Market Overview

| Study Period | 2021 - 2031 |

|---|---|

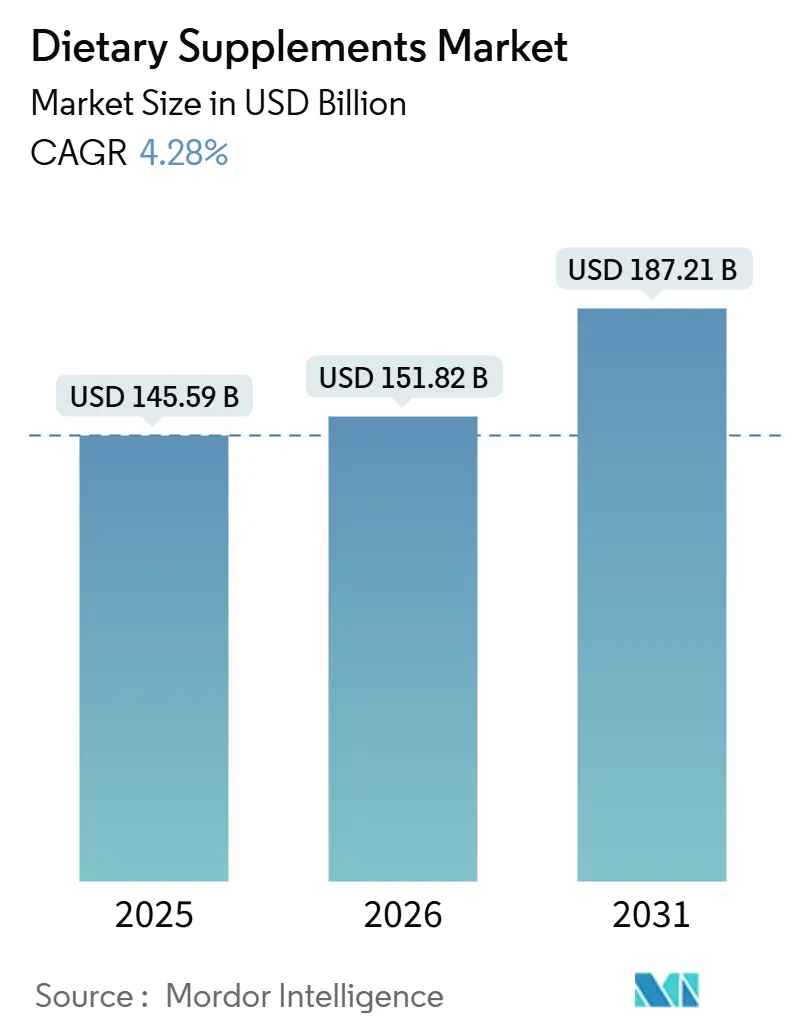

| Market Size (2026) | USD 151.82 Billion |

| Market Size (2031) | USD 187.21 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

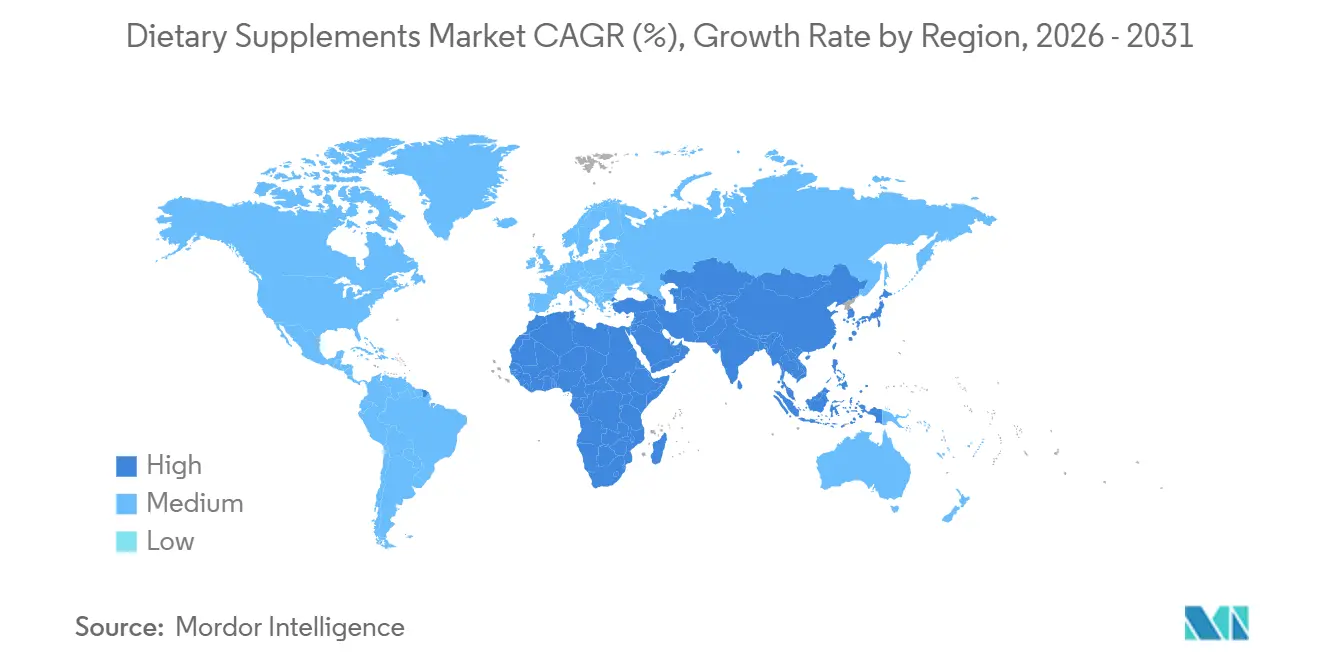

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dietary Supplements Market Analysis by Mordor Intelligence

The dietary supplements market size is expected to grow from USD 145.59 billion in 2025 to USD 151.82 billion in 2026 and is forecast to reach USD 187.21 billion by 2031 at 4.28% CAGR over 2026-2031. This market is undergoing a significant shift, driven by a growing consumer focus on preventive healthcare and wellness. Key growth drivers include heightened health awareness, an aging demographic, and rising disposable incomes in emerging markets. There's been a pronounced surge in demand for supplements aimed at bolstering the immune system, optimizing digestive health, and preventing nutritional deficiencies. The industry has evolved, moving beyond traditional pills and capsules to embrace innovative delivery methods like gummies, liquid shots, and functional beverages. These advancements cater to consumer preferences for convenience and aim to boost supplement effectiveness through better bioavailability and taste.

Product innovation is clearly leaning towards convenience and taste. Gummies, growing at a robust CAGR of 12.01%, are outpacing traditional tablets. This surge is attributed to formulators mastering pectin-based matrices, which not only eliminate gelatin but also cater to the vegan demographic. Prebiotics and probiotics, with a CAGR of 9.61%, are the fastest-growing product type. Their rise is fueled by clinical findings linking gut microbiome diversity to both immune and mental health. Furthermore, the Food and Drug Administration's (FDA) Generally Recognized as Safe (GRAS) notices for new Lactobacillus and Bifidobacterium strains have eased regulatory hurdles for market entrants. Meanwhile, plant-based supplements are witnessing a CAGR of 9.81%, nearly double that of their synthetic counterparts. This surge is driven by clean-label demands and sustainability concerns, prompting brands to pivot towards sourcing from algae, mushrooms, and fermented botanicals, moving away from traditional petroleum-derived ingredients.

Key Report Takeaways

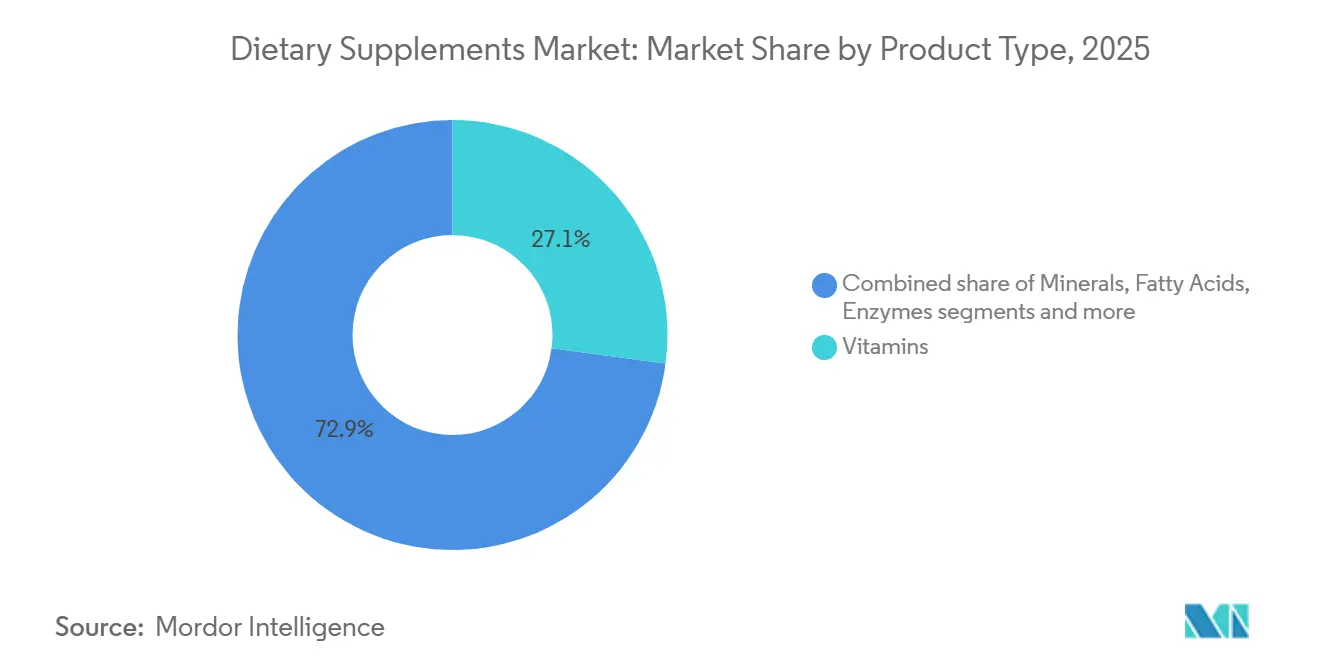

- By product type, vitamins dominated with 27.11% of the dietary supplements market share in 2025, while prebiotics and probiotics supplements are expected to grow at a 9.61% CAGR through 2031.

- By form, capsules and softgels held 38.00% of the dietary supplements market share in 2025, with gummies projected to grow fastest at a 12.01% CAGR through 2031.

- By source, synthetic/fermentation-derived products led with 56.11% market share in 2025, while plant-based supplements are growing at a 9.81% CAGR through 2031.

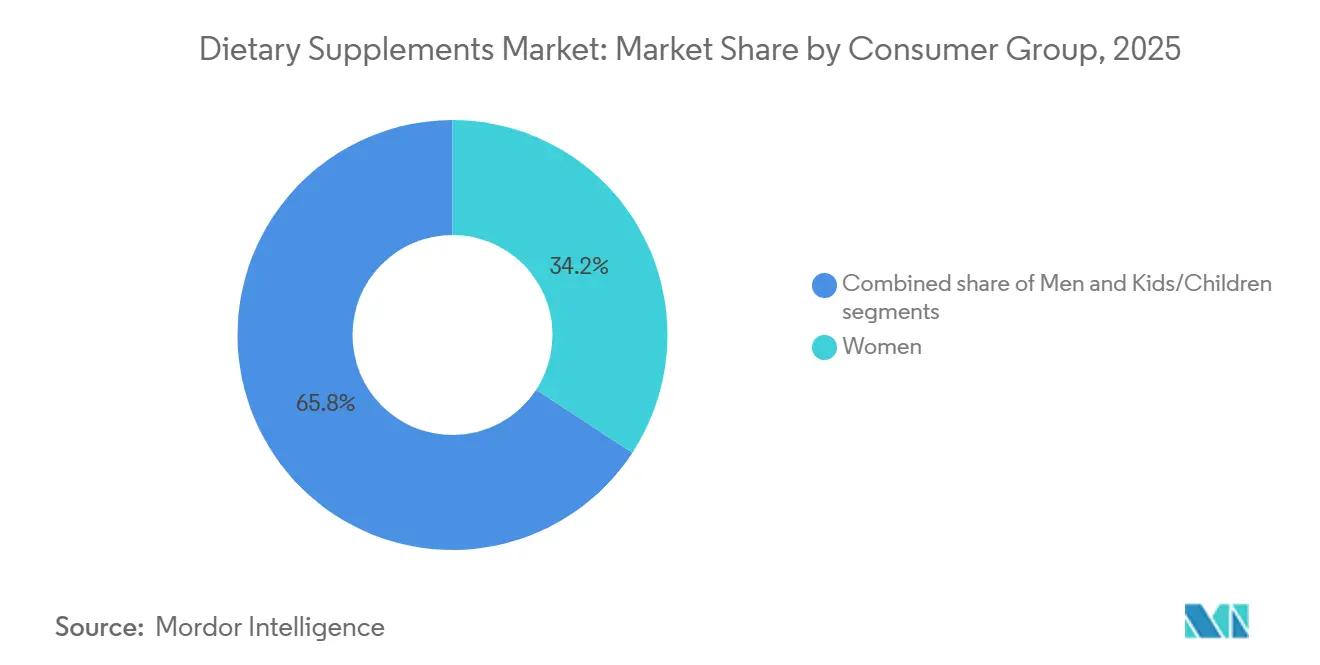

- By consumer group, women captured 34.22% of the market share in 2025, with the kids/children segment projected to grow at an 11.01% CAGR through 2031.

- By health application, general health and wellness comprised 41.12% of the market in 2025, while immunity enhancement shows the highest growth potential at a 9.40% CAGR through 2031.

- By distribution channel, the online retail channel represented 25.45% of market share in 2025 and is projected to grow at a CAGR of 13.00% through 2031, representing the fastest-growing segment.

- By geography, Asia-Pacific dominated 49.48% of the market share in 2025, while the Middle East and Africa region demonstrated the highest growth rate with a 7.83% CAGR in 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dietary Supplements Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Focus on Preventive Healthcare | +0.9% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Supplements Targeting Women Consumers Fueling Growth | +0.7% | Global, particularly Asia-Pacific and North America | Long term (≥4 years) |

| Growing Preference for Clean-label, Plant-based and Vegan Formulas | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Healthy-ageing Focus Accelerating Multivitamin Uptake Among Consumers | +0.6% | Europe, Japan, North America | Long term (≥4 years) |

| E-commerce Growth Enhances Supplement Accessibility and Market Reach | +1.0% | Global, led by China, India, United States | Short term (≤2 years) |

| Research and Development Investments Drive Innovative Product Development and Targeted Solutions | +0.5% | North America, Europe, select APAC hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Increased Focus on Preventive Healthcare

Preventive healthcare has shifted from being a wellness trend to a key purchasing factor. This change is particularly evident among millennials and Generation Z consumers, who are now prioritizing supplements even before any symptoms appear. In 2025, the World Health Organization highlighted a concerning trend: non-communicable diseases were responsible for 74% of global deaths[1]Source: World Health Organization "Noncommunicable diseases," who.int. In response, governments and insurers have introduced measures such as tax credits and employer wellness programs, which subsidize supplement purchases. This broader societal shift has created opportunities for multivitamin and mineral blends, now seen as essential daily safeguards against micronutrient deficiencies. Additionally, telemedicine platforms are enhancing their services by including supplement recommendations during virtual consultations. This innovation has created a seamless ecosystem where diagnosis, prescription, and fulfillment are completed digitally within a short timeframe. In the United States, the Dietary Supplement Health and Education Act, along with the European Union's Food Supplements Directive, serve as key regulatory frameworks. These not only legitimize the dietary supplement category but also allow for structure-function claims, appealing directly to prevention-focused consumers.

Market analysis shows a growing preference among consumers for supplements designed to address specific health needs. These include strengthening the immune system, managing stress, and improving sleep quality. As global healthcare systems increasingly adopt preventive measures to reduce long-term medical costs, the dietary supplement market is well-positioned for sustained growth and deeper market penetration.

Supplements Targeting Women Consumers Fueling Growth

The women's health supplements market is experiencing significant growth within the broader dietary supplements industry. Moving beyond traditional prenatal products, the market now offers a wide array of solutions designed to meet the specific health needs of women. These include specialized formulations aimed at addressing menopause management, supporting hormonal balance, and enhancing reproductive health. Recent developments in product innovation emphasize multifunctional supplements that not only help manage stress but also provide beauty-enhancing benefits, while simultaneously supporting hormonal regulation and boosting energy levels. Since women often play a central role in making healthcare decisions for their families, their preferences in supplements are a key driver of market trends. The Women's Health Innovation Opportunity Map Progress Report for 2026 highlights that, despite progress through increased funding and the establishment of innovation centers, global healthcare research and development funding for female-specific conditions outside of oncology remains minimal.

Growing Preference for Clean-label, Plant-based, and Vegan Formulas

Driven by a growing demand for transparency and natural ingredients, the dietary supplements industry is undergoing a significant transformation. The plant-based segment is projected to outpace the overall market, with an anticipated CAGR of 9.81% from 2026 to 2031, compared to the market's 4.28% growth rate. Today, consumers prioritize environmental sustainability and ethical production, viewing them as essential rather than as premium add-ons. In response, manufacturers are not only modifying existing formulations but are also crafting plant-based alternatives to traditional animal-derived supplements, such as collagen and omega-3s. Younger consumers, in particular, are scrutinizing ingredient lists and manufacturing processes, propelling the clean-label movement within the dietary supplements arena. Highlighting the industry's shift, the European Commission's Horizon Europe Work Programme 2023-2025 underscores the importance of sustainable agricultural practices. These include reducing chemical pesticide usage, promoting organic farming, and enhancing biodiversity in food systems, all of which influence the sourcing of botanical ingredients in the dietary supplements sector.

Healthy-Ageing Focus Accelerating Multivitamin Uptake Among Consumers

As the global population continues to age, there is a growing demand for supplements that support longevity and improve quality of life. This trend is particularly evident in regions such as Japan, Europe, and China, where older demographics are actively seeking nutritional products tailored to their specific needs. The market for healthy aging supplements has undergone significant evolution, transitioning from traditional multivitamins to a diverse range of products designed to enhance cognitive function, support joint health, and promote cellular regeneration. For example, in Japan, FANCL's "Brain Active" supplement addresses the need for cognitive enhancement, while in Germany, Doppelherz develops formulations specifically targeting joint and heart health for aging individuals.

In addition, consumer preferences in the dietary supplements market are shifting toward products that offer clinical validation and demonstrable benefits, moving away from generic wellness claims. This change has driven increased investments in research and development, with a focus on improving bioavailability and creating formulations tailored to specific age groups. Advanced innovations, such as liposomal delivery systems and DNA-based product customization, are gaining traction within the dietary supplements industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of Counterfeit Products Hampering the Growth | -0.6% | Global, acute in Asia-Pacific and Middle East | Short term (≤2 years) |

| Rising Consumer Scepticism Toward Synthetic Additives and Mega-dose Safety Concerns | -0.5% | North America, Europe | Medium term (2-4 years) |

| Tighter Regulations on Dietary Supplements and Borderline Products | -0.4% | Europe, North America, emerging in APAC | Long term (≥4 years) |

| Price Wars from Local Producers Reduce Profit Margins | -0.3% | Asia-Pacific, South America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit Products Hampering the growth

Counterfeit supplements are infiltrating supply chains, primarily through third-party e-commerce sellers and unregulated cross-border shipments. This not only erodes consumer trust but also exposes buyers to potentially harmful adulterated ingredients or subpotent formulations. Recently, the United States Food and Drug Administration issued several warning letters targeting products with undeclared pharmaceutical ingredients. This included sildenafil, commonly found in male-enhancement supplements, and sibutramine, often used in weight-loss formulas. Both substances pose significant cardiovascular risks and breach drug-approval mandates. The Asia-Pacific region sees the highest prevalence of counterfeits. Here, fragmented distribution networks and limited enforcement resources allow rogue manufacturers to easily mimic branded packaging.

A report from the World Health Organization highlighted that a significant portion of supplements sold through informal channels in Southeast Asia failed authenticity tests. In response, brand owners are turning to blockchain-enabled track-and-trace systems. For instance, Nestlé Health Science has a QR-code verification program. This initiative lets consumers authenticate a product's origin with a smartphone scan, leading to a notable drop in return rates in the markets where it was piloted. Despite these efforts, achieving regulatory harmonization remains a challenge. The European Union's Falsified Medicines Directive, for example, mandates serialization for medicinal products. However, it excludes supplements, leaving a gap that counterfeiters are quick to exploit.

Tighter Regulations on Dietary Supplements and Borderline Products

Globally, regulatory frameworks for dietary supplements are becoming stricter, impacting both market growth and product innovation. The Food and Drug Administration's Human Foods Program is focusing on dietary supplements, emphasizing updates to New Dietary Ingredient Notifications guidance and food product chemical safety standards. These regulatory changes are raising entry barriers for new companies and increasing compliance costs for established manufacturers, particularly for those introducing new ingredients or making health claims. Highlighting the need for change, the United States Pharmacopeia's policy position paper critiques the Dietary Supplement Health and Education Act of 1994 for its shortcomings in ensuring product safety and market consistency.

Products that fall between supplements, foods, and pharmaceuticals face regulatory challenges, as classification ambiguities hinder their market access in the dietary supplements industry. In Europe, the regulatory landscape is even more challenging. The European Food Safety Authority enforces strict health claim criteria, which only a small number of supplement ingredients can satisfy. Such regional regulatory disparities create significant operational hurdles for multinational firms striving for consistent product formulations across diverse markets.

Segment Analysis

By Product Type: Vitamins Lead While Probiotics Surge

In 2025, vitamins accounted for 27.11% of the market share, establishing themselves as the leading segment by type. This dominance is attributed to the proven effectiveness of vitamins and their consistent endorsement by healthcare professionals. Multivitamin supplements continue to act as the primary entry point for new consumers exploring dietary supplements. At the same time, individual vitamins, particularly Vitamin D and Vitamin C, are experiencing increased demand due to their well-recognized immune-boosting properties, which are highly valued across the dietary supplements industry.

Between 2026 and 2031, the prebiotics and probiotics segment is anticipated to grow at a compound annual growth rate (CAGR) of 9.61%, surpassing the overall market growth rate. This expansion is driven by growing scientific evidence highlighting the connection between gut health and brain function, as well as the critical role of the microbiome in maintaining overall health. These supplements are widely recognized for their benefits in improving gastrointestinal health, enhancing immune function, and addressing various medical conditions. When prebiotics and probiotics are combined as synbiotics, they deliver enhanced benefits, including improved gut health and potential applications in managing obesity, diabetes, and mental health conditions. Additionally, minerals, fatty acids, and protein supplements maintain a stable presence in the market. Herbal supplements exhibit varying growth trends across regions, influenced by local traditional medicine practices. Enzyme supplements primarily target digestive health, while blended formulations are gaining traction for offering multiple health benefits in a single product.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Capsules Dominate While Gummies Disrupt

In 2025, capsules and softgels are expected to hold a dominant 38.00% market share. This leadership position is primarily due to their ability to protect sensitive ingredients from degradation and deliver precise dosing, which is critical for maintaining product efficacy. These formats continue to be widely used in pharmaceutical-adjacent sectors, where ensuring ingredient stability and enabling controlled release are essential for achieving desired outcomes. On the other hand, the gummies segment is projected to experience remarkable growth, with a compound annual growth rate (CAGR) of 12.01% forecasted for the period from 2026 to 2031. This growth is driven by increasing consumer preference for more enjoyable and palatable consumption methods, as well as the format's effectiveness in masking the bitter taste of certain ingredients, particularly in the dietary supplements industry.

The vitamin gummies market demonstrates significant growth potential, fueled by rising health awareness among consumers and an increasing demand for functional foods that offer additional health benefits. While tablets remain a cost-effective and efficient option for manufacturers, they face challenges related to consumer perceptions about their slower dissolution rates. Similarly, powders continue to play a vital role in sports nutrition and protein supplements due to their flexibility in dosage customization. Liquid formats are also gaining popularity, particularly in applications that require rapid absorption, and among specific consumer groups such as the elderly and children, who often find it difficult to consume pills.

By Source: Synthetic Dominance Challenged by Plant-Based Innovation

In 2025, synthetic and fermentation-derived supplements held a significant 56.11% market share. This dominance reflects their cost advantages and scalable manufacturing processes, which have supported mass-market adoption over the past fifty years. At the same time, plant-based supplements are growing at a compound annual growth rate (CAGR) of 9.81%, driven by consumers who are increasingly focused on ingredient transparency and environmental sustainability. Algae-derived omega-3s illustrate this shift, offering the same concentrations of docosahexaenoic acid (DHA) and eicosapentaenoic acid (EPA) as fish oil while producing 75% fewer carbon emissions per gram. This eco-friendly alternative appeals strongly to environmentally conscious millennials and Generation Z consumers. Additionally, advancements in fermentation technology are enabling the production of plant-based alternatives for compounds traditionally sourced from animals. For example, vitamin D3 derived from lichen and collagen precursors produced from yeast allow brands to market vegan products without compromising on bioavailability.

Animal-based supplements, such as collagen peptides, glucosamine, and fish oil, continue to attract a loyal customer base. These consumers often value traditional sourcing methods and perceive animal-derived nutrients as more bioavailable. However, this segment is facing increasing challenges from animal welfare advocacy groups and stricter regulatory requirements, particularly regarding marine sustainability certifications. Synthetic vitamins, on the other hand, are favored for their precise dosing and consistent quality across batches, making them a preferred choice for formulators targeting specific therapeutic outcomes. Despite these advantages, synthetic vitamins face growing competition from the clean-label movement, which often positions whole-food-derived ingredients as superior to synthetic alternatives.

By Consumer Group: Women's Wellness Expands While Children's Market Accelerates

In 2025, women accounted for 34.22% of the consumer base, driven by specific life-stage needs such as prenatal nutrition, bone health, and managing menopause symptoms. At the same time, the kids and children segment is expanding at a strong CAGR of 11.01%. Parents are increasingly focused on addressing perceived nutritional gaps in processed diets and tackling health concerns related to excessive screen time. Pediatric formulations are designed to support immune health, cognitive development, and bone growth. These products often combine vitamin D, calcium, omega-3 docosahexaenoic acid (DHA), and probiotics in gummy formats, making them more appealing and easier for children to consume.

Men's supplements primarily focus on testosterone support, prostate health, and cardiovascular function, with common ingredients including zinc, saw palmetto, and coenzyme Q10 (CoQ10). However, this segment faces challenges such as market saturation in developed regions and societal stigma around men seeking health-related products. The kids' segment benefits from endorsements by pediatricians and wellness programs in schools, which help normalize daily supplementation and encourage habits that often continue into adulthood. Regulatory frameworks, such as the United States Food and Drug Administration's (FDA) guidelines on age-appropriate dosing and child-resistant packaging, ensure safety but also increase compliance costs. These regulations favor established brands with expertise in regulatory affairs, creating barriers for new entrants[2]Source: Food and Drug Administration "FDA Advisory No.2023-1994 || Public Health Warning Against the Purchase and Consumption of the Unregistered Food Supplement," fda.gov. Additionally, brands are increasingly merging consumer segments by introducing family-pack stock-keeping units (SKUs) that combine adult and pediatric formulations. This approach leverages household purchasing trends and builds cross-generational brand loyalty.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Health Application: General Wellness Leads While Immunity Surges

In 2025, general health and wellness applications are expected to hold a 41.12% share of the market, forming the foundation of the supplements industry with products designed for daily nutritional support and preventive health. This segment continues to dominate due to its broad consumer appeal and its accessibility for individuals new to supplements who are seeking overall health benefits. The growth of this segment aligns with the increasing focus on preventive healthcare, supported by the Dietary Guidelines for Americans issued by the United States Department of Agriculture (USDA) and the United States Department of Health and Human Services (HHS). These guidelines emphasize the importance of healthy dietary patterns across all life stages and highlight the role of nutrient-dense foods and beverages.

Between 2026 and 2031, applications targeting immunity enhancement are projected to grow at a CAGR of 9.40%, surpassing the overall market growth rate as consumers prioritize immune system support. Advances in research on the relationship between nutrition and immune function have enabled the development of targeted formulations with evidence-based claims. The National Institutes of Health's (NIH) Office of Dietary Supplements provides detailed insights into probiotics and their role in supporting immune health. Other application segments exhibit varied growth patterns. Bone and joint health maintains steady growth due to aging populations, while energy and weight management benefit from trends favoring active lifestyles. Gastrointestinal health sees growth driven by increasing demand for probiotics, and applications for cardiovascular health, diabetes management, and cognitive health expand as consumers address specific health needs through supplements.

By Distribution Channel: Online Retail Dominates and Accelerates

In 2025, online retail channels are expected to hold a 25.45% market share and are projected to grow at a CAGR of 13% from 2026 to 2031, surpassing other distribution channels. This growth highlights a significant transformation in consumer purchasing behaviors across diverse regions and demographic groups. E-commerce platforms play a crucial role in this shift by offering consumers access to detailed product information, customer reviews, and comparison tools. These features enable buyers to make well-informed decisions when purchasing dietary supplements, aligning with their specific needs and preferences.

Specialty stores continue to remain competitive by providing expert guidance and carefully selected product offerings, catering to consumers who seek personalized recommendations. Supermarkets and hypermarkets benefit from their convenience and ability to drive impulse purchases; however, they face challenges such as narrow profit margins and limited shelf space for supplement products. Direct selling channels, while experiencing a decline in market share, still hold importance in certain regions and product categories where personal relationships and community engagement foster customer loyalty. Additionally, other distribution channels, including healthcare practitioners, fitness centers, and subscription services, address specific market segments by connecting dietary supplements to targeted wellness programs and use cases within the industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Asia-Pacific region dominated with a 49.48% of the market share in 2025. This dominance was fueled by several factors, including the rising disposable incomes of the middle class in China and India, rapid urbanization that has encouraged greater adoption of dietary supplements, and government-led initiatives aimed at promoting preventive healthcare. A notable development in India was the introduction of mandatory third-party testing for imported supplements by the Food Safety and Standards Authority of India (FSSAI). While this regulation extended clearance timelines by 60 to 90 days, it significantly enhanced consumer confidence in the quality of these products[3]Source: Food Safety and Standards Authority of India "Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use, Food for Special Medical Purpose, Functional Food and Novel Food) Regulations," fssai.gov. In Japan, the aging population has been a key driver of demand for multivitamins and bone-health supplements. Government-subsidized health screenings have played a pivotal role in identifying nutritional deficiencies, with physicians frequently recommending specific supplements to address these gaps.

The Middle East and Africa region demonstrated the highest growth rate with a 7.83% CAGR through 2031. This growth is largely attributed to Gulf nations' efforts to diversify their economies beyond hydrocarbons and invest in sectors such as wellness tourism and domestic nutraceutical manufacturing. The United Arab Emirates (UAE) has been at the forefront of this transformation, establishing free zones that offer tax incentives and streamlined licensing processes for supplement manufacturers. These initiatives have successfully attracted foreign direct investment from European and North American brands, which are increasingly viewing the region as a strategic hub for production and distribution.

North America and Europe represent mature markets characterized by moderate growth. These regions have reached saturation in terms of multivitamin penetration, with innovation now focusing on condition-specific formulations and advanced delivery systems. In Europe, the European Food Safety Authority (EFSA) has implemented a rigorous review process for novel ingredients, which often delays the market entry of innovative products. However, this stringent regulatory framework ensures consumer safety and provides an advantage to established brands with expertise in navigating these complex requirements. This dynamic has allowed such brands to maintain a competitive edge in these highly regulated markets.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The dietary supplements market showcases a fragmented landscape. Here, no single player dominates, and competitive intensity arises from the interplay of multinational giants, regional experts, and digital disruptors. Established entities like Abbott, Nestlé Health Science, and Bayer harness clinical trial infrastructures and adept regulatory teams. This not only validates their efficacy claims but also smoothens their journey through intricate approval processes. Such advantages often lead to premium pricing and exclusive access to pharmacy channels. In contrast, nimble startups are turning the tables. By leveraging direct-to-consumer strategies and the influence of social media influencers, they are reaching niche audiences such as vegan athletes, biohacking enthusiasts, or postpartum mothers at a significantly lower customer-acquisition cost compared to traditional retail methods. This marks a significant shift in the industry, prioritizing speed over sheer scale.

There's a burgeoning focus on personalized nutrition. Platforms like Viome are at the forefront, merging microbiome sequencing and blood biomarkers to curate tailored supplement regimens. Additionally, there's a push for condition-specific formulations, catering to often-overlooked groups like perimenopausal women and shift workers grappling with circadian disruptions. Technology is the dividing line between industry leaders and those lagging behind. For instance, blockchain systems are being deployed to counteract counterfeiting, while artificial intelligence tools are refining demand forecasts to minimize inventory waste. Subscription models are even predicting customer churn with impressive accuracy, allowing companies to intervene and retain clients proactively.

Smaller players, such as Ritual and Athletic Greens, are shaking up the status quo. By openly sharing details about ingredient sourcing and third-party testing, they are challenging long-standing industry practices. This transparency is compelling established brands to either audit their supply chains or risk losing credibility to these more transparent newcomers. Navigating regulatory waters is proving to be a significant competitive advantage. The United States Food and Drug Administration's Current Good Manufacturing Practice mandates come with fixed costs, a heavier burden for smaller operators. Meanwhile, the European Union's Novel Foods Regulation introduces lengthy approval processes, favoring those with both regulatory know-how and the financial muscle to invest in necessary toxicology studies.

Dietary Supplements Industry Leaders

-

Amway Corporation

-

Herbalife Ltd.

-

Nestle S.A.

-

Bayer AG

-

Haleon plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Awshad introduced CalmaGummies to the market, formulated to enhance relaxation, mental focus, and sleep quality. Each gummy contains 135mg of full-spectrum hemp extract, incorporating CBD and THC compounds to deliver therapeutic benefits.

- April 2025: The Vitamin Shoppe introduced GLP-1 Support from Whole Health Rx, a product line offering nutritional supplements for individuals using GLP-1 medications in their weight management programs.

- March 2025: Life Time has introduced NOURISH, a drinkable multivitamin and greens powder, as part of its LTH supplements product line. Each serving of NOURISH contains 23 essential vitamins and minerals, which is 21% more than competing brands.

- February 2025: Fenix Health Science expanded its brain health product portfolio with enhanced formulations in its Omega, Neuro, and Mineral product lines. The Omega product line incorporates Lysoveta LPC, an ingredient that enhances Omega-3 absorption to support cognitive function.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dietary supplements market as finished, packaged ingestible products, vitamins, minerals, botanicals, fatty acids, proteins, probiotics, enzymes, and blended formulations, consumed to complement regular diets and improve specific health outcomes. Values represent manufacturer-level revenue generated through retail, direct-to-consumer, and practitioner channels across six regions in constant 2024 USD, with the study period 2020-2030.

Scope exclusion: Functional foods, sports drinks, fortified staple foods, and testing or contract manufacturing services are deliberately left out to keep the lens on end-use supplement products only.

Segmentation Overview

-

By Product Type

-

Vitamins

- Vitamin A

- Vitamin C

- Vitamin D

- Vitamin B (Includes B6, B7 / Biotin, B9/ Folic, B12, etc.)

- Other Vitamin Supplements

- Multivitamin Supplements

-

Minerals

- Iron Supplements

- Calcium Supplements

- Magnesium and Zinc Supplements

- Multi-Mineral Supplements

- Other Minerals

- Fatty Acids

- Protein and Amino Acids

- Prebiotic and Probiotic Supplements

- Herbal Supplements

- Enzymes

- Blended Supplements

- Others

-

Vitamins

-

By Form

- Tablets

- Capsules and Softgels

- Powders

- Gummies

- Liquids

- Others

-

By Source

- Plant-based

- Animal-based

- Synthetic/Fermentation-derived

-

By Consumer Group

- Men

- Women

- Kids/Children

-

By Health Application

- General Health and Wellness

- Bone and Joint Health

- Energy and Weight Management

- Gastrointestinal and Gut Health

- Immunity Enhancement

- Cardiovascular Health

- Diabetes Management

- Cognitive and Mental Health

- Skin, Hair and Nail Care

- Eye Health

- Other Health Applications

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Channels

- Direct Selling

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts conduct structured interviews and pulse surveys with nutraceutical formulators, raw-material suppliers, e-commerce category managers, retail pharmacists, and sports-nutrition coaches across North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. These conversations clarify dosage trends, average selling prices, regulatory bottlenecks, and inventory rotations that desk research alone cannot surface.

Desk Research

We start by mapping supply-demand indicators from open, high-confidence sources such as UN Comtrade shipment data (HS 2106, 3004), World Health Organization nutrition statistics, United States NIH Dietary Supplement Label Database, Eurostat health expenditure tables, and industry position papers released by the Council for Responsible Nutrition, the International Alliance of Dietary/Food Supplement Associations, and similar bodies. Company 10-Ks, IPO filings, investor decks, and reputable business media retrieved through Dow Jones Factiva and D&B Hoovers give pricing moves, channel splits, and competitive actions. Trade journals and patent counts round out innovation signals. This list is illustrative; many additional references underpin every data point we publish.

Market-Sizing & Forecasting

Top-down modeling begins with regional household health and wellness spend, demographic aging curves, and per-capita supplement penetration; these pools are then apportioned across product types using consumption surveys and import-export balances, before being further cross-checked by sampled ASP × volume roll-ups from leading brand portfolios. Key variables include discretionary income growth, e-commerce share of OTC sales, sports participation rates, prevalence of vitamin-deficiency conditions, and regulatory claim approvals. A multivariate regression projects each driver and feeds an ARIMA overlay to capture cyclical shocks, while bottom-up supplier checks adjust anomalies and plug gaps where reporting lags exist.

Data Validation & Update Cycle

Mordor analysts run variance dashboards that flag deviations above pre-set thresholds, re-contact at-source experts, and escalate outliers to senior review panels. The dataset refreshes annually, with interim tweaks when material events, regulation, M&A, or supply shocks shift the baseline. A final pre-publication audit ensures clients receive the latest vetted view.

Why Mordor's Dietary Supplements Baseline Commands Reliability

Published market values often diverge because firms disagree on what counts as a supplement, which geographies to bundle, and how quickly retail prices escalate. Our disciplined scoping, yearly refresh cadence, and dual-lens (penetration pools plus ASP checks) minimize such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 145.62 B (2025) | Mordor Intelligence | - |

| USD 179.53 B (2024) | Global Consultancy A | broader inclusion of fortified foods; higher assumed e-commerce mark-ups |

| USD 192.65 B (2024) | Industry Association B | uses shipment values without retail discounting; no scope exclusion for contract testing |

| USD 189.23 B (2024) | Regional Consultancy C | aggregates adjacent nutraceutical categories and applies constant forex without inflation adjustment |

In short, the Mordor approach delivers a balanced, transparent baseline that traces every figure to observable variables and repeatable steps, giving decision-makers a dependable springboard for strategy and investment planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast growth rate for the global dietary supplements market to 2031?

The market is projected to expand at a 4.28% CAGR, moving from USD 151.82 million in 2026 to USD 187.22 million by 2031.

Which form factor is growing fastest within dietary supplements?

Gummies, advancing at a 12.01% CAGR, are the quickest-expanding form because their taste and texture boost consumer adherence.

Which region currently leads in dietary supplements demand?

Asia-Pacific holds 49.48% of worldwide revenue on the strength of China, India, and Japan.

Why are plant-based supplements gaining traction?

Environmental sustainability, vegan ethics, and clean-label preferences push consumers toward algae-derived omega-3s and fermented botanicals, supporting a 9.81% CAGR for plant-based products.

How significant is e-commerce to supplement sales?

Online retail captured 25.45% of 2025 revenue and is growing at 13.00% CAGR, driven by subscription programs and direct-to-consumer convenience.