| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 88.03 Billion |

| Market Size (2030) | USD 119.14 Billion |

| CAGR (2025 - 2030) | 6.24 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

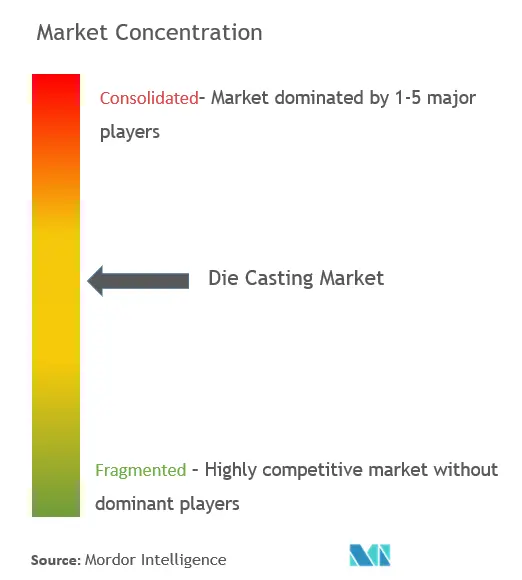

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Die Casting Market Analysis

The Die Casting Market size is estimated at USD 88.03 billion in 2025, and is expected to reach USD 119.14 billion by 2030, at a CAGR of 6.24% during the forecast period (2025-2030).

The die casting industry is experiencing significant transformation driven by technological advancements and strategic consolidations. Major manufacturers are investing heavily in advanced die casting technologies, particularly in mega casting machines and automated production systems. For instance, in January 2023, General Motors announced a substantial investment of USD 918 million across four manufacturing plants, with USD 55 million specifically allocated for EV die casting components. The industry is witnessing a trend toward larger, more sophisticated die casting equipment, as evidenced by Tesla's implementation of 9,000-ton Giga presses for Cybertruck production in late 2022.

The shift towards electric vehicles is revolutionizing die casting manufacturing processes and material requirements. According to industry data, electric vehicles currently use 25% to 27% more aluminum by weight compared to traditional combustion engine vehicles, averaging 250 kg per unit. This trend is driving significant innovations in die casting technologies, with manufacturers developing specialized processes for EV-specific components such as battery housings and structural frames. The industry is seeing a particular focus on thin-wall casting manufacturing capabilities and multi-material integration to meet the unique requirements of electric vehicle production.

Supply chain optimization has become a critical focus area, with manufacturers implementing vertical integration strategies and localizing production capabilities. In 2023, several major die casting manufacturers expanded their global footprint through strategic partnerships and facility expansions. A notable example is Xusheng's USD 350 million investment in May 2023 to establish its first North American production facility in Mexico, focusing on metal components for automotive powertrains, chassis, and battery systems. This trend reflects the industry's move toward more resilient and geographically diverse supply chains.

The industry is witnessing substantial investments in manufacturing capacity expansion and technological upgrades. In March 2023, UBE Corporation developed an ultra-large die casting machine specifically designed for electric vehicle components, demonstrating the industry's commitment to innovation. Similarly, GF Casting Solutions inaugurated a new plant in Shenyang, Northern China, in April 2023, focusing on complex aluminum and magnesium metal casting for the automotive industry. These developments highlight the industry's response to increasing demand for sophisticated die-cast components and the growing emphasis on sustainable manufacturing practices.

Die Casting Market Trends

Growth of the Automotive Industry is Likely to Drive Demand for Die Casting Market

The automotive industry's increasing focus on lightweight vehicles and electric mobility is creating substantial demand for die casting components. According to industry data, the average aluminum content per vehicle is expected to reach 550 pounds (250 kg) by 2026 for light-duty trucks, representing a significant increase in material usage across automotive body sheets, castings, and extrusions. This transition is exemplified by electric vehicle manufacturers like Tesla, which uses over 800 pounds (360 kg) of aluminum for structural components, castings, extrusions, and vehicle bodies. The industry's commitment to lightweight materials is further evidenced by recent investments, such as Wencan Group's 2022 announcement to build a production base for aluminum die casting parts specifically for New Energy Vehicles (NEVs) in China's Anhui Province.

The automotive sector's evolution toward electric vehicles has intensified the demand for die casting solutions, particularly in manufacturing critical components like battery housings and structural parts. This trend is supported by significant industry developments, such as Sandhar Engineering's 2022 expansion into manufacturing various electrical, electronic, and mechanical automotive parts through die casting processes. Additionally, major automotive manufacturers are actively investing in die casting capabilities, as demonstrated by General Motors' January 2023 announcement of a USD 918 million investment across four manufacturing plants, with USD 55 million specifically allocated for EV die casting components. These investments reflect the industry's recognition of die casting as a crucial technology for meeting the demands of next-generation vehicles.

Understand The Key Trends Shaping This Market

Download PDF

Benefits of Gravity Die Casting May Propel the Market Growth

Gravity die casting offers several compelling advantages that are driving its adoption across various industries. The process provides significantly lower tooling costs compared to high pressure die casting while enabling the production of high-quality heat-treatable aluminum parts. This cost-effectiveness, combined with the ability to produce complex aluminum parts with superior surface finish and dimensional accuracy, makes gravity die casting particularly attractive for manufacturers seeking to optimize their production processes. The method's suitability for automated medium to high-volume production has made it increasingly popular among manufacturers looking to scale their operations efficiently.

The versatility of gravity die casting is demonstrated through its wide range of applications across multiple sectors. In the automotive industry, it is extensively used for manufacturing gearbox cases, structural components, and engine components. The process has also gained significant traction in the electronics sector for producing components used in lighting fixtures, control panels, and electronic housings. Recent technological advancements have further enhanced the capabilities of gravity die casting, as evidenced by BMW's March 2022 announcement regarding the implementation of innovative multi-plate die casting technology at their light metal foundry. This new process increases profitability and reduces energy consumption compared to traditional die casting systems, while enabling the production of function-optimized component designs through direct gating in multi-plate mold technology.

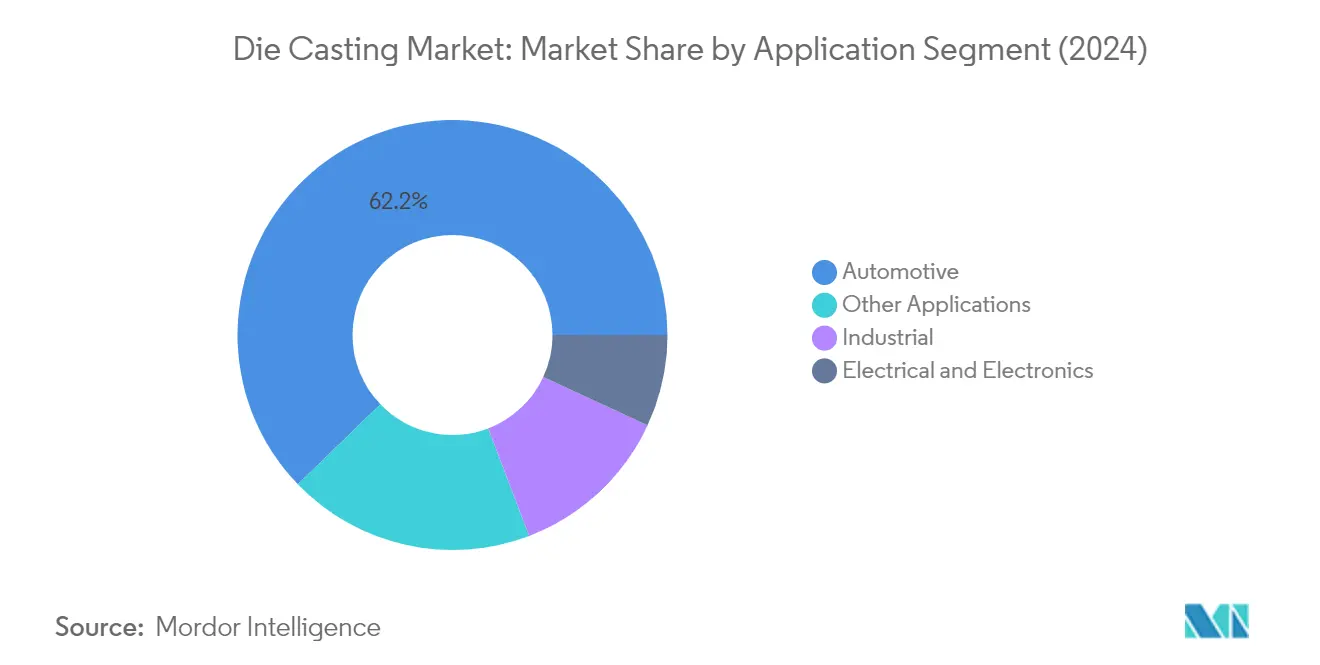

Segment Analysis: By Application

Automotive Segment in Die Casting Market

The automotive segment dominates the global die casting market, commanding approximately 62% of the total market share in 2024. This significant market position is primarily driven by the increasing adoption of lightweight components in vehicle manufacturing to improve fuel efficiency and reduce emissions. The segment's growth is further bolstered by the rising demand for electric vehicles, which require a higher density of die-cast components such as battery housings, motor casings, and structural parts. Major automotive manufacturers are increasingly investing in advanced die-casting technologies to produce complex, lightweight components, particularly for electric vehicle applications. The segment's robust performance is also supported by stringent environmental regulations pushing automakers toward lightweight materials and the growing trend of vehicle electrification across global markets.

Automotive Segment in Die Casting Market (Growth Perspective)

The automotive segment is projected to maintain strong growth momentum during the forecast period 2024-2029, with an expected growth rate of approximately 6% annually. This growth trajectory is driven by several key factors, including the accelerating transition to electric vehicles, which requires sophisticated die-cast components for battery enclosures and structural parts. The segment's expansion is further supported by ongoing technological advancements in die-casting processes, enabling the production of larger and more complex automotive components. Additionally, the increasing focus on vehicle weight reduction to meet stringent emission standards continues to drive the adoption of die-cast aluminum components across various automotive applications, from structural components to powertrain parts.

Remaining Segments in Die Casting Market

The electrical and electronics, industrial, and other applications segments collectively represent significant opportunities in the die casting market. The electrical and electronics segment is particularly notable for its growing demand in manufacturing components for consumer electronics, LED lighting, and telecommunications equipment. The industrial segment maintains its importance through applications in machinery, equipment manufacturing, and industrial automation components. Other applications, including aerospace, construction, and medical equipment, contribute to market diversification by providing specialized applications for die-cast components. These segments benefit from ongoing technological advancements in die-casting processes and the increasing adoption of lightweight materials across various industries.

Segment Analysis: By Process

Pressure Die Casting Segment in Die Casting Market

Pressure die casting dominates the global die casting market, commanding approximately 55% of the total market share in 2024. This significant market position is attributed to its effectiveness in mass manufacturing complex shapes with high durability and seamless integration capabilities with other mating components. The process has become vital in the production of transmission components, powertrain elements, and battery compartment housings, particularly for hybrid and electric vehicles. The automotive industry's increasing demand for lightweight components and the growing adoption of high-pressure die-casting technology have further strengthened this segment's position. Major manufacturers are actively expanding their pressure die-casting capabilities, with several companies investing in large-tonnage machines ranging from 4,000 to 6,000 tons to meet the rising demand for structural automotive components.

Vacuum Die Casting Segment in Die Casting Market

The vacuum die casting segment is emerging as the fastest-growing segment in the die casting market, projected to grow at approximately 7% during 2024-2029. This growth is primarily driven by the segment's ability to produce superior weldable automotive products compared to conventional die-casting processes. The vacuum die-casting production process eliminates air from the mold, allowing the front of molten metal to merge freely without forming shuts or pores, which is a major advantage over traditional pressure die-casting. The technology's ability to handle metals with high melting temperatures and produce components with enhanced metallurgical characteristics has made it increasingly attractive to manufacturers. The automotive industry's growing focus on quality and performance, particularly in electric vehicle components, has further accelerated the adoption of vacuum die-casting technology.

Remaining Segments in Process Segmentation

The squeeze die casting and other processes segments continue to play important roles in the die casting market. Squeeze die casting offers unique advantages in producing high-quality heat-treatable parts with excellent mechanical properties and microstructural refinement. This process is particularly valuable for manufacturing automotive suspension components and other parts requiring high strength and integrity. Other processes, including semi-solid die casting and gravity die casting, serve specific niche applications where specialized characteristics are required. These processes are particularly important in industries such as aerospace, medical equipment manufacturing, and specialized industrial applications where unique material properties or complex geometries are essential.

Segment Analysis: By Raw Material

Aluminum Segment in Die Casting Market

The aluminum die casting segment dominates the global die casting market, accounting for approximately 81% of the total market value in 2024. This significant market share is driven by aluminum's exceptional properties, including its lightweight nature, high corrosion resistance, and excellent thermal conductivity. The automotive industry's increasing focus on lightweight materials has been a major factor in aluminum's dominance, particularly in the manufacturing of electric vehicle components. The material's ability to withstand extreme temperatures while maintaining structural integrity makes it ideal for various applications across automotive, aerospace, and industrial sectors. Additionally, aluminum's abundance in the Earth's crust makes it a cost-effective option compared to other metals, contributing to its widespread adoption. The segment's growth is further supported by stringent environmental regulations promoting fuel efficiency and reduced emissions, driving manufacturers to increasingly utilize aluminum die casting processes.

Magnesium Segment in Die Casting Market

The magnesium die casting segment is emerging as the fastest-growing segment in the die casting market, with a projected growth rate of approximately 6% during 2024-2029. This growth is primarily driven by magnesium's exceptional lightweight properties, being approximately 30% lighter than aluminum and 75% lighter than steel. The material's high strength-to-weight ratio makes it particularly attractive for applications where weight reduction is critical, such as in electric vehicles and aerospace components. Magnesium die casting also offers excellent dimensional stability, high impact resistance, and superior electromagnetic interference shielding capabilities, making it increasingly popular in electronic and automotive applications. The segment's growth is further supported by technological advancements in die casting processes that have improved the handling and processing of magnesium alloys, enabling more complex and precise component manufacturing.

Remaining Segments in Raw Material Segmentation

The zinc die casting segment completes the raw material segmentation, offering unique advantages in the die casting market. Zinc die casting is particularly valued for its ability to produce components with excellent surface finish, high dimensional accuracy, and superior mechanical properties like toughness. The segment plays a crucial role in manufacturing automotive components such as door lock housing, pawls, and sensor components. Zinc die-cast products often require minimal post-processing, making them cost-effective for certain applications. The material's better thermal and electrical conductivity compared to other die-casting materials makes it particularly suitable for electronic and electrical applications, while its ability to be cast into thin-walled and intricate shapes provides designers with greater flexibility in component design.

Die Casting Market Geography Segment Analysis

Die Casting Market in North America

The North American die casting market demonstrates robust growth driven by a significant automotive manufacturing presence and increasing adoption of electric vehicles. The United States and Canada represent the key markets in this region, with both countries showing a strong focus on technological advancement in die casting processes. The region benefits from well-established infrastructure, research capabilities, and the presence of major die casting manufacturers who continue to invest in expanding their production capabilities.

Die Casting Market in the United States

The United States dominates the North American die casting market as the largest market in the region. The country's market position is strengthened by the presence of over 300 die-casting companies operating approximately 400 distinct die-casting plants. The automotive sector remains the primary growth driver, with increasing demand for lightweight vehicle components and electric vehicle parts. The US market accounts for approximately 89% of the North American die casting market in 2024, supported by robust domestic manufacturing capabilities and continuous technological innovations in high-pressure die casting processes.

Die Casting Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 6% during 2024-2029. The country's die casting industry is experiencing significant expansion, particularly in the automotive sector, with an increasing focus on electric vehicle component manufacturing. Canada's growth is driven by strategic investments in advanced die casting technologies, strong government support for manufacturing initiatives, and the presence of major automotive OEMs. The country's die casting industry benefits from its rich aluminum resources and established manufacturing infrastructure, positioning it well for sustained growth in the coming years.

Die Casting Market in Europe

The European die casting market showcases strong technological advancement and innovation, particularly in automotive and industrial applications. The region's market is characterized by the presence of established players in Germany, Italy, France, the United Kingdom, and Russia. European manufacturers are increasingly focusing on sustainable practices and electric vehicle component production, driving significant market evolution. The region benefits from strong research and development capabilities and a robust automotive manufacturing base.

Die Casting Market in Germany

Germany maintains its position as the largest die casting market in Europe, representing approximately 30% of the European market in 2024. The country's dominance is attributed to its advanced automotive manufacturing sector, strong technological capabilities, and the presence of major die casting equipment manufacturers. German companies are at the forefront of developing innovative die casting solutions for electric vehicles and lightweight automotive components, supported by substantial investments in research and development.

Die Casting Market in Italy

Italy emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 6% during 2024-2029. The country's die casting industry is experiencing rapid advancement, particularly in machinery manufacturing and automotive component production. Italy's growth is driven by its strong tradition in die casting machinery manufacturing, continuous technological innovation, and increasing export activities. The country's expertise in high-pressure die casting technology and growing focus on lightweight automotive components position it favorably for continued expansion.

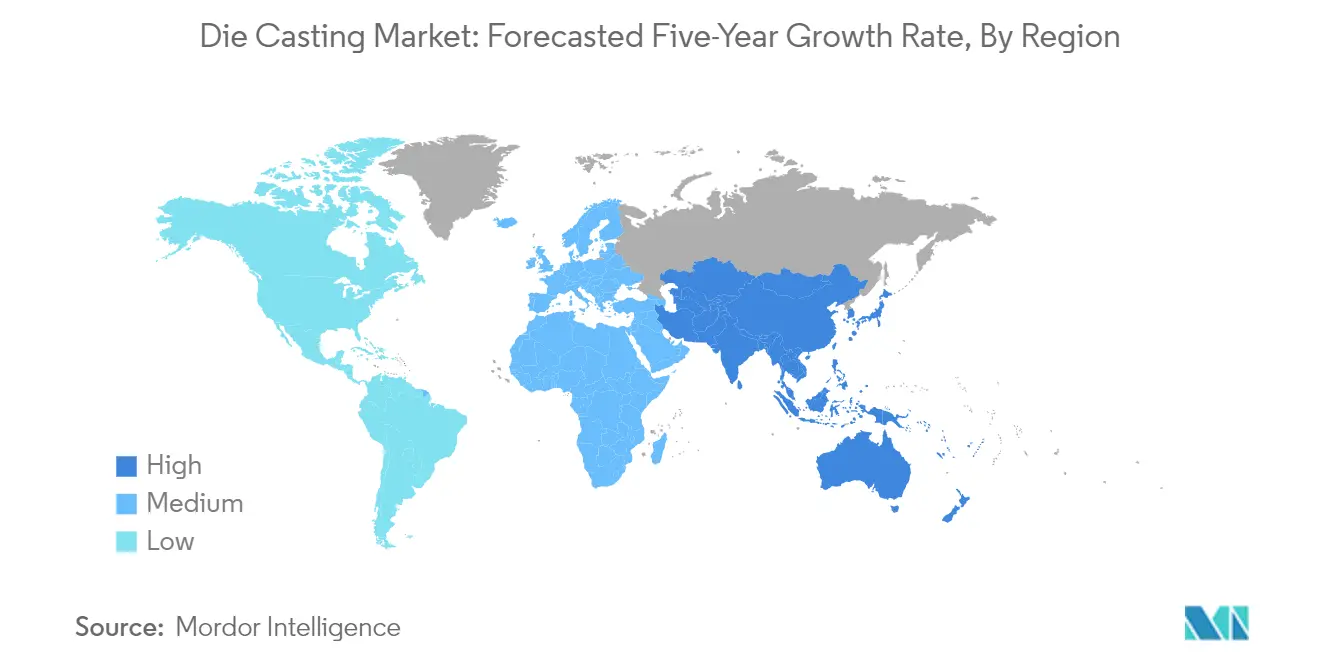

Die Casting Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic die casting market globally, with significant manufacturing capabilities across multiple countries. China, Japan, India, and South Korea serve as major manufacturing hubs, while emerging markets like Thailand, Malaysia, and Indonesia demonstrate increasing capabilities. The region's growth is driven by robust automotive production, an expanding electronics industry, and increasing investments in manufacturing infrastructure.

Die Casting Market in China

China maintains its position as the dominant force in the Asia-Pacific die casting market. The country's market leadership is supported by extensive manufacturing infrastructure, cost-competitive production capabilities, and strong government support for industrial development. Chinese manufacturers are increasingly focusing on high-end die casting applications, particularly in electric vehicle components and advanced industrial applications.

Die Casting Market in Thailand

Thailand emerges as the fastest-growing market in the Asia-Pacific region. The country's die casting industry is experiencing rapid development, particularly in automotive component manufacturing and electronics applications. Thailand's growth is supported by increasing foreign investments, government initiatives promoting manufacturing sector development, and growing integration into global automotive supply chains.

Die Casting Market in South America

The South American die casting market continues to evolve, with Brazil and Argentina serving as key manufacturing hubs. Brazil emerges as both the largest and fastest-growing market in the region, driven by its substantial automotive industry and increasing investments in manufacturing capabilities. The region's market development is supported by growing domestic demand, improving industrial infrastructure, and increasing integration with global supply chains.

Die Casting Market in Middle East & Africa

The Middle East & Africa die casting market shows promising growth potential, with Turkey and South Africa as key markets. Turkey represents the largest market in the region, while also demonstrating the fastest growth rate. The region's market development is driven by increasing investments in manufacturing capabilities, a growing automotive sector, and rising demand for die-cast components in construction and industrial applications.

Get Analysis on Important Geographic Markets

Download PDF

Die Casting Industry Overview

Top Companies in Die Casting Market

The die casting market features prominent players like Alcoa Corporation, Nemak, Linamar Corporation, Ryobi Die Casting, and Georg Fischer Limited leading the industry through continuous innovation and strategic initiatives. Companies are increasingly focusing on developing independent technologies and automated solutions to enhance production efficiency and quality control. The die casting industry witnesses significant investments in plant expansions and modernization efforts, particularly in emerging markets across Asia-Pacific. Strategic collaborations and joint ventures are becoming more prevalent, especially in the electric vehicle segment, as companies aim to capitalize on the growing demand for lightweight metal components. Market leaders are also emphasizing sustainability initiatives, including the development of eco-friendly manufacturing processes and the use of recycled materials, while simultaneously expanding their global footprint through strategic acquisitions and partnerships.

Fragmented Market with Strong Regional Players

The die casting market exhibits a highly fragmented structure, with the top twelve players collectively holding less than one-third of the market share, while numerous small and medium-sized enterprises dominate the remaining landscape. Global conglomerates maintain their competitive edge through extensive research and development capabilities, advanced manufacturing facilities, and strong distribution networks, while regional specialists thrive by leveraging their local market knowledge and customer relationships. The market witnesses a mix of vertically integrated manufacturers and specialized casting manufacturing service providers, with many companies expanding their capabilities through strategic acquisitions and technological partnerships.

The industry is characterized by ongoing consolidation activities, particularly in mature markets, as larger players seek to strengthen their market position and expand their technological capabilities. Mergers and acquisitions are primarily driven by the need to access new geographic markets, acquire advanced technologies, and achieve economies of scale. Regional players, especially in emerging markets, are increasingly becoming attractive acquisition targets for global companies looking to establish a stronger presence in high-growth regions and diversify their customer base.

Innovation and Adaptability Drive Market Success

Success in the die casting industry increasingly depends on companies' ability to innovate and adapt to changing industry demands, particularly in the automotive and electronics sectors. Incumbent players are focusing on developing proprietary technologies, investing in automation and digitalization, and expanding their product portfolios to maintain their market position. Companies are also emphasizing the development of lightweight solutions and complex components to address the growing demands of electric vehicle manufacturers and other emerging applications. Building strong relationships with key customers, maintaining high quality standards, and offering value-added services have become crucial factors for sustained growth.

Market contenders can gain ground by focusing on niche applications, developing specialized expertise in high-growth segments, and leveraging advanced technologies to improve operational efficiency. The industry faces moderate substitution risks from alternative manufacturing processes, making it essential for companies to continuously innovate and demonstrate the superior cost-effectiveness and quality of precision casting solutions. Regulatory requirements, particularly environmental regulations and safety standards, are becoming increasingly stringent, requiring companies to invest in compliance measures and sustainable practices. Success also depends on managing raw material costs, maintaining efficient supply chains, and developing strong relationships with both suppliers and end-users.

Die Casting Market Leaders

-

Nemak

-

Linamar Corporation

-

Alcoa Corporation

-

Rheinmetall AG

-

Form Technologies Inc. (Dynacast)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Die Casting Market News

- In March 2022, Ningbo Tuopu Group Co. Ltd (Tuopu Group) announced that the integrated huge die-casting rear cabin that is developed based on the 7,200-ton giant die-casting machine rolled off the assembly line at the Hangzhou Bay plant in Ningbo.

- In March 2021, Sandhar Technologies entered into a non-binding Memorandum of Understanding with Unicast Autotech to acquire its aluminum die-casting business.

- In 2021, Foryou Corporation (Foryou) unveiled several die-casted aluminum engine components, new energy drive components, and smart key components at the Auto Shanghai 2021 show.

- In March 2021, Rheinmetall AG won an engine block supply contract of over EUR 100 million for a German car manufacturer. Full-scale production is planned to begin in 2023. The lifetime of the contract extends beyond 2030.

Die Casting Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD Billion)

-

5.1 By Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial

- 5.1.4 Other Applications

-

5.2 By Process

- 5.2.1 Pressure Die Casting

- 5.2.2 Vacuum Die Casting

- 5.2.3 Squeeze Die Casting

- 5.2.4 Other Processes

-

5.3 By Raw Material

- 5.3.1 Aluminum

- 5.3.2 Maginesium

- 5.3.3 Zinc

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Thailand

- 5.4.3.6 Malaysia

- 5.4.3.7 Indonesia

- 5.4.3.8 South Korea

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Turkey

- 5.4.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles*

- 6.2.1 Form Technologies Inc. (Dynacast)

- 6.2.2 Nemak

- 6.2.3 Endurance Technologies Limited

- 6.2.4 Sundaram Clayton Ltd

- 6.2.5 Shiloh Industries

- 6.2.6 Georg Fischer Limited

- 6.2.7 Koch Enterprises (Gibbs Die Casting Group)

- 6.2.8 Bocar Group

- 6.2.9 Engtek Group

- 6.2.10 Rheinmetall AG (Rheinmetall Automotive, formerly KSPG AG)

- 6.2.11 Rockman Industries

- 6.2.12 Ryobi Die Casting Ltd

- 6.2.13 Linamar Corporation

- 6.2.14 Meridian Lightweight Technologies UK Ltd

- 6.2.15 Sandhar Group

- 6.2.16 Alcoa Corporation

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Die Casting Industry Segmentation

Die casting is an automated casting process for producing metal parts of a particular shape are produced by pouring molten material into a mold under pressure.

The Die Casting Market is Segmented by Application (Automotive, Electrical and Electronics, Industrial, and Other Applications), Process (Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, and Other Processes), Raw Material (Aluminum, Magnesium, and Zinc), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa).

| By Application | Automotive | ||

| Electrical and Electronics | |||

| Industrial | |||

| Other Applications | |||

| By Process | Pressure Die Casting | ||

| Vacuum Die Casting | |||

| Squeeze Die Casting | |||

| Other Processes | |||

| By Raw Material | Aluminum | ||

| Maginesium | |||

| Zinc | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Thailand | |||

| Malaysia | |||

| Indonesia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | South Africa | ||

| Turkey | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Die Casting Market Research FAQs

How big is the Die Casting Market?

The Die Casting Market size is expected to reach USD 88.03 billion in 2025 and grow at a CAGR of 6.24% to reach USD 119.14 billion by 2030.

What is the current Die Casting Market size?

In 2025, the Die Casting Market size is expected to reach USD 88.03 billion.

Who are the key players in Die Casting Market?

Nemak, Linamar Corporation, Alcoa Corporation, Rheinmetall AG and Form Technologies Inc. (Dynacast) are the major companies operating in the Die Casting Market.

Which is the fastest growing region in Die Casting Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Die Casting Market?

In 2025, the Asia-Pacific accounts for the largest market share in Die Casting Market.

What years does this Die Casting Market cover, and what was the market size in 2024?

In 2024, the Die Casting Market size was estimated at USD 82.54 billion. The report covers the Die Casting Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Die Casting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Die Casting Market Research

Mordor Intelligence provides a comprehensive analysis of the die casting industry, utilizing extensive expertise in the industrial casting and metal forming sectors. Our research covers the full range of processes, including high pressure die casting, gravity die casting, as well as both hot chamber die casting and cold chamber die casting technologies. The report offers detailed insights into metal casting applications, focusing on materials such as aluminum die casting, zinc die casting, magnesium die casting, brass die casting, and copper die casting. Special attention is given to automotive casting applications and precision casting methodologies.

The downloadable report PDF provides stakeholders in the metal forming industry with valuable insights into casting manufacturing trends and developments in foundry equipment. Our analysis spans the entire ecosystem, from casting machinery to industrial mold applications, offering comprehensive coverage of metal components production and metal parts manufacturing. The report examines emerging technologies in metal injection molding and pressure die casting. It also offers a detailed analysis of permanent mold casting and low pressure die casting processes. Stakeholders gain actionable intelligence on foundry equipment market dynamics and developments in the precision casting industry, supporting strategic decision-making across the value chain.