Market Size of Data Center Processor Industry

| Study Period | 2022 - 2029 |

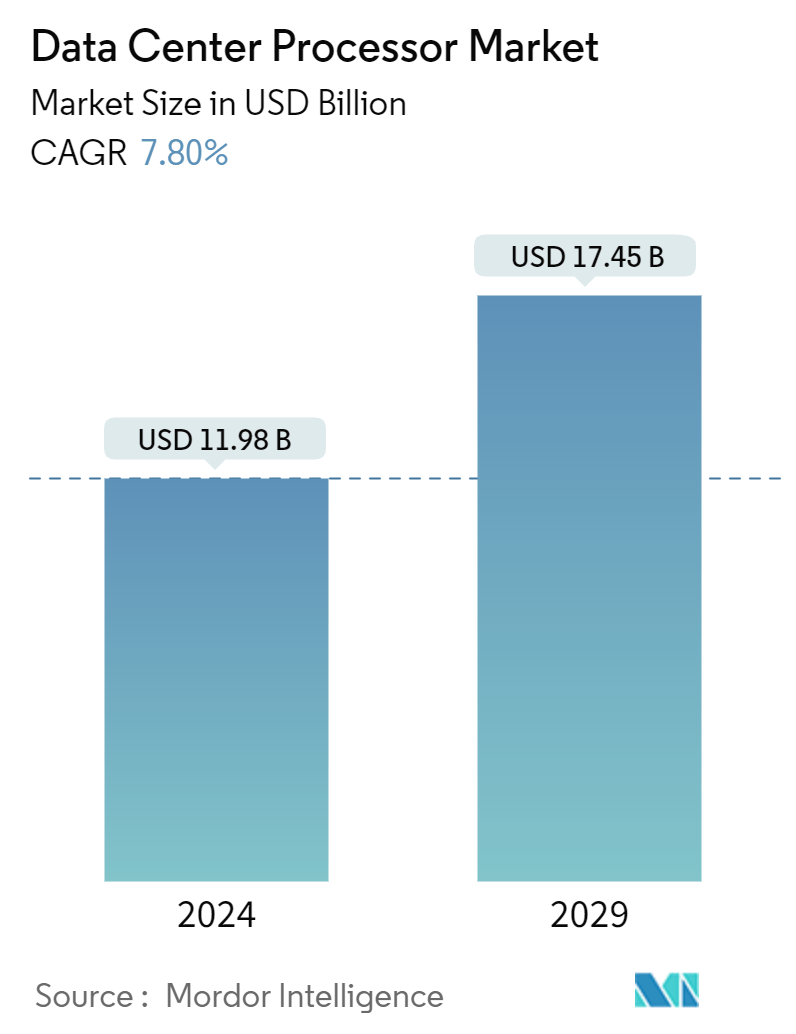

| Market Size (2024) | USD 11.98 Billion |

| Market Size (2029) | USD 17.45 Billion |

| CAGR (2024 - 2029) | 7.80 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Data Center Processor Market Analysis

The Data Center Processor Market size is estimated at USD 11.98 billion in 2024, and is expected to reach USD 17.45 billion by 2029, growing at a CAGR of 7.80% during the forecast period (2024-2029).

- A data center processor is a critical component of a data center's computing infrastructure. It is a high-performance chip that performs various tasks, including arithmetic, logic, and input/output operations. Data centers rely on servers, which are high-performance computers with large storage space, memory, processing power, and input/output capabilities. These servers use data center processors to handle the computational workload and run applications. The choice of processors in a data center depends on the specific tasks and requirements. General-purpose CPUs may be suitable for many applications, but processors optimized for these workloads may be preferred for specialized tasks like artificial intelligence (AI) and machine learning (ML).

- CPU processors are the most common type of processors found in data centers. They provide the capability to handle various tasks and applications, making them versatile and adaptable. Initially designed for graphics-intensive applications, GPU processors have become indispensable in data centers due to their parallel processing capabilities. GPUs perform highly parallel computations, making them suitable for machine learning, artificial intelligence, and big data analytics. Their massive number of cores enables them to process vast amounts of data simultaneously, significantly reducing processing time and improving overall performance.

- FPGA processors offer the advantage of programmable hardware, allowing customization to specific applications. They provide the flexibility to reconfigure their circuitry, making them suitable for tasks that require low latency and high throughput. FPGA processors are often used for functions such as encryption, video processing, and network packet processing, where real-time processing is crucial.

- With the proliferation of connected devices, cloud computing, and the Internet of Things, the amount of data being generated is increasing at an unprecedented rate. This surge in data necessitates powerful processors that can handle data centers' processing and analysis requirements. Further, data centers are responsible for processing and analyzing vast real-time data. As industries increasingly rely on data-driven insights and complex computations, processors must deliver high performance and efficiently handle demanding workloads.

- Moreover, energy efficiency is a significant market driver for data center processors. Data centers consume enormous amounts of energy, and optimizing power consumption is crucial for reducing operational costs and environmental impact. Processors that offer higher performance per watt are in high demand as they allow for more efficient data center operations. Moreover, the increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies is driving the demand for processors with enhanced capabilities in handling AI workloads. AI and ML algorithms require powerful processors to process and analyze complex data patterns and make accurate predictions, driving the need for specialized processors optimized for AI workloads.

- One of the key macroeconomic trends that can affect the data center processors market is GDP growth. As the economy expands, companies are inclined to increase their investments in IT infrastructure, such as data centers. This increased investment leads to a higher demand for data center processors, as businesses require more computing power to handle the growing volume of data. For instance, the United States is a prominent data center market. According to the Bureau of Economic Analysis (BEA), the US GDP increased from USD 25.7 trillion in 2022 to about USD 27.36 trillion in 2023.

- However, the data center processor market faces several market restraints that can hinder its growth and potential. The high cost of data center processors is a significant barrier for small and medium-sized businesses, limiting their adoption. Additionally, the rapid technological advancements in the industry lead to a shorter lifecycle of processors, making it challenging for businesses to keep up with the latest innovations.

Data Center Processor Industry Segmentation

A data center processor is a key component of a computing infrastructure. It is a high-performance chip that performs various tasks, including arithmetic, logic, and input/output operations.

The data center processor market is segmented by processor type (CPU [central processing Unit], GPU [graphics processing unit], FPGA [field-programmable gate array], ASIC [application-specific integrated circuit] only ai-dedicated accelerators, and networking accelerators [Smart NIC and DPUs]), application (artificial intelligence [deep learning & machine learning], data analytics/graphics, and high-performance computing [HPC]/scientific computing), and geography (North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America). The report offers the market size and forecasts for all the above segments in value (USD).

| By Processor | |

| CPU (Central Processing Unit) | |

| GPU (Graphics Processing Unit) | |

| FPGA (Field-programmable Gate Array) | |

| ASIC (Application-specific Integrated Circuit) - Only AI-dedicated Accelerators | |

| Networking Accelerators (SmartNIC and DPUs) |

| By Application | |

| Artificial Intelligence (Deep Learning and Machine Learning) | |

| Data Analytics/Graphics | |

| High-performance Computing (HPC)/Scientific Computing |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Data Center Processor Market Size Summary

The data center processor market is poised for significant growth, driven by the increasing demand for high-performance computing solutions to manage the burgeoning volume of data generated by connected devices, cloud computing, and the Internet of Things. Data center processors, including CPUs, GPUs, and FPGAs, are integral to the infrastructure of data centers, enabling them to perform complex computations and handle vast amounts of data efficiently. The market is characterized by the need for processors that offer high performance, energy efficiency, and the ability to support advanced applications such as artificial intelligence and machine learning. As industries continue to rely on data-driven insights, the demand for specialized processors optimized for these workloads is expected to rise, further propelling market growth.

The market landscape is semi-consolidated, with major players like Intel, NVIDIA, AMD, Xilinx, and Arm Holdings leading the charge in innovation to meet evolving consumer needs. These companies are continuously developing advanced products to enhance processing capabilities and energy efficiency. The rapid expansion of cloud computing services and the increasing adoption of AI and machine learning technologies are key drivers of market expansion. However, challenges such as high costs and the rapid pace of technological advancements pose constraints, particularly for small and medium-sized enterprises. Despite these challenges, the market is set to experience robust growth, supported by substantial investments in data center infrastructure and the ongoing demand for powerful, efficient processors.

Data Center Processor Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Technology Snapshot

-

1.2.1 Impact of Deep Learning, Public Cloud Interface, and Enterprise Interface on Data Center Accelerators

-

1.2.2 Technological Updates/Developments by Various Vendors

-

-

1.3 Industry Value Chain Analysis

-

1.4 Industry Attractiveness - Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

1.5 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

-

1.6 Market Scenario Based on the Setup - On-premise vs Cloud

-

-

2. MARKET SEGMENTATION

-

2.1 By Processor

-

2.1.1 CPU (Central Processing Unit)

-

2.1.2 GPU (Graphics Processing Unit)

-

2.1.3 FPGA (Field-programmable Gate Array)

-

2.1.4 ASIC (Application-specific Integrated Circuit) - Only AI-dedicated Accelerators

-

2.1.5 Networking Accelerators (SmartNIC and DPUs)

-

-

2.2 By Application

-

2.2.1 Artificial Intelligence (Deep Learning and Machine Learning)

-

2.2.2 Data Analytics/Graphics

-

2.2.3 High-performance Computing (HPC)/Scientific Computing

-

-

2.3 By Geography***

-

2.3.1 North America

-

2.3.2 Europe

-

2.3.3 Asia

-

2.3.4 Australia and New Zealand

-

2.3.5 Latin America

-

2.3.6 Middle East and Africa

-

-

Data Center Processor Market Size FAQs

How big is the Data Center Processor Market?

The Data Center Processor Market size is expected to reach USD 11.98 billion in 2024 and grow at a CAGR of 7.80% to reach USD 17.45 billion by 2029.

What is the current Data Center Processor Market size?

In 2024, the Data Center Processor Market size is expected to reach USD 11.98 billion.