| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 12.29 Billion |

| Market Size (2030) | USD 16.75 Billion |

| CAGR (2025 - 2030) | 6.39 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

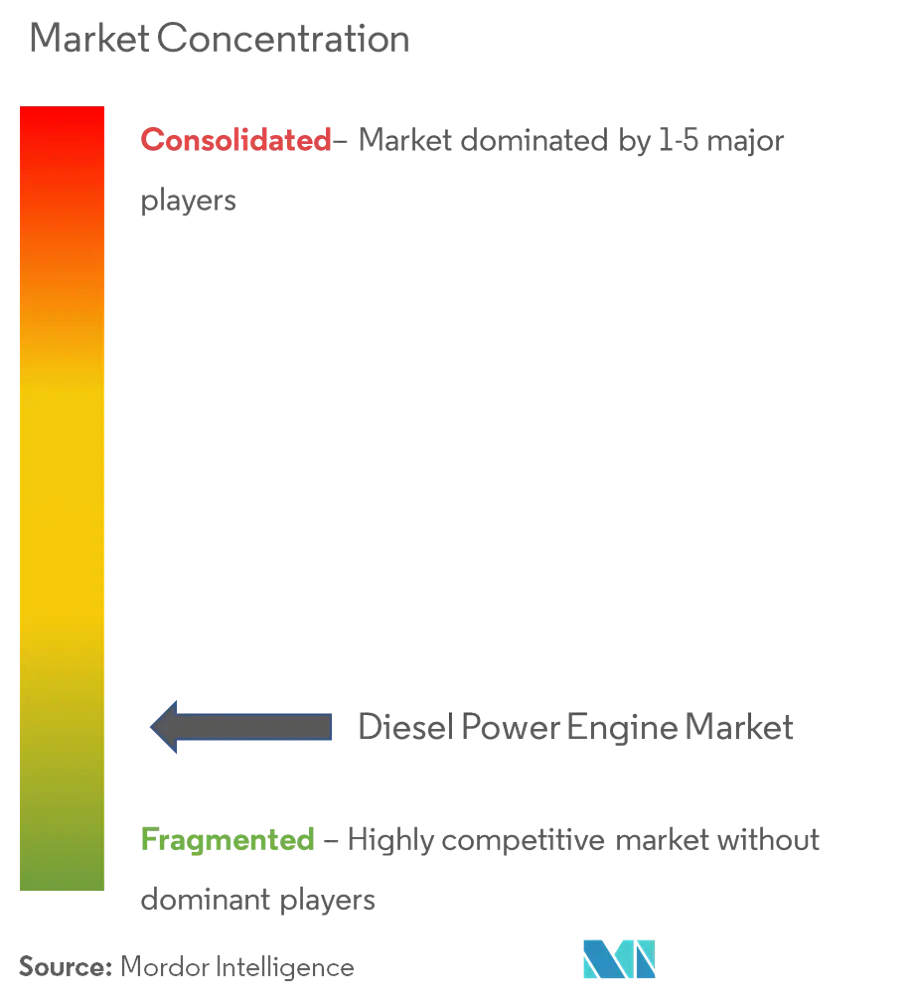

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Diesel Power Engine Market Analysis

The Diesel Power Engine Market size is estimated at USD 12.29 billion in 2025, and is expected to reach USD 16.75 billion by 2030, at a CAGR of 6.39% during the forecast period (2025-2030).

The diesel engine industry is experiencing significant transformation driven by global infrastructure development initiatives and technological advancements. Construction activities across major economies have shown remarkable growth, with the United States leading with substantial establishments across key states—Texas alone hosting 61,700 construction establishments as of Q1 2023. The surge in infrastructure projects has been particularly notable in emerging economies, with countries like Singapore announcing construction contracts worth USD 32-38 billion for 2024. This widespread infrastructure development has created a robust demand for reliable diesel power systems, particularly in areas where grid connectivity is limited or unreliable.

Power reliability concerns and aging grid infrastructure have emerged as critical factors shaping the industry landscape. According to recent data, about 83% of reported significant power outages between 2000 and 2021 in the United States are attributed to weather-related events, highlighting the crucial role of backup power systems. The increasing frequency of extreme weather events and the growing strain on existing power infrastructure have led to a greater emphasis on reliable backup power solutions, particularly in critical applications such as data centers, healthcare facilities, and industrial operations.

Technological advancements in diesel engine technology and manufacturing have significantly enhanced their efficiency and environmental performance. Manufacturers are increasingly focusing on developing cleaner-burning engines with advanced emission control systems to comply with stringent environmental regulations. This evolution is particularly evident in the commercial and industrial sectors, where the demand for more efficient and environmentally conscious power solutions continues to grow. The industry has witnessed a notable shift towards hybrid solutions that combine diesel engines with renewable energy sources, offering more sustainable power generation options.

The digital transformation of various sectors has created new demand patterns, particularly in the data center industry. As of March 2024, the United States leads globally with 5,381 data centers, followed by Germany with 521 centers and the United Kingdom with 514 centers. This rapid expansion of digital infrastructure has intensified the need for reliable backup power systems, as even brief power interruptions can result in significant operational disruptions and financial losses. The trend towards edge computing and the proliferation of smaller, distributed data centers has further diversified the applications for diesel power engines, creating new market opportunities in urban and semi-urban locations.

Diesel Power Engine Market Trends

INCREASING DEMAND FROM INDUSTRIAL SECTOR

The industrial sector's growing reliance on an uninterrupted power supply has emerged as a primary driver for the diesel engine market, particularly due to its superior reliability and enhanced power quality characteristics. In the construction sector, where power failures can lead to significant project delays and financial losses, diesel power equipment such as industrial diesel engines have become indispensable for ensuring continuous operations and site safety. This demand is evidenced by major infrastructure initiatives, such as China's announcement in April 2023 to increase spending on construction and infrastructure projects by USD 1.8 trillion year-on-year. Similarly, India's approval for the development of 21 greenfield airports in January 2023, along with 1,174 projects worth USD 855.12 million under the AMRUT 2.0 mission for water body rejuvenation, water supply, and sewage management, demonstrates the escalating need for reliable power backup solutions in large-scale infrastructure development.

The manufacturing and healthcare sectors represent another significant driver for diesel engine adoption. Manufacturing facilities rely heavily on diesel machinery to prevent production disruptions, as power outages can lead to reduced output quality and complete process shutdowns. The healthcare sector's dependence on sensitive equipment such as oxygen ventilators, infusion pumps, ECG machines, and defibrillators necessitates a stable power supply, making commercial diesel engines the preferred backup power solution. Additionally, the mining and steel industries' heavy-duty operations require consistent power sources, as demonstrated by the scale of operations in countries like China, which produced 77.9 million metric tonnes of crude steel as of December 2022. The telecommunications and data center sectors also contribute to the growing demand, as these facilities require an uninterrupted power supply to maintain critical operations and prevent service disruptions. The integration of diesel engine components in these sectors further underscores the importance of diesel power units in maintaining operational continuity.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: END-USER

Industrial Segment in Diesel Power Engine Market

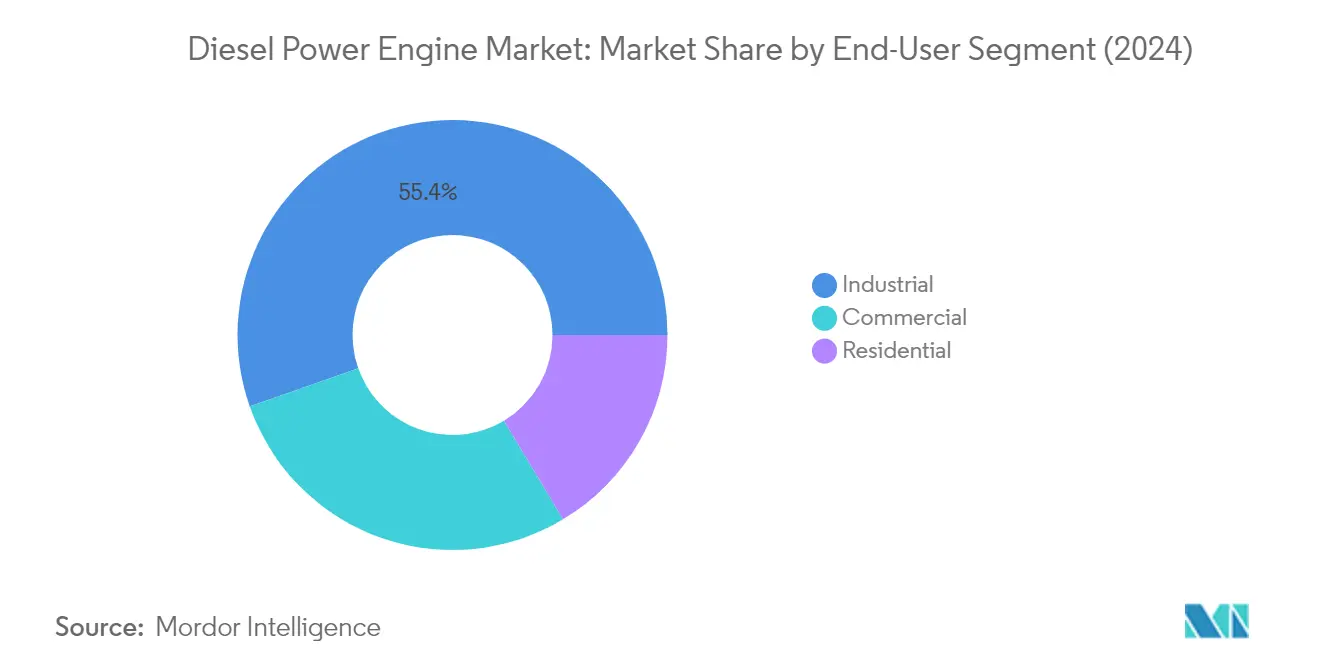

The industrial segment dominates the global diesel power engine market, accounting for approximately 55% of the total market share in 2024. It also demonstrates the strongest growth trajectory, with a projected growth rate of around 7% during 2024-2029. This segment's prominence is primarily driven by the extensive utilization of diesel engines in construction sites, mining operations, and manufacturing facilities, where a reliable power supply is crucial for continuous operations. The construction sector, in particular, relies heavily on diesel power engines for powering heavy machinery, with nearly 98% of all energy use in construction coming from diesel. Additionally, the industrial sector's demand is further bolstered by the increasing need for backup power solutions in data centers, telecommunications infrastructure, and critical manufacturing processes where power interruptions could result in significant financial losses.

Commercial and Residential Segments in Diesel Power Engine Market

The commercial and residential segments collectively represent significant portions of the diesel generator market, each serving distinct yet essential roles in backup power generation. The commercial segment, accounting for about 28% of the market, caters to establishments like offices, retail stores, hotels, hospitals, and educational institutions, providing crucial backup power during grid outages. This segment's importance is particularly evident in regions with unreliable grid infrastructure or frequent power disruptions. The residential segment, while smaller, plays a vital role in providing backup power solutions for homes, apartments, and residential complexes, especially in areas prone to weather-related power outages or regions with limited grid access. Both segments are experiencing steady growth driven by increasing urbanization, rising power consumption, and growing awareness about the importance of reliable backup power systems.

Segment Analysis: APPLICATION

Standby Segment in Diesel Power Engine Market

The standby segment dominates the global diesel power engine market, commanding approximately 56% of the total market share in 2024. This segment's prominence is driven by its critical role in providing backup power during emergencies and grid outages across various industries. Standby diesel generators are extensively deployed in critical facilities such as hospitals, data centers, telecommunications networks, and industrial facilities where uninterrupted power supply is essential for operations. These engines are designed to automatically activate within seconds of detecting power loss, ensuring a seamless transition to backup power and maintaining operational continuity. The segment's growth is further bolstered by increasing investments in infrastructure development, rising frequency of power outages, and growing demand for reliable backup power solutions across commercial and industrial sectors. Manufacturers are continuously innovating to enhance the efficiency and reliability of standby diesel power engines, with recent developments focusing on improved fuel efficiency, reduced emissions, and integration of smart monitoring systems.

Prime Segment in Diesel Power Engine Market

The prime segment serves as the primary source of power in locations where grid access is limited or unavailable. This segment is witnessing steady growth, particularly in remote industrial operations, construction sites, mining facilities, and off-grid locations. The segment's expansion is driven by increasing industrialization in developing regions, growing demand for reliable power supply in remote areas, and the expansion of mining and construction activities globally. Prime stationary diesel engines are designed for continuous operation, offering reliable performance for extended periods without interruption. The segment's growth is supported by ongoing infrastructure development projects, expansion of industrial facilities in remote locations, and the need for dependable power sources in areas with unreliable grid connectivity.

Remaining Segments in Application Segmentation

The peak shaving segment plays a crucial role in helping facilities manage their electricity costs by supplementing grid power during periods of high demand. This application involves using stationary diesel engines to reduce the strain on the electrical grid during peak usage periods, thereby helping organizations avoid costly peak demand charges. Peak shaving applications are particularly valuable for commercial buildings, industrial facilities, and data centers that experience significant variations in their power consumption patterns throughout the day. The segment's importance continues to grow as more organizations seek to optimize their energy costs and maintain operational efficiency during periods of high electricity demand.

Diesel Power Engine Market Geography Segment Analysis

Diesel Power Engine Market in North America

The North American diesel engine market demonstrates robust growth driven by extensive industrial applications and infrastructure development across the United States, Canada, and Mexico. The region's strong manufacturing base, particularly in the construction and mining sectors, continues to fuel demand for diesel power engines. The market is characterized by stringent emission regulations pushing manufacturers toward developing cleaner and more efficient engines. The presence of major diesel engine companies and continuous technological advancements in engine design further strengthen the regional market dynamics.

Diesel Power Engine Market in United States

The United States dominates the North American diesel power engine market, holding approximately 79% of the regional market share in 2024. The country's leadership position is reinforced by its large-scale construction sector, which, according to the Bureau of Economic Analysis, contributes nearly USD 1 trillion to the country's GDP. The nation's extensive oil and gas sector, particularly in the Permian Basin and Gulf of Mexico, drives substantial demand for diesel power engines. The construction industry's high mechanization level, where nearly 98% of energy use comes from diesel, further cements the country's market dominance. Additionally, the growing need for backup power solutions in data centers and critical infrastructure facilities continues to drive market growth.

Diesel Power Engine Market in Canada

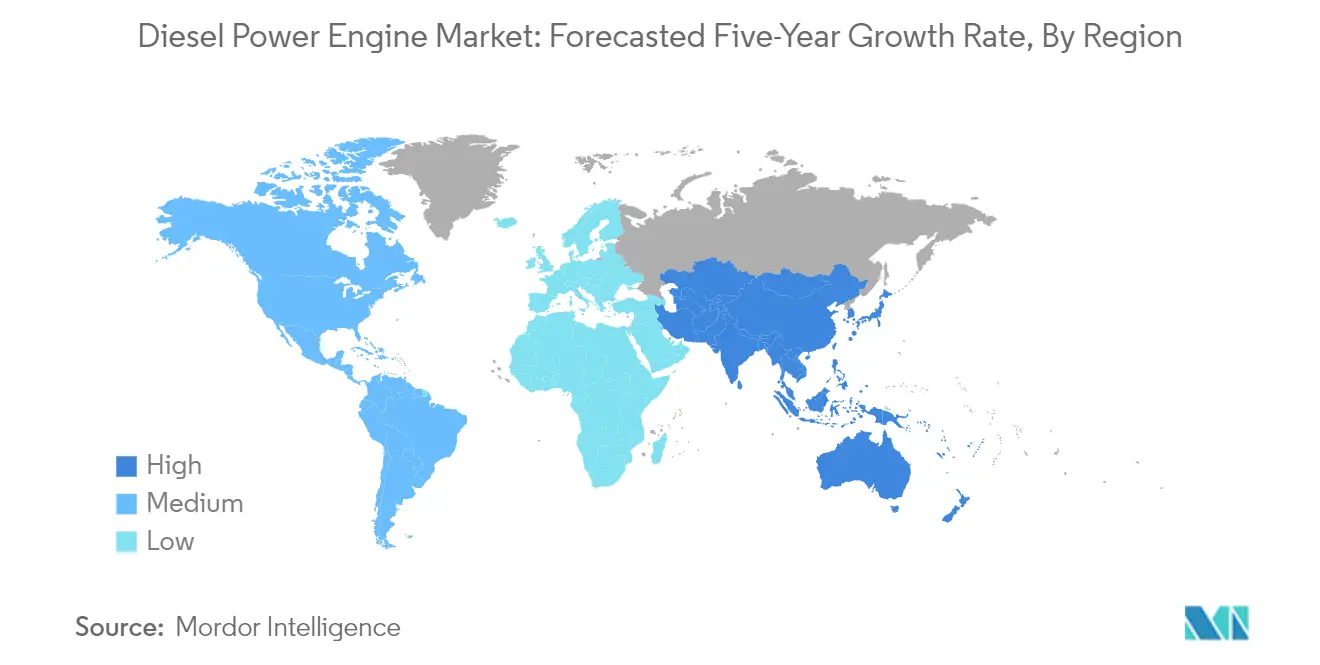

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 7% from 2024 to 2029. The country's expanding mining sector, particularly in remote areas, drives significant demand for diesel power engines. Canada's vast geographical expanse and sparse population density necessitate reliable power solutions in off-grid locations, particularly for applications in animal husbandry, forestry, and farming. The country's focus on developing low-emission diesel generators, exemplified by recent initiatives like Aggreko's Tier 4 Final generators, demonstrates its commitment to sustainable growth while maintaining operational efficiency. The strong presence of manufacturing facilities and ongoing infrastructure projects further supports the market's robust growth trajectory.

Diesel Power Engine Market in Europe

The European diesel engine market showcases a mature landscape with significant contributions from the United Kingdom, Germany, France, and Spain. The region's market is characterized by stringent emission regulations and a growing focus on sustainable technologies. Each country brings unique strengths to the market, with the UK's emphasis on backup power solutions, Germany's engineering excellence, France's industrial applications, and Spain's diverse end-user base. The region's commitment to reducing emissions while maintaining industrial efficiency drives continuous innovation in diesel engine technology.

Diesel Power Engine Market in United Kingdom

The United Kingdom leads the European market, commanding approximately 20% of the regional market share in 2024. The country's robust industrial sector and critical infrastructure requirements drive significant demand for diesel power engines. The National Grid Electricity Transmission's extensive use of diesel generators across over 250 sites in England and Wales demonstrates the crucial role of these engines in maintaining power infrastructure. The UK's diverse application base, spanning from construction sites to data centers, and its position as Europe's third-largest data center market with 458 facilities, reinforces its market leadership.

Diesel Power Engine Market in Germany

Germany exhibits the highest growth potential in Europe, with a projected growth rate of approximately 5% from 2024 to 2029. The country's strong manufacturing heritage and leadership in diesel engine technology development position it for sustained growth. Germany's expertise extends beyond traditional applications to include specialized sectors such as military applications, where German manufacturers provide high-performance engines for tanks, armored vehicles, and military aircraft. The country's continuous investment in research and development, coupled with its focus on reducing emissions and improving sustainability, drives market expansion.

Diesel Power Engine Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for diesel power engines, encompassing diverse economies including China, India, Australia, and ASEAN countries. The region's rapid industrialization, extensive infrastructure development, and growing power requirements drive substantial market growth. The varying levels of grid infrastructure development across countries create significant opportunities for diesel power engines, particularly in backup power applications and off-grid locations. The region's commitment to industrial growth while addressing environmental concerns shapes market development strategies.

Diesel Power Engine Market in China

China maintains its position as the largest market in the Asia-Pacific region, driven by its extensive construction industry and manufacturing sector. The country's ambitious infrastructure development plans, including significant investments in construction projects, sustain strong demand for diesel power engines. China's strategic focus on ensuring stable diesel supply through refinery expansions and new facility construction demonstrates its commitment to supporting industrial growth. The nation's comprehensive approach to industrial development, coupled with initiatives to improve fuel efficiency and reduce emissions, reinforces its market leadership.

Diesel Power Engine Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by rapid industrialization and increasing power requirements. The country's extensive power deficit and growing industrial sector create substantial opportunities for diesel power engines. The expansion of critical sectors such as telecommunications, data centers, and healthcare facilities drives demand for reliable backup power solutions. India's focus on infrastructure development, particularly in smart cities and industrial corridors, coupled with the need for uninterrupted power supply in various sectors, supports market growth.

Diesel Power Engine Market in South America

The South American diesel power engine market, encompassing Brazil, Argentina, and other countries, demonstrates steady growth potential driven by diverse industrial applications. Brazil emerges as the largest market, benefiting from its extensive industrial base and significant power requirements in remote locations. Argentina shows the fastest growth trajectory, supported by its expanding mining sector and increasing industrial activities. The region's challenging power infrastructure and growing industrial requirements create sustained demand for diesel power engines, particularly in mining, oil and gas, and construction sectors.

Diesel Power Engine Market in Middle East & Africa

The Middle East & Africa region presents a diverse market landscape for diesel power engines, with significant contributions from Saudi Arabia, Nigeria, and South Africa. Saudi Arabia maintains its position as the largest market, driven by its extensive industrial infrastructure and ongoing development projects. Nigeria demonstrates the fastest growth potential, supported by its expanding industrial sector and significant power infrastructure challenges. The region's unique combination of developed and emerging economies, coupled with extensive off-grid power requirements and industrial development initiatives, creates sustained demand for diesel power engines across various applications.

Get Analysis on Important Geographic Markets

Download PDF

Diesel Power Engine Industry Overview

Top Companies in Diesel Power Engine Market

The diesel engine market features prominent global players like Cummins, Caterpillar, Volvo, Mitsubishi Heavy Industries, and Rolls-Royce, leading the industry through continuous innovation and strategic expansion. These diesel engine companies are increasingly focusing on developing next-generation diesel engine technology with enhanced fuel efficiency and reduced emissions through technologies like exhaust gas recirculation and selective catalytic reduction. The industry witnesses significant investments in research and development to create sustainable competitive advantages, with companies exploring alternative fuel compatibility and hybrid solutions. Market leaders are strengthening their positions through strategic partnerships and licensing agreements, particularly in emerging markets, while simultaneously expanding their service networks and aftermarket support capabilities. The emphasis on telematics integration and digital solutions for engine monitoring and maintenance has become a key differentiator, alongside efforts to optimize manufacturing processes and supply chain resilience.

Global Leaders Dominate Consolidated Market Structure

The diesel engine industry exhibits a relatively consolidated structure dominated by large multinational corporations with diverse product portfolios and extensive manufacturing capabilities. These established players leverage their strong brand recognition, comprehensive distribution networks, and significant financial resources to maintain their market positions, while regional players focus on specific applications or geographical markets. The industry landscape is characterized by high entry barriers due to substantial capital requirements, stringent regulatory compliance needs, and the importance of established relationships with OEMs and end-users.

Recent market activities indicate a trend toward strategic consolidations and partnerships, as evidenced by notable acquisitions and joint ventures between major players and technology providers. Companies are increasingly pursuing vertical integration strategies to enhance control over critical components and technologies, while also establishing strategic alliances to access new markets and technologies. The market structure is further shaped by the presence of specialized manufacturers focusing on specific applications or power ranges, though their market share remains limited compared to the global leaders.

Innovation and Sustainability Drive Future Success

Success in the diesel powertrain market increasingly depends on companies' ability to balance environmental compliance with performance optimization while maintaining cost competitiveness. Market incumbents must focus on developing proprietary technologies that address stricter emission standards while maintaining engine efficiency, alongside building comprehensive service networks and digital capabilities to enhance the customer value proposition. The ability to offer flexible solutions that can accommodate various fuel types and hybrid configurations will become increasingly critical, as will the capacity to provide comprehensive lifecycle support and predictive maintenance solutions.

For emerging players and contenders, the path to market share growth lies in identifying and exploiting niche segments while developing innovative solutions that address specific customer pain points or regulatory requirements. Success factors include establishing strong relationships with key component suppliers, developing specialized expertise in emerging technologies, and creating efficient after-sales service networks. The industry's future will be shaped by the ability to navigate increasing regulatory pressures, particularly regarding emissions and fuel efficiency standards, while managing the threat from alternative power solutions and maintaining strong relationships with increasingly concentrated customer bases in key sectors like construction, mining, and power generation.

Diesel Power Engine Market Leaders

-

Caterpillar Inc.

-

Cummins Inc.

-

Volvo AB

-

Kohler Co

-

Mitsubishi Heavy Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Diesel Power Engine Market News

- October 2023: Mitsubishi Heavy Industries Engine & Turbocharger Ltd (MHIET), a part of Mitsubishi Heavy Industries (MHI) Group, approved the use of unblended Hydrotreated Vegetable Oil (HVO) that complies with EN15940 and blends with diesel fuel. Approved engine series include SM, SD, SB, SA, SH, SR, and SU series for all applications, including power systems and marine.

- August 2023: United H2 Limited (UHL) and its subsidiary H2i Technology launched hydrogen injection kits for diesel-fueled combustion engines.

- May 2023: Caterpillar announced the introduction of two new industrial diesel power units (IPU). The new engines are intended for construction, material handling, and other off-highway applications in the 74 to 134-hp power range while meeting the emissions standards of higher regulated markets. These new engines meet the emissions standards of EU Stage V, US EPA Tier 4 Final, China Non-road IV, Korea Stage V, and Japan 2014. With the addition of these power units, Caterpillar offers industrial engines from 48 to 950 hp, addressing the emission standards of higher regulated markets. These kits will be used within diesel-powered combustion engines to reduce carbon emissions and fuel costs for consumers and industries operating within the oil and gas and mining sectors. As per the company, hydrogen systems could reduce exhaust smoke from diesel engines by 49% and exhaust opacity by 50%.

Diesel Power Engine Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Industrial Sector

- 4.5.1.2 Rising Power Outages To Increase The Demand For Diesel Generators

- 4.5.2 Restraints

- 4.5.2.1 Increasing Shift Toward Cleaner Energy Resources

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By End User

- 5.1.1 Industrial

- 5.1.2 Commercial

- 5.1.3 Residential

-

5.2 By Application

- 5.2.1 Standby

- 5.2.2 Prime

- 5.2.3 Peak Shaving

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 ASEAN Countries

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Kohler Co

- 6.3.4 Volvo AB

- 6.3.5 Mitsubishi Heavy Industries Ltd

- 6.3.6 Wartsila Oyj Abp

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 Rolls-Royce Holding PLC

- 6.3.10 YANMAR HOLDINGS Co. Ltd

- *List Not Exhaustive

- 6.4 Market Ranking/Share (%) Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity Of Hybrid Power Diesel Generators

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Diesel Power Engine Industry Segmentation

A diesel power engine is an internal combustion engine in which compressed air is heated to a high enough temperature to ignite diesel fuel pumped into the cylinder, where combustion and expansion operate a piston.

The diesel power engine market is segmented by end user, application, and geography. By end user, the market is segmented into industrial, commercial, and residential. By application, the market is segmented into standby, prime, and peak shaving. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also covers the market size and forecasts for the diesel power engine market across major regions. For each segment, the market sizing and forecasts were made based on revenue (USD).

| By End User | Industrial | ||

| Commercial | |||

| Residential | |||

| By Application | Standby | ||

| Prime | |||

| Peak Shaving | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| ASEAN Countries | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Nigeria | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Diesel Power Engine Market Research FAQs

How big is the Diesel Power Engine Market?

The Diesel Power Engine Market size is expected to reach USD 12.29 billion in 2025 and grow at a CAGR of 6.39% to reach USD 16.75 billion by 2030.

What is the current Diesel Power Engine Market size?

In 2025, the Diesel Power Engine Market size is expected to reach USD 12.29 billion.

Who are the key players in Diesel Power Engine Market?

Caterpillar Inc., Cummins Inc., Volvo AB, Kohler Co and Mitsubishi Heavy Industries, Ltd. are the major companies operating in the Diesel Power Engine Market.

Which is the fastest growing region in Diesel Power Engine Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Diesel Power Engine Market?

In 2025, the Asia Pacific accounts for the largest market share in Diesel Power Engine Market.

What years does this Diesel Power Engine Market cover, and what was the market size in 2024?

In 2024, the Diesel Power Engine Market size was estimated at USD 11.50 billion. The report covers the Diesel Power Engine Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Diesel Power Engine Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Diesel Power Engine Market Research

Mordor Intelligence offers a comprehensive analysis of the diesel power engine industry. We leverage extensive expertise in diesel engine technology and market dynamics. Our research covers the entire spectrum of diesel engine components, ranging from diesel powertrains to complete diesel power systems. The report provides detailed insights into industrial diesel engine applications, marine diesel engine developments, and automotive diesel engine innovations. We focus particularly on compression ignition engine advancements and diesel power generation capabilities.

Stakeholders across the diesel engine industry benefit from our thorough analysis of diesel machinery trends and diesel propulsion systems. The report covers various segments, including stationary diesel engine applications, diesel power plant operations, and commercial diesel engine developments. Our research insights are available as an easy-to-read report PDF download, featuring comprehensive data on diesel power equipment and diesel power unit specifications. The analysis includes a detailed examination of diesel engine companies and their technological innovations. This provides valuable insights for industry decision-makers and investors in the diesel power engine market.