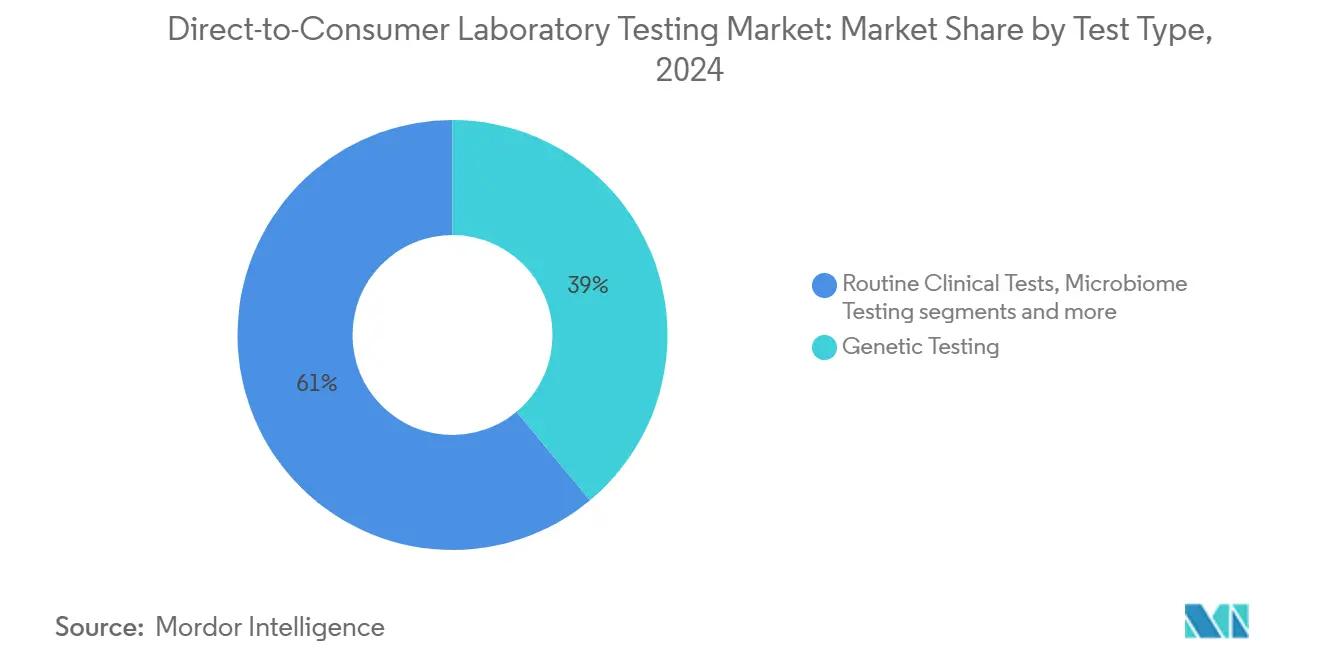

By test type, Genetic Testing led with 38.95% of the Direct to Consumer Laboratory Testing market share in 2024, while Hormonal Wellness Panels are set to expand at an 11.89% CAGR to 2030.

By sample type, Saliva retained 46.56% share of the Direct to Consumer Laboratory Testing market size in 2024; Blood sampling is advancing at a 12.23% CAGR through 2030.

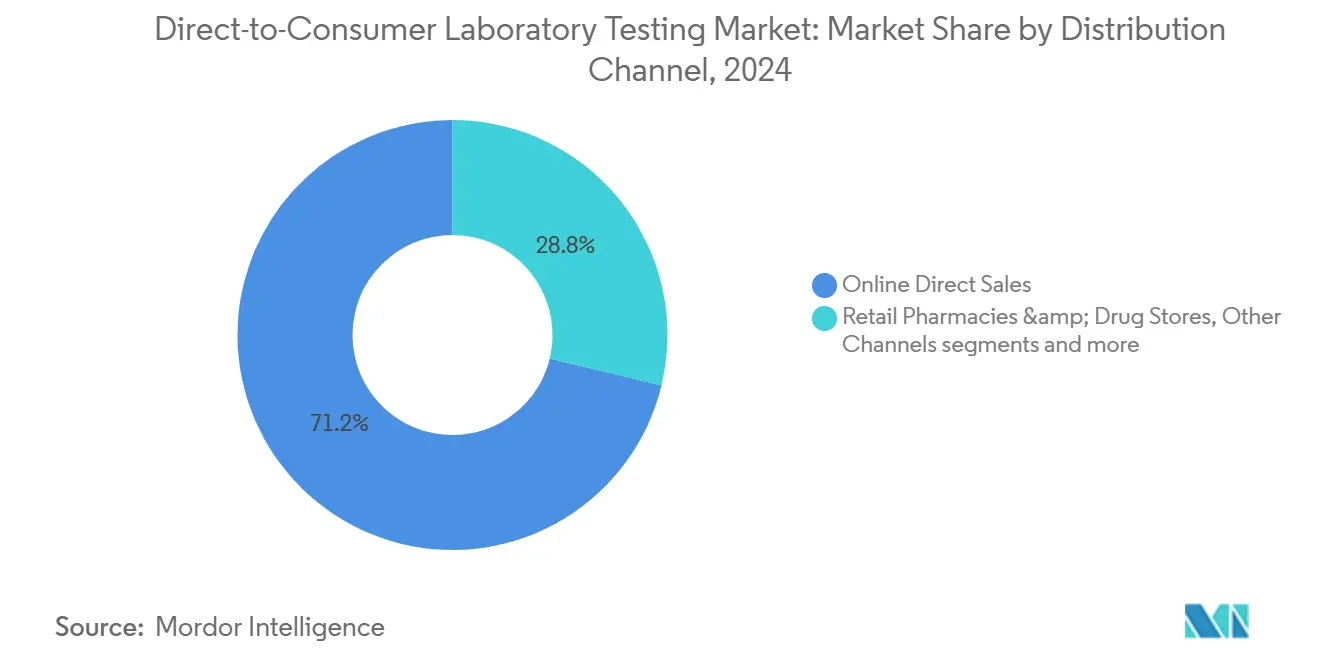

By distribution channel, Online Direct Sales accounted for 71.23% of 2024 revenue, whereas Other Channels are forecast to grow at a 12.59% CAGR through 2030.

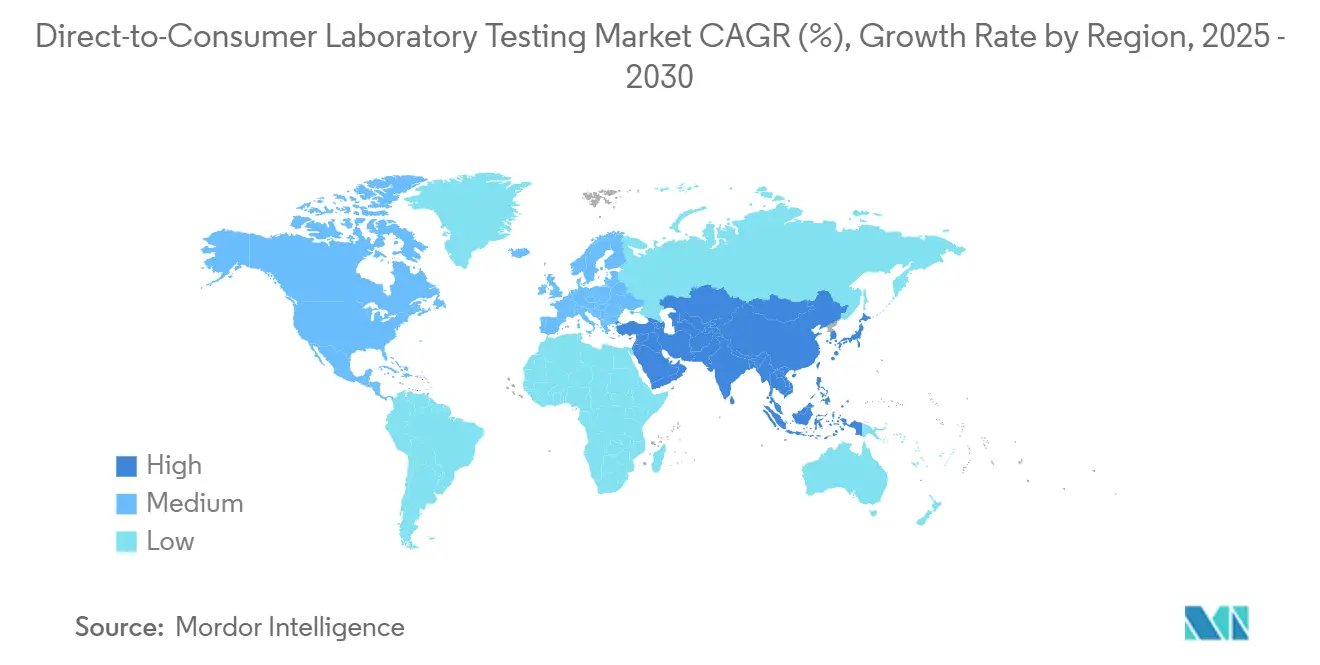

By geography, North America held 39.89% share in 2024; Asia-Pacific is the fastest-growing region with a 12.95% CAGR to 2030.

Global Direct-to-Consumer Laboratory Testing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for convenient at-home testing | +2.8% | Global, with strongest uptake in North America & Europe | Medium term (2-4 years) |

| Expansion of telehealth-integrated digital ordering platforms | +2.1% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Falling genomic sequencing & assay costs | +1.9% | Global, with accelerated adoption in price-sensitive markets | Long term (≥ 4 years) |

| Employer-sponsored wellness test subsidies | +1.4% | North America & EU, pilot programs in APAC | Medium term (2-4 years) |

| Blockchain-enabled data-custody boosting trust | +0.8% | Global, with early adoption in privacy-conscious regions | Long term (≥ 4 years) |

| Microfluidic dried-blood-spot logistics breakthroughs | +1.1% | Global, with manufacturing concentration in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Convenient At-Home Testing

Pandemic-era habits have evolved into lasting preferences as insurers such as QualChoice mail kits directly to members, validating at-home models as cost-effective preventive tools. Platforms like Quest Health now market more than 100 self-ordered tests supported by physician review, eliminating the wait time and expense of clinic visits. Venture funding mirrors this shift; Function Health secured USD 53 million to scale a USD 499 yearly plan covering 100 biomarkers. The convenience imperative extends from painless sample collection to app-based result dashboards, cementing consumer autonomy even in well-served urban areas. As a result, the Direct to Consumer Laboratory Testing market enjoys a demand floor insulated from hospital capacity constraints.

Expansion of Telehealth-Integrated Digital Ordering Platforms

Federal guidance specifically endorses direct-to-consumer telehealth workflows, encouraging integrated clinical protocols that flow from test ordering to treatment, Partnerships such as 23andMe–Nightingale pair genetic insights with immediate blood-based risk scoring to trigger diet or medication consults. B2B2C enablers like Locke Bio embed full lab menus into white-label telehealth portals, creating cross-sell loops that lift lifetime value. Subscription telehealth programs that bundle testing with weight-management drugs or dermatology care now set higher consumer expectations, reinforcing network effects between diagnostics and virtual prescribing. The Direct to Consumer Laboratory Testing market is therefore tilting toward ecosystems rather than single-product offerings.

Falling Genomic Sequencing & Assay Costs

WIPO data show whole-genome sequencing costs dropping from USD 100 million in 2001 to just above USD 500 in 2025, with a roadmap toward USD 10. This deflation underlies Labcorp’s tie-up with Ultima Genomics and the launch of 23andMe’s “Total Health,” which blends whole-exome analysis with twice-yearly blood panels. Lower cost curves unlock mass-market and emerging-economy adoption, expanding the Direct to Consumer Laboratory Testing market far beyond its early-adopter base. The same trend allows payers to contemplate population-level screening programs, turning once-premium tests into preventive-care staples.

Employer-Sponsored Wellness Test Subsidies

Labcorp’s employer services bundle routine labs, drug screens, and biometric panels into benefits programs that promise absenteeism reductions. Self-insured firms now co-pay or fully subsidize Function Health memberships, arguing that USD 499 per employee is lower than chronic-disease treatment outlays. UnitedHealthcare expanded reimbursement codes for consumer-initiated tests that meet medical-necessity documentation. As labor markets tighten, companies view expansive wellness benefits as retention tools, injecting new volume into the Direct to Consumer Laboratory Testing market over the medium term.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened FDA scrutiny & evolving regulations | -1.7% | North America core, regulatory spillover to global markets | Short term (≤ 2 years) |

| Privacy / genetic-discrimination concerns | -1.2% | Global, with acute sensitivity in EU & privacy-conscious demographics | Medium term (2-4 years) |

| Lack of reimbursement paths for price-sensitive users | -0.9% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Public backlash over biobank ethics | -0.6% | Global, with concentrated impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened FDA Scrutiny & Evolving Regulations

The FDA’s 2025 final rule applies device-quality system, adverse-event reporting, and eventual premarket review to most laboratory-developed tests, with compliance costs estimated up to USD 3.56 billion industry-wide. Pediatric hospitals warn that specialized diagnostics could become scarcer and costlier, while industry associations pursue litigation to narrow the rule’s scope. Because direct-to-consumer assays are excluded from enforcement discretion, companies must divert capital toward validation and documentation, extending product-launch timelines. Although long-term certainty attracts strategic investors, near-term margin compression limits smaller entrants, tempering the Direct to Consumer Laboratory Testing market’s otherwise strong outlook.

Privacy/Genetic-Discrimination Concerns

After 23andMe’s 2024 breach exposed data from nearly 7 million users, the FTC levied penalties on multiple testing firms for lax security and deceptive marketing. Thirteen U.S. states have since enacted statutes requiring affirmative consent and explicit secondary-use disclosures, while the EU’s January 2025 Health Data Space regulation tightens cross-border data handling. Although the Genetic Information Nondiscrimination Act shields Americans from insurer misuse, consumer worry persists, especially when financially distressed firms change ownership. Companies must therefore triple-down on encryption, zero-knowledge architectures, and transparent policies—investments that raise operational costs and slow consumer onboarding.

Segment Analysis

By Test Type: Genetic Breadth Meets Hormonal Momentum

Genetic Testing held a 38.95% share of the Direct to Consumer Laboratory Testing market in 2024, reflecting decades of brand recognition and the rich insights extractable from DNA profiles. The segment benefited from premium price points and add-on services such as pharmacogenomics counseling. However, Hormonal Wellness Panels are positioned as the growth engine, advancing at an 11.89% CAGR through 2030 as awareness of endocrine health links to weight management, fertility, and mental wellbeing. The Direct to Consumer Laboratory Testing market size for hormonal tests is projected to widen rapidly as athletes, perimenopausal women, and biohackers seek actionable metrics. Routine Clinical Tests keep unit-volume leadership but fight commoditization, while Microbiome, Allergy, and Infectious Disease panels expand as cross-sell options inside subscription bundles. Product diversification therefore underpins revenue resilience even if single-segment demand softens.

Genetic providers are broadening into actionable disease monitoring; 23andMe recently added homocysteine lab panels to complement MTHFR genotyping. This blend of genotype and phenotype pushes average selling prices higher without inflating customer-acquisition spend. Meanwhile, startups target niche specialties—nutrigenomics for personalized meal planning or pharmacogenomics for drug-response optimization—adding long-tail value to the Direct to Consumer Laboratory Testing market. Successful players align test menus with clear intervention pathways, satisfying regulators that results directly influence care decisions.

Note: Segment shares of all individual segments available upon report purchase

By Sample Type: Saliva Convenience vs Blood Precision

Saliva retained 46.56% of 2024 revenue thanks to non-invasive self-collection that truly dematerializes geography. Yet blood sampling is on track for a 12.23% CAGR as capillary devices shrink discomfort and logistical hurdles. The Direct to Consumer Laboratory Testing market size attached to fingertip-blood assays is expanding as BD’s MiniDraw shows equivalency to venous draws while requiring only basic training. Urine testing remains integral for hormones and toxicology, whereas stool sampling powers microbiome analytics and colorectal cancer screens. Emerging matrices—hair for long-term substance exposure, breath for metabolic profiling—occupy specialized niches.

Medical-establishment preference for serum over saliva in many hormone assays boosts prospects for blood-based services; Aetna policies highlight these validity concerns. Companies capturing both convenience and clinical rigor stand to differentiate in the Direct to Consumer Laboratory Testing market. Expect hybrid kits bundling saliva DNA with capillary blood for biomarkers, offering a single shipping envelope and unified app reporting.

By Distribution Channel: Online Scale Meets Retail Trust

Online Direct Sales represented 71.23% of 2024 turnover, riding search-driven discovery, influencer marketing, and frictionless checkouts. The model excels in breadth, privacy, and automated fulfillment. Yet Other Channels are moving faster—12.59% CAGR—on the back of pharmacy partnerships and employer programs. Walmart now sells Quest-branded kits in-store, giving less tech-savvy shoppers immediate access and pharmacist guidance. Retail Pharmacies also offer pickup for online orders, merging digital convenience with physical collection points.

Meanwhile, large reference labs deploy direct-to-consumer storefronts that leverage insurance networks where medical-necessity criteria are met. Integrated triage and e-prescribing guardrails enable compliance with evolving FDA expectations. As hybrid models mature, online players must invest in physical nodes or risk ceding share to omnichannel incumbents. The Direct to Consumer Laboratory Testing market therefore rewards channel diversification alongside digital excellence

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 39.89% of 2024 value, supported by early regulatory clarity and entrenched telehealth infrastructure. The FDA’s final rule, while burdensome, reassures investors about long-term pathways, and insurers often reimburse physician-ordered versions of the same assays. Quest Diagnostics’ CAN 1.35 billion LifeLabs acquisition extends reach across the United States–Canada corridor and delivers economies of scale in specialized testing.

Asia-Pacific represents the growth frontier at a 12.95% CAGR through 2030. Rising middle-class wealth, mobile-first consumer behavior, and ongoing hospital capacity constraints favor direct-to-consumer solutions. Dr. Lal Path Labs’ profit surge illustrates demand depth in India, while China’s regulators steadily refine consumer diagnostics rules to align with international standards. Singapore, Japan, and South Korea anchor premium genetic and hormonal panels, whereas Southeast Asian markets prioritize basic health screens and infectious-disease panels.

Europe grows steadily under the recently adopted Health Data Space framework, which balances cross-border data flows with strict privacy guarantees. High consumer awareness of GDPR boosts willingness to pay for secure testing platforms. South America and the Middle East & Africa trail in absolute numbers but offer long-run upside once logistics and privacy regulations mature. Brazil leads Latin America’s adoption curve, and GCC governments are piloting national screening initiatives to curb chronic-disease burdens.

Competitive Landscape

Competition is moderate and tilting toward consolidation. Digital natives pursue vertical integration—LetsGetChecked absorbed Truepill for USD 525 million to couple pharmacy fulfillment with diagnostics—while telehealth giants like Hims & Hers buy laboratories to close their care loop. Reference laboratories, including Quest Diagnostics and Labcorp, counterpunch with branded portals that marry physician-ordering and insurance billing to direct purchase flexibility. Technology moats now center on painless sampling devices, AI-driven risk stratification, and HIPAA-grade data vaults rather than basic assay accuracy.

The 2025 nonprofit buyout of 23andMe for USD 305 million removed a major public competitor yet preserved its vast genotype database under research stewardship. This exit opens space for challengers that foreground privacy and transparent governance. Compliance capability also differentiates; firms with ISO-certified quality systems and experienced regulatory teams scale faster under the new FDA regime. Partnership velocity—from fintech-enabled FSA payments to employer portals—further separates leaders from niche players in the Direct to Consumer Laboratory Testing market.

Direct-to-Consumer Laboratory Testing Industry Leaders

-

Any Lab Test Now Inc.

-

DirectLabs, LLC.

-

EasyDNA

-

Everlywell, Inc.

-

Genesis Healthcare Co

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Anne Wojcicki’s nonprofit TTAM Research Institute acquired 23andMe for USD 305 million, safeguarding consumer genetic data under charitable governance.

- February 2025: Hims & Hers bought Trybe Labs to embed whole-body lab testing into its subscription model.

- November 2024: WellRX acquired Bioreach Lab to deepen preventative-care capabilities

Global Direct-to-Consumer Laboratory Testing Market Report Scope

As per the scope of the report, direct-to-consumer (DTC) lab tests are pathology tests marketed directly to the public. Consumers purchase and choose which tests to access. DTC testing does not require the recommendation or referral from a consulting doctor nor the facilitation of a public health program. The direct-to-consumer laboratory testing is segmented into sample type, test type, and geography. By sample type, the market is segmented into blood, urine, saliva, and other sample types. By application, the market is segmented into routine clinical testing, diabetes testing, genetic testing, thyroid-stimulating hormone testing, and other applications (infectious diseases testing and pregnancy testing). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.

| Meditation & Mindfulness Apps |

| Digital Therapy Platforms |

| Emotion-sensing Wearables |

| VR/AR Mental Wellness Solutions |

| AI Chatbots & Companion Apps |

| Mobile Application |

| Web-based |

| In-person Hybrid |

| Anxiety & Stress |

| Depression |

| Sleep Disorders |

| PTSD & Trauma |

| Others |

| Individual Consumers |

| Enterprises & Employers |

| Healthcare Providers |

| Educational Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Meditation & Mindfulness Apps | |

| Digital Therapy Platforms | ||

| Emotion-sensing Wearables | ||

| VR/AR Mental Wellness Solutions | ||

| AI Chatbots & Companion Apps | ||

| By Delivery Mode | Mobile Application | |

| Web-based | ||

| In-person Hybrid | ||

| By Mental-health Condition | Anxiety & Stress | |

| Depression | ||

| Sleep Disorders | ||

| PTSD & Trauma | ||

| Others | ||

| By End-user | Individual Consumers | |

| Enterprises & Employers | ||

| Healthcare Providers | ||

| Educational Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Why is the FDA’s 2025 rule so important for direct-to-consumer tests?

The rule extends medical-device quality, reporting, and premarket review to most laboratory-developed tests, forcing companies to invest heavily in compliance yet providing long-term regulatory certainty.

How fast are sequencing costs falling?

Whole-genome sequencing averaged just above USD 500 in 2025 and is projected to reach USD 10 within a decade, unlocking wider adoption.

Which test category is growing the quickest?

Hormonal Wellness Panels are forecast to rise at an 11.89% CAGR through 2030 on heightened awareness of endocrine health.

What makes capillary blood devices a game changer?

Technologies like BD’s MiniDraw match venous-draw accuracy but require only a fingertip sample, removing a major barrier to blood-based home testing.

Page last updated on: