Data Governance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

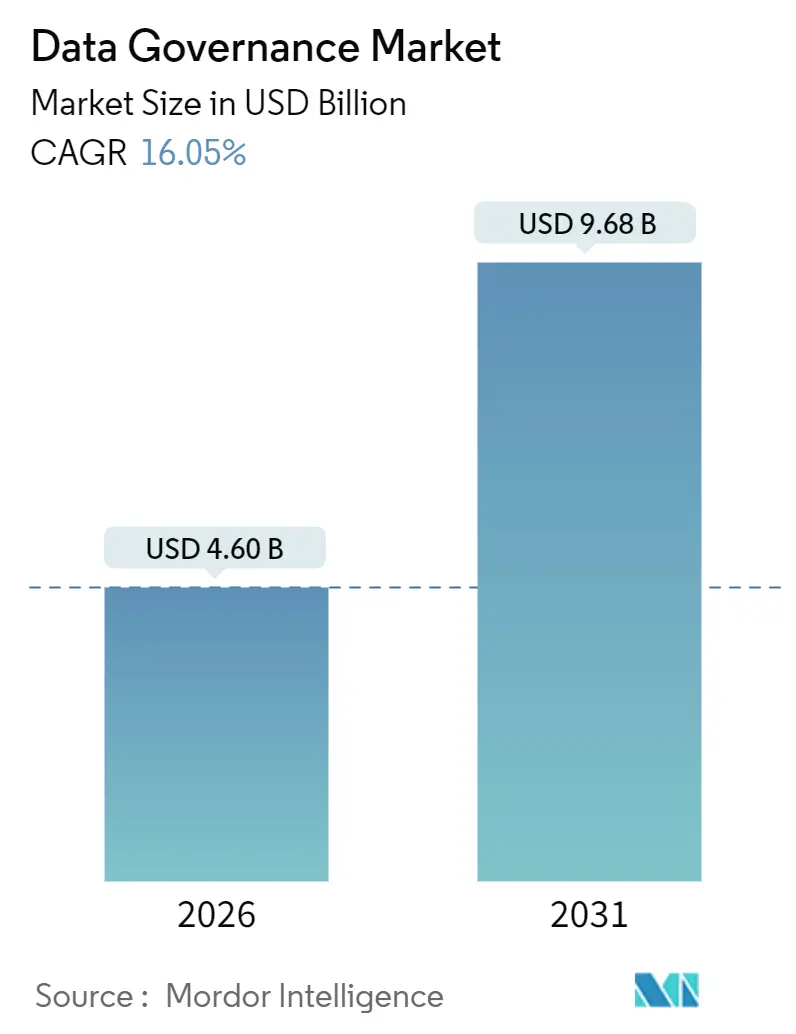

| Market Size (2026) | USD 4.60 Billion |

| Market Size (2031) | USD 9.68 Billion |

| Growth Rate (2026 - 2031) | 16.05% CAGR |

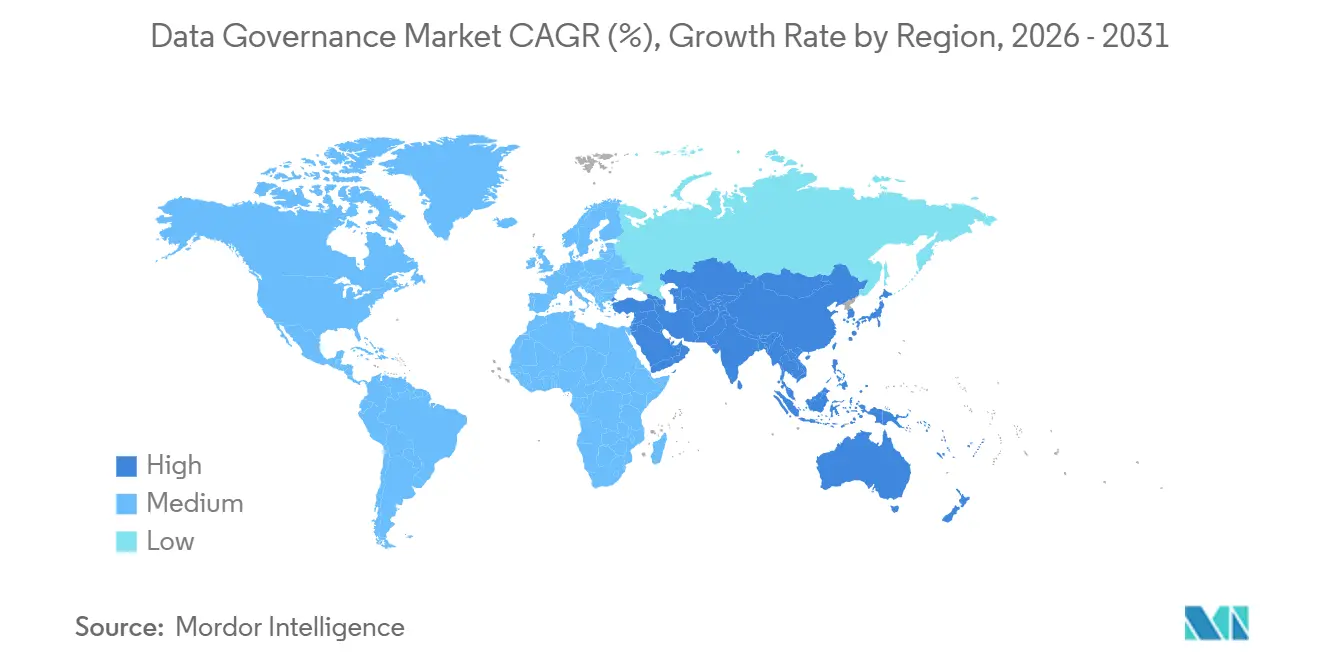

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

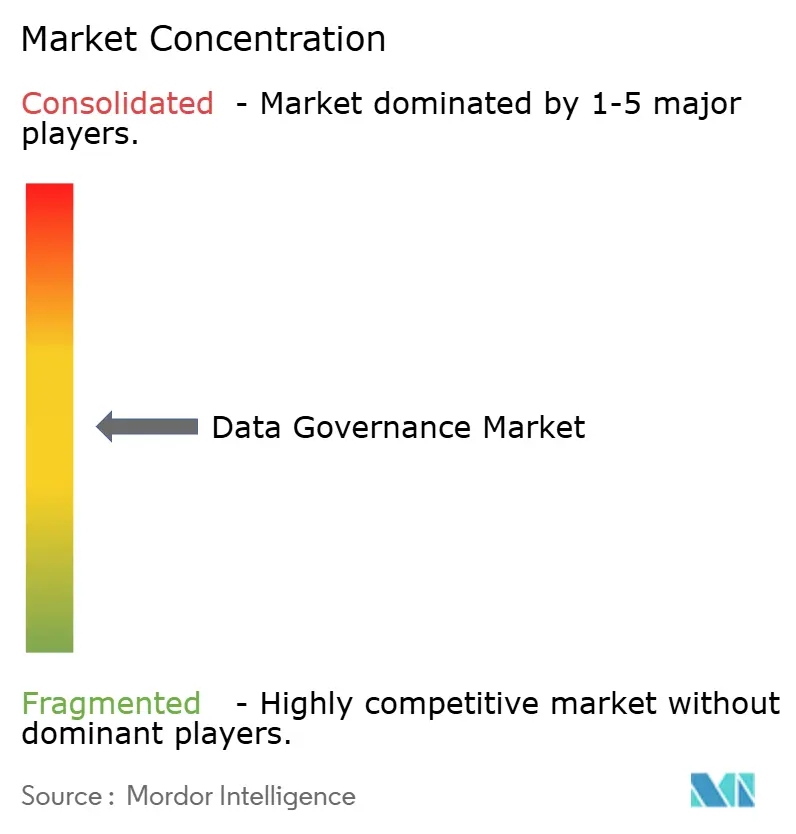

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Governance Market Analysis by Mordor Intelligence

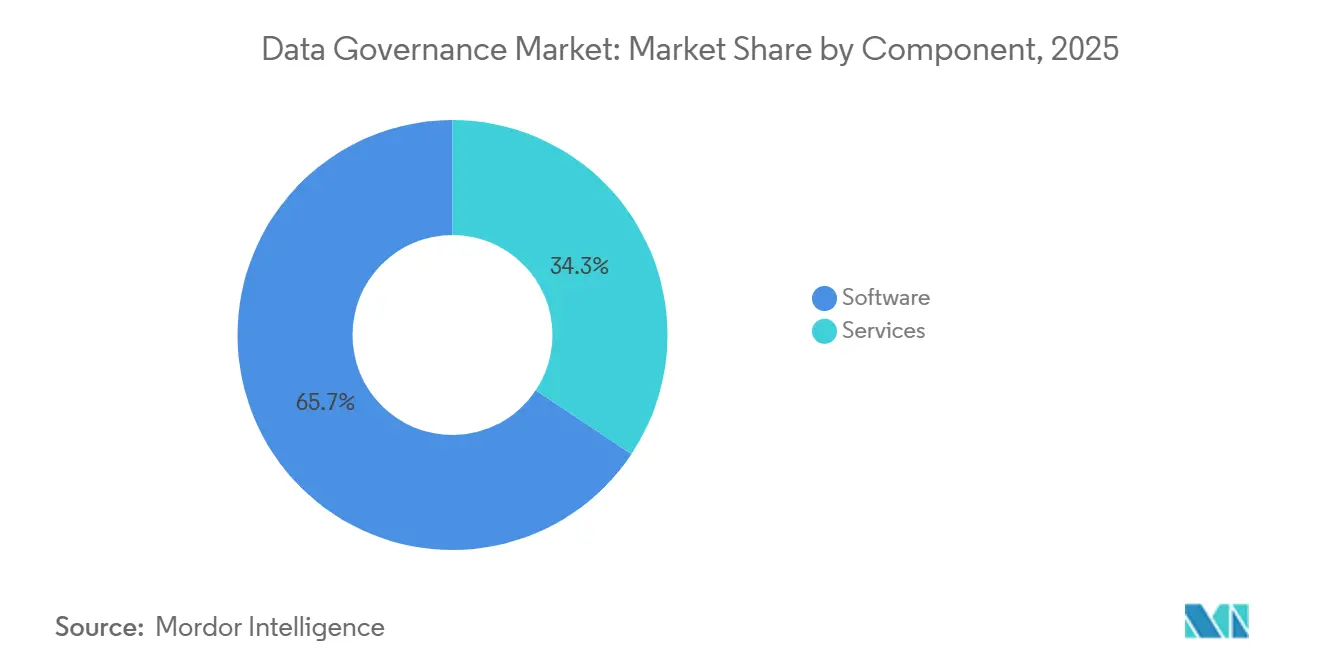

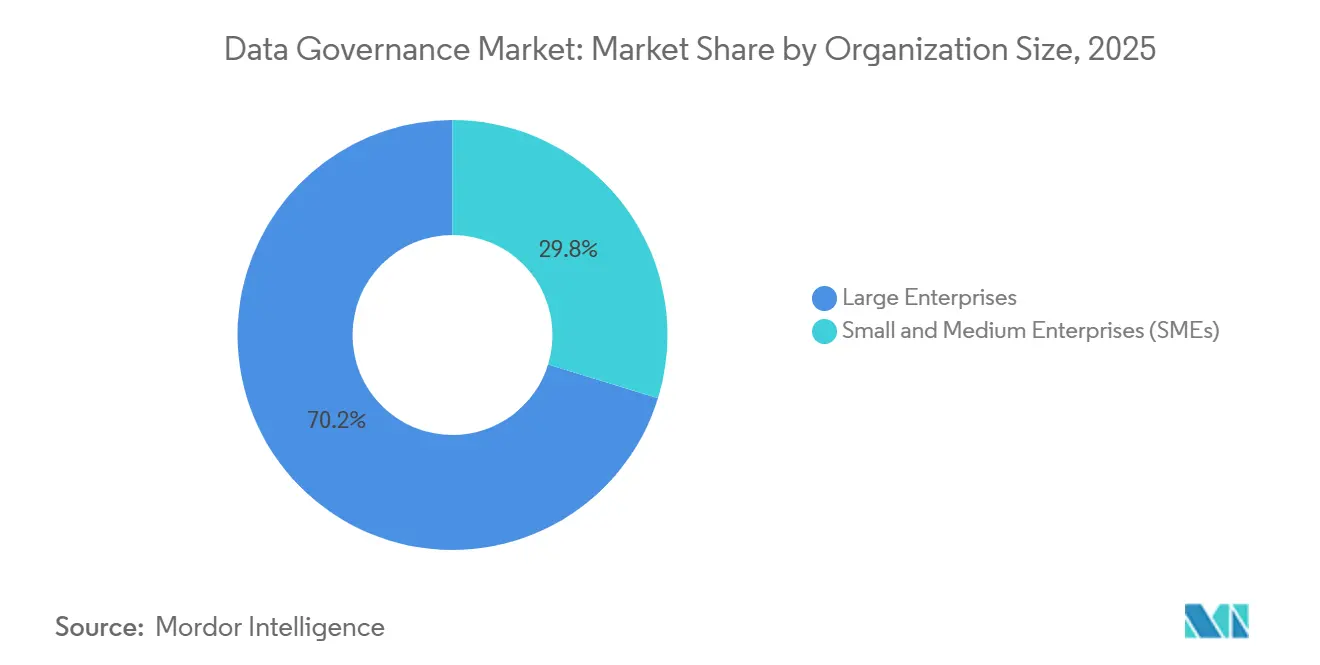

The data governance market size stood at USD 4.60 billion in 2026 and is projected to reach USD 9.68 billion by 2031, translating into a robust 16.05% CAGR across the forecast window. Strategic stewardship of enterprise data is replacing compliance-only postures as regulators demand explainable lineage for AI, real-time payment rails collapse batch reconciliation windows, and sovereign-cloud mandates force in-country catalog replication. Software continued to dominate with 65.66% revenue share in 2025, though data security and privacy governance tools are scaling fastest at 19.62% CAGR. Cloud deployment already accounts for 72.44% of installations and is growing at 17.42% CAGR because hyperscalers embed lineage and quality controls directly into managed pipelines. Large enterprises generated 70.24% of 2025 spending, yet small and medium enterprises are accelerating at 18.76% CAGR as modular SaaS pricing lowers entry barriers for firms lacking seven-figure budgets.

Key Report Takeaways

- By component, software led with 65.66% of revenue in 2025, while data security and privacy governance tools are set to expand at a 19.62% CAGR through 2031.

- By deployment, cloud commanded a 72.44% share of the data governance market size in 2025 and is poised to advance at a 17.42% CAGR to 2031.

- By organization size, large enterprises held 70.24% of 2025 spending, yet small and medium enterprises are projected to grow at an 18.76% CAGR during the same period.

- By business function, IT and operations captured 34.56% of 2025 revenue, whereas legal and compliance is forecast to expand at a 16.38% CAGR through 2031.

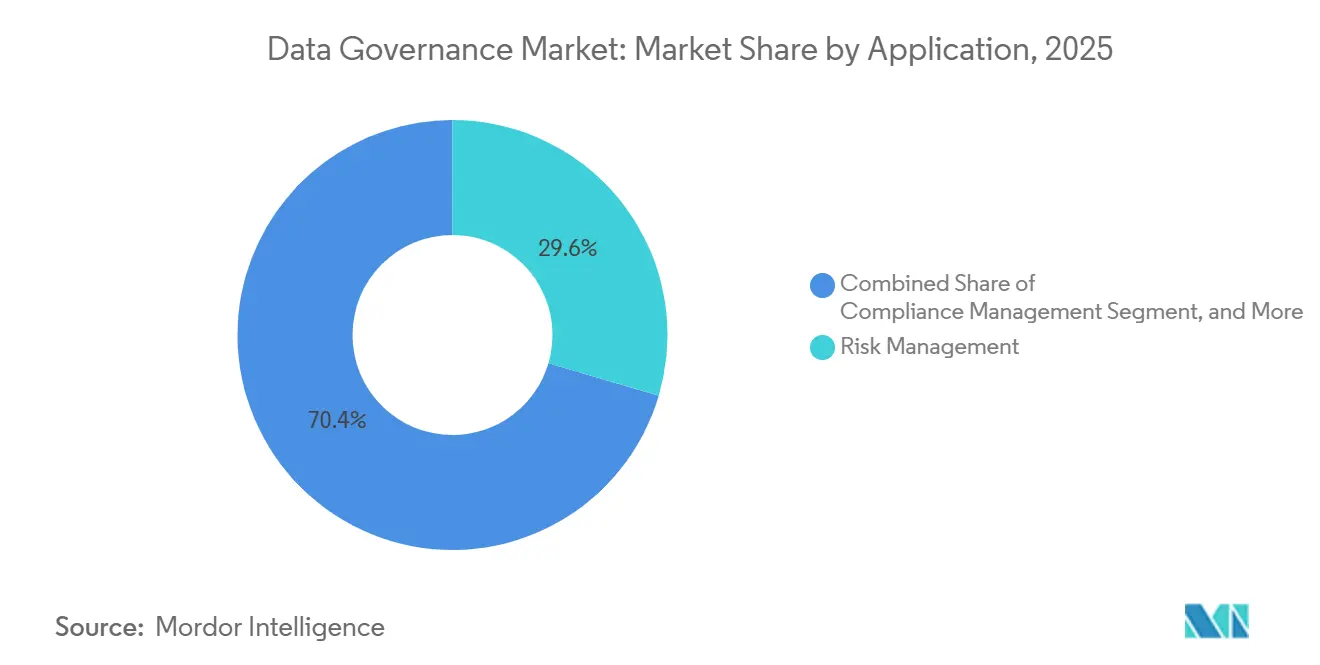

- By application, risk management accounted for 29.56% of the data governance market share in 2025, and data quality management is tracking a 17.58% CAGR to 2031.

- By end-user industry, BFSI led with 25.38% of 2025 spending; manufacturing shows the fastest momentum with an 18.96% CAGR through 2031.

- By geography, North America remained the largest region at 42.64% share in 2025, while Asia Pacific is advancing at an 18.22% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Data Governance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage | +3.2% | Global, with early enforcement in EU27 and spillover to UK, Canada | Medium term (2-4 years) |

| FedNow and Real-Time Payment Rails Forcing Sub-millisecond Data Integrity in North American BFSI | +2.8% | North America, with parallel initiatives in Brazil (PIX) and India (UPI) | Short term (≤ 2 years) |

| Asia Pacific Sovereign-Cloud Mandates Accelerating In-Country Data Catalog Investments | +3.5% | APAC core (India, Indonesia, Vietnam), spillover to Middle East and Africa | Medium term (2-4 years) |

| Retail-Media Monetisation Elevating Product-Master Data Quality Spend | +2.1% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Edge Analytics in Manufacturing 4.0 Demands Near-Edge Metadata Federation | +2.4% | Global, with manufacturing hubs in Germany, China, United States, Japan | Long term (≥ 4 years) |

| Generative AI Governance Use Cases Elevating Automated Metadata Discovery Spend | +3.0% | Global, led by technology firms in North America and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

The EU AI Act has been in force since August 2024 and classifies high-risk systems, compelling deployers to maintain end-to-end lineage that documents data provenance, bias-mitigation steps, and retraining triggers. Multinationals now standardize on automated lineage platforms that parse SQL, Python, and ETL workflows for cross-jurisdictional audit readiness, a trend already mirrored by Canada’s Artificial Intelligence and Data Act.[1]Government of Canada, “Artificial Intelligence and Data Act,” canada.ca Financial institutions face heightened exposure because algorithmic models intertwine AI Act duties with stringent GDPR obligations. Penalties reaching 6% of global turnover elevate governance from an IT concern to a board-level risk, quickly unlocking budget approvals for catalog and lineage projects in the data governance market.

FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North American BFSI

FedNow, which attained critical mass in 2025, processes payments within 10 seconds, compressing reconciliation cycles and demanding real-time data-quality checks at the transaction edge. Banks have retired nightly profiling jobs in favor of streaming tools that validate Kafka topics or Flink state stores in milliseconds. Comparable dynamics in Brazil’s PIX system and India’s UPI underscore a global move toward instant payments, and a single data-quality lapse can cascade into millions of false declines or duplicate postings, far outweighing governance tool costs.

Asia Pacific Sovereign-Cloud Mandates Accelerating In-Country Data Catalog Investments

India’s Digital Personal Data Protection Act restricts cross-border transfers, obliging enterprises to run catalogs within national borders while still synchronizing global metadata.[2]Ministry of Electronics and Information Technology, “Digital Personal Data Protection Act, 2023,” meity.gov.in Indonesia and Vietnam have enacted similar localization laws, prompting hyperscalers to launch sovereign regions and enterprises to implement air-gapped governance stacks.[3]Amazon Web Services, “AWS Sovereign Cloud,” aws.amazon.com Financial services, healthcare, and telecom operators shoulder the heaviest burden as sectoral rules overlay general data-protection statutes, sparking double-digit catalog spending across the region.

Generative AI Governance Use-Cases Elevating Automated Metadata Discovery Spend

Large language models ingest terabytes of unstructured files, making manual tagging infeasible. Organizations now deploy discovery engines that apply NLP to flag sensitive documents before model training. Microsoft Purview and AWS Macie have added AI-specific classifiers, yet double-digit false-positive rates necessitate human-in-the-loop review. Demand is strongest in finance where generative models draft investment memos that must exclude embargoed content, turning automated discovery into a non-negotiable control for audit-ready transparency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling in Tier-1 Banks | -1.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Talent Shortage of Certified Data Stewards and DCAM Practitioners | -1.5% | Global, acute in North America and Western Europe | Medium term (2-4 years) |

| Legacy Mainframe Interoperability Issues Limiting Real-Time Governance in Defense Agencies | -0.9% | National, with early challenges in United States, United Kingdom, France | Long term (≥ 4 years) |

| Limited Inter-Catalog Interoperability Creating Metadata Silos in Multi-Cloud Environments | -1.2% | Global, affecting enterprises with hybrid AWS, Azure, Google Cloud deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling in Tier-1 Banks

Full-stack governance programs can exceed USD 10 million during the first year when software licenses, professional services, and custom connectors are combined, with ongoing spend near USD 5 million annually. Budget approval therefore competes with revenue-generating priorities such as digital banking. Mid-tier banks struggle even more, lacking IT staff to configure complex lineage engines, which further inflates the effective cost per data asset and prolongs payback periods.

Talent Shortage of Certified Data Stewards and DCAM Practitioners

Fewer than 10,000 professionals worldwide hold CDMP or equivalent credentials, with median salaries in North America surpassing USD 120,000 and turnover exceeding 20%. Regulated industries suffer most because stewards must blend domain and compliance knowledge. Universities are only beginning to update curricula, so enterprises adopt AI-assisted classification tools to ease the load, yet those tools still demand human validation, leaving the shortage unresolved in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates but Security Tools Surge

Software generated 65.66% of 2025 revenue as enterprises preferred best-of-breed catalogs, lineage, and master-data platforms over monolithic suites. Data security and privacy governance sub-segments are forecast to grow at 19.62% CAGR, propelled by EU AI Act transparency requirements and sovereign-cloud mandates. Services captured 34.34%, with professional engagements expanding as on-premise estates migrate to cloud architectures. Vendors now overlap governance and observability, folding lineage alerts into DevOps dashboards, although pure-play providers still hold the deepest catalog capabilities.

Demand patterns illustrate how governance converges with cyber postures. Security-oriented platforms automate consent tracking and cross-border transfer logs, while quality and profiling tools extend into machine learning pipelines. The data governance market size attributable to privacy tools is poised to double by 2031. Growth also benefits from ISO 27001 certification trends, because BFSI and healthcare buyers request third-party attestations as procurement prerequisites in the data governance market.

By Deployment: Cloud Leads with Hybrid Architectures Gaining

Cloud deployment owned 72.44% share in 2025 and is on track for a 17.42% CAGR. Hyperscaler services such as AWS Glue Data Catalog, Microsoft Purview, and Google Dataplex integrate lineage at the pipeline level, sidestepping separate catalog rollouts. Digital-native retailers and media firms favor these managed services to minimize operational overhead. On-premise installations remain relevant for defense, government, and highly regulated banks where data must stay behind firewalls, keeping hybrid architectures in play.

Cost dynamics are nuanced. Scanning millions of cloud objects daily can push monthly catalog fees beyond USD 50,000. Consequently, some enterprises repatriate governance workloads to self-hosted Kubernetes clusters, especially when GDPR transfer-impact assessments complicate standard hyperscaler contracts. Over the forecast period, cloud footprints will still expand, but tooling flexibility to trace data across hybrid estates will dictate vendor selection.

By Organization Size: SMEs Adopt Modular SaaS

Large enterprises contributed 70.24% of 2025 revenue thanks to sprawling data estates and dedicated data-office teams. They run multi-year programs with budgets topping USD 1 million and require cross-cloud lineage plus role-based access control. Small and medium enterprises are growing at 18.76% CAGR as vendors unbundle features into per-user SaaS modules, eliminating six-figure upfront licenses.

Vertical-specific bundles are emerging, such as healthcare catalogs pre-populated with HIPAA taxonomies or retail templates that map product master data out of the box. The data governance market share for SMEs will climb as automated classification reduces the need for in-house stewards. Meanwhile, large enterprises experiment with federated governance where business units manage local catalogs but synchronize metadata centrally, heightening demand for inter-catalog APIs.

By Business Function: Legal and Compliance Accelerate

IT and operations sustained 34.56% share in 2025, reflecting ownership of infrastructure budgets. However, legal and compliance is advancing at a 16.38% CAGR because India’s Digital Personal Data Protection Act and the EU AI Act have pushed documentation duties onto in-house counsel. Finance and risk teams remain major users for Basel III and Solvency II reporting.

Marketing departments increasingly rely on catalogs to manage customer consent and retail-media data quality, while HR integrates governance to track diversity analytics under labor laws. Vendors pitching governance as a compliance enabler win quicker funding than those emphasizing productivity because penalties are quantifiable, whereas efficiency gains are harder to monetize.

By Application: Data Quality Management Gains Momentum

Risk management led with 29.56% share in 2025 due to stringent regulatory reporting in BFSI. Data quality management posts the fastest 17.58% CAGR, driven by retail-media networks that cannot tolerate duplicate product entries or stale inventory feeds. Compliance management also commands sizeable demand, automating GDPR and CCPA workflows.

Incident management remains niche but valuable for breach investigations. The data governance market size tied to data quality will swell as unstructured text, image, and IoT streams flood into AI models that require anomaly detection beyond relational profiling. Convergence with observability platforms enables automated quarantine of bad records, closing the loop from detection to remediation in minutes rather than days.

By End-User Industry: Manufacturing Surges on Edge Analytics

BFSI maintained the highest 25.38% share during 2025 as banks and insurers documented lineage for risk and regulatory audits. Manufacturing, however, is expanding at 18.96% CAGR because Industry 4.0 programs must reconcile sensor streams with ERP data in near real time. IT and telecom, healthcare, and retail each deploy governance for sector-specific needs such as 5G fraud detection, clinical-trial integrity, and omnichannel personalization.

In discrete manufacturing, recall liabilities push governance spending higher than in process industries. ISO 9001 and IATF 16949 traceability demands reinforce purchases of automated lineage that can capture shop-floor data without human intervention. As factories modernize MES and PLM systems, data catalog integration becomes an essential companion project.

Geography Analysis

North America held 42.64% share in 2025, underpinned by FedNow adoption, major cloud hyperscalers, and AI regulations converging with Canada’s new federal act. Historical CAGR of roughly 13% has ticked upward as instant payments and generative AI elevate governance urgency. Mexico adds incremental upside as nearshoring extends U.S. supply-chain transparency frameworks.

Asia Pacific is the fastest-growing region at 18.22% CAGR. Sovereign-cloud mandates in India, Indonesia, and Vietnam oblige in-country catalogs, while China’s Personal Information Protection Law drives domestic demand for lineage tools embedded in Alibaba and Tencent clouds. Japan and South Korea invest steadily to support digital manufacturing and open banking, whereas mature Australian markets expand more modestly.

Europe continues to invest due to GDPR and the EU AI Act. Nordic governments adopt cloud-first strategies that favor managed governance services, but Southern and Eastern Europe lag owing to constrained budgets. The Middle East and Africa and South America remain smaller markets, yet sovereign investment funds and privacy statutes in the UAE, Brazil, and South Africa are catalyzing compliance-driven rollouts.

Competitive Landscape

Competitive Landscape

The market is moderately fragmented. Hyperscalers bundle governance into platform services that appeal to single-cloud adopters, while neutral vendors such as Collibra, Informatica, and Alation position themselves as cross-cloud orchestration layers. New entrants like Monte Carlo and Ataccama embed lineage into data observability workflows, broadening the field.

White-space opportunities persist in real-time lineage for streaming architectures and automation for unstructured lakes. Partnerships between catalog and security providers such as Varonis and OneTrust combine discovery with access governance. Vendors differentiate through generative-AI capabilities, natural-language search, and blockchain-backed audit trails, though these features still demand human oversight to validate edge cases.

Pricing and implementation complexity keep total cost of ownership high, but modular SaaS and vertical templates are lowering barriers for SMEs. Vendor roadmaps now emphasize sovereign-cloud readiness and AI-driven classifiers to maintain relevance amid accelerating regulation.

Data Governance Industry Leaders

Collibra NV

TIBCO Software Inc.

Alation Inc.

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft announced general availability of Purview Data Governance for Azure OpenAI Service, enabling automated lineage for generative-AI training datasets.

- December 2025: Collibra completed its acquisition of Octopai to enhance automated discovery across legacy ETL and mainframe systems.

- November 2025: AWS launched Glue Data Catalog Federation, allowing unified metadata queries across AWS, Azure, and Google estates.

- October 2025: Informatica committed USD 150 million to expand its Bangalore engineering hub focused on AI-powered metadata discovery for sovereign-cloud deployments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data governance market as all software and related services that set policies, steward metadata, trace lineage, monitor quality, and enforce privacy for enterprise data assets across on-premise and cloud environments. The focus lies on platforms and professional services that help large and mid-size organizations meet regulatory mandates and turn trusted data into business value.

Scope exclusions include stand-alone data quality utilities, master data management suites marketed without governance modules, and generic AI governance tools that fall outside this boundary.

Segmentation Overview

- By Component

- Software

- Data Quality and Profiling Tools

- Metadata Management and Data Catalog

- Master Data Management

- Data Lineage and Impact Analysis

- Data Security and Privacy Governance

- Services

- Professional Services

- Managed Services

- Software

- By Deployment

- Cloud

- On-Premise

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Business Function

- IT and Operations

- Legal and Compliance

- Finance and Risk

- Marketing and Sales

- Human Resources

- Other Business Functions

- By Application

- Compliance Management

- Risk Management

- Audit Management

- Incident Management

- Data Quality Management

- Other Applications

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Retail and E-Commerce

- Government and Defense

- Manufacturing

- Energy and Utilities

- Media and Entertainment

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Chile

- Mexico

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Sweden

- Norway

- Finland

- Denmark

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chief data officers across North America, Europe, and Asia Pacific, plus regional compliance consultants and open-source tool maintainers, to test revenue pools, refresh user penetration ratios, and sense-check pricing shifts flagged during desk work. These conversations filled gaps around shadow IT spending and phase-wise rollouts in heavily regulated verticals.

Desk Research

We began by mapping publicly available statistics from authorities such as the EU Commission, the U.S. Federal Trade Commission, and India's DPDP nodal ministry, which quantify regulatory fines and enforcement trends that spur governance spending. Trade bodies, including EDM Council and the Cloud Security Alliance, provide adoption benchmarks, and corporate 10-Ks reveal budget shares assigned to compliance tooling. News and patent feeds from Dow Jones Factiva and Questel helped us trace vendor product launches and IP clusters to size emerging demand pockets. Company filings, investor decks, and procurement data extracted from Volza offered unit-price signposts that anchor our average selling price (ASP) curves. This list is illustrative; many other sources informed data collection, validation, and clarifications.

Two periodic deep dives into peer-reviewed journals and conference papers, such as IEEE's Big Data series, helped us confirm the technical domains included and identify spend drivers tied to cloud migration and AI initiatives before we carried those insights into the model.

Market-Sizing & Forecasting

A top-down construct starts with the global enterprise IT security and management outlay, which is then filtered by the share earmarked for governance based on regulation severity indices, data-center footprint, and cloud penetration. Supplier roll-ups of leading vendors and sampled ASP multiplied by active license counts supply a bottom-up cross-check, and any variance above three percentage points triggers model recalibration. Key variables include the annual count of material data-breach fines, average terabytes stored per enterprise, proportion of workloads shifted to public cloud, number of AI projects in production, and median price of enterprise governance suites. We project forward through multivariate regression blended with scenario analysis for landmark policy shifts (for instance, the EU AI Act), thus capturing both linear spend drivers and step-change shocks.

Data Validation & Update Cycle

Outputs undergo internal peer review and anomaly checks against third-party shipment logs and audited vendor revenues. When quarterly filings or major legislative events signal deviation beyond preset thresholds, an interim update is issued; otherwise, reports refresh each year, and an analyst revisits every table before final delivery to clients.

Why Mordor's Data Governance Baseline Earns Superior Credibility

Published estimates often diverge because firms slot different tool categories, apply varied ASP assumptions, or freeze exchange rates on dissimilar dates.

Key gap drivers include narrower component mixes, aggressive pricing uplift, or slower refresh cadences adopted elsewhere, whereas Mordor's model locks scope to governance-centric platforms, blends observed ASPs with contract-weighted discounts, and updates forex at every revision.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.91 B (2025) | Mordor Intelligence | - |

| USD 3.35 B (2023) | Global Consultancy A | Excludes professional services and applies 2022 FX rates |

| USD 4.75 B (2025) | Regional Consultancy B | Counts adjacent data quality tools and uses vendor list prices |

| USD 4.44 B (2024) | Industry Journal C | Projects growth from a single-region survey before extrapolating globally |

In sum, the disciplined scoping, timely updates, and dual-angle validation adopted by Mordor Intelligence give decision-makers a balanced, transparent baseline that traces each number back to observable variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the data governance market in 2031?

The market is forecast to reach USD 9.68 billion by 2031, reflecting a 16.05% CAGR from 2026 to 2031.

Which component is expanding the fastest through 2031?

Data security and privacy governance software is growing at a 19.62% CAGR as firms meet AI-related transparency and localization mandates.

Why is Asia Pacific the fastest-growing region?

Sovereign-cloud laws in India, Indonesia, and Vietnam force in-country catalog deployment, driving an 18.22% CAGR in regional spending.

How are small and medium enterprises adopting governance tools?

Modular SaaS pricing and vertical-specific templates reduce upfront costs, propelling SME spending at an 18.76% CAGR.

Which application shows the strongest growth momentum?

Data quality management leads with a 17.58% CAGR as retail-media and IoT use cases demand cleaner, real-time datasets.

What key challenge hampers large-scale governance programs?

High total cost of ownership, often exceeding USD 10 million in the first year for Tier-1 banks, slows adoption despite regulatory pressure.

Page last updated on: