Dicing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

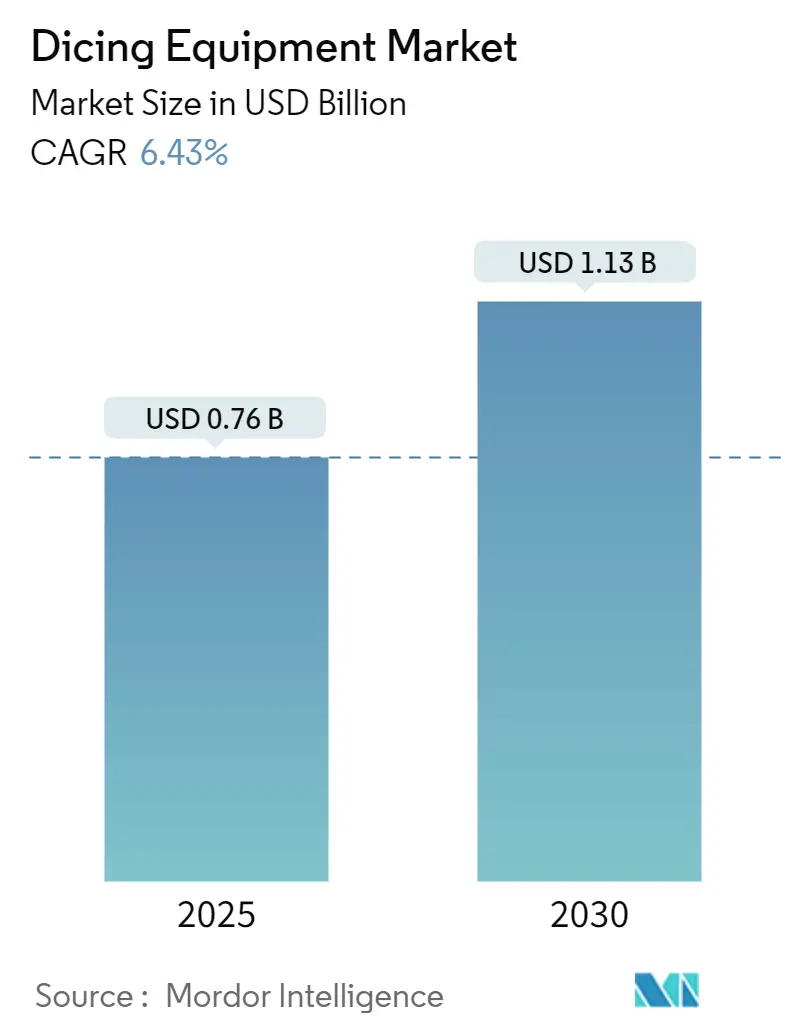

| Market Size (2025) | USD 0.76 Billion |

| Market Size (2030) | USD 1.13 Billion |

| Growth Rate (2025 - 2030) | 6.43% CAGR |

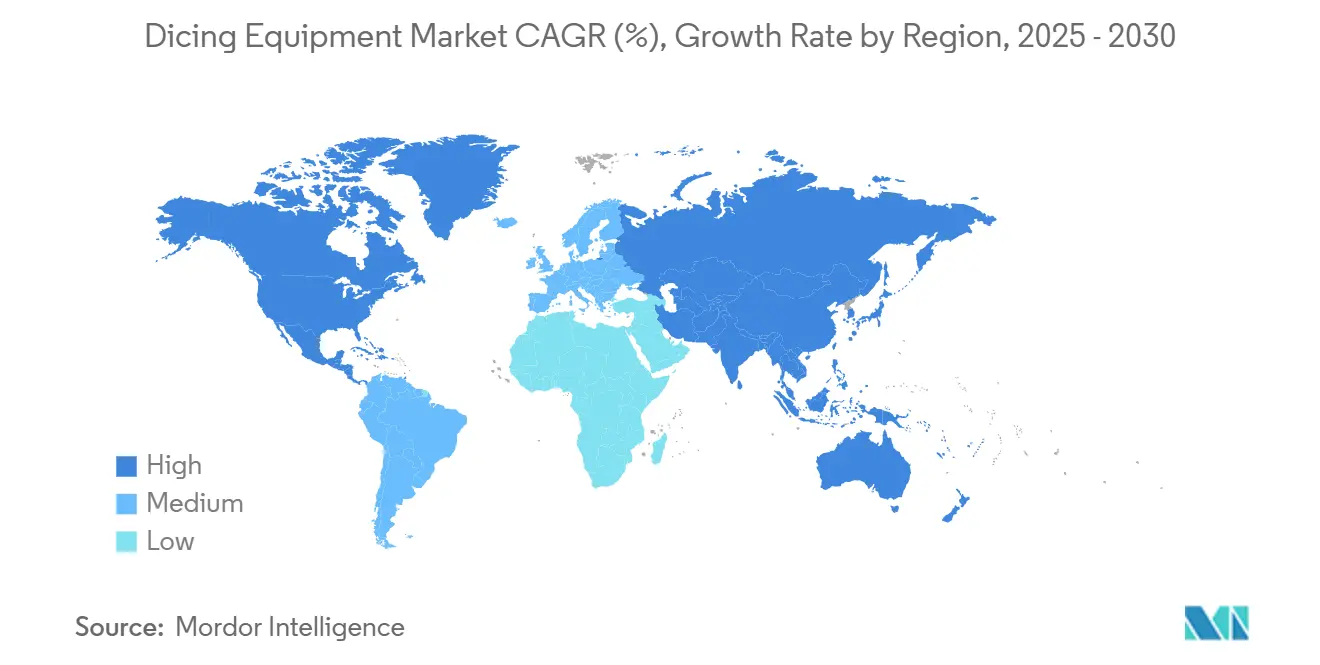

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dicing Equipment Market Analysis by Mordor Intelligence

The dicing equipment market size reached USD 0.83 billion in 2025 and is projected to increase to USD 1.13 billion by 2030, reflecting a 6.43% CAGR over the forecast period. Robust investment in semiconductor backend manufacturing, especially for thinner wafers, advanced packaging formats, and wide-bandgap power devices, underpins this steady expansion. As electric-vehicle, renewable-energy, and AI workloads intensify, chipmakers prioritize high-yield die singulation, favoring systems that combine sub-micrometer positioning accuracy, contamination-controlled processing, and integrated inspection. Continuous migration toward 3D and heterogeneous integration is elevating the demand for plasma and laser dicing tools that minimize chipping and enable narrower streets. Meanwhile, automation upgrades help fabs offset labor constraints, shorten changeover times, and boost overall equipment effectiveness. Supply-chain localization programs in the United States, Europe, and East Asia introduce new regional demand nodes; however, persistent geopolitical frictions surrounding rare-earth laser sources and stringent slurry-disposal rules continue to keep capital intensity high.

Key Report Takeaways

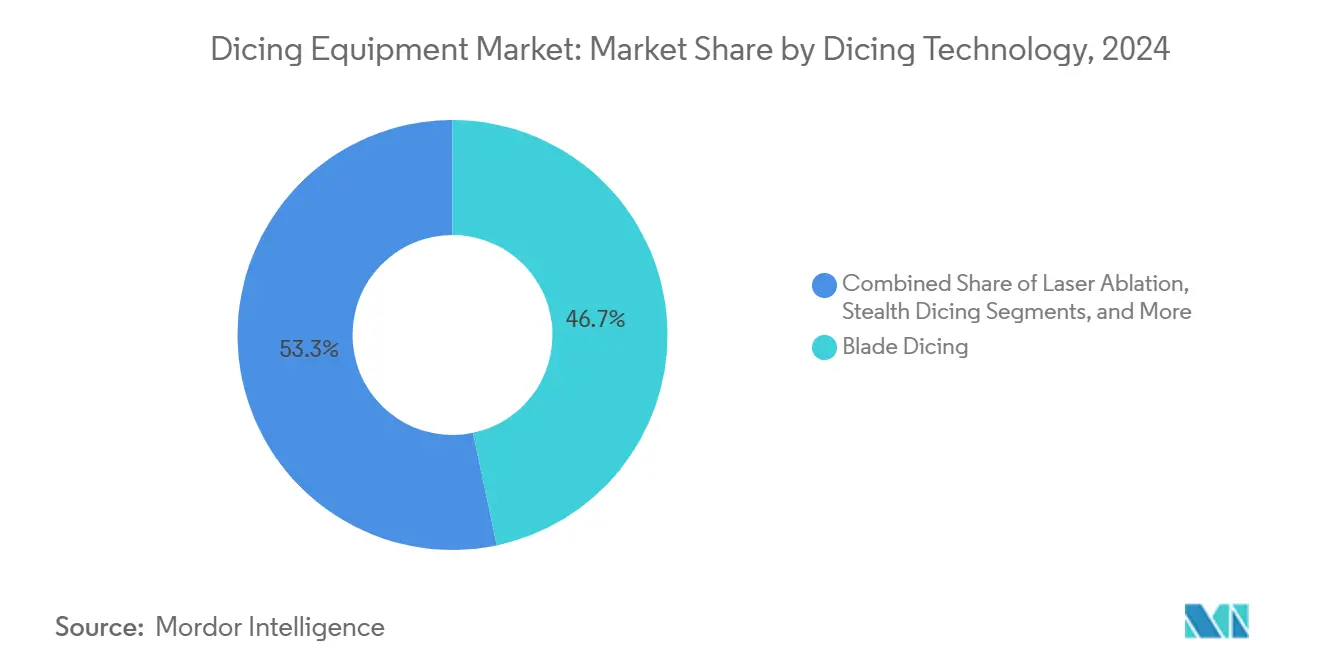

- By dicing technology, blade systems held 46.7% of the dicing equipment market share in 2024; laser ablation systems are projected to post a 6.6% CAGR through 2030.

- By wafer size, the 300 mm segment led with a 38.1% revenue share in 2024, while the ≥ 450 mm segment is advancing at a 6.5% CAGR through 2030.

- By application, CMOS image sensors led with 30.9% revenue share in 2024, while power-device processing is advancing at a 7.1% CAGR to 2030.

- By end-user industry, foundries held 32.2% of the dicing equipment market share in 2024; OSATs are projected to post a 7.2% CAGR through 2030.

- By geography, Asia-Pacific captured 42.90% of the dicing equipment market size in 2024 and is forecast to record a 7.60% CAGR between 2025-2030.

Global Dicing Equipment Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High-precision motion-system innovation | +1.2% | Japan, Germany, global diffusion | Medium term (2-4 years) |

| Advanced logic and memory fab expansion | +1.8% | Asia-Pacific core, Americas spill-over | Short term (≤ 2 years) |

| Rapid uptake of 3D packaging and integration | +1.5% | Taiwan, South Korea, global | Medium term (2-4 years) |

| EV and renewable-energy power-device demand | +1.1% | China, Europe, North America | Long term (≥ 4 years) |

| Shift toward plasma dicing for thin wafers | +0.9% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Chinese localization incentives | +0.7% | Mainland China, secondary Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in High-Precision Motion Systems

Recent motion-control breakthroughs deliver sub-micrometer stage accuracy essential for heterogeneous integration lines. DISCO’s DFD6370 platform, for instance, handles 330 × 330 mm substrates while using selectable height sensors that keep cut depth within ±1 µm, an advantage for panel-level packaging. [1]Source: DISCO Corporation, “Development of DFD6370: A Dicing Saw for Package Singulation,” disco.co.jp Active damping, closed-loop robotics, and vision-guided alignment further trim vibration and thermal drift, enabling higher yield when processing brittle silicon-carbide wafers. Vendors integrating multi-axis stages with on-board metrology now offer turnkey singulation cells that combine cutting, cleaning, and inspection in a single flow, reducing handling defects and cycle time.

Surge in Demand from Advanced Logic and Memory Fabs

SEMI projects cumulative 300 mm fab equipment outlays to reach USD 400 billion between 2025 and 2027, with foundries accounting for USD 230 billion of that total. New extreme-ultraviolet nodes and 3D-stacked DRAM lines magnify backside contamination risks, prompting fabs to specify dicing tools with electrostatic-charge suppression and hermetic chip-collection. As capacity ramps accelerate, particularly at TSMC, Samsung, and China’s domestic foundries, rapid tool delivery and field-service reach become procurement gatekeepers for equipment suppliers.

Rapid Adoption of 3D Packaging and Heterogeneous Integration

IEEE studies document stress-less dicing methods that guard through-silicon-via structures in 2.5D/3D packages.[2]Source: IEEE, “Stress-less Dicing Solution for Thin and Large Die Handling for 2.5D/3D IC Packaging,” ieee.org Plasma and stealth techniques, which eliminate mechanical contact, reduce edge micro-cracks and enable <20 µm streets, freeing valuable silicon area for IO density gains. The packaging turn toward chiplets for AI servers fuels OSAT spending, with plasma dicing lines increasingly ordered alongside hybrid-bonding tools to assure defect-free die walls that sustain high-current micro-bumps.

Growing Deployment of Power Devices for EV and Renewables

Automotive-grade silicon-carbide MOSFETs and on-board chargers now use SiC at more than 75% penetration. Processing hard, thermally conductive SiC demands diamond-coated blades or ultrafast lasers tuned for minimal heat-affected zones. Toolmakers that bundle cooling-optimized chucks, adaptive blade wear sensing, and recipe libraries for 150 mm and 200 mm SiC wafers capture an outsized share of this fast-moving vertical.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capex and long payback | −0.8% | Global, heavier in emerging economies | Short term (≤ 2 years) |

| Yield losses from chipping and micro-cracks | −0.6% | Advanced packaging hubs worldwide | Medium term (2-4 years) |

| Tighter slurry/chemical disposal rules | −0.4% | Europe, North America, and spreading in Asia | Long term (≥ 4 years) |

| Rare-earth–linked laser-source bottlenecks | −0.5% | Non-Chinese supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Slurry/Chemical Disposal Regulations

ISO 14644 cleanroom revisions and emerging PFAS controls require fabs to retrofit wastewater loops, install fluorinated-compound abatement systems, and adopt closed-loop coolants.[3]Source: Technical Safety Services, “ISO Cleanroom Standards,” techsafety.comVendors that embed recycling modules and real-time particulate monitors inside dicing cells help customers meet regulatory thresholds while reducing utility bills; however, the added equipment cost and facility retrofit delay some purchase decisions.

Laser Source Supply Bottlenecks and Rare-Earth Dependency

Export curbs on gallium and germanium have driven longer lead times for high-power laser diodes, inflating the bill of materials for laser wafer-dicing tools. To mitigate exposure, Lumentum and other photonics suppliers are qualifying alternative gain media and expanding their geographic sourcing footprints, although full diversification remains a multi-year effort.[4]Source: Lumentum, “Dicing Applications,” lumentum.com Buyers now weigh material-sourcing resilience alongside throughput in tender evaluations, slightly lengthening sales cycles.

Segment Analysis

By Dicing Technology: Blade Economics vs. Laser Precision

Blade systems controlled 46.7% of the dicing equipment market in 2024, their cost-per-wafer edge and mature service networks suiting high-volume logic and memory lines. However, the laser segment is expanding at a 6.6% CAGR as sub-50 µm wafers proliferate, requiring kerf-free singulation that conventional blades cannot guarantee. Panasonic’s APX300 plasma platform enables 20 µm streets on 300 mm wafers, underscoring the performance leap plasma and laser tools deliver. Hybrid lines that combine blade rough-cutting with laser finishing are also gaining traction, striking a balance between throughput and die strength.

The incremental cost of laser optics, rare-earth alignment components, and multi-kW power supplies still limits adoption in price-sensitive fabs. Yet where die-to-package vertical interconnect or brittle SiC substrates prevail, the higher upfront spend is offset by lower scrap and tighter design rules. Over the forecast horizon, sustained research and development in ultrafast pulse shaping and auto-focus optics is expected to enhance tool duty cycle, gradually narrowing the per-wafer cost gap.

Note: Segment shares of all individual segments available upon report purchase

By Wafer Size: 300 mm Dominance Yields to Larger Formats

The semiconductor industry is transitioning to larger wafer formats, with wafers exceeding 450 mm projected to grow at a 6.5% CAGR through 2030, challenging the 300 mm wafers, which held a 38.1% market share in 2024. Advanced packaging applications, particularly in panel-level packaging workflows, are driving demand for larger substrate-handling capabilities. DISCO Corporation’s DFD6370 supports workpieces up to 330 × 330 mm, addressing the gap between conventional wafer processing and emerging large-format requirements.

Smaller wafer sizes, including 200 mm and below, remain relevant in specialized applications such as MEMS devices and power semiconductors, where substrate costs and process optimization favor established formats. The 200 mm segment benefits from mature node expansion and automotive semiconductor demand, while 150 mm wafers serve niche applications in compound semiconductors and legacy device production. However, the economic advantages of larger wafers, including higher die yield per substrate and reduced per-unit processing costs, are driving format migration. SEMI’s World Fab Forecast identifies 79 high-probability facilities beginning operations through 2027, many incorporating mixed wafer-size capabilities. Equipment suppliers developing scalable handling systems for multiple wafer formats within single platforms are well-positioned for this evolving landscape.

By Application: Image-Sensor Dominance Meets Power-Device Momentum

CMOS imagers captured 30.9% of the dicing equipment market size in 2024, supported by stringent edge-quality tolerances for automotive ADAS, AR/VR headsets, and advanced multi-camera smartphones. Automotive sensor roadmaps toward stacked pixel architectures push dicing tolerance envelopes even tighter; contamination-controlled plasma cuts reduce debris that could scatter light onto active areas.

Power devices are the fastest riser, with a 7.1% CAGR through 2030, as EV inverters, high-voltage chargers, and solar inverters transition to SiC and GaN die. These wide-bandgap wafers require lower subsurface damage and are cut at slower feed rates, favoring laser or diamond-blade hybrid processes. Across MEMS microphones, RFID, and smart-card ICs, demand stays steady, with incremental design rule shrink driving minor equipment refresh cycles rather than wholesale tool replacement.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Foundries Lead While OSATs Accelerate

In 2024, foundries held a 32.2% market share, reflecting their significant role in the production of advanced logic and memory. This production requires advanced dicing capabilities for leading-edge nodes and complex device architectures. OSATs recorded the fastest growth among end-user segments, with an 7.2% CAGR, driven by demand for artificial-intelligence accelerators and advanced packaging. These trends are shifting value-added processing toward specialized assembly and testing providers. The foundry segment benefits from TSMC's USD 100 billion U.S. investment and Samsung's advanced-node development, sustaining demand for precision dicing equipment capable of handling sub-3 nm process requirements and gate-all-around transistor architectures. Taiwan's foundry concentration drives regional equipment demand, while China's domestic foundry expansion supports growth despite challenges from export controls.

OSAT growth reflects the industry's shift toward heterogeneous integration and chiplet architectures, requiring specialized assembly capabilities beyond traditional foundry operations. Integrated device manufacturers maintain a steady demand for dicing equipment to support internal production, while fabless companies influence equipment procurement through their foundry and OSAT partners. The shift toward specialized service providers creates opportunities for equipment suppliers offering turnkey solutions with integrated inspection and handling capabilities. Memory manufacturers, though concentrated, represent a high-volume segment, with DRAM and 3D NAND production requiring specialized dicing techniques for multi-layer device architectures and ultra-thin wafer processing.

Geography Analysis

The Asia-Pacific region retained a 42.90% share of the dicing equipment market in 2024, driven by its deep-seated manufacturing clusters across Taiwan, South Korea, Japan, and mainland China. Tokyo-backed subsidies totaling JPY 3.9 trillion (USD 0.026 trillion) underpin Japan’s resurgence, channeling orders to precision-motion vendors and automation integrators. Chinese OSATs accelerate plasma-dicing line installs to raise yields on locally designed AI accelerators, while Southeast Asian nations attract assembly spillover, spawning mid-tier blade-dicer demand.

North America’s CHIPS Act has unlocked more than USD 50 billion in incentives, transforming greenfield fabs in Arizona, Texas, and upstate New York into new procurement hubs starting in 2026. These sites prioritize fully automated blade and laser cells, equipped with predictive maintenance analytics, to offset skilled labor shortages.

Europe’s Chips Act funnels USD 47 billion into continental capacity, led by German and French projects focused on silicon-carbide power electronics for EV supply chains. Although smaller than Asian volumes, the stringent environmental standards in EU fabs accelerate uptake of closed-loop slurry and low-water-consumption plasma dicing systems, nudging regional ASPs upward.

Competitive Landscape

Incumbents such as DISCO Corporation and Tokyo Seimitsu maintain their market share through extensive blade-saw portfolios, global parts depots, and application labs that expedite recipe development. Panasonic targets the premium plasma market with the APX300, while Lumentum and Laser Photonics extend their ultrafast-laser competence into semiconductor dicing niches.

Product strategy now hinges on integrating vision inspection, die-pick handling, and AI-driven cut-path optimization into one tool chain. Early movers offering predictive spindle-wear analytics report double-digit service-revenue growth as fabs adopt usage-based maintenance contracts.

Regulatory compliance, notably ISO 11553 laser-safety certification, has become a procurement prerequisite in Europe and the United States, favoring suppliers with proven functional-safety engineering. Meanwhile, demand for SiC-ready lines sparks collaboration between dicer OEMs and consumable-blade manufacturers to co-develop diamond coatings that increase throughput without compromising edge integrity.

Dicing Equipment Industry Leaders

-

DISCO Corporation

-

Advanced Dicing Technologies Ltd.

-

Plasma-Therm LLC

-

Han’s Laser Technology Industry Group Co., Ltd.

-

Tokyo Seimitsu Co., Ltd. (ACCRETECH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Panasonic Connect rolled out its APX300 plasma dicer with multi-chamber options for 300 mm wafers, enabling ≤20 µm streets and particle-free cuts suited to advanced packaging.

- December 2024: DISCO Corporation introduced the DFD6370 automatic dicing saw for 330 mm × 330 mm panels, adding selectable height-sensing for precise half-cut control.

- December 2024: Laser Photonics unveiled the BlackStar laser wafer-dicing system after acquiring Control Micro Systems, eliminating water-jet cooling and improving die yield.

- October 2024: Infineon Technologies produced 20 µm-thick 300 mm power wafers, halving conventional thickness and reducing conduction losses by 15% for automotive-grade devices.

Global Dicing Equipment Market Report Scope

| Blade Dicing |

| Laser Ablation |

| Stealth Dicing |

| Plasma Dicing |

| ≤ 150 mm |

| 200 mm |

| 300 mm |

| ≥ 450 mm |

| Logic and Memory |

| MEMS Devices |

| Power Devices |

| CMOS Image Sensors |

| RFID / Smart Cards |

| Foundries |

| IDMs |

| OSATs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Dicing Technology | Blade Dicing | ||

| Laser Ablation | |||

| Stealth Dicing | |||

| Plasma Dicing | |||

| By Wafer Size | ≤ 150 mm | ||

| 200 mm | |||

| 300 mm | |||

| ≥ 450 mm | |||

| By Application | Logic and Memory | ||

| MEMS Devices | |||

| Power Devices | |||

| CMOS Image Sensors | |||

| RFID / Smart Cards | |||

| By End-User Industry | Foundries | ||

| IDMs | |||

| OSATs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the dicing equipment market in 2030?

The dicing equipment market is forecast to reach USD 1.13 billion by 2030, growing at a 6.43% CAGR.

Why is laser dicing gaining share against blade systems?

Increased use of ultra-thin wafers and 3D packages requires kerf-free singulation that laser or plasma tools can deliver without edge damage.

How will EV adoption influence equipment demand?

Silicon-carbide and gallium-nitride power devices for EV inverters and chargers are driving an 7.1% CAGR for power-device dicing lines through 2030.

Which region is poised for the fastest capacity additions outside Asia-Pacific?

North America, backed by CHIPS Act incentives, will see new fabs come online from 2026 onward, spurring fresh tool orders.

What environmental regulations affect dicing operations?

Emerging PFAS and slurry-disposal rules require closed-loop coolant recycling and advanced filtration, raising compliance costs but reducing environmental footprint.

Page last updated on: