Data Center Processor Market Size and Share

Market Overview

| Study Period | 2022 - 2030 |

|---|---|

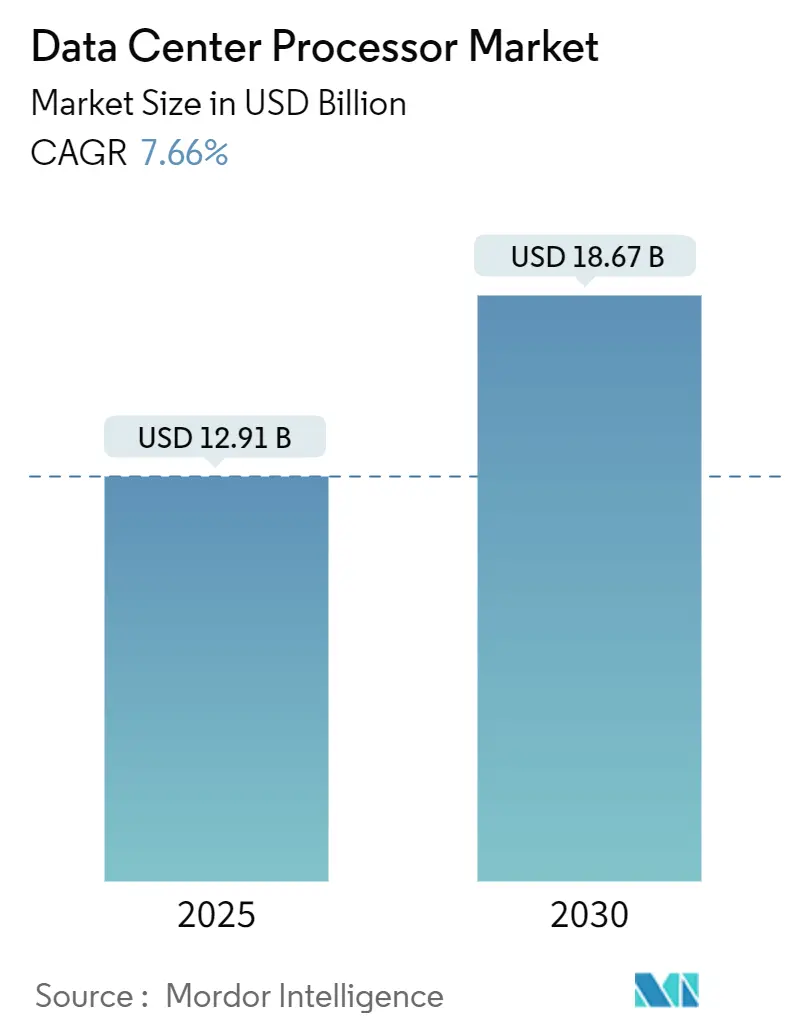

| Market Size (2025) | USD 12.91 Billion |

| Market Size (2030) | USD 18.67 Billion |

| Growth Rate (2025 - 2030) | 7.66% CAGR |

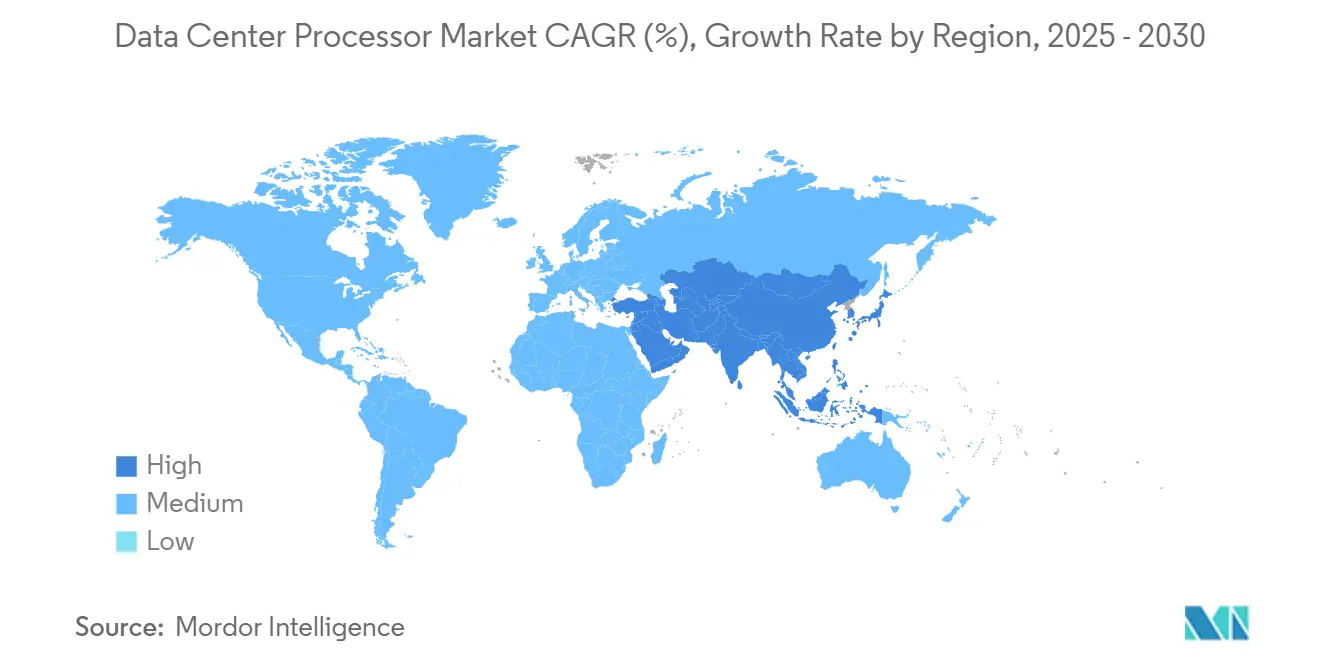

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Center Processor Market Analysis by Mordor Intelligence

The Data center processor market size is valued at USD 12.91 billion in 2025 and is forecast to reach USD 18.67 billion by 2030, advancing at a 7.66% CAGR. Growing artificial intelligence (AI) workloads, the pivot to energy-efficient architectures, and region-wide semiconductor incentives are reshaping global demand. Specialized accelerators, including GPUs and ARM-based CPUs, are easing the computational bottlenecks created by generative AI while export controls spur architectural diversification. Edge and micro data centers gain momentum as latency-sensitive inference pushes compute closer to users, and sustainability mandates accelerate adoption of high-core-count processors. Supply chain constraints around CoWoS packaging and high-bandwidth memory remain the principal headwinds, yet capacity expansions by leading foundries and memory makers signal gradual relief beyond 2026.

Key Report Takeaways

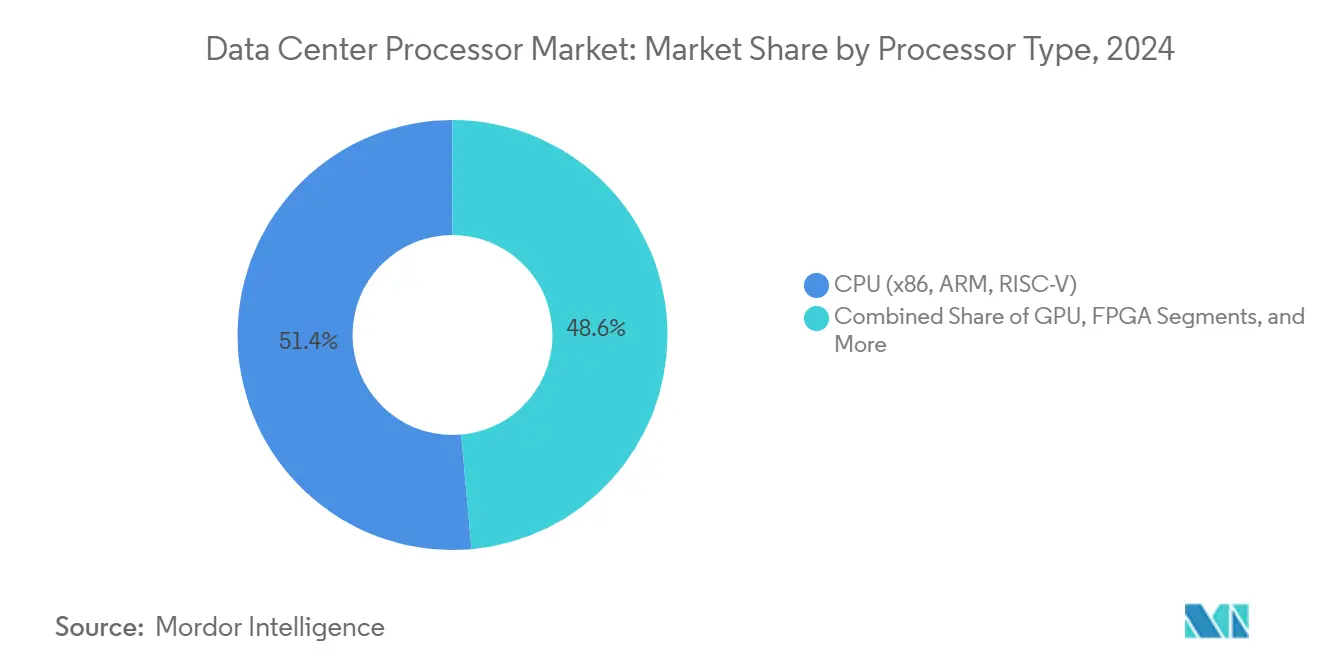

- By processor type, CPUs held 51.4% of the data center processor market share in 2024, while GPUs are projected to rise at a 12.5% CAGR through 2030.

- By deployment model, hyperscale cloud data centers led with 48.1% revenue share in 2024; edge/micro data centers are set to expand at a 14.8% CAGR to 2030.

- By application, AI/deep learning accounted for 38.3% of the data center processor market size in 2024, whereas HPC/scientific computing is progressing at an 11.2% CAGR through 2030.

- By end-user industry, IT & telecommunications contributed 34.5% share of the data center processor market size in 2024; healthcare and life sciences are forecast to grow at a 9.3% CAGR.

- By geography, North America led with 27.8% revenue share in 2024, while Asia-Pacific is expanding at an 8.2% CAGR.

Global Data Center Processor Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale AI Workload Surge Increasing GPU and ASIC Demand in North-American Cloud Clusters | 2.8% | North America, Global spillover | Short term (≤ 2 years) |

| Rising Adoption of ARM-based CPUs in Chinese Hyperscalers to Optimize TCO | 1.4% | China, APAC expansion | Medium term (2-4 years) |

| SmartNIC/DPU Integration to Offload Networking and Reduce Latency in Edge Data Centers | 1.1% | Global, concentrated in edge locations | Medium term (2-4 years) |

| Government-Subsidized Semiconductor Fabs in Asia-Pacific Expanding Local Supply of Server CPUs | 0.9% | Asia-Pacific, Japan, South Korea | Long term (≥ 4 years) |

| Rapid Refresh Cycles for PCIe Gen5 and CXL-Ready Processors in European Colocation Sites | 0.7% | Europe, North America | Short term (≤ 2 years) |

| Sustainability Mandates Driving Shift to High-Core-Count Energy-Efficient CPUs in the Nordics | 0.5% | Nordic region, EU expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale AI workload surge boosting GPU and ASIC demand

Compute requirements for training and inference of large language models climbed sharply in 2025, prompting cloud operators to reserve nearly full output from advanced packaging lines that serve GPUs equipped with high-bandwidth memory. Rack power densities breached 100 kW in several hyperscale clusters, forcing facility designs to transition to liquid cooling. Capital commitments from leading providers exceed USD 80 billion in new AI-ready campuses, reinforcing a structural rather than cyclical demand pattern.[1]Microsoft, “Investment Fact Sheet on AI Data Center Expansion,” microsoft.com Data center operators view this shift as a permanent architectural reset that centers on accelerated compute.

ARM-based CPU adoption in Chinese hyperscalers lowering total cost of ownership

Chinese cloud platforms widened deployments of ARM servers after performance gains and power savings were validated in production databases. In parallel, indigenous RISC-V designs entered pilot phases, underscoring national strategies aimed at semiconductor self-reliance. Market analysts expect ARM to reach one-half of cloud CPU deliveries by 2026, signaling enduring changes in procurement preference beyond China as public clouds worldwide test core-dense ARM platforms for container workloads.

SmartNIC/DPU integration cutting latency in edge data centers

Data processing units (DPUs) offload encryption, storage, and network virtualization, reducing CPU overhead by up to 70% in field trials. Edge locations deploy DPUs to sustain 100 Gbps links while maintaining deterministic latency for real-time analytics. Research shows Key-Value store throughput improves more than fourfold under optimized SmartNIC configurations, a gain that unlocks new service revenue at the network edge. Implementation complexity is falling as software ecosystems mature, accelerating mainstream adoption.

Government-subsidized fabs increasing local server CPU supply

Asia-Pacific governments expanded incentive programs to secure next-generation logic and packaging capacity. Japan allocated USD 4.9 billion for an advanced fab that will supply 6-nm and finer-pitch server chips, while South Korea launched a USD 1.1 billion GPU development plan. These policies underpin long-run supply resilience, enabling regional cloud and colocation providers to access advanced processors at reduced geopolitical risk and lower logistics cost.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent CoWoS and HBM Packaging Bottlenecks Limiting GPU Shipments | -1.8% | Global, concentrated in Taiwan | Short term (≤ 2 years) |

| Cooling and Power-Density Constraints in Legacy On-Premise Facilities | -1.2% | Global, mature markets | Medium term (2-4 years) |

| Export Controls on Advanced AI Processors to China Disrupt Global Supply Chains | -0.9% | Global, China-focused | Medium term (2-4 years) |

| Scarcity of Firmware and Kernel Talent for Heterogeneous DPU Architectures | -0.6% | Global, developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CoWoS and HBM bottlenecks limiting GPU shipments

Through-silicon-via stacking and high-bandwidth memory packaging scale more slowly than wafer front-end capacity, constraining availability of top-bin AI accelerators.[2]SK Hynix, “HBM Supply Status,” skhynix.com Leading foundries report full bookings through 2026, while memory vendors signal sold-out allocations. The shortage inflates lead times to nine months for flagship GPUs and restrains near-term revenue upside for cloud operators seeking to expand AI clusters.[3] NVIDIA Corporation, “CoWoS Capacity Allocation Update,” nvidia.com

Cooling and power-density constraints in legacy facilities

Traditional on-premise data centers designed for sub-12 kW racks struggle to host modern accelerators that exceed 700 W per socket. Air-cooled systems reach thermal limits quickly, driving higher energy use and stranded capacity. Operators face difficult retrofit economics, often opting for greenfield builds that support liquid cooling loops and high-voltage power distribution. The capital burden slows migration for enterprises with aging estates.

Segment Analysis

By Processor Type: GPU acceleration captures growth upside

The data center processor market size for CPUs remained dominant in 2024, yet GPUs posted the fastest expansion at a 12.5% CAGR, reflecting unrelenting AI training demand. GPUs integrate thousands of cores and high-bandwidth memory that deliver substantial performance per watt for tensor operations. Supply constraints continue as leading GPU vendors reserve advanced packaging lines, but additional CoWoS capacity slated for 2027 should gradually balance demand. ARM-based CPUs and custom accelerators from hyperscalers diversify compute choices, creating competitive pricing pressure on traditional x86 incumbents. FPGA and ASIC products also gain share in specialized workloads where deterministic latency outweighs general-purpose flexibility.

A second wave of heterogeneous architectures is forming as CPU, GPU, and DPU roadmaps converge around chiplet topologies. Cloud operators assess these developments to match application kernels with the lowest total cost of ownership. The outcome is a nuanced procurement landscape in which performance density, thermal efficiency, and software ecosystem breadth determine platform selection more than single-thread results.

Note: Segment shares of all individual segments available upon report purchase

By Application: AI and HPC converge

AI/deep learning held the largest 38.3% share of the data center processor market size in 2024, driven by model training that scales quadratically with parameter count. HPC/scientific computing shows the highest 11.2% CAGR as exascale programs adopt hybrid CPU-GPU nodes that handle both floating-point and matrix math. Convergence blurs historical distinctions between supercomputing and AI services, fostering co-design of hardware and software stacks. Data analytics maintains steady momentum, yet an increasing portion of analytic pipelines incorporates machine learning inference, elevating demand for mixed-precision engines.

Network and storage offload workloads transition to DPUs that free CPU cycles for revenue-generating tasks, while graphics virtualization supports new streaming workloads in creative and metaverse applications. These shifts encourage cross-domain silicon reuse, further blending application categories and broadening the total addressable opportunity.

By Deployment Model: Edge gains speed

Hyperscale cloud continues to command 48.1% of revenue, but edge and micro architectures are expected to outpace at a 14.8% CAGR as enterprises pursue near-user inference to meet stringent latency targets. Micro data centers typically operate at power utilization efficiency below 1.05 and support rack-level liquid cooling, delivering compute closer to industrial IoT endpoints and 5G base stations. Hybrid models spread workloads among on-premise, colocation, cloud, and edge resources, yielding resilience and cost optimization. Colocation providers accelerate expansion with AI-ready halls and plug-and-play liquid cooling loops, offering an attractive migration path for enterprises unwilling to build new facilities.

Legacy enterprise campuses confront upgrade crossroads as processor thermal design power climbs. Some firms deploy smaller GPU pods on-premise for data-privacy-sensitive workloads while bursting peak requirements to cloud. This balanced model supports flexible budgets and risk management.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare accelerates

IT and telecommunications retained the top revenue position at 34.5% in 2024, yet healthcare and life sciences are projected to post the quickest 9.3% CAGR. Diagnostic imaging analysis, genomics, and drug discovery drive demand for on-device inference and high-memory GPUs. BFSI sustains investment in fraud analytics and low-latency trading, whereas government agencies prioritize cybersecurity and surveillance workloads. Manufacturing firms apply predictive maintenance through edge inferencing that minimizes downtime, and retailers embrace real-time recommendation engines. Taken together, vertical adoption underscores the broad relevance of accelerated compute.

Geography Analysis

North America generated the largest revenue in 2024 owing to hyperscaler investments and a mature cloud ecosystem. Multi-billion-dollar expansion projects, including AI-optimized campuses powered by nuclear or renewable energy, reinforce regional dominance. Policy incentives under the CHIPS and Science Act catalyze domestic advanced-node fabrication, easing long-term supply vulnerability.[4]U.S. Department of Commerce, “CHIPS and Science Act Implementation Report,” commerce.gov Canada’s AI research clusters likewise attract new colocation builds that incorporate liquid cooling and dense GPU trays.

Asia-Pacific exhibits the strongest growth trajectory at an 8.2% CAGR. Manufacturing subsidies in Japan, South Korea, and Taiwan reduce cost structures for local operators, while Chinese providers race toward architectural self-sufficiency through ARM and RISC-V deployments. Southeast Asian nations court cloud entrants with tax holidays and renewable energy commitments, positioning the region as an emerging edge-compute hotbed.

Europe emphasizes sustainability, with Nordic sites leveraging abundant hydropower to offer attractive total cost of ownership. The European Union’s reporting requirements on energy and water efficiency incentivize high-core-count, low-power processors and advanced liquid cooling. Middle East and Africa markets are scaling rapidly from a small base, highlighted by landmark investments in Saudi Arabia that bundle renewable power with next-generation GPU clusters.

Competitive Landscape

The data center processor market features moderate concentration as traditional x86 incumbents confront ARM, GPU, and custom-ASIC challengers. Intel and AMD maintain large CPU installed bases, yet hyperscalers’ proprietary silicon programs dilute future share. NVIDIA’s leadership in AI accelerators secures extended supply agreements, compelling rivals to differentiate through price, power efficiency, and ecosystem depth.

Strategic collaborations intensify. Chiplet interconnect standards encourage multi-vendor assemblies that mix CPU, GPU, and DPU tiles. Foundries expand advanced packaging services, lowering barriers for fabless entrants. Venture funding flows to startups specializing in transformer inference chips and storage-attached processing.

Export controls spur regionalization of supply chains. Chinese firms invest in domestic fabs and alternative architectures, while Western operators diversify sourcing across multiple foundries. Component scarcity compels closer alignment between server vendors and memory suppliers to secure HBM allocations. The next competitive phase hinges on delivering performance per watt gains while mitigating supply-chain risk.

Data Center Processor Industry Leaders

-

Intel Corporation

-

NVIDIA Corporation

-

Advanced Micro Devices Inc.

-

Xilinx Inc.

-

Arm Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA locked up Wistron’s AI server capacity through 2026, enabling output of 240,000 Blackwell-based systems each quarter.

- June 2025: South Korea unveiled a USD 1.1 billion GPU initiative led by regional technology firms to bolster domestic AI capabilities.

- June 2025: AMD joined forces with DigitalOcean to introduce cloud GPU services for AI workloads across the provider’s global footprint.

- June 2025: KDDI selected HPE’s platform using NVIDIA Blackwell GPUs for an Osaka facility employing hybrid air-and-liquid cooling.

- May 2025: Saudi Arabia’s DataVolt agreed a USD 20 billion purchase with Supermicro to build AI data centers across the kingdom.

- April 2025: SoftBank finalized a USD 6.5 billion acquisition of Ampere Computing, strengthening its position in ARM-based server processors.

- April 2025: TSMC confirmed a third fab in Arizona valued at more than USD 65 billion, supported by up to USD 6.6 billion in CHIPS Act funding.

- March 2025: Alibaba introduced the XuanTie C930 RISC-V processor for high-performance computing, advancing domestic semiconductor self-sufficiency.

- February 2025: Intel rolled out three Xeon 6 models, including the 128-core 6980P that debuted as host CPU in NVIDIA’s DGX B300 AI system.

- February 2025: Japan approved USD 4.9 billion in incentives for TSMC’s second Kumamoto facility targeted at 6-nm production.

Global Data Center Processor Market Report Scope

A data center processor is a key component of a computing infrastructure. It is a high-performance chip that performs various tasks, including arithmetic, logic, and input/output operations.

The data center processor market is segmented by processor type (CPU [central processing Unit], GPU [graphics processing unit], FPGA [field-programmable gate array], ASIC [application-specific integrated circuit] only ai-dedicated accelerators, and networking accelerators [Smart NIC and DPUs]), application (artificial intelligence [deep learning & machine learning], data analytics/graphics, and high-performance computing [HPC]/scientific computing), and geography (North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America). The report offers the market size and forecasts for all the above segments in value (USD).

| CPU (x86, ARM, RISC-V) |

| GPU |

| FPGA |

| ASIC (AI-Dedicated Accelerators) |

| SmartNIC/Data-Processing Units (DPUs) |

| Artificial Intelligence/Deep Learning |

| Data Analytics and Graphics |

| High-Performance Computing (HPC)/Scientific |

| Network and Storage Offload |

| Cloud-Native Workloads |

| On-Premise Enterprise Data Centers |

| Colocation Facilities |

| Hyperscale Cloud Data Centers |

| Edge/Micro Data Centers |

| IT and Telecommunications |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Manufacturing and Industrial |

| Retail and E-Commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Processor Type | CPU (x86, ARM, RISC-V) | ||

| GPU | |||

| FPGA | |||

| ASIC (AI-Dedicated Accelerators) | |||

| SmartNIC/Data-Processing Units (DPUs) | |||

| By Application | Artificial Intelligence/Deep Learning | ||

| Data Analytics and Graphics | |||

| High-Performance Computing (HPC)/Scientific | |||

| Network and Storage Offload | |||

| Cloud-Native Workloads | |||

| By Deployment Model | On-Premise Enterprise Data Centers | ||

| Colocation Facilities | |||

| Hyperscale Cloud Data Centers | |||

| Edge/Micro Data Centers | |||

| By End-User Industry | IT and Telecommunications | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Manufacturing and Industrial | |||

| Retail and E-Commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the data center processor market?

The data center processor market stands at USD 12.91 billion in 2025 and is projected to reach USD 18.67 billion by 2030.

Which processor category is growing the fastest?

GPUs record the highest growth at a 12.5% CAGR because AI training and inference workloads demand massively parallel architectures.

Why are edge data centers important for processors?

Edge facilities support latency-sensitive AI inference and offer power-efficient micro footprints, driving a 14.8% CAGR in edge deployments.

How do export controls affect processor supply?

Restrictions on advanced AI chips to China disrupt global supply chains and encourage domestic alternatives, trimming the market CAGR by an estimated 0.9%.

Which region is expanding fastest in processor adoption?

Asia-Pacific leads with an 8.2% CAGR, underpinned by government subsidies for local semiconductor manufacturing and large-scale AI investments.

What cooling technologies are data centers adopting for high-density processors?

Operators increasingly deploy direct-to-chip and immersion liquid cooling, replacing legacy air systems that cannot manage racks exceeding 100 kW.

Page last updated on: