Direct-to-Consumer Genetic Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

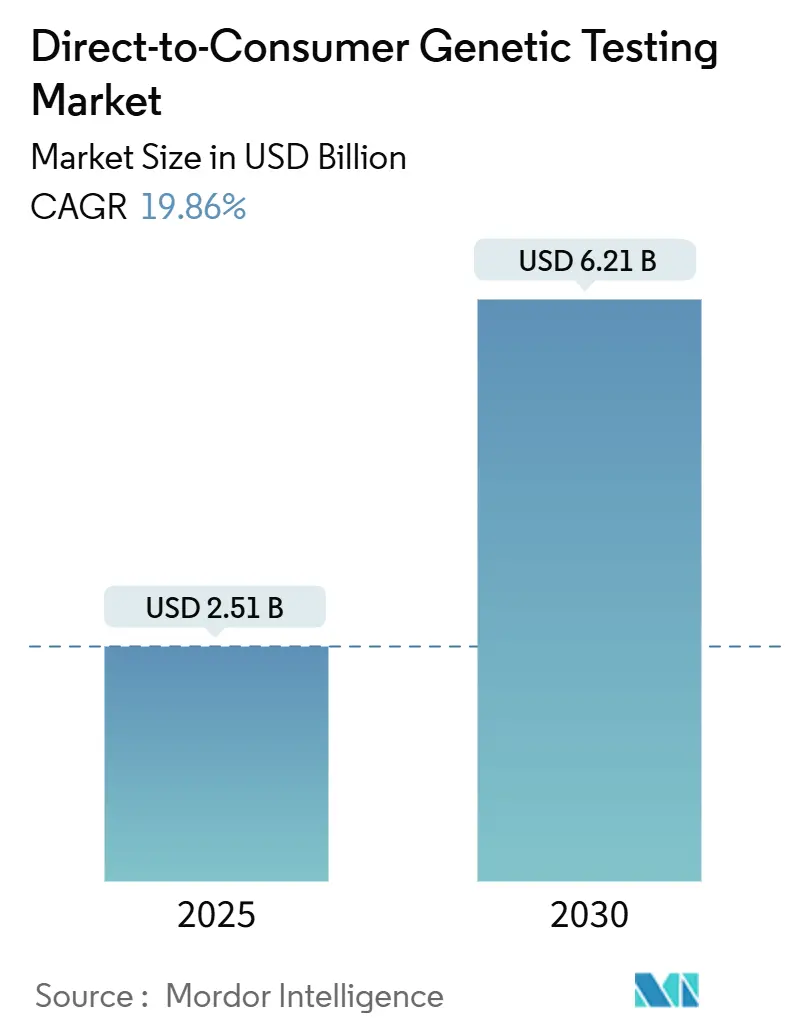

| Market Size (2025) | USD 2.51 Billion |

| Market Size (2030) | USD 6.21 Billion |

| Growth Rate (2025 - 2030) | 19.86% CAGR |

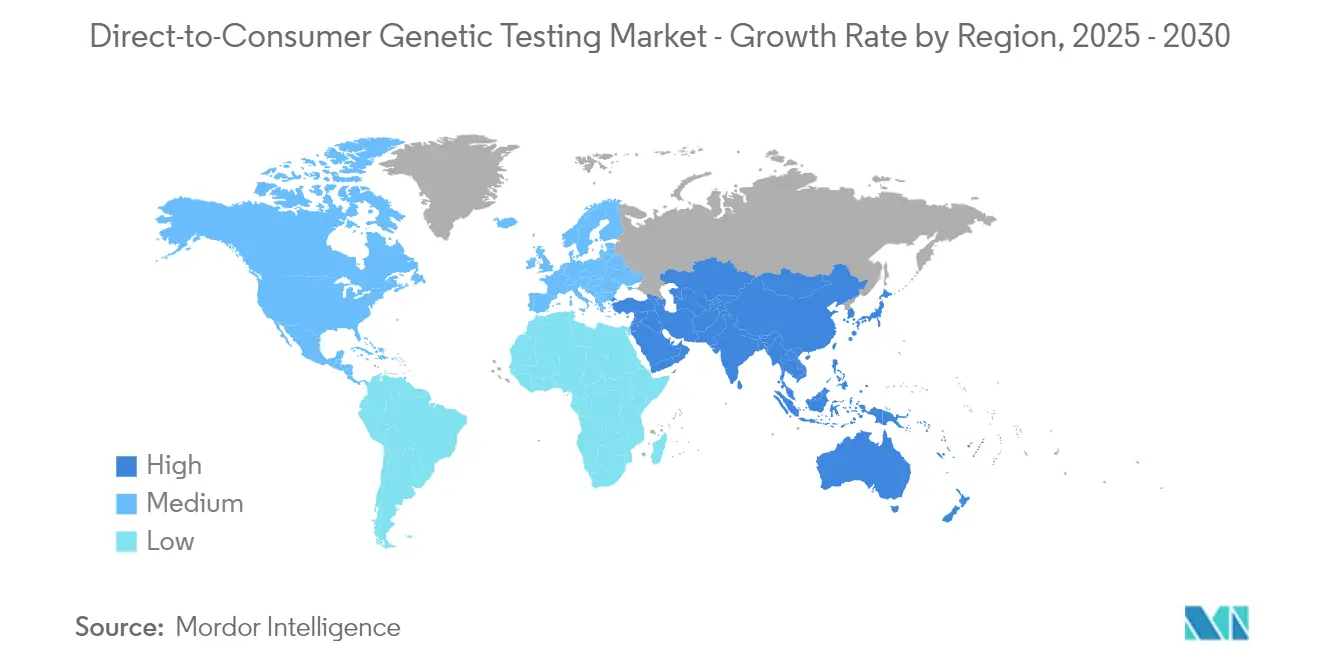

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct-to-Consumer Genetic Testing Market Analysis by Mordor Intelligence

The Direct-to-Consumer Genetic Testing Market size is estimated at USD 2.51 billion in 2025, and is expected to reach USD 6.21 billion by 2030, at a CAGR of 19.86% during the forecast period (2025-2030).

Direct-to-Consumer Genetic Testing Market Overview

The direct-to-consumer genetic testing industry has witnessed substantial transformation in recent years, driven by increasing consumer awareness and accessibility of genetic information. As per the data updated in December 2024 in the University of Texas Southwestern Medical Center, among the 6,252 respondents surveyed, 72% demonstrated awareness of ancestry testing, 55% were aware of testing for specific diseases, 37% recognized prenatal genetic carrier testing, and 25% were familiar with personal trait testing, demonstrating growing mainstream adoption. This widespread acceptance has led to enhanced competition among service providers, resulting in more affordable testing options and expanded service offerings. The industry has also experienced significant technological democratization, with companies increasingly focusing on user-friendly interfaces and comprehensive result interpretation services to make genetic information more accessible to the average consumer.

The medical community has shown strong support for integrating direct-to-consumer genetic testing into mainstream healthcare practices. Healthcare systems are increasingly developing protocols to incorporate DTC genetic test results into electronic health records, enabling more comprehensive patient care while maintaining data security and privacy standards.

Companies are increasingly leveraging targeted digital marketing strategies and strategic collaborations to build consumer trust and understanding. For instance, in June 2024, 23andMe Holding Co., a prominent player in preventive health and therapeutics, entered into a strategic collaboration with Nightingale Health Plc, a leader in biomarker testing and risk prediction. This partnership aims to pilot Nightingale's clinically validated and cost-efficient blood metabolomics panel with a selected cohort of 23andMe members. The industry has witnessed a shift toward more transparent communication about test capabilities and limitations, with providers offering more detailed explanations of scientific methodologies and result interpretations.

Regulatory frameworks and privacy considerations continue to shape the industry landscape, with varying approaches across different regions. Industry stakeholders are implementing enhanced data protection measures, including advanced encryption protocols and stringent access controls, to address growing privacy concerns. Companies are increasingly adopting transparent privacy policies and obtaining additional security certifications to build consumer trust, while also working closely with regulatory bodies to establish standardized guidelines for test accuracy and result reporting.

Global Direct-to-Consumer Genetic Testing Market Trends and Insights

Rapid Advancements in Genomic Technologies

The dramatic reduction in genetic sequencing costs has revolutionized access to genomic testing, with the cost of sequencing a human genome plummeting from approximately USD 100 million in 2001 to under USD 1,000 in 2023, as reported by the J. Craig Venter Institute. This remarkable cost reduction has been driven by breakthrough innovations in next-generation sequencing (NGS) technologies, including improved read lengths, higher throughput capabilities, and enhanced accuracy rates. The development of portable sequencing devices, miniaturized lab-on-chip platforms, and automated sample preparation systems has further accelerated the accessibility of genetic testing for consumers. These technological advances have also reduced turnaround times from weeks to just days, making direct-to-consumer genetic testing more convenient and practical for the average consumer.

The emergence of third-generation sequencing technologies like nanopore sequencing and single-molecule real-time (SMRT) sequencing has enabled real-time analysis of DNA sequences with unprecedented accuracy and speed. These innovations have expanded the scope of genetic testing beyond basic ancestry tracking to include comprehensive health screening, pharmacogenomics, and precision medicine applications. The integration of advanced bioinformatics tools and cloud computing platforms has also enhanced the ability to process and interpret complex genomic data, providing consumers with more detailed and actionable insights about their genetic makeup. Additionally, the development of non-invasive sampling methods and at-home collection kits has simplified the testing process, contributing to wider adoption of DTC genetic testing services.

Rising Consumer Interest in Personalized Healthcare

The growing awareness of personalized medicine and its potential benefits has sparked unprecedented consumer interest in genetic testing services. As per the article published in August 2024 in the Cureus journal, personalized medicine, by integrating genomics with clinical and familial histories, is transforming the healthcare landscape by enabling treatments tailored to individual patient characteristics. A key driver of this transformation is pharmacogenomics, which optimizes medication prescriptions based on genetic profiles, improving drug efficacy and safety. This precision medicine approach not only enhances disease diagnosis, prevention, and treatment but also aligns with the growing demand for direct-to-consumer genetic testing, which empowers individuals to access personalized healthcare solutions. Targeted therapies for conditions such as autoimmune disorders, rheumatoid arthritis, and certain cancers further underscore the market's potential. The increasing availability of educational resources and genetic counseling services has also empowered consumers to better understand and utilize their genetic information for making informed healthcare decisions, from preventive care strategies to lifestyle modifications based on genetic predispositions.

Consumer demand for personalized healthcare solutions has been further amplified by successful cases of early disease detection and prevention through genetic testing. This shift towards personalized medicine has been supported by increasing insurance coverage for genetic testing services and the development of more sophisticated interpretation tools that help consumers understand their genetic results in the context of their overall health profile. The integration of genetic information with digital health platforms and wellness apps has also made it easier for consumers to incorporate genetic insights into their daily health routines.

Growing Adoption of Artificial Intelligence in Genetic Analysis

The integration of artificial intelligence and machine learning technologies in genetic analysis has transformed the capability to process and interpret complex genomic data with unprecedented accuracy and efficiency. Advanced AI algorithms can now analyze millions of genetic variants simultaneously, identifying patterns and correlations that would be impossible to detect through traditional analysis methods. These AI-powered systems have significantly improved the accuracy of genetic risk assessments, enabling more precise predictions of disease susceptibility and drug responses. The implementation of deep learning models has also enhanced the ability to interpret variants of unknown significance (VUS), providing more comprehensive and actionable insights for consumers.

The convergence of AI with genetic testing has led to the development of sophisticated recommendation engines that can provide personalized health insights and actionable recommendations based on individual genetic profiles. These AI systems can continuously learn and update their algorithms as new genetic research becomes available, ensuring that consumers receive the most current and relevant information about their genetic predispositions. The application of natural language processing (NLP) has also improved the accessibility of genetic test results by translating complex genetic information into clear, understandable reports for consumers. Furthermore, AI-driven automation has streamlined the entire testing process, from sample processing to data analysis, reducing both costs and processing times while maintaining high accuracy standards.

Direct-to-Consumer Genetic Testing Market Test Type Segmental Analysis

Ancestry and Relationship Testing Segment in Direct-to-Consumer Genetic Testing Market

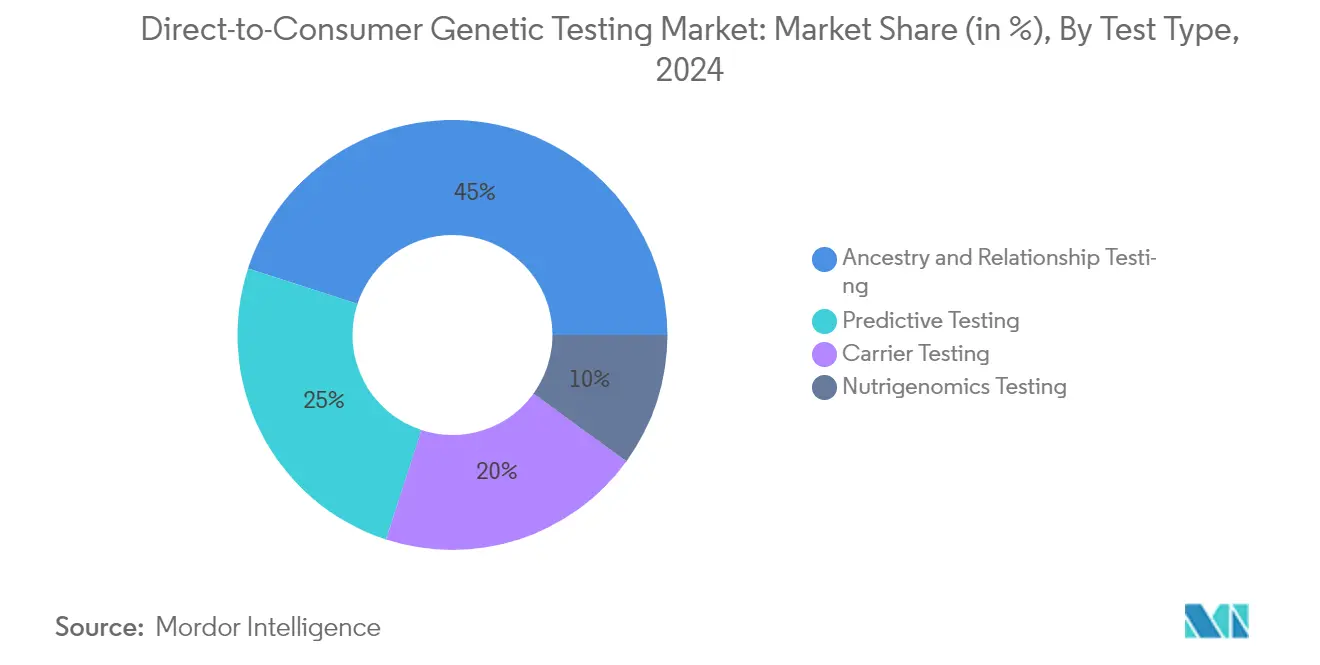

The ancestry and relationship testing segment maintains its dominant position in the direct-to-consumer genetic testing market, commanding approximately 45% of the market share in 2024. This segment's leadership is primarily driven by increasing consumer interest in discovering family heritage and genealogical connections. The widespread availability of comprehensive ancestry databases has significantly enhanced the accuracy and depth of results, making these tests more attractive to consumers. Major market players have invested heavily in marketing campaigns and educational initiatives to promote ancestry testing, further solidifying the segment's market position. The segment's success is also attributed to its relatively lower complexity and faster turnaround time compared to other genetic testing types. Additionally, the integration of advanced AI algorithms for more precise ancestral mapping and relationship identification has enhanced the value proposition for consumers. The segment benefits from strong word-of-mouth marketing and social media influence, as users often share their discovery experiences online.

Predictive Testing Segment in Direct-to-Consumer Genetic Testing Market

The predictive testing segment emerges as the fastest-growing category in the direct-to-consumer genetic testing market. This remarkable growth is fueled by increasing consumer awareness about preventive healthcare and the desire to understand personal genetic predispositions to various health conditions. The segment's expansion is supported by technological advancements in genomic sequencing and analysis, enabling more accurate and comprehensive predictive insights. Healthcare providers are increasingly recognizing the value of predictive genetic information in personalized medicine, contributing to broader acceptance and adoption. The integration of artificial intelligence and machine learning technologies has enhanced the accuracy and scope of predictive testing, making it more attractive to consumers. Rising healthcare costs and a growing emphasis on preventive care have also driven consumers to seek predictive genetic information for better health management. The segment's growth is further accelerated by expanding test portfolios and improving result interpretation capabilities.

Direct-to-Consumer Genetic Testing Market Technology Type Segmental Analysis

Genotyping Arrays Segment in Direct-to-Consumer Genetic Testing Market

Genotyping arrays currently dominate the direct-to-consumer genetic testing market. This significant market position is primarily attributed to the technology's cost-effectiveness and ability to analyze thousands of genetic variants simultaneously. The segment's prominence is further strengthened by its widespread adoption among major direct-to-consumer genetic testing companies, particularly for ancestry testing and health risk assessments. The scalability of array technology, combined with its established infrastructure and standardized protocols, has made it the preferred choice for high-throughput genetic testing applications. Additionally, recent improvements in array design and analysis algorithms have enhanced the accuracy and reliability of results, contributing to sustained market leadership. The segment's strong performance is also supported by increasing consumer awareness and the growing popularity of genetic testing for personal health management and genealogical research.

Whole Genome Sequencing Segment in Direct-to-Consumer Genetic Testing Market

Whole genome sequencing (WGS) emerges as the fastest-growing segment in the direct-to-consumer genetic testing market. This remarkable growth trajectory is driven by rapid technological advancements that have significantly reduced sequencing costs while improving accuracy and throughput capabilities. The segment's expansion is further fueled by increasing consumer demand for comprehensive genetic information and the rising adoption of precision medicine approaches. Recent innovations in artificial intelligence and machine learning applications for WGS data analysis have enhanced the technology's clinical utility and accessibility. The integration of cloud computing solutions has also streamlined data processing and storage capabilities, making WGS more practical for commercial applications. Moreover, the segment's growth is supported by expanding applications in rare disease diagnosis, pharmacogenomics, and personalized healthcare planning, positioning WGS as a transformative force in the direct-to-consumer genetic testing landscape.

Direct-to-Consumer Genetic Testing Market Distribution Channel Segmental Analysis

Online Platforms Segment in Direct-to-Consumer Genetic Testing Market

The online platforms segment has emerged as the dominant distribution channel in the direct-to-consumer genetic testing market. This segment's supremacy is primarily attributed to the increasing consumer preference for convenient, direct-to-home genetic testing services. The digital transformation of healthcare services, coupled with the widespread adoption of e-commerce platforms, has significantly contributed to this segment's dominance. Online platforms offer consumers the advantage of discrete purchasing, detailed product information, and often competitive pricing through various promotional strategies. Additionally, these platforms provide enhanced user experience through interactive interfaces, educational resources, and seamless integration with genetic counseling services.

Over-the-Counter (OTC) Channels Segment in Direct-to-Consumer Genetic Testing Market

The over-the-counter (OTC) channels segment represents a crucial traditional distribution channel in the direct-to-consumer genetic testing market, offering consumers the ability to purchase genetic testing kits through physical retail locations. This segment has maintained its relevance by providing immediate access to products and face-to-face consultation opportunities with healthcare professionals at pharmacies and specialized medical stores. The OTC channel has evolved to incorporate hybrid models, combining physical presence with digital support services to enhance customer experience. Recent developments include the integration of QR codes on packaging for accessing digital resources, partnerships with local healthcare providers for result interpretation, and the implementation of in-store educational programs. The segment has also benefited from strategic collaborations with major pharmacy chains and healthcare retailers, expanding its accessibility to diverse consumer demographics. Despite facing competition from online platforms, OTC channels continue to serve as an important touchpoint for consumers who prefer traditional purchasing methods or require immediate access to genetic testing products.

Direct-to-Consumer Genetic Testing Market Geographical Analysis

Direct-to-Consumer Genetic Testing Market in North America

North America has established itself as the dominant force in the direct-to-consumer genetic testing market, commanding approximately 62% of the global market share in 2024. The region's leadership position can be attributed to several key factors, including advanced healthcare infrastructure and high consumer awareness about genetic testing benefits. The presence of major market players and their robust distribution networks has significantly contributed to market penetration. The region's regulatory framework, particularly in the United States, has evolved to accommodate direct-to-consumer genetic testing while maintaining quality standards. Strong healthcare reimbursement policies and increasing integration of genetic testing results in preventive healthcare approaches have further strengthened market growth. Additionally, the rising adoption of personalized medicine and growing consumer interest in ancestry testing have created a favorable market environment. The region's technological advancement in genomic sequencing and data analysis capabilities has also played a crucial role in market development.

Direct-to-Consumer Genetic Testing Market in Europe

Europe has demonstrated remarkable progress in the direct-to-consumer genetic testing market, emerging as a key growth region. The market has experienced substantial expansion driven by increasing acceptance of personalized treatments and growing awareness about genetic disorders. The region's sophisticated healthcare systems and strong research infrastructure have facilitated market development. European countries have implemented comprehensive regulatory frameworks to ensure consumer protection while promoting innovation in genetic testing services. The presence of well-established biotechnology companies and research institutions has fostered technological advancements in genetic testing methodologies. Growing collaborations between healthcare providers and genetic testing companies have enhanced market penetration. The region's focus on preventive healthcare and increasing consumer interest in understanding genetic predispositions has further accelerated market growth. Additionally, the rise in genetic counseling services and improved accessibility to testing facilities has contributed to market expansion.

Direct-to-Consumer Genetic Testing Market in Asia-Pacific

The Asia-Pacific region is poised for substantial growth in the direct-to-consumer genetic testing market. The region's market dynamics are shaped by rapid technological adoption and increasing healthcare awareness among consumers. Growing disposable income levels and expanding middle-class populations have created new opportunities for market expansion. The region has witnessed significant investments in healthcare infrastructure and genetic research facilities. Countries like Japan, China, and South Korea are leading the adoption of advanced genetic testing technologies. Rising awareness about preventive healthcare and genetic predispositions to diseases has fueled market growth. The presence of large population bases and increasing healthcare expenditure has attracted international players to establish their presence in the region. Additionally, government initiatives supporting genetic research and personalized medicine have created a conducive environment for market development.

Direct-to-Consumer Genetic Testing Market in Middle East and Africa

The Middle East and Africa region presents untapped potential in the direct-to-consumer genetic testing market, with growing healthcare awareness and increasing investments in medical infrastructure. The market is characterized by the rising adoption of advanced healthcare technologies, particularly in Gulf Cooperation Council countries. Growing initiatives to modernize healthcare systems and increase accessibility to genetic testing services have supported market development. The region's unique genetic composition and high prevalence of genetic disorders have created specific opportunities for market growth. Healthcare tourism in countries like the GCC and South Africa has contributed to increased awareness and adoption of genetic testing services. The region has witnessed growing partnerships between international genetic testing companies and local healthcare providers. Rising consumer awareness about preventive healthcare and personalized medicine has stimulated market growth. Additionally, government initiatives to improve healthcare services and increase technological adoption have created a favorable environment for market expansion.

Direct-to-Consumer Genetic Testing Market in South America

South America represents an emerging market for direct-to-consumer genetic testing, characterized by growing healthcare awareness and increasing adoption of advanced medical technologies. The region's market is driven by improving healthcare infrastructure and rising consumer interest in personalized medicine. Countries like Brazil and Argentina are leading the regional market growth through increased healthcare spending and adoption of genetic testing services. The presence of diverse genetic pools and growing research activities in genetic diseases has created unique opportunities for market expansion. Healthcare providers in the region are increasingly incorporating genetic testing in their service offerings. Rising awareness about hereditary diseases and preventive healthcare approaches has stimulated market growth. The region has also witnessed increasing collaborations between international genetic testing companies and local healthcare providers, enhancing market accessibility and service quality.

Competitive Landscape

Top Companies in Direct-to-Consumer Genetic Testing Market

The direct-to-consumer genetic testing market is led by prominent players including 23andMe, Ancestry, Color Health, EasyDNA, Family Tree DNA, Full Genomes Corporation, Living DNA and MyHeritage. These companies have demonstrated consistent focus on product innovation through enhanced testing capabilities and expanded genetic markers coverage. Market leaders are increasingly investing in artificial intelligence and machine learning capabilities to improve test accuracy and provide more comprehensive health insights. Strategic partnerships with healthcare providers and research institutions have become a common approach to strengthen market positions and expand service offerings. Companies are also focusing on geographical expansion through both organic growth and strategic acquisitions, while simultaneously working on making their testing services more accessible and affordable to broader consumer segments.

Consolidation and Competition Shape Market Dynamics

The direct-to-consumer genetic testing market exhibits a moderately consolidated structure, with global players holding significant market share while regional specialists maintain strong presence in specific geographical areas. The market is characterized by a mix of large biotechnology conglomerates and specialized genetic testing companies, each bringing unique strengths to the competitive landscape. Large companies leverage their extensive research capabilities and established distribution networks, while specialized firms often excel in niche areas such as ancestry testing or specific health conditions. The industry has witnessed numerous strategic mergers and acquisitions, primarily aimed at expanding testing capabilities, accessing new geographical markets, and acquiring innovative technologies.

Recent years have seen increased collaboration between traditional genetic testing companies and healthcare providers, creating a more integrated approach to consumer genetic services. Market leaders are actively pursuing vertical integration strategies, developing in-house capabilities for sample processing, data analysis, and result interpretation. The competitive dynamics are further influenced by the entry of pharmaceutical companies and healthcare providers into the direct-to-consumer genetic testing space, leading to increased competition and service diversification.

Innovation and Adaptation Drive Future Success

Success in the direct-to-consumer genetic testing market increasingly depends on companies' ability to differentiate their offerings through technological innovation and comprehensive service packages. Market leaders must focus on developing proprietary testing technologies, expanding their genetic databases, and enhancing data security measures to maintain their competitive edge. Companies need to balance between offering standardized testing services and providing personalized genetic insights, while maintaining compliance with evolving regulatory requirements. The ability to form strategic partnerships with healthcare providers, research institutions, and technology companies will become increasingly crucial for maintaining market relevance and expanding service offerings.

For emerging players and contenders, success lies in identifying and serving underserved market segments or geographical regions with unique genetic testing needs. Companies must invest in developing user-friendly platforms and educational resources to help consumers understand and act upon their genetic information. The industry faces ongoing challenges related to privacy concerns, regulatory compliance, and maintaining consumer trust, making it essential for companies to establish robust data protection measures and transparent practices. Future market success will also depend on companies' ability to adapt to changing consumer preferences, integrate new technologies, and maintain competitive pricing while ensuring service quality.

Direct-to-Consumer Genetic Testing Industry Leaders

23andMe

Ancestry

Color Health

EasyDNA

Family Tree DNA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: 23andMe Holding Co., a prominent player in human genetics, unveiled a polygenic risk score (PRS) report focused on osteoporosis exclusively for its 23andMe+ Premium members. Leveraging its proprietary research database, 23andMe crafted a statistical model to gauge customers' susceptibility to osteoporosis. The report not only highlights this risk but also offers actionable lifestyle recommendations to mitigate it. By analyzing an individual's genetic markers, ancestry, and birth sex, the report estimates the likelihood of developing osteoporosis.

- November 2024: ProPhase Labs, Inc., a prominent biotech, genomics, and diagnostics firm, launched DNA Complete, Inc., its wholly owned subsidiary. DNA Complete introduces an advanced direct-to-consumer DNA testing service that sequences nearly 100% of a customer’s genome, delivering comprehensive insights into health, wellness, and ancestry.

- November 2024: ProPhase Labs introduced DNA Complete, a comprehensive whole genome sequencing service designed to provide actionable insights into health, wellness, and ancestry. The offering includes advanced bioinformatics, access to genetic counseling, and a subscription-based model. Additionally, the company launched DNA Expand, a value-added feature that enhances existing DNA ancestry data with 50 times more information, available through an annual subscription priced at USD 49.95.

Global Direct-to-Consumer Genetic Testing Market Report Scope

As per the scope of the report, direct-to-consumer genetic tests are directly marketed to consumers through channels such as television, radio, print advertisements, and online platforms. Customers can purchase these kits either online or in retail stores. After acquiring a test kit, they submit their DNA sample to the company and receive their results through a secure website, app, or a written report. This model enables individuals to access their genetic data without requiring the involvement of healthcare providers or insurance companies.

The direct-to-consumer genetic testing market is segmented into test type, technology type, distribution channel and geography. By test type, the market is segmented into predictive testing, carrier testing, nutrigenomics testing, and ancestry and relationship testing. By technology type, the market is segmented into whole genome sequencing, genotyping arrays, PCR and targeted sequencing. By distribution channel, the market is segmented into online platforms and over-the-counter (OTC) channels). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD) for the above segments.

| Predictive Testing |

| Carrier Testing |

| Nutrigenomics Testing |

| Ancestry and Relationship Testing |

| Whole Genome Sequencing |

| Genotyping Arrays |

| PCR and Targeted Sequencing |

| Online Platforms |

| Over-the-Counter (OTC) Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Predictive Testing | |

| Carrier Testing | ||

| Nutrigenomics Testing | ||

| Ancestry and Relationship Testing | ||

| By Technology Type | Whole Genome Sequencing | |

| Genotyping Arrays | ||

| PCR and Targeted Sequencing | ||

| By Distribution Channel | Online Platforms | |

| Over-the-Counter (OTC) Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Direct-to-Consumer Genetic Testing Market?

The Direct-to-Consumer Genetic Testing Market size is expected to reach USD 2.51 billion in 2025 and grow at a CAGR of 19.86% to reach USD 6.21 billion by 2030.

What is the current Direct-to-Consumer Genetic Testing Market size?

In 2025, the Direct-to-Consumer Genetic Testing Market size is expected to reach USD 2.51 billion.

Which is the fastest growing region in Direct-to-Consumer Genetic Testing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Direct-to-Consumer Genetic Testing Market?

In 2025, the North America accounts for the largest market share in Direct-to-Consumer Genetic Testing Market.

What years does this Direct-to-Consumer Genetic Testing Market cover, and what was the market size in 2024?

In 2024, the Direct-to-Consumer Genetic Testing Market size was estimated at USD 2.01 billion. The report covers the Direct-to-Consumer Genetic Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Direct-to-Consumer Genetic Testing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: