Market Size of Diabetes Care Drugs Industry

| Study Period | 2019 - 2029 |

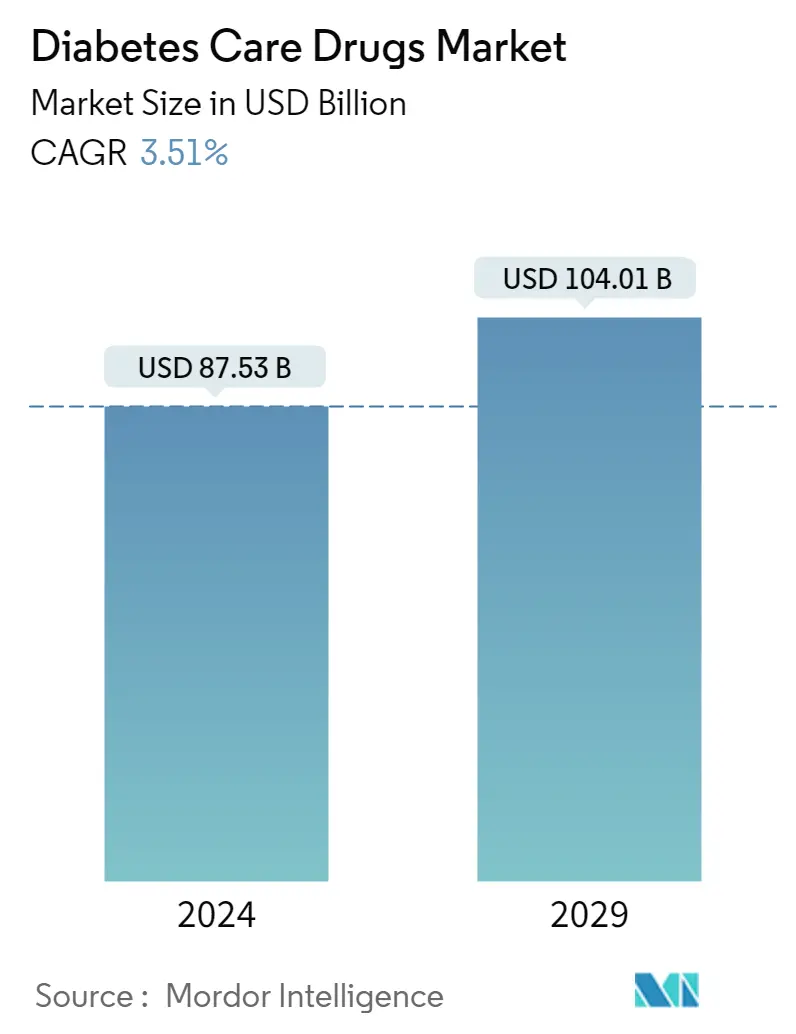

| Market Size (2024) | USD 87.53 Billion |

| Market Size (2029) | USD 104.01 Billion |

| CAGR (2024 - 2029) | 3.51 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Diabetes Drug Market Analysis

The Diabetes Care Drugs Market size is estimated at USD 87.53 billion in 2024, and is expected to reach USD 104.01 billion by 2029, growing at a CAGR of 3.51% during the forecast period (2024-2029).

The diabetes care drugs market experienced a significant impact due to the COVID-19 pandemic. This global health crisis shed light on the potential for advancements in diabetes care through virtual consultations between healthcare professionals and individuals with diabetes, as well as the utilization of diabetes technology. The management of the crisis led to an unprecedented interest in remote care from both patients and providers, resulting in the removal of various regulatory barriers that had long been in place. As an example, the US Food and Drug Administration permitted the use of personal blood glucose meters and continuous glucose monitoring devices in hospitals during the pandemic. The high prevalence of diabetes among individuals hospitalized with COVID-19 infection, coupled with the understanding that better glycemic control could enhance outcomes and reduce hospital stays for patients with SARS-CoV-2, emphasized the significance of diabetes care devices.

Diabetes is a chronic, life-threatening disease with no known cure. As per the World Health Organization, there are over 400 million people with diabetes across the world, and its treatment constitutes around 12% of the total healthcare expenditure on a global scale. It has emerged as a global epidemic and afflicted millions worldwide.

The significant growth in the market can be attributed to factors such as the rising prevalence of diabetes and the increasing number of programs initiated by various health organizations related to health awareness. Currently, about 10% of all diabetes cases are Type-1, and the remaining are Type-2.

As of 2021, North America accounted for a major share of the market, followed by Asia-Pacific. The increase in the number of diabetes patients is primarily due to increasing obesity among people caused by unhealthy diets and sedentary lifestyles. The market in Asia-Pacific is mainly driven by increasing demand for diabetes drugs from China and India. Currently, China has over 129 million diabetes patients, while the number of diabetes patients in India is expected to reach 82 million by 2027.

Based on drugs, the insulin segment holds a significant share of the market. Over 100 million people around the world need insulin, including all the people who have Type-1 diabetes and between 10% and 25% of people with Type-2 diabetes. Production of insulin is very complex, and there are very few companies in the market that manufacture insulin. Due to this, there is high competition between these manufacturers, who always strive to meet the patient's needs to supply the best-quality insulin.

Diabetes Drug Industry Segmentation

Diabetes or diabetes mellitus describes a group of metabolic disorders characterized by a high blood sugar level in a person. With diabetes, the body either does not produce enough insulin the body's cells do not respond properly to insulin, or both.

The diabetes care drugs market is segmented by drugs into insulin (basal or long-acting, bolus or fast-acting, traditional human insulin drugs, and insulin biosimilars), oral anti-diabetic drugs (alpha-glucosidase inhibitors, DPP-4 inhibitors, and SGLT-2 inhibitors), non-insulin injectable drugs (GLP-1 receptor agonists, and amylin analog), and combination drugs (combination insulin, oral combination). by Route of Administration (Oral, Intravenous, Subcutaneous), by Distribution Channel (Online, and Offline), and by Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and Latin America). The report offers the value (in USD) and Volume (in ml) for the above segments.

| By Drugs | ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

|

| By Route of Administration | |

| Oral | |

| Subcutaneous | |

| Intravenous |

| By Distribution Channel | |

| Online | |

| Offline |

| Geography | |||||||||||||

| |||||||||||||

| |||||||||||||

| |||||||||||||

| |||||||||||||

|

Diabetes Care Drugs Market Size Summary

The diabetes drug market is poised for steady growth, driven by the increasing prevalence of diabetes globally and the rising demand for effective treatment options. The market has been significantly influenced by the COVID-19 pandemic, which highlighted the importance of diabetes care and accelerated the adoption of remote healthcare solutions. This shift has led to the removal of regulatory barriers, facilitating the use of advanced diabetes management technologies. The market is characterized by a high demand for insulin, particularly among Type-1 diabetes patients, and is supported by ongoing advancements in insulin delivery systems and drug development. North America, especially the United States, holds a dominant position in the market due to its high diabetic population and the introduction of new drugs. The region's market growth is further bolstered by increased awareness and initiatives aimed at diabetes care.

The competitive landscape of the diabetes drug market is moderately fragmented, with a mix of significant and generic players. Major pharmaceutical companies like Novo Nordisk, Sanofi, and AstraZeneca lead the market, particularly in the insulin and SGLT-2 drug segments. The market for oral diabetes medications, such as Sulfonylureas and Meglitinides, is more populated with generic players, contributing to high competition. Companies are actively seeking to expand their market share by developing new drugs and entering emerging markets with high demand. Recent strategic moves, such as Sanofi's presentation of promising Phase 3 trial results and Novo Nordisk's acquisition of Inversago Pharma, underscore the dynamic nature of the market and the ongoing efforts to address the global diabetes epidemic.

Diabetes Care Drugs Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products and Services

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Drugs

-

2.1.1 Oral Anti-diabetic drugs

-

2.1.1.1 Biguanides

-

2.1.1.1.1 Metformin

-

-

2.1.1.2 Alpha-glucosidase Inhibitors

-

2.1.1.3 Dopamine -D2 Receptor Agonist

-

2.1.1.3.1 Cycloset (Bromocriptin)

-

-

2.1.1.4 Sodium-glucose Cotransport -2 (SGLT-2) Inhibitors

-

2.1.1.4.1 Invokana (Canagliflozin)

-

2.1.1.4.2 Jardiance (Empagliflozin)

-

2.1.1.4.3 Farxiga/Forxiga (Dapagliflozin)

-

2.1.1.4.4 Suglat (Ipragliflozin)

-

-

2.1.1.5 Dipeptidyl Peptidase-4 (DPP-4) Inhibitors

-

2.1.1.5.1 Januvia (Sitagliptin)

-

2.1.1.5.2 Onglyza (Saxagliptin)

-

2.1.1.5.3 Tradjenta (Linagliptin)

-

2.1.1.5.4 Vipidia/Nesina (Alogliptin)

-

2.1.1.5.5 Galvus (Vildagliptin)

-

-

2.1.1.6 Sulfonylureas

-

2.1.1.7 Meglitinides

-

-

2.1.2 Insulin

-

2.1.2.1 Basal or Long-acting Insulin

-

2.1.2.1.1 Lantus (Insulin Glargine)

-

2.1.2.1.2 Levemir (Insulin Detemir)

-

2.1.2.1.3 Toujeo (Insulin Glargine)

-

2.1.2.1.4 Tresiba (Insulin Degludec)

-

2.1.2.1.5 Basaglar (Insulin Glargine)

-

-

2.1.2.2 Bolus or Fast-acting Insulin

-

2.1.2.2.1 NovoRapid/Novolog (Insulin Aspart)

-

2.1.2.2.2 Humalog (Insulin Lispro)

-

2.1.2.2.3 Apidra (Insulin Glulisine)

-

-

2.1.2.3 Traditional Human Insulin

-

2.1.2.3.1 Novolin/Actrapid/Insulatard

-

2.1.2.3.2 Humulin

-

2.1.2.3.3 Insuman

-

-

2.1.2.4 Biosimilar Insulin

-

2.1.2.4.1 Insulin Glargine Biosimilars

-

2.1.2.4.2 Human Insulin Biosimilars

-

-

-

2.1.3 Non-insulin Injectable Drug

-

2.1.3.1 GLP-1 Receptor Agonists

-

2.1.3.1.1 Victoza (Liraglutide)

-

2.1.3.1.2 Byetta (Exenatide)

-

2.1.3.1.3 Bydureon (Exenatide)

-

2.1.3.1.4 Trulicity (Dulaglutide)

-

2.1.3.1.5 Lyxumia (Lixisenatide)

-

-

2.1.3.2 Amylin Analogue

-

2.1.3.2.1 Symlin (Pramlintide)

-

-

-

2.1.4 Combination Drug

-

2.1.4.1 Combination Insulin

-

2.1.4.1.1 NovoMix (Biphasic Insulin Aspart)

-

2.1.4.1.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

-

2.1.4.1.3 Xultophy (Insulin Degludec and Liraglutide)

-

-

2.1.4.2 Oral Combination

-

2.1.4.2.1 Janumet (Sitagliptin and Metformin HCl)

-

-

-

-

2.2 By Route of Administration

-

2.2.1 Oral

-

2.2.2 Subcutaneous

-

2.2.3 Intravenous

-

-

2.3 By Distribution Channel

-

2.3.1 Online

-

2.3.2 Offline

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

2.4.1.3 Rest of North America

-

-

2.4.2 Europe

-

2.4.2.1 France

-

2.4.2.2 Germany

-

2.4.2.3 Italy

-

2.4.2.4 Spain

-

2.4.2.5 United Kingdom

-

2.4.2.6 Russia

-

2.4.2.7 Rest of Europe

-

-

2.4.3 Latin America

-

2.4.3.1 Mexico

-

2.4.3.2 Brazil

-

2.4.3.3 Rest of Latin America

-

-

2.4.4 Asia-Pacific

-

2.4.4.1 Japan

-

2.4.4.2 South Korea

-

2.4.4.3 China

-

2.4.4.4 India

-

2.4.4.5 Australia

-

2.4.4.6 Vietnam

-

2.4.4.7 Malaysia

-

2.4.4.8 Indonesia

-

2.4.4.9 Philippines

-

2.4.4.10 Thailand

-

2.4.4.11 Rest of Asia-Pacific

-

-

2.4.5 Middle-East and Africa

-

2.4.5.1 Saudi Arabia

-

2.4.5.2 Iran

-

2.4.5.3 Egypt

-

2.4.5.4 Oman

-

2.4.5.5 South Africa

-

2.4.5.6 Rest of Middle-East and Africa

-

-

-

Diabetes Care Drugs Market Size FAQs

How big is the Diabetes Care Drugs Market?

The Diabetes Care Drugs Market size is expected to reach USD 87.53 billion in 2024 and grow at a CAGR of 3.51% to reach USD 104.01 billion by 2029.

What is the current Diabetes Care Drugs Market size?

In 2024, the Diabetes Care Drugs Market size is expected to reach USD 87.53 billion.