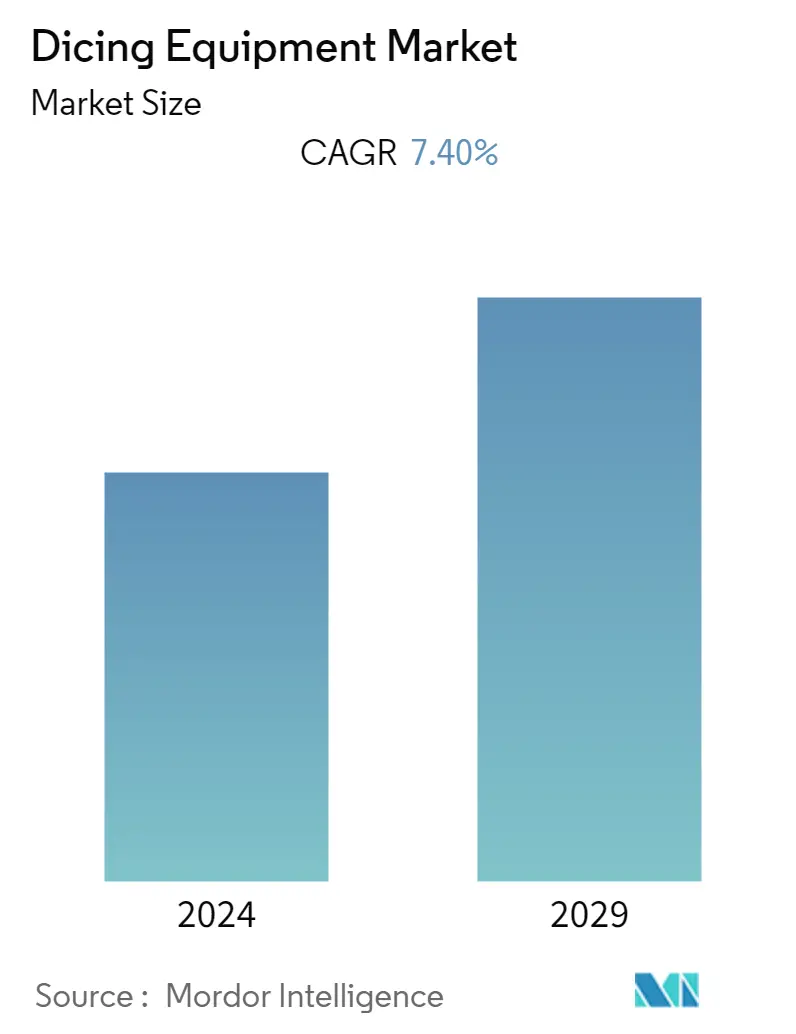

Market Size of Dicing Equipment Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 7.40 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Dicing Equipment Market Analysis

The Dicing Equipment Market is expected to grow by registering a CAGR of 7.4% over the forecast period. The primary factors driving the growth of the dicing equipment market are the increasing demand for smart cards, RFID technology, and automotive power ICs. The increasing consumer electronics market and the inclination toward miniaturization and technology migration has forced market vendors to increase R&D expenditure to reduce the size and improve performance, leading to the emergence of micro-electro-mechanical systems (MEMS) and 3D packaging, which in turn is driving the demand for dicing equipment.

- In electronics manufacturing, IC (integrated circuit) packaging is the final stage of semiconductor device fabrication, in which the tiny block of semiconducting material is encased in a supporting case that prevents physical damage and corrosion. The increasing efforts to make electronic packaging highly resourceful have amplified usage in myriad applications.

- The reduction in package size is inversely proportional to the power dissipation. Therefore, players in the market strive to develop semiconductors that can retain power with reduced size. For instance, NXP Semiconductors' MaxQFP package delivers the same I/O in a smaller footprint. While comparing 16x16 mm 172 MaxQFP to 24x24 mm 176 LQFP, the company claims a reduction of about 55% in footprint.

- Furthermore, the increasing number of electronic components in vehicles or automobiles is a key driver, particularly in hybrid and electric cars, due to the consumer demand for constant connectivity. For instance, according to the International Energy Agency (IEA), the sales of electric vehicles nearly doubled, reaching 6.6 million. The automotive industry's push to deliver autonomous and electric vehicles in the next decade is also driving the growth of the market studied.

- With most RFIDs being integrated into several consumer electronics and identity solutions, such as identification tags and smart cards, end users increasingly demand ultra-smooth surfaces and thinner wafers to incorporate them seamlessly into these devices. Such scenarios, coupled with the strong demand for RFID applications, such as enterprise identity management solutions and automobile telematics, are expected to create more demand for thin wafers, thus providing positive growth for dicing equipment during the forecast period.

- Blade dicing has been the most widely used process in separating silicon wafers into individual chips/devices, both in MEMS and semiconductor technologies. It is also the low-cost dicing technology in many applications, which is expected to drive its demand during the forecast period.

- However, with the miniaturization trend becoming prevalent, the complexity of patterns has increased significantly, increasing the chances of functional defects in manufacturing processes which is among the major factors challenging the growth of the studied market.

- COVID-19 and the economic disruption caused by it resulted in the overall decline in the economies of several nations and a drastic fall in business and trade. The semiconductor or wafer market was no exception and suffered major falls in revenue, manufacturing, and expansion due to the pandemic, which had a similar impact on the dicing equipment market. However, with the semiconductor manufacturers focusing on expanding their production capabilities to match the market demand, the studied market is also expected to follow a similar trajectory.

Dicing Equipment Industry Segmentation

Dicing is the process used to cut or groove semiconductors, glass crystals, and many other types of materials. The instrument used during this process is known as dicing equipment. The dicing technologies are continually evolving due to the rising demand for thinner wafers and more robust die, significantly impacting the dicing equipment industry.

Dicing equipment, such as blade dicing, laser ablation, stealth dicing, and plasma dicing, are considered a part of the study. Equipment trends for various applications across regions have also been analyzed as a part of the study. Also, the impact of COVID-19 on the market has been considered for analysis.

The Dicing Equipment Market is segmented by Dicing Technology (Blade Dicing, Laser Ablation, and Plasma Dicing), Application (Logic & Memory, MEMS Devices, Power Devices, CMOS Image Sensors, and RFID), and Geography (China, Taiwan, South Korea, North America, Europe, and Rest of the World).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Dicing Technology | |

| Blade Dicing | |

| Laser Ablation | |

| Plasma Dicing |

| By Application | |

| Logic & Memory | |

| MEMS Devices | |

| Power Devices | |

| CMOS Image Sensor | |

| RFID |

| By Geography | |

| China | |

| Taiwan | |

| South Korea | |

| North America | |

| Europe | |

| Rest of the World |

Dicing Equipment Market Size Summary

The dicing equipment market is poised for significant growth, driven by the rising demand for smart cards, RFID technology, and automotive power ICs. The consumer electronics sector's expansion and the trend towards miniaturization and technology migration have compelled market players to invest heavily in research and development. This has led to advancements in micro-electro-mechanical systems (MEMS) and 3D packaging, which are boosting the demand for dicing equipment. In electronics manufacturing, dicing equipment plays a crucial role in the final stage of semiconductor device fabrication, where integrated circuits are packaged to prevent damage and corrosion. The push for smaller, more efficient electronic packaging has increased the use of dicing equipment across various applications, particularly in the automotive industry, where the number of electronic components in vehicles is on the rise due to the demand for hybrid and electric cars.

The market is characterized by the widespread use of blade dicing technology, which remains the most cost-effective method for separating silicon wafers into individual chips. Despite challenges such as the complexity of patterns and potential functional defects, the demand for dicing equipment is expected to grow, supported by the increasing need for thin wafers in consumer electronics and identity solutions. The COVID-19 pandemic temporarily disrupted the market, but recovery is anticipated as semiconductor manufacturers expand production capabilities. The competitive landscape features major players like Suzhou Delphi Laser Co. Ltd, ASM Laser Separation International (ALSI) BV, and Neon Tech Co. Ltd, who are focusing on innovation and market expansion. Additionally, initiatives in countries like China and India to bolster local semiconductor industries are expected to further drive market growth.

Dicing Equipment Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitutes

-

-

1.3 Industry Value Chain Analysis

-

1.4 Assessment of the Impact of COVID-19 on the Dicing Equipment Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Dicing Technology

-

2.1.1 Blade Dicing

-

2.1.2 Laser Ablation

-

2.1.3 Plasma Dicing

-

-

2.2 By Application

-

2.2.1 Logic & Memory

-

2.2.2 MEMS Devices

-

2.2.3 Power Devices

-

2.2.4 CMOS Image Sensor

-

2.2.5 RFID

-

-

2.3 By Geography

-

2.3.1 China

-

2.3.2 Taiwan

-

2.3.3 South Korea

-

2.3.4 North America

-

2.3.5 Europe

-

2.3.6 Rest of the World

-

-

Dicing Equipment Market Size FAQs

What is the current Dicing Equipment Market size?

The Dicing Equipment Market is projected to register a CAGR of 7.40% during the forecast period (2024-2029)

Who are the key players in Dicing Equipment Market?

Suzhou Delphi Laser Co. Ltd, SPTS Technologies Limited (KLA Tencor Corporation), ASM Laser Separation International (ALSI) BV, Neon Tech Co. Ltd and Nippon Pulse Motor Taiwan (NPM) Group are the major companies operating in the Dicing Equipment Market.