Distributed Denial Of Service (DDoS) Protection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

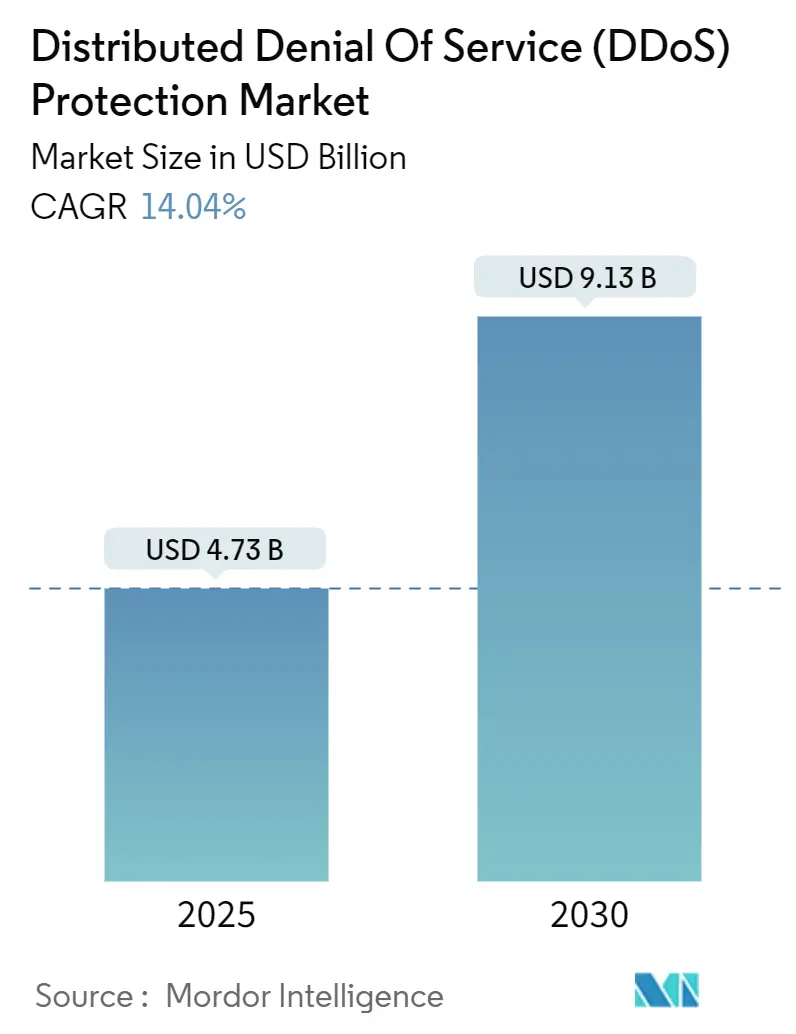

| Market Size (2025) | USD 4.73 Billion |

| Market Size (2030) | USD 9.13 Billion |

| Growth Rate (2025 - 2030) | 14.04% CAGR |

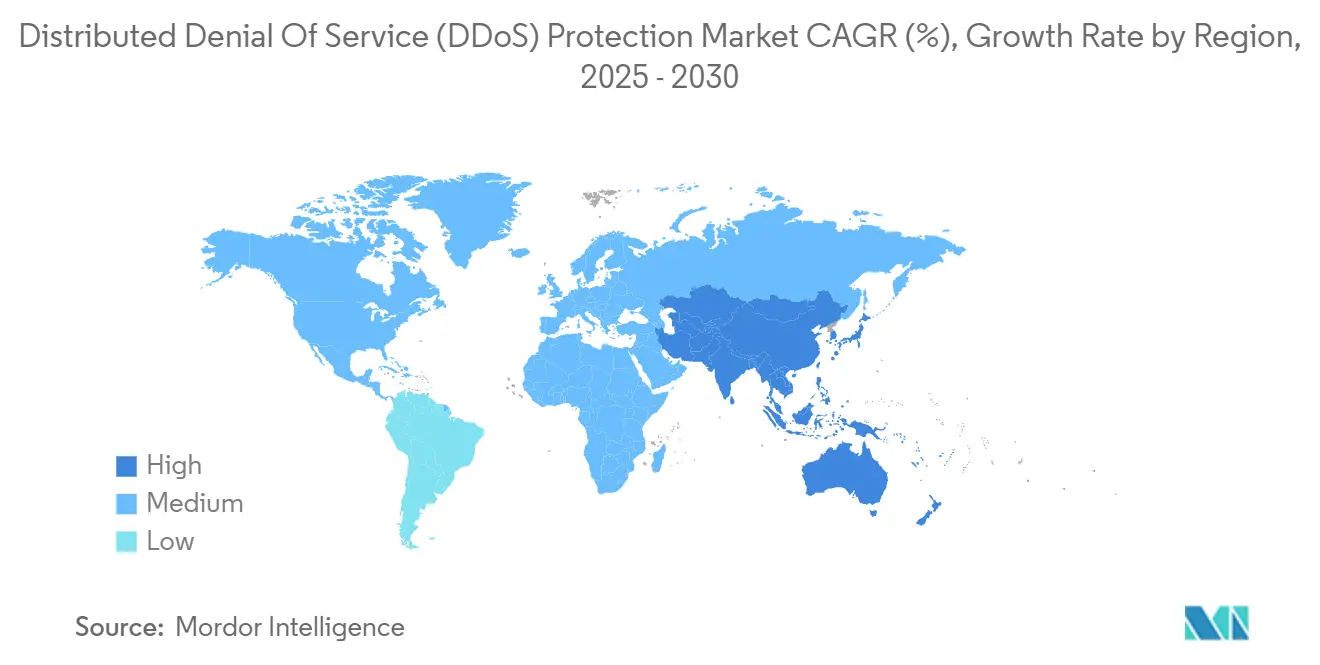

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Distributed Denial Of Service (DDoS) Protection Market Analysis by Mordor Intelligence

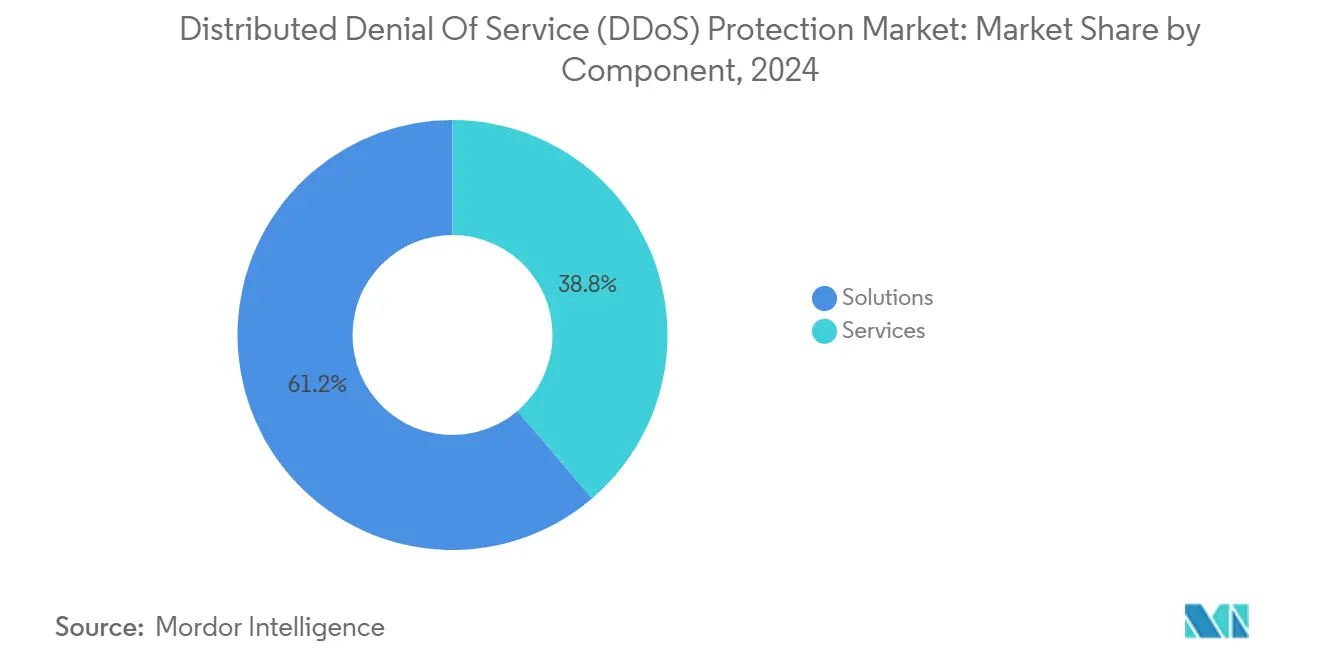

The DDoS protection market size stood at USD 4.73 billion in 2025 and is projected to reach USD 9.13 billion in 2030, reflecting a robust 14.04% CAGR. This expansion is fueled by the mounting frequency of multi-vector, terabit-scale incidents, strengthened regulatory mandates, and the widespread embrace of hybrid and cloud-based mitigation models. Solution-centric offerings maintained dominance with 61.23% share in 2024, underscoring enterprise demand for integrated, programmable defenses. Cloud-first deployments accounted for nearly half the addressable opportunity, yet hybrid architectures are gaining ground as organizations balance latency, control, and compliance. Regional dynamics remain pivotal: North America led with 39.34% revenue share in 2024, while Asia Pacific is advancing at a 14.89% CAGR, driven by rapid 5G rollouts and surging IoT adoption.

Key Report Takeaways

- By component, solutions captured 61.23% of the DDoS protection market share in 2024, whereas advanced bot mitigation is forecast to grow at 15.23% CAGR to 2030.

- By deployment mode, cloud-based offerings held 49.35% of the DDoS protection market size in 2024, while hybrid solutions are expanding at a 15.67% CAGR through 2030.

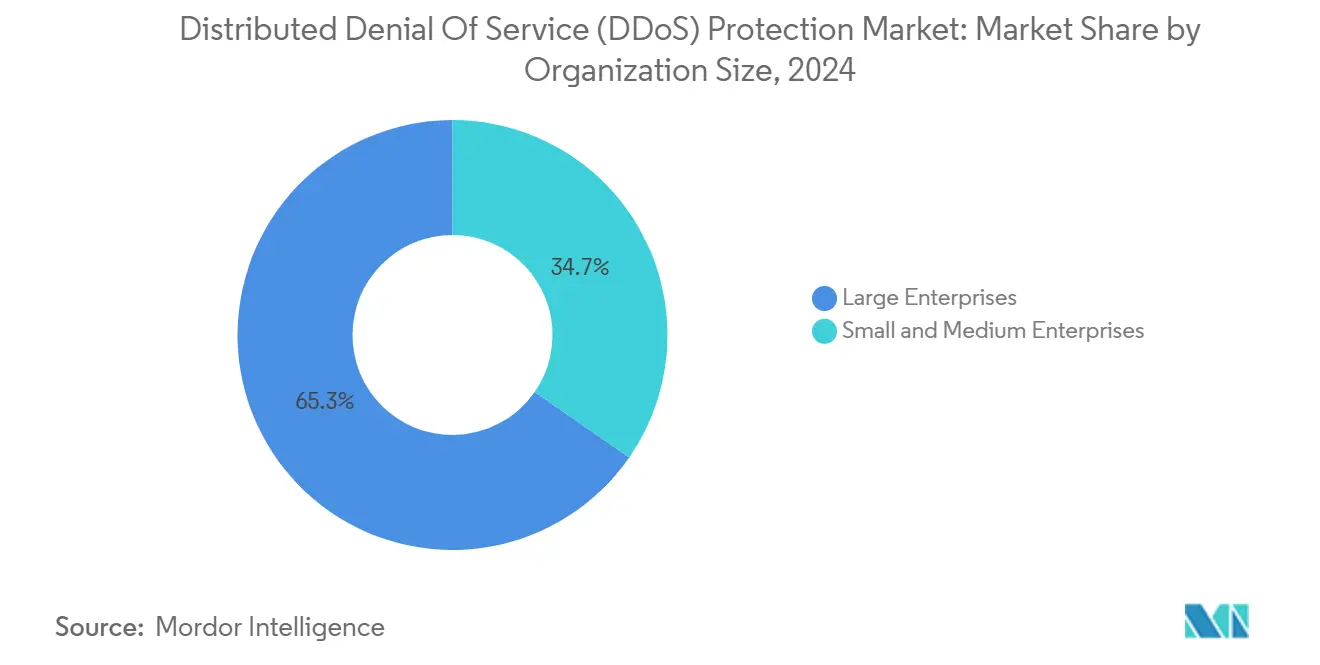

- By organization size, large enterprises controlled 34.56% of revenue in 2024, yet SMEs are set to post the fastest 15.78% CAGR across the forecast horizon.

- By end-user industry, IT and telecommunications led with 35.50% share in 2024; healthcare and life sciences is on track for a 14.67% CAGR to 2030.

- By geography, North America retained 39.34% share in 2024; Asia Pacific is the fastest-growing region at 14.89% CAGR.

Global Distributed Denial Of Service (DDoS) Protection Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating frequency of multi-vector, terabit-scale attacks | +3.8% | Global | Short term (≤ 2 years) |

| Rapid migration to cloud and hybrid mitigation models | +2.7% | North America, APAC, Europe | Medium term (2-4 years) |

| Expansion of IoT-, 5G- and edge-connected devices | +2.1% | APAC, North America, EMEA | Long term (≥ 4 years) |

| AI-powered “DDoS-as-a-Service” marketplaces lowering entry barriers | +1.6% | Global, with APAC and EMEA hotspots | Medium term (2-4 years) |

| Critical-infrastructure regulations mandating resiliency (e.g., NIS2, CISA) | +1.2% | EU, US, selected APAC | Short-Medium term |

| Adoption of programmable SDN-based scrubbing at the network edge | +0.8% | North America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating frequency of multi-vector attacks

A record 6.3 Tbps event in 2025 highlighted the jump from volumetric floods to blended protocol and application-layer campaigns, overwhelming legacy rule-based appliances and escalating procurement of adaptive, AI-driven platforms. Communication service providers and financial institutions remain high-value targets, and global regulators now require demonstrated resilience for critical infrastructure operators.[1]Cybersecurity & Infrastructure Security Agency, “2024 Year in Review,” cisa.gov

Rapid migration to cloud and hybrid mitigation models

Elastic, always-on cloud scrubbing has become indispensable as short-burst attacks spike; however, latency-sensitive workloads keep on-premises defenses relevant, accelerating hybrid demand.[2]Akamai, “A Retrospective on DDoS Trends in 2023,” akamai.com Partnerships between hyperscale clouds and security specialists are bridging skills gaps for SMEs while meeting emerging compliance obligations.

Expansion of IoT-, 5G-, and edge-connected devices

The proliferation of resource-constrained endpoints is fueling botnet scale, compelling investment in decentralized, SDN-based edge filtering and federated anomaly detection. Regulatory efforts now extend to device-level hardening and network segmentation, particularly across APAC’s fast-digitizing economies.

AI-powered “DDoS-as-a-Service” marketplaces lowering entry barriers

Automation and pay-per-hour attack kits have democratized threat execution, enabling non-technical actors to orchestrate short-burst “carpet-bombing” campaigns that evade threshold-based detection. Vendors are countering with behavior analytics, global threat-intel sharing, and zero-touch orchestration to reduce operator burden.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO of on-prem appliances for SMEs | -2.6% | Global, especially APAC/EU | Short term (≤ 2 years) |

| Shortage of skilled cyber-security professionals | -1.8% | Global, with APAC and EMEA | Medium term (2-4 years) |

| Rising share of encrypted attack traffic limiting visibility | -1.3% | North America, Europe | Medium term (2-4 years) |

| Risk of false-positive mitigation causing downtime | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High TCO of on-prem appliances for SMEs

Capex-heavy hardware plus ongoing signature updates remain prohibitive for smaller enterprises, steering demand toward subscription-based cloud scrubbing paired with managed SOC services.[3]Radware, “Anti-DDoS: Techniques & Key Considerations,” radware.com

Shortage of skilled cybersecurity professionals

Global vacancy rates in network security roles exceed 3.4 million positions, amplifying interest in automated, policy-guided defenses that alleviate operational workload and satisfy audit requirements.[4]Microsoft, “Microsoft Denial-of-Service Defense Strategy,” microsoft.com

Segment Analysis

By Component: Solutions Lead, Advanced Bot Mitigation Accelerates

Solutions commanded 61.23% revenue in 2024 as enterprises sought unified, programmable defenses capable of spanning L3/4 volumetric floods and L7 application abuses. Within this umbrella, network-layer protection retained the largest slice, yet advanced bot mitigation is forecast to rise at a 15.23% CAGR, driven by AI-enabled bots that mimic legitimate user behavior. Vendors are embedding machine-learning classifiers, device fingerprinting, and real-time challenge mechanisms to blunt credential-stuffing and inventory hoarding. Services—managed and professional—continue to gain relevance as organizations consolidate suppliers for compliance reporting and 24×7 monitoring. The interplay of solutions and services underscores a shift toward outcome-based contracting across the DDoS protection market.

Growing adoption of hybrid topologies demands orchestration between on-premises hardware, cloud scrubbing centers, and containerized network functions. As offerings converge, differentiation pivots on API-centric integration, attack-forensics depth, and zero-trust alignment. Solution vendors that blend behavioral analytics with actionable intelligence are positioned to capitalize on rising regulatory pressure for demonstrable resiliency across critical sectors.

By Deployment Mode: Cloud Dominates, Hybrid Grows Fastest

Cloud-based defenses captured 49.35% of the DDoS protection market size in 2024, offering elastic bandwidth pools and global anycast routing to absorb multi-Tbps assaults. Always-on models ensure response within seconds, a necessity amid sub-minute “pulse” attacks. Meanwhile, hybrid architectures are projected to expand at a 15.67% CAGR through 2030 as enterprises merge low-latency, on-premises detection with cloud-scale scrubbing during surge periods. This flexible posture satisfies jurisdictional data constraints while minimizing capex and operational complexity.

On-premises appliances retain niche traction among financial trading platforms, defense agencies, and media broadcasters that demand micro-second mitigation. However, even these verticals are layering cloud capacity for volumetric overflow. Continuous API-driven telemetry exchange between sites, scrubbing nodes, and SIEM platforms is becoming table stakes across the DDoS protection market.

By Organization Size: Large Enterprises Hold Share, SMEs Drive Growth

Large enterprises accounted for 34.56% of 2024 revenue, buoyed by extensive digital estates, stringent uptime SLAs, and mandatory compliance attestations. Procurement cycles emphasize multi-layered controls, integration breadth, and advanced reporting dashboards. Small and midsize enterprises, though smaller in absolute spend, represent the fastest-growing cohort at 15.78% CAGR thanks to SaaS delivery, predictable opex, and bundled managed offers. Subscription tiers that scale with bandwidth and traffic profiles are lowering adoption barriers across the DDoS protection market.

The talent shortage further accelerates managed service uptake: vendors now bundle 24×7 SOC oversight, regulatory documentation, and attack post-mortems. As cyber insurance underwriters tighten coverage prerequisites, both SMEs and mid-market firms are investing in baseline protective controls, expanding the total addressable audience for the DDoS protection industry.

By End-User Industry: IT and Telecom Lead, Healthcare and Life Sciences Surge

IT and telecommunications providers held 35.50% share in 2024, reflecting their status as backbone infrastructure and frequent botnet origin points. Their vast subscriber footprints make service degradation highly visible, reinforcing continuous investment in AI-driven, multi-tenant mitigation. The BFSI segment remains a prime target for politically and financially motivated actors, prompting zero-dwell-time mitigation requirements.

Healthcare and life sciences will post a 14.67% CAGR through 2030, propelled by critical-infrastructure mandates and heightened adversary focus on patient-data availability. Digital front doors, telemedicine portals, and IoT-enabled medical devices broaden the threat surface, compelling hospitals to adopt layered defenses integrated with incident-response playbooks. Retail, energy, and manufacturing increasingly converge IT and OT networks, further expanding the DDoS protection market.

Geography Analysis

DDoS Protection Market in North America

North America’s 39.34% share underscores a mature yet volatile landscape. High-value targets include finance, SaaS, and energy. CISA directives increasingly require real-time telemetry sharing and zero-trust alignment, prompting deeper vendor-customer collaboration on incident response. Investments prioritize encrypted-traffic inspection and machine-learning-driven anomaly scoring.

Asia Pacific exhibits the strongest growth trajectory at 14.89% CAGR. Digital economies are onboarding tens of millions of new broadband and mobile subscribers annually, amplifying botnet recruitment potential. Regional telcos partner with security vendors to deploy edge scrubbing nodes across 5G core networks, reducing hop latency and improving customer experience. Regulatory agencies in Japan and Australia now mandate quarterly resilience reporting for critical infrastructure operators, reinforcing demand across the DDoS protection market.

Europe balances stringent privacy mandates with elevated attack sophistication. NIS2 imposes fines up to 2% of global turnover for inadequate defenses, accelerating migration toward certified, multi-tenant mitigation services. Central and Eastern European utilities face politically motivated flood attacks, driving adoption of AI-guided traffic classification coupled with sovereign data-hosting guarantees. Latin America, the Middle East, and Africa represent emerging vectors both for botnet origination and targeted campaigns, necessitating localized, context-aware defense strategies within the DDoS protection market.

Competitive Landscape

Top Companies in DDoS Protection Market

Market competition is intense and consolidating. DigiCert’s acquisition of Vercara integrated UltraDDoS Protect with a broader digital-trust stack, enabling cross-sell of certificate lifecycle management and DNS services. Akamai, Cloudflare, and F5 leverage massive edge footprints and ML pipelines to deliver millisecond-level mitigation informed by petabyte-scale telemetry. Radware’s partnership with Taiwan’s CHT Security underscores regional MSP alliances aimed at SME penetration.

Emerging challengers exploit innovations in federated learning and blockchain-enhanced telemetry to supply decentralized, low-latency defenses for 5G and industrial IoT ecosystems. Vendors differentiate through API protection, behavioral bot management, and compliance attestation bolted onto core volumetric scrubbing. The table stakes now include automatic attack context sharing with national CERTs, policy-driven failover, and customer self-service portals. As regulations tighten, certified audit trails and rapid remediation reporting will shape purchasing criteria across the DDoS protection market.

Incumbents also invest in programmable SDN-based scrubbing, enabling dynamic path steering and capacity pooling across geographically dispersed nodes. Multi-cloud deployment templates, containerized mitigation functions, and pay-as-you-grow licensing structures enhance stickiness among digitally native enterprises. Competitive gaps remain in ultra-low-latency mitigation for high-frequency trading and sovereign-cloud alignment for defense agencies, presenting whitespace opportunities.

Distributed Denial Of Service (DDoS) Protection Industry Leaders

-

Arbor Networks Inc. (NetScout Systems Inc.)

-

Akamai Technologies Inc.

-

F5, Inc.

-

Radware Ltd.

-

Corero Network Security plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cloudflare mitigated a record 3.8 Tbps flood using its global anycast architecture, underscoring the scale of modern volumetric threats.

- June 2025: Akamai introduced its Behavioral DDoS Engine, applying continuous ML feedback loops to tailor mitigation per application context.

- March 2025: Radware partnered with Taiwan’s CHT Security to deliver AI-powered cloud protection to more than 300 enterprises and 40,000 SMEs.

- February 2025: F5 earned Platinum status in EMA’s PRISM report for Distributed Cloud DDoS Mitigation, citing real-time analytics and global scrubbing coverage.

Global Distributed Denial Of Service (DDoS) Protection Market Report Scope

DDoS prevention refers to the process of protecting a targeted server or network from a distributed denial-of-service (DDoS) attack. A targeted victim can mitigate the incoming threat using specially designed network equipment or a cloud-based protection service.

Distributed Denial of Service (DDoS) Protection Market is segmented by component (solution and service), deployment type (cloud, on-premise, and hybrid), size of enterprise (small and medium enterprises and large enterprises), end-user industry (government and defense, it and telecommunication, healthcare, retail, BFSI, and media and entertainment), and geography (North America, Europe, Asia-Pacific, Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| Solution | Network-layer protection |

| Application-layer protection | |

| DNS protection | |

| Advanced bot mitigation | |

| Service | Professional services |

| Managed services |

| Cloud |

| On-Premises |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Government and Defense |

| Banking, Financial Services and Insurance |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Media and Entertainment |

| Energy and Utilities |

| Manufacturing |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solution | Network-layer protection | |

| Application-layer protection | |||

| DNS protection | |||

| Advanced bot mitigation | |||

| Service | Professional services | ||

| Managed services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Government and Defense | ||

| Banking, Financial Services and Insurance | |||

| Information Technology and Telecommunications | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Media and Entertainment | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the DDoS protection market?

The DDoS protection market size reached USD 4.73 billion in 2025 and is forecast to hit USD 9.13 billion by 2030.

Which deployment model is growing fastest for DDoS mitigation?

Hybrid deployments, combining on-premises appliances with cloud scrubbing, are projected to expand at 15.67% CAGR through 2030.

Which region is expected to show the highest growth in DDoS defense spending?

Asia Pacific is advancing at a 14.89% CAGR, fueled by 5G adoption, IoT proliferation, and evolving regulations.

Which industry vertical is anticipated to record the strongest DDoS defense growth?

Healthcare and life sciences will expand at a 14.67% CAGR as patient-care digitization and critical-infrastructure mandates intensify.

What are the leading components in DDoS protection solutions?

Integrated solution suites covering network-layer, application-layer, DNS, and advanced bot mitigation presently hold 61.23% market share.

Page last updated on: