Desktop 3D Printing Market Size

| Study Period | 2019 - 2029 |

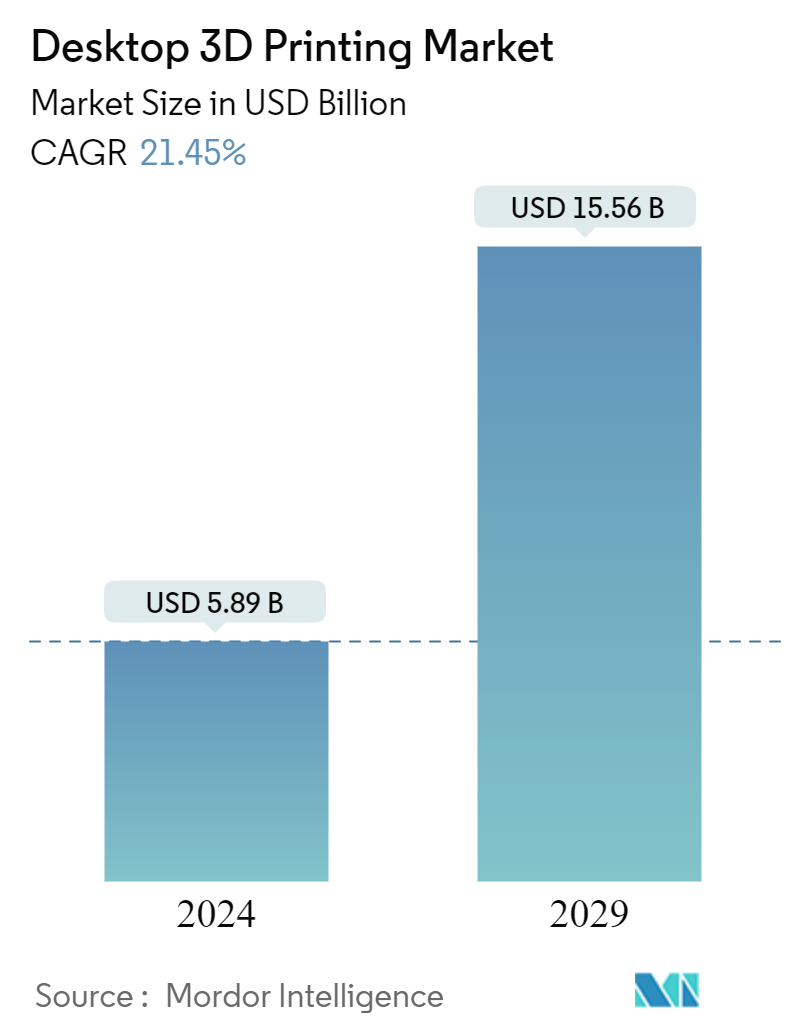

| Market Size (2024) | USD 5.89 Billion |

| Market Size (2029) | USD 15.56 Billion |

| CAGR (2024 - 2029) | 21.45 % |

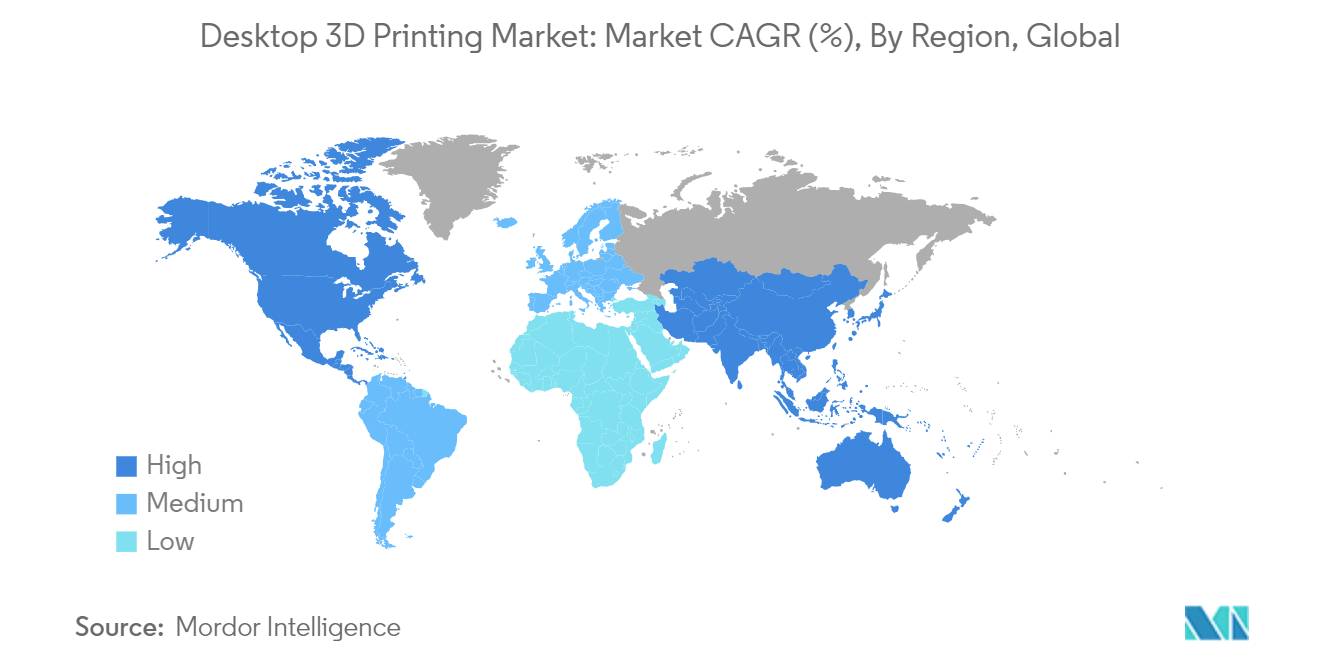

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

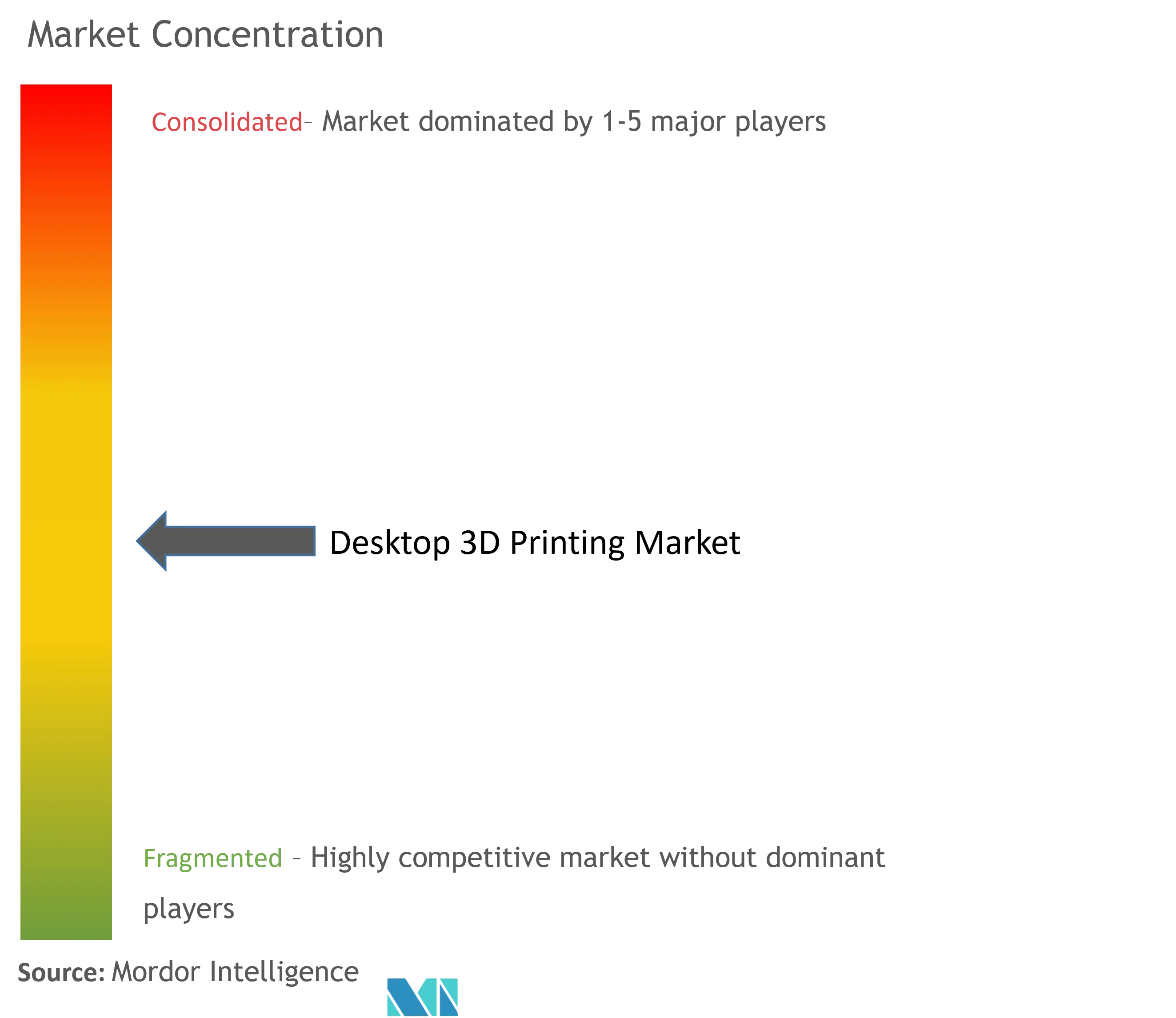

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Desktop 3D Printing Market Analysis

The Desktop 3D Printing Market size is estimated at USD 5.89 billion in 2024, and is expected to reach USD 15.56 billion by 2029, growing at a CAGR of 21.45% during the forecast period (2024-2029).

- Advancements in print quality and resolution have revolutionized the desktop 3D printing market. Printers deliver heightened precision and intricate details, facilitating the creation of complex designs that were challenging to produce. This superior quality resonates with industries like aerospace, automotive, and consumer goods, where precision is paramount. For example, in the automotive industry, manufacturers can produce exact prototypes and end-use components that adhere to rigorous performance benchmarks, minimizing errors and elevating product quality.

- The growing array of materials for 3D printing has further broadened the market's horizons. Breakthroughs in materials science have introduced a spectrum of printable materials, from metals and ceramics to composites, alongside conventional plastics. This expanded palette empowers industries to tap into novel applications. In architecture, for instance, 3D printing can craft intricate structural elements, while in education, varied materials can enrich teaching tools and models. As the material landscape evolves, industries are poised to harness 3D printing's full potential, fueling demand.

- In the evolving landscape of 3D printing, integration with technologies like artificial intelligence (AI) and the Internet of Things (IoT) is rising. These smart features not only optimize printing processes but also monitor performance and predict maintenance needs, bolstering the efficiency and reliability of desktop 3D printers. For instance, AI's capability to analyze print data allows for real-time adjustments and suggestions, significantly minimizing errors and waste. As these technologies advance, they render desktop 3D printing increasingly appealing to businesses aiming to refine their manufacturing processes.

- The high costs associated with premium materials often motivate companies to seek more cost-effective alternatives. This situation encourages manufacturers to invest in research and development to produce lower-cost materials that meet quality standards. As these alternative materials become available, they can help reduce the overall cost of 3D printing, making the technology more accessible to small businesses, educational institutions, and hobbyists.

- Geopolitical tensions between countries like Russia, the US-China trade war, etc., can create uncertainty, leading to fluctuations in raw material prices. When countries impose tariffs or import restrictions, the costs of materials for desktop 3D printing can surge. This uptick in costs impacts the market's overall pricing structure, complicating efforts for manufacturers to maintain competitive pricing. As a result, businesses might be reluctant to invest in 3D printing technologies or broaden their operations, hindering market growth.

Desktop 3D Printing Market Trends

Healthcare Segment is Expected to Grow Significantly

- The desktop 3D printing market is experiencing heightened demand from the healthcare industry, driven by evolving needs and the distinct advantages of 3D printing technology. A standout benefit is the creation of customized medical devices. Traditional manufacturing often relies on standardized products, which may not cater perfectly to every patient.

- Further, desktop 3D printing's customization capabilities empower manufacturers to craft implants that align precisely with individual patients' anatomical requirements. Such tailored solutions enhance the fit and function of the implants and boost patient satisfaction and outcomes.

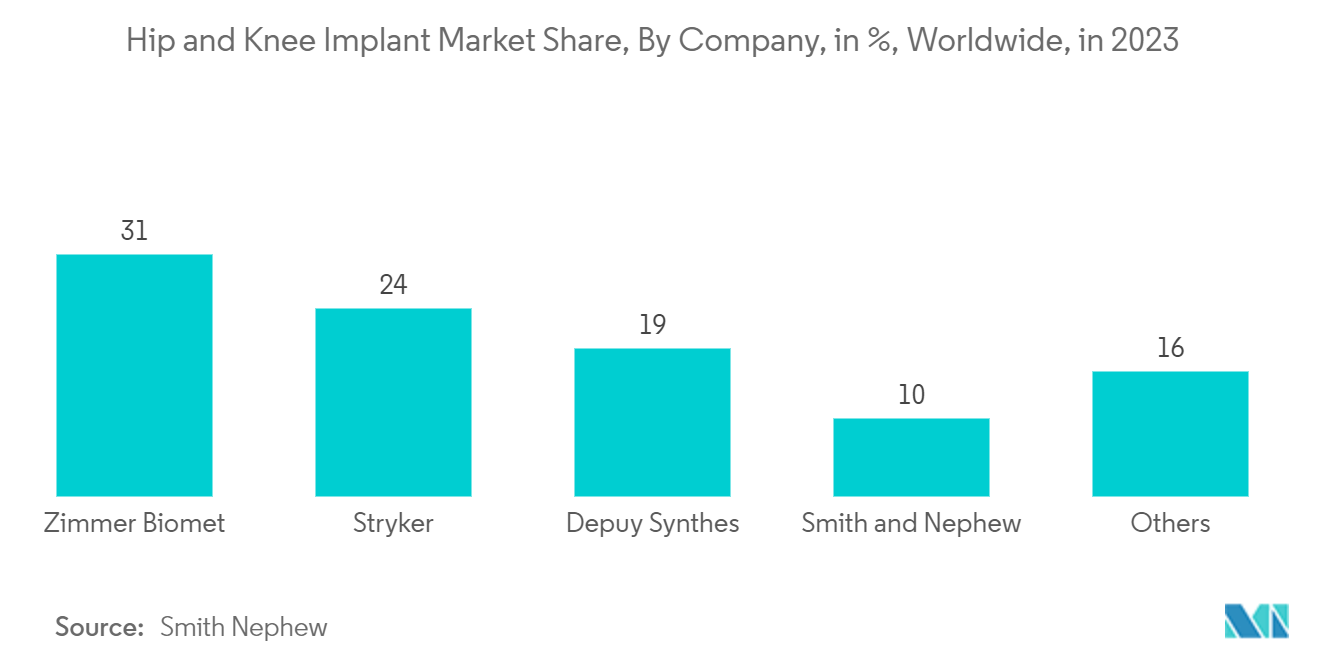

- Smith & Nephew's annual report in 2023 revealed a growing trend in the hip and knee implant market, which currently commands a ten per cent share of the global market. With healthcare providers increasingly pursuing these effective, personalized solutions, the demand for customized implants is set to surge, consequently broadening the market share for companies harnessing the power of 3D printing.

- Another pivotal factor fueling this demand is rapid prototyping. The swift design, printing, and testing of surgical instruments and implant prototypes in healthcare can drastically reduce development timelines. This skill enables medical professionals to refine designs based on real-world feedback, resulting in superior products that align closely with clinical needs.

- Further, cost efficiency is also a significant driver. Desktop 3D printers can substantially lower manufacturing costs when juxtaposed with traditional methods. Factors like reduced material waste, diminished labor costs, and less reliance on costly tooling culminate in a more budget-friendly production process. This advantage is especially pronounced for smaller healthcare providers and startups, which, despite tighter budgets, still demand top-tier medical devices.

- 3D printing technology is revolutionizing education and training in the healthcare sector. Medical students and professionals leverage 3D-printed models to hone their surgical techniques and other procedures. These lifelike models enhance hands-on learning, ensuring better readiness for actual clinical scenarios. Such training is especially vital in surgical disciplines, where precision and a deep understanding of anatomy are paramount.

North America is Expected to Hold Significant Market Share

- North America's healthcare infrastructure is robust and quick to adopt technological advancements. Hospitals, clinics, and regional research institutions are increasingly utilizing 3D printing for custom implants, surgical planning models, and educational tools. The dense network of healthcare facilities accelerates the integration of these innovative technologies, spurring demand.

- North America hosts a plethora of leading 3D printing firms and research institutions, such as Stratasys, 3D Systems, Inc., Formlabs, etc. This concentration fosters innovation and collaboration and propels the development of cutting-edge 3D printing technologies and materials. With key players firmly established in the market desktop 3D printers are swiftly adopted in several industries.

- Substantial investments in research and development are a hallmark of the region. Both government initiatives and private-sector funding are pivotal in advancing 3D printing technology across several industries. For instance, in March 2024, GE Aerospace announced its plan to invest USD 650 million in its manufacturing facilities and supply chain. Over USD 150 million of this investment will be directed towards facilities utilizing additive manufacturing equipment. This strategic move aims to bolster production capabilities and enhance the quality of support offered to both commercial and defense clients. Such investments bolster the capabilities of desktop 3D printing, making them increasingly attractive to defense providers as desktop 3D printers play a crucial role in prototyping and manufacturing end-use components for military equipment undergoing testing.

- Moreover, North America's regulatory landscape is becoming more accommodating for 3D-printed devices, especially 3D-printed medical devices. For instance, the FDA oversees medical products created through 3D medical printing, operating under the Federal Food, Drug, and Cosmetic Act (FD&C Act).

- This authority has been updated by both the Medical Device User Fee and Modernization Act (MDUFA) and the 21st Century Cures Act (Cures Act). 3D-printed medical devices fall into three regulatory categories: Class I, Class II, and Class III, determined by their associated risk levels. Class I devices, deemed the least risky, encompass items such as surgical instruments and handpieces. Class II devices carry a moderate risk, including blood pressure monitors and oxygen masks. Class III devices, classified as the most risky, comprise implantable devices and those essential for life support.

- Regulatory bodies are crafting guidelines and approval processes that streamline the integration of 3D printing. This proactive stance encourages manufacturers to delve into 3D-printed products and amplifies demand across the region.

Desktop 3D Printing Industry Overview

The desktop 3D printing market exhibits a semi-consolidated structure, featuring a mix of global and regional players across diverse segments. While a handful of large multinational corporations dominate specific high-value segments, a multitude of regional and niche players enrich the competitive landscape, underscoring the market's diversity. This fragmentation stems from the myriad applications of desktop 3D printers, creating an ecosystem where both large and small enterprises can coexist and flourish.

Prominent players in the desktop 3D printing arena encompass Stratasys, 3D Systems, Inc., EOS GmbH, ELEGOO, and Markforged. These industry leaders boast robust brand recognition and a vast global footprint, empowering them to secure a substantial market share. Their competitive edge is anchored in relentless innovation, a diverse product lineup, and a formidable distribution network.

For companies eyeing success in desktop 3D printing, prioritizing innovation is paramount. Engaging in strategic acquisitions and forging partnerships is essential to not only retain a competitive edge but also broaden market presence. Furthermore, firms that channel investments into emerging markets and tailor their offerings to meet regional demands stand poised to carve out a significant advantage in this fragmented landscape.

Desktop 3D Printing Market Leaders

-

Stratasys

-

3D Systems, Inc.

-

EOS GmbH

-

ELEGOO

-

Markforged

*Disclaimer: Major Players sorted in no particular order

Desktop 3D Printing Market News

- June 2024: At RAPID + TCT 2024, ELEGOO unveiled three desktop 3D printers, its inaugural CoreXY flagship 3D printer, the Centauri Carbon. This debut, coupled with the introduction of the latest Mars series additions, the Mars 5 and Mars 5 Ultra, signifies ELEGOO's first instance of launching multiple printers at the event. The Centauri Carbon boasts cutting-edge features such as smart AI camera capabilities and a robust aluminium die-cast construction. The Centauri Carbon's CoreXY technology utilizes a distinctive belt system, ensuring swift and precise movements on the X and Y axes. This precision makes it perfect for various applications, from intricate prototypes and artistic models to educational projects and products for small businesses.

- April 2024: Anycubic rolled out its innovative product matrix strategy, debuting two flagship offerings: the Kobra 3 combo, a multi-colour filament material extrusion printer, and the Photon Mono M7 Pro, an intellectually-assisted printer boasting 14K precision. Building on these launches, Anycubic is set to introduce a suite of products tailored to diverse printing needs, aiming squarely at competing with Bambu Labs in the desktop 3D printer arena. This move dovetails with the launch of Makeronline, Anycubic’s creative community platform, designed to elevate users' creative pursuits in 3D printing.

Desktop 3D Printing Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Advancements in 3D Printing Technologies

5.1.2 Increased Use in Medical Dental Fields

5.2 Market Restraint

5.2.1 Limited Material Choices with High Material Costs

6. MARKET SEGMENTATION

6.1 By Technology

6.1.1 Stereolithography (SLA)

6.1.2 Selective Laser Sintering (SLS)

6.1.3 Fused Deposition Modeling (FDM)

6.1.4 Digital Light Process (DLP)

6.1.5 Multi Jet Fusion (MJF)

6.1.6 PolyJet

6.1.7 Direct Metal Laser Sintering (DMLS)

6.1.8 Electron Beam Melting (EBM)

6.2 By Application

6.2.1 Prototyping

6.2.2 Tooling

6.2.3 Replacement Parts

6.3 By End-User Industry

6.3.1 Education

6.3.2 Healthcare

6.3.3 Automotive

6.3.4 Fashion and Jewellery

6.3.5 Entertainment

6.3.6 Architecture

6.4 By Geography***

6.4.1 North America

6.4.2 Europe

6.4.3 Asia

6.4.4 Australia and New Zealand

6.4.5 Latin America

6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Stratasys

7.1.2 3D Systems, Inc.

7.1.3 EOS GmbH

7.1.4 Formlabs

7.1.5 Markforged

7.1.6 Tinkerine Studios Ltd.

7.1.7 WOL 3D

7.1.8 Tiertime Technology Co. Ltd.

7.1.9 Protolabs

7.1.10 Zortrax

7.1.11 SHINING 3D

7.1.12 Flashforge 3D Technology Co., Ltd

7.1.13 Desktop Metal

7.1.14 ELEGOO

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Desktop 3D Printing Industry Segmentation

Desktop 3D printers, typically employed for smaller items, find applications across various fields, including industrial design, education, animation, archaeology, and lighting. These printers have made inroads into the dental medical industry and are pivotal in the dental digital production process. Integrated into the digital medical model, they facilitate the printing of essential dental products. The study monitors revenues generated from global sales of desktop 3D printers. Additionally, it examines the geopolitical and macroeconomic factors influencing the market.

Desktop 3D printing market is segmented by technology (stereolithography (SLA), selective laser sintering (SLS), fuse deposition modelling (FDM), digital light processing (DLP), multi-jet fusion (MJF), polyjet, direct metal laser sintering (DMLS), and electron beam melting (EBM)), application (prototyping, tooling, and replacement parts), end-user industry (education, healthcare, automotive, fashion and jewellery, entertainment, and architecture), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Technology | |

| Stereolithography (SLA) | |

| Selective Laser Sintering (SLS) | |

| Fused Deposition Modeling (FDM) | |

| Digital Light Process (DLP) | |

| Multi Jet Fusion (MJF) | |

| PolyJet | |

| Direct Metal Laser Sintering (DMLS) | |

| Electron Beam Melting (EBM) |

| By Application | |

| Prototyping | |

| Tooling | |

| Replacement Parts |

| By End-User Industry | |

| Education | |

| Healthcare | |

| Automotive | |

| Fashion and Jewellery | |

| Entertainment | |

| Architecture |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Desktop 3D Printing Market Research FAQs

How big is the Desktop 3D Printing Market?

The Desktop 3D Printing Market size is expected to reach USD 5.89 billion in 2024 and grow at a CAGR of 21.45% to reach USD 15.56 billion by 2029.

What is the current Desktop 3D Printing Market size?

In 2024, the Desktop 3D Printing Market size is expected to reach USD 5.89 billion.

Who are the key players in Desktop 3D Printing Market?

Stratasys, 3D Systems, Inc., EOS GmbH, ELEGOO and Markforged are the major companies operating in the Desktop 3D Printing Market.

Which is the fastest growing region in Desktop 3D Printing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Desktop 3D Printing Market?

In 2024, the North America accounts for the largest market share in Desktop 3D Printing Market.

What years does this Desktop 3D Printing Market cover, and what was the market size in 2023?

In 2023, the Desktop 3D Printing Market size was estimated at USD 4.63 billion. The report covers the Desktop 3D Printing Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Desktop 3D Printing Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Desktop 3D Printing Industry Report

Statistics for the 2024 Desktop 3D Printing market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Desktop 3D Printing analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.