Direct Current (DC) Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.44 Billion |

| Market Size (2031) | USD 46.27 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

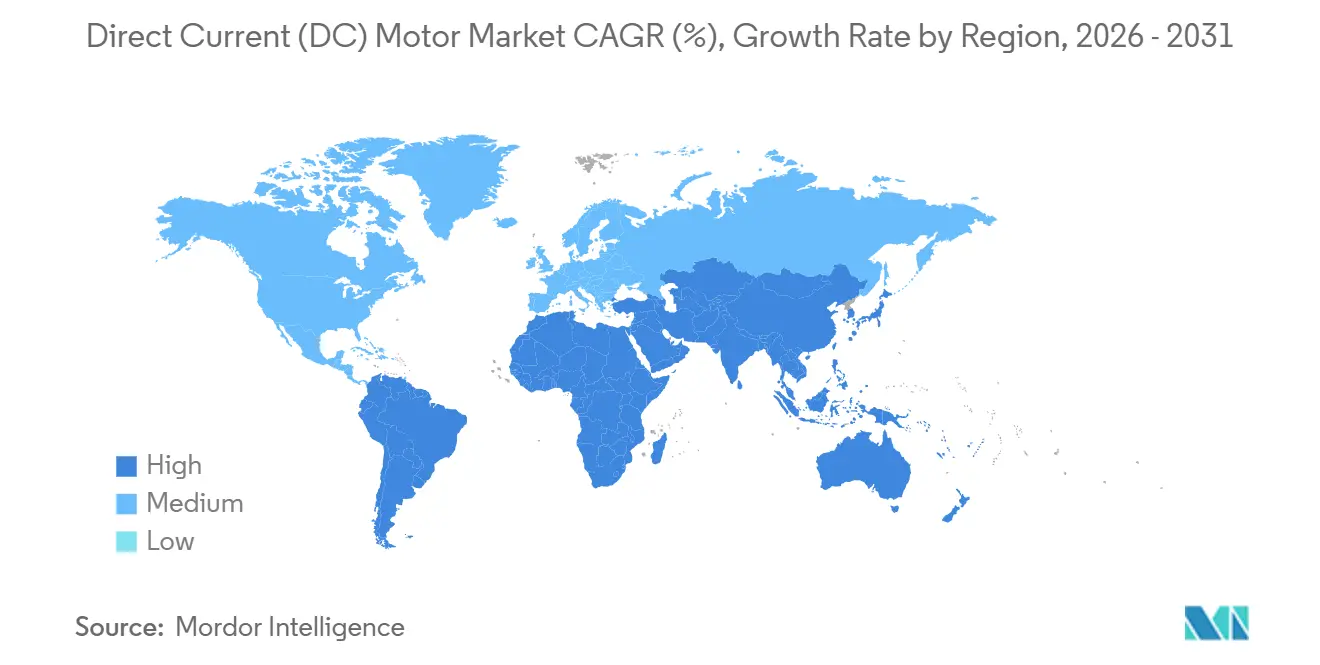

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

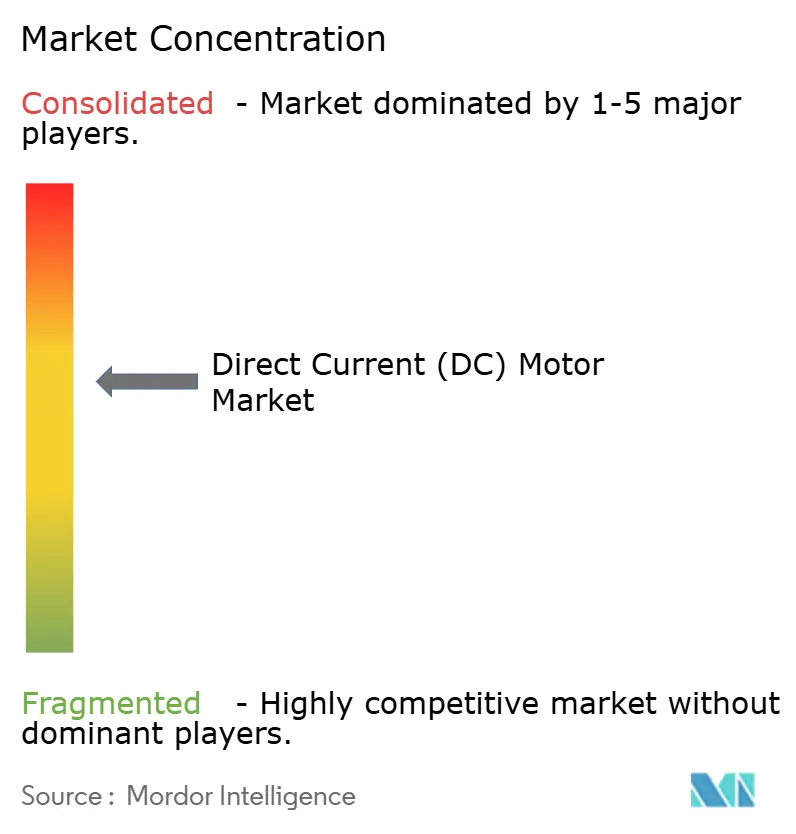

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct Current (DC) Motor Market Analysis by Mordor Intelligence

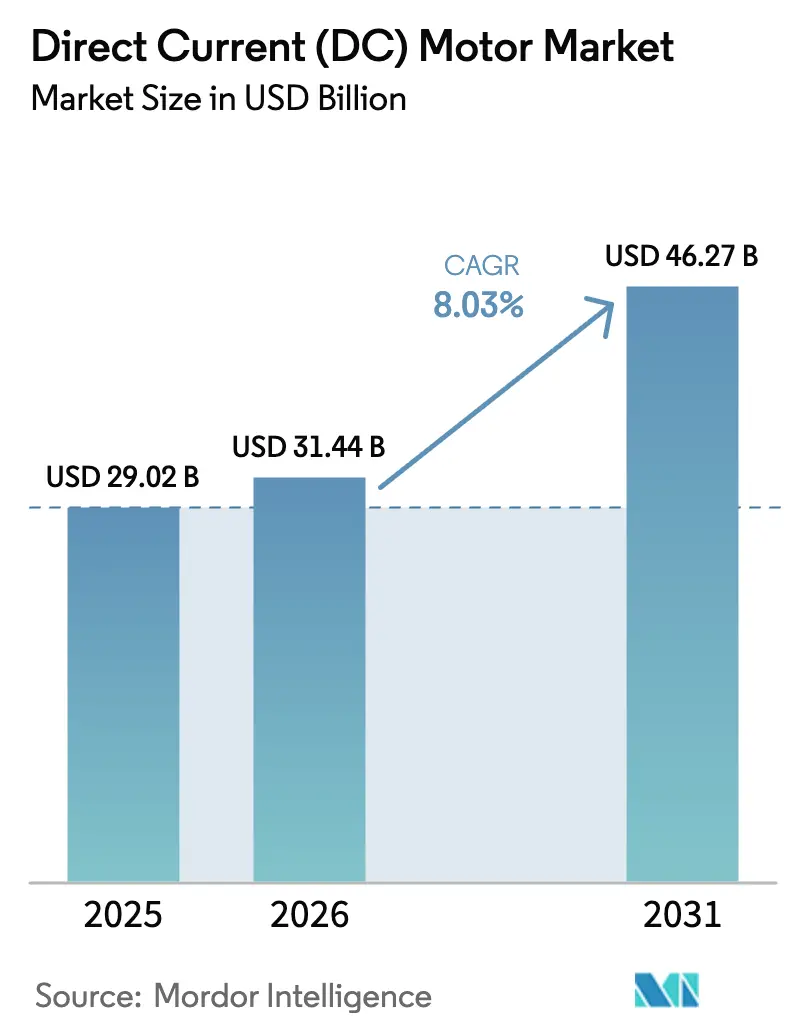

The Direct Current (DC) Motor market size is projected to be USD 29.02 billion in 2025, USD 31.44 billion in 2026, and reach USD 46.27 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031. Proliferation of battery-electric vehicles, tighter industrial efficiency mandates, and the rapid spread of IoT-enabled predictive-maintenance software are reshaping the competitive field. Automakers are rolling out 48-volt electrical architectures that cut copper mass and open room for steer-by-wire actuators, while factory operators in Asia-Pacific and Europe are retiring legacy AC induction drives in favor of brushless DC (BLDC) units that meet IE4 and IE5 efficiency classes. HVAC retrofits in North America are pivoting toward electronically commutated BLDC fans to unlock 30–50% energy savings. Manufacturers that combine vertically integrated magnet supply with digital-twin design tools are capturing early-mover advantages in both automotive and industrial end-markets.

Key Report Takeaways

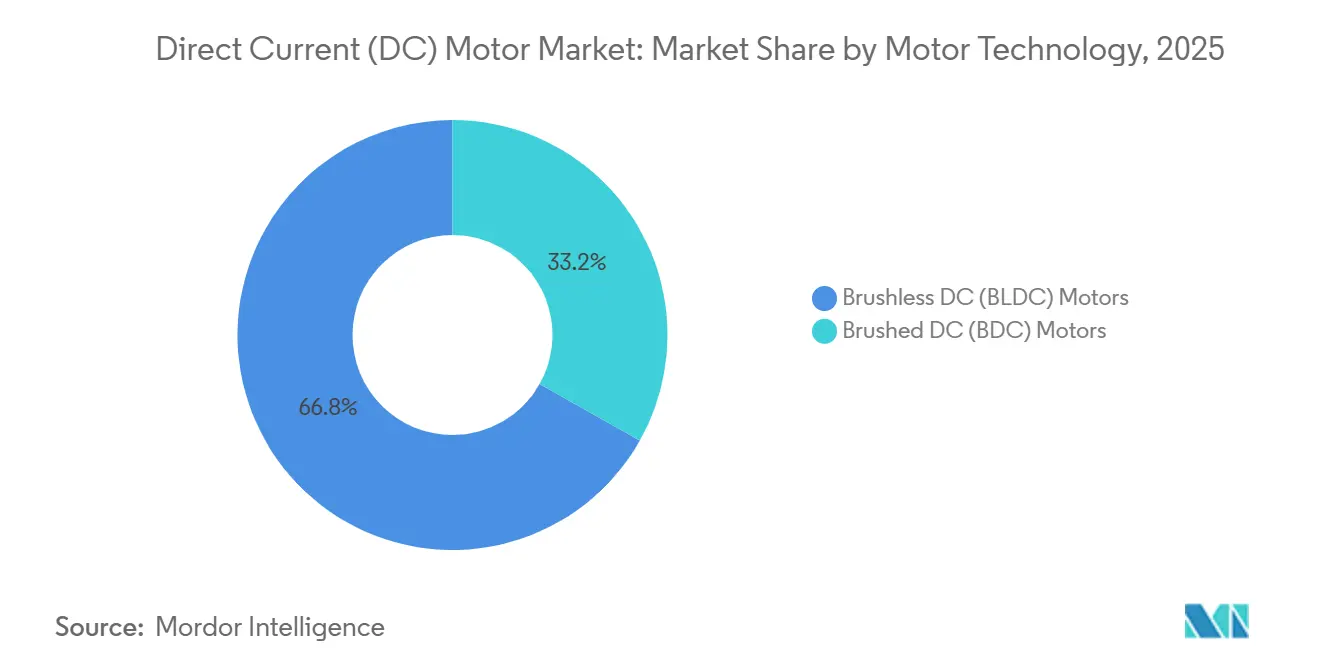

- By motor technology, brushless DC motors led with 66.83% of Direct Current (DC) Motor market share in 2025 and are forecast to advance at an 8.11% CAGR through 2031.

- By power rating, units below 75 watts held 56.72% revenue in 2025, but drives above 75 kilowatts record the fastest 8.06% CAGR through 2031.

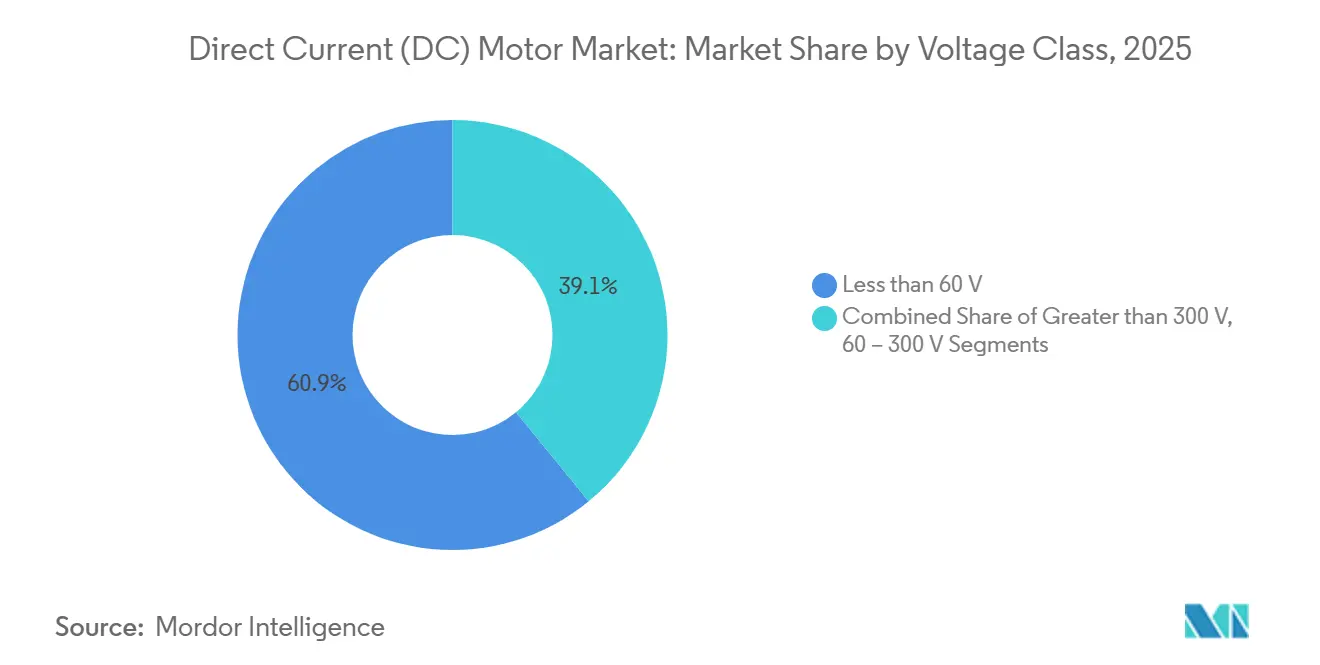

- By voltage class, systems below 60 volts dominated at 60.93% in 2025, whereas motors above 300 volts are expanding at an 8.22% CAGR on the back of electric buses and grid-scale storage.

- By end-use industry, industrial automation commanded 30.26% of 2025 revenue, yet automotive and transportation is the fastest-growing segment at an 8.31% CAGR through 2031.

- By geography, Asia-Pacific contributed 48.84% of global 2025 turnover, while North America is set to post the highest regional CAGR of 8.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Direct Current (DC) Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Electric Vehicles | +2.1% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Transition to Energy-Efficient Industrial Automation | +1.8% | Global, led by Asia-Pacific manufacturing hubs and Europe | Long term (≥4 years) |

| Growing HVAC Retrofit Demand for BLDC Fans and Blowers | +1.2% | North America and Europe, emerging in Middle East | Medium term (2-4 years) |

| Government Incentives for High-Efficiency Motors | +1.0% | North America, Europe, China, India | Short term (≤2 years) |

| 48-Volt Electrical Architectures in Light-Duty Vehicles | +0.9% | North America, Europe, China | Medium term (2-4 years) |

| IoT-Enabled Smart DC Motor Modules | +0.7% | Global, early adoption in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Electric Vehicles

Global battery-electric vehicle output surpassed 14 million units in 2025, and each vehicle now integrates 30–50 BLDC motors for traction, steering, and thermal management—triple the count found in combustion models.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Chinese brands BYD and Geely vertically integrated motor production to shield margins, while European OEMs move to 800-volt platforms that require high-voltage BLDC motor-generators for rapid charging. Tesla’s 48-volt low-voltage network trims 1.5 kilometers of copper wiring per pickup and anchors steer-by-wire designs that rely solely on BLDC actuators.[2]Tesla Inc., “Cybertruck Engineering and Design,” tesla.com Tier-1 suppliers such as Bosch and Continental have unveiled dedicated 48-volt motor families, and outer-rotor BLDC designs are entering wheel-hub use cases in compact urban cars.

Transition to Energy-Efficient Industrial Automation

Industrial buyers are retiring AC induction motors where variable-speed duty cycles prevail. BLDC drives surpass IE4 and IE5 standards, delivering 5–8 percentage-point efficiency gains at partial loads. ABB’s smart motor suite uses vibration and thermal analytics to trim unplanned stoppages by up to 40% in automotive plants.[3]ABB Ltd., “ABB Ability Digital Solutions for Motors,” abb.com Siemens’ digital-twin software lets engineers simulate energy use before purchase, supporting evidence-based capital allocation. Adoption is strongest across Asia-Pacific, where China’s dual-carbon plan targets a 13.5% cut in energy intensity by 2025.

Growing HVAC Retrofit Demand for BLDC Fans and Blowers

Commercial property owners in the United States and Europe are swapping permanent-split capacitor motors for electronically commutated BLDC fans that deliver 30–50% electricity savings with sub-three-year paybacks. Nidec’s EC motor line couples variable-frequency drives with occupancy sensors to modulate airflow, easing peak-demand tariffs. The efficiency proposition has migrated to data-center cooling where BLDC blowers lift power-usage effectiveness scores. Middle Eastern district-cooling operators are beginning similar transitions as 24/7 demand underscores lifetime energy cost advantages.

Government Incentives for High-Efficiency Motors

Fiscal measures are shortening ROI cycles. India’s Energy Efficient Solutions for MSMEs scheme subsidizes up to 50% of incremental capex for IE4 upgrades in small enterprises. China’s Top Runner catalog bars sub-IE4 motors from public procurement, and the European Union is phasing IE5 mandates for select power bands by 2027. The United States offers accelerated depreciation for high-efficiency motor retrofits under the Inflation Reduction Act. Incentives amplify demand for certified BLDC portfolios and reward suppliers with accredited testing capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Cost Versus AC Induction Alternatives | -1.3% | Global, most acute in price-sensitive emerging markets | Short term (≤2 years) |

| Supply-Chain Volatility of Rare-Earth Magnets | -1.1% | Global, with acute impact on North America and Europe | Medium term (2-4 years) |

| EMC/EMI Compliance Hurdles for High-Switch-Frequency Drives | -0.6% | Global, particularly stringent in Europe and North America | Medium term (2-4 years) |

| Thermal-Management Limits in Compact High-Power Designs | -0.5% | Global, critical in automotive and aerospace | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus AC Induction Alternatives

BLDC units cost 20–40% more than equivalent AC induction motors, deterring uptake in capital-constrained industries. Although total cost of ownership favors BLDC at utilization levels above 4,000 hours per year, procurement teams in India and Southeast Asia often select the lowest headline bid, slowing replacement cycles. Leasing and energy-as-a-service contracts are emerging to bridge capex gaps, yet penetration remains uneven across fragmented industrial user bases.

Supply-Chain Volatility of Rare-Earth Magnets

China controls more than 90% of neodymium-iron-boron refining capacity, and export curbs in 2024 drove spot prices up by 35–50%, squeezing motor OEM margins. Some suppliers redesigned products around ferrite magnets, sacrificing 15–20% torque density. The United States has mapped domestic mining projects, but commercial output is unlikely before 2028, leaving OEMs exposed to further volatility. European manufacturers are piloting magnet-recycling lines, yet reclaimed volumes cover less than 5% of annual demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Technology: BLDC Dominance Driven by Efficiency Mandates

Brushless DC drives captured 66.83% of Direct Current (DC) Motor market share in 2025 and are on track for an 8.11% CAGR through 2031. Inner-rotor BLDC architectures prevail in traction motors and CNC spindles because their stator-to-housing path expedites heat removal, while outer-rotor options are scaling in wheel-hub applications that need high torque at low speed. Brushed DC variants retained 33.17% share by serving cost-driven starter-motor and power-tool niches, yet rising CAFE penalties are steering automakers toward BLDC solutions. Sensorless control algorithms have shaved USD 2–5 from per-unit bills, widening adoption across ceiling-fan and refrigerator compressors.

Elevated efficiency ceilings help BLDC units qualify for IE4 and IE5 ratings that brushed designs cannot meet above 750 watts. As governments tighten minimum-performance rules, brushed motor production lines face obsolescence, and several tier-2 vendors are pivoting toward aftermarket spares. Premium BLDC suppliers differentiate with direct-winding cooling and oil-spray housings that enable sustained duty in traction motors at power densities beyond 10 kilowatts per liter.

By Power Rating: Micro-Motors Lead Volume While High-Power Drives Fuel Value Growth

Motors under 75 watts accounted for 56.72% of shipments in 2025, buoyed by smartphones, medical infusion pumps, and automotive micro-actuators. BLDC is displacing coreless brushed types in these categories to extend battery life and cut electromagnetic interference with radios. The 0.75–75 kilowatt bracket serves industrial conveyors and commercial HVAC where variable-speed savings recoup premiums within five years. The >75 kilowatt tier is the fastest-growing, expanding at an 8.06% CAGR as electric buses, mining conveyors, and water-treatment plants demand high-efficiency continuous-duty drives.

Electric submersible pumps in offshore wells are adopting BLDC to lift fluid volumes 8–12% more efficiently than induction alternatives, and water utilities report paybacks under four years for BLDC retrofits in 24/7 operations. Thermal constraints above 50 kilowatts are being tackled with liquid-cooling jackets and aluminum-nitride heat sinks, although weight penalties still curb deployment in aerospace where power-to-mass ratios must top 5 kilowatts per kilogram.

By Voltage Class: Low-Voltage Dominance, High-Voltage Rapid Upswing

Sub-60-volt models held 60.93% revenue in 2025, anchored by battery-powered tools and consumer devices. The rise of 48-volt mild-hybrid vehicles is enlarging this slice; belt-starter-generators and active-suspension actuators draw 5–10 kilowatts during acceleration bursts. Motors working at 60–300 volts address industrial automation and VRF HVAC, where integrated variable-frequency drives enable regenerative braking. The >300-volt cohort is poised for an 8.22% CAGR through 2031 as electric buses and grid-scale inverters migrate to 400–800 volt rails to curb I²R losses.

High-voltage BLDC variants must comply with IEC 61800-3 Category C2 electromagnetic rules, prompting vendors to bundle shielded cables and common-mode filters. Tesla’s 48-volt wiring layout proved that low-voltage networks can shrink copper use by 40 kilograms per pickup, and suppliers such as Valeo and Bosch have followed with integrated 48-volt drive modules.

By End-Use Industry: Automation Commands Value, Automotive Fuels Growth

Industrial machinery and automation captured 30.26% of 2025 turnover, reflecting deep penetration in CNC lathes, robotic arms, and AGVs where closed-loop speed control lifts throughput and quality. Automotive is the fastest climber at an 8.31% CAGR through 2031 because battery-electric models need three times as many motors as combustion vehicles. HVAC systems are swapping permanent-split capacitor motors for BLDC compressors and blowers that trim building-energy bills by up to 50%.

Surgical-robot makers specify autoclave-ready coreless BLDC units from Maxon to meet ISO 13485 sterilization rules. Portescap’s insulin-pump motors combine low acoustic noise with magnetic shielding to protect implantable sensors. Oil-and-gas players use BLDC drives in subsea pumps for variable-speed lift, and wind-farm operators rely on BLDC pitch-control actuators for precise blade alignment in offshore turbines.

Geography Analysis

Asia-Pacific delivered 48.84% of global revenue in 2025, underpinned by China’s cradle-to-grave motor supply chain stretching from rare-earth mining to final vehicle integration. The country produced over 9 million battery-electric cars in 2025, sustaining robust domestic demand and exports across Southeast Asia. Japan’s precision suppliers—Nidec, MinebeaMitsumi, and Mabuchi—dominate micro-motor exports on the back of ultra-tight winding tolerances. India’s Bureau of Energy Efficiency star-rating program plus Make in India incentives are luring fresh capital into domestic production. South Korea’s semiconductor-equipment builders favor BLDC for vibration-sensitive stages, adding high-margin demand.

North America is forecast to clock the highest 8.38% CAGR through 2031. The Inflation Reduction Act offers tax credits for motor retrofits, while Detroit-based automakers have earmarked USD 50 billion for domestic battery and motor lines to derisk supply chains. Canada sees uptake in mining conveyors and hydrocarbon pumps in remote areas with high power costs. Mexico has become a regional export base after Nidec’s USD 1 billion Nuevo León complex came online in 2025.

Europe’s path is steered by the Ecodesign Directive 2019/1781 that bans sub-IE4 motors in new installs, steering factories toward BLDC and synchronous-reluctance designs. Germany’s automotive suppliers accelerate R and D in integrated motor-drive modules, and the United Kingdom’s offshore wind build-out creates demand for low-maintenance yaw systems. France and Spain drive HVAC retrofits in commercial real estate, aided by utility rebates that shorten paybacks to under three years. South America is weighed down by macro volatility, yet Brazil’s mining and agricultural sectors provide pockets of opportunity. GCC economies deploy BLDC in desalination plants and district cooling where round-the-clock duty magnifies energy savings.

Competitive Landscape

The Direct Current (DC) Motor market exhibits moderate concentration, Nidec, ABB, Siemens, Bosch, and Yaskawa together hold roughly 35–40% revenue, leaving space for regional and niche innovators. Nidec’s USD 1.8 billion Serbian traction-motor campus demonstrates the scale needed to serve European OEMs that demand annual lots above 1 million units. ABB and Siemens differentiate through IoT suites Ability and MindSphere that integrate condition-monitoring analytics and cut downtime by up to 40% in high-volume plants.

Emerging Chinese automakers have vertically integrated motor lines to lock in rare-earth supply and squeeze cost from drivetrain bills. Technology rivalry orbits three vectors: sensorless control that removes Hall sensors, oil-splash cooling that raises continuous ratings, and magnet-free switched-reluctance designs that sidestep supply-chain risk. Patent data from 2025 shows an uptick in filings for combined motor-drive packages that merge power electronics with mechanical housing for EMI compliance.

Barriers to entry are rising as IE4 and IE5 certifications demand extensive lab tests. Suppliers owning accredited facilities gain speed-to-market advantages. Mid-tier brands compete on customization—surgical robots, aerospace actuators, and subsea pumps—where volume is low but margins exceed 25%. The absence of a single dominant player leaves ample runway for disruptive entrants with thermal-simulation expertise or captive magnet recycling.

Direct Current (DC) Motor Industry Leaders

ABB Ltd.

Allied Motion Technologies Inc.

AMETEK Inc.

Delta Electronics Inc.

FAULHABER Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nidec Corporation allocated EUR 800 million for a new electric-vehicle motor factory in Hungary, broadening European capacity for 48 V and BLDC traction units to meet rising demand from regional automakers.

- July 2025: ABB unveiled a smart-motor platform that uses AI-driven vibration and temperature analytics to help industrial plants cut unplanned downtime by up to 40%.

- May 2025: Siemens AG secured a USD 650 million supply contract for BLDC drives that will power solar trackers and wind-turbine pitch systems in the expanding renewable-energy parks of Brazil and Argentina.

- January 2025: Nidec completed a USD 1.8 billion Serbian plant with 1.2 million-unit traction-motor capacity and in-house magnet production for Stellantis and Renault.

Global Direct Current (DC) Motor Market Report Scope

A Direct Current (DC) motor is an electric motor that converts direct electrical energy (DC) into mechanical rotation. It works using the principle that a current-carrying conductor placed in a magnetic field experiences a force, causing motion.

The Direct Current (DC) Motor Market Report is Segmented by Motor Technology (Brushed DC, Brushless DC), Power Rating (Less than 75 W, 75-750 W, 0.75-75 kW, Greater than 75 kW), Voltage Class (Less than 60 V, 60-300 V, Greater than 300 V), End-Use Industry (Automotive, Industrial, HVAC, Consumer Electronics, Healthcare, Oil and Gas, Water, Renewable Energy, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Brushed DC (BDC) Motors | Shunt-Wound |

| Series-Wound | |

| Compound-Wound | |

| Permanent-Magnet DC (PMDC) | |

| Brushless DC (BLDC) Motors | Inner-Rotor BLDC |

| Outer-Rotor BLDC |

| Less than 75 W |

| 75 - 750 W |

| 0.75 - 75 kW |

| Greater than 75 kW |

| Less than 60 V |

| 60 - 300 V |

| Greater than 300 V |

| Automotive and Transportation |

| Industrial Machinery and Automation |

| HVAC and Refrigeration |

| Consumer Electronics and Appliances |

| Healthcare and Medical Devices |

| Oil, Gas and Mining |

| Water and Wastewater |

| Renewable Energy Systems |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Motor Technology | Brushed DC (BDC) Motors | Shunt-Wound |

| Series-Wound | ||

| Compound-Wound | ||

| Permanent-Magnet DC (PMDC) | ||

| Brushless DC (BLDC) Motors | Inner-Rotor BLDC | |

| Outer-Rotor BLDC | ||

| By Power Rating (Output) | Less than 75 W | |

| 75 - 750 W | ||

| 0.75 - 75 kW | ||

| Greater than 75 kW | ||

| By Voltage Class | Less than 60 V | |

| 60 - 300 V | ||

| Greater than 300 V | ||

| By End-Use Industry | Automotive and Transportation | |

| Industrial Machinery and Automation | ||

| HVAC and Refrigeration | ||

| Consumer Electronics and Appliances | ||

| Healthcare and Medical Devices | ||

| Oil, Gas and Mining | ||

| Water and Wastewater | ||

| Renewable Energy Systems | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Direct Current (DC) Motor space be by 2031?

Value is projected to reach USD 46.27 billion, up from USD 31.44 billion in 2026.

What compound annual growth rate (CAGR) is forecast for Direct Current (DC) Motor sales during 2026-2031?

A CAGR of 8.03% is expected over the period.

Which geographic region is set to expand the quickest?

North America is on track for the highest 8.38% CAGR, supported by reshoring incentives and efficiency subsidies.

Which motor technology currently dominates global revenue?

Brushless DC designs lead with 66.83% share in 2025 and are outpacing brushed alternatives.

What single factor is adding the most units per electric vehicle?

The shift to 48-volt and 800-volt electrical architectures boosts BLDC motor counts to 30-50 units per vehicle compared with 10-15 in internal-combustion models.

Why is rare-earth supply considered a strategic risk?

China refines more than 90% of neodymium-iron-boron magnets, so export curbs or pricing shifts can quickly squeeze motor OEM margins and prompt redesigns.

Page last updated on: