| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 92.33 Billion |

| Market Size (2030) | USD 221.08 Billion |

| CAGR (2025 - 2030) | 19.08 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Cyber Warfare Market Analysis

The Cyber Warfare Market size is estimated at USD 92.33 billion in 2025, and is expected to reach USD 221.08 billion by 2030, at a CAGR of 19.08% during the forecast period (2025-2030).

The cyber warfare landscape has evolved significantly, with attacks becoming increasingly sophisticated and diverse in their targeting approach. According to recent data, the distribution of detected cyber threats worldwide in 2022 revealed ransomware as the dominant threat vector at 68.42%, followed by network breaches at 18.42% and data exfiltration at 3.95%. This trend highlights the growing complexity of cyber threats and the need for advanced warfare solutions that can address multiple attack vectors simultaneously. The financial sector remains particularly vulnerable, with financial institutions experiencing 173 basic web application attacks between November 2021 and October 2022, followed by the information technology and professional services sectors with 121 and 113 attacks, respectively.

The integration of advanced technologies like artificial intelligence, machine learning, and blockchain is revolutionizing cyber warfare capabilities. Organizations are increasingly adopting these technologies to enhance their defensive and offensive cyber operations, enabling more sophisticated threat detection, automated response mechanisms, and improved resilience against evolving cyber threats. This technological evolution has led to the emergence of new startups offering innovative solutions, as evidenced by Safe Security's USD 50 million Series B funding round in April 2023, focusing on real-time, data-driven platforms for managing and mitigating cyber risks.

Global regulatory frameworks and cyber security initiatives are reshaping the market landscape. In March 2023, the Biden Administration launched an updated National Cybersecurity Strategy to secure a safe digital ecosystem, emphasizing stronger cyber security regulation and increased counter-hacking activity. Similarly, the European Union has introduced new regulations establishing common cyber and information security measures across its institutions, while the UK government announced a £2.6 billion investment in cyber and legacy IT systems to maintain its position at the forefront of cybersecurity innovation.

The industry faces significant workforce challenges amid rising threat levels. According to a survey by the Center for Internet Security, state and local governments experienced a 148% increase in malware attacks and a 51% rise in ransomware incidents during the first eight months of 2023. In response, governments are implementing comprehensive workforce development initiatives, such as the July 2023 launch of the US National Cyber Workforce and Education Strategy, aimed at addressing immediate and long-term cyber workforce needs. The UK government's February 2023 announcement of an £18.9 million investment in Northern Ireland's cyber security industry further demonstrates the global focus on developing skilled cybersecurity professionals.

Cyber Warfare Market Trends

Increasing Concerns Regarding National Security

Critical infrastructure safety has become a paramount concern with growing digitalization, as cybersecurity and other risks pose continuous threats to key technologies and systems required for essential services like energy, food, electricity, and healthcare. The severity of these threats is evident from recent high-profile incidents. In July 2023, 12 Norwegian ministries were hit with a cyber attack linked to Russia's state hackers, while in February 2023, the US Marshals Service faced a major ransomware attack that compromised sensitive law enforcement materials and potential federal investigation targets. These incidents have prompted governments worldwide to strengthen their cyber defense frameworks, with 36 governments and the European Union establishing the International Counter Ransomware Task Force in January 2023 to combat ransomware attacks threatening national security.

The escalating nature of national security threats has led to substantial governmental investments in cybersecurity measures. In 2022, the US Department of Homeland Security allocated $2.4 billion for cybersecurity, while the Department of Justice invested $1.2 billion in protecting critical systems. Furthermore, regulatory frameworks are being enhanced to address these challenges. The European Union's NIS2 Network and Information Security Directive, which entered into force in January 2023, introduces strict requirements for 'essential undertakings' including energy providers, transport operators, and healthcare services. These organizations will be subject to rigorous regulation, including potential site inspections and specifically targeted independent security audits, with EU countries having until October 2024 to comply with the new rules.

Understand The Key Trends Shaping This Market

Download PDF

Increase in Defense Spending

The surge in defense spending has emerged as a crucial driver for the cyber warfare market, particularly as nations recognize military cybersecurity's critical role in maintaining military superiority and protecting national interests. According to SIPRI data, global military expenditure reached an unprecedented $2.24 trillion in 2022, with major powers like the United States ($877 billion), China ($292 billion), and Russia ($86.4 billion) leading the investments. This increased spending has directly translated into enhanced cybersecurity budgets. For instance, the United States announced new spending plans for fiscal year 2023 that included $15.6 billion specifically for defending against cyber threats, with the Department of Defense receiving $11.2 billion of this allocation.

The investment momentum continues to build across various regions, with governments implementing comprehensive funding programs for cyber defense solutions. The United Kingdom demonstrated this commitment in December 2022 by announcing a £2.6 billion investment in cyber and legacy IT systems over three years, including significant funding for the National Cyber Force. Similarly, Australia's Federal budget 2023-2024 allocated over AUD 2 billion for digital solutions, modernizing outdated legacy platforms, and IT systems. These investments reflect a growing recognition that traditional military capabilities must be complemented by robust cyber warfare capabilities, particularly as state-sponsored cyber attacks become more sophisticated and frequent. The trend is further evidenced by the US Department of Homeland Security's August 2023 announcement of $374.9 million in grant funding for the State and Local Cybersecurity Grant Program, marking a significant increase from the previous year's allocation.

Segment Analysis: By End-User Industry

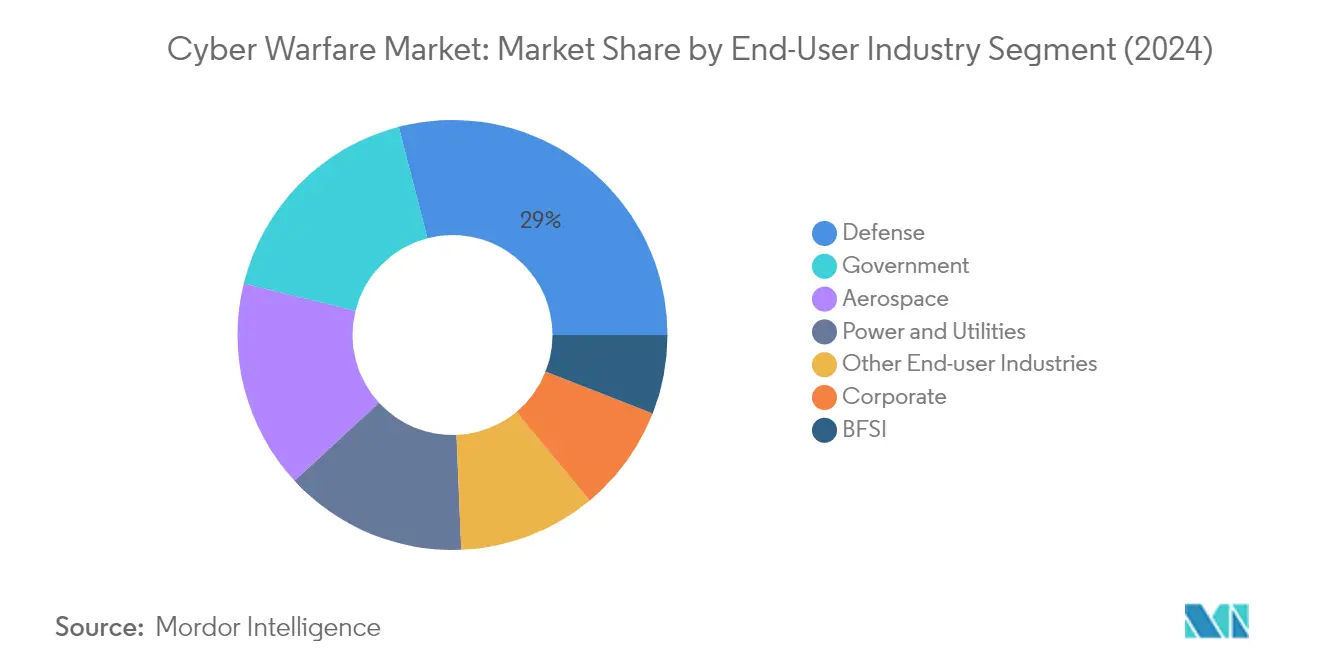

Defense Segment in Cyber Warfare Market

The defense segment continues to dominate the global cyber warfare market, commanding approximately 29% market share in 2024, equivalent to USD 22.24 billion. This significant market position is driven by the increasing prioritization of cyber defense capabilities within military organizations worldwide. The defense sector's dominance is reinforced by substantial investments in digital security units aimed at moderating and deterring potential risks from state-sponsored cyber threats. The rise of innovations and the Internet of Things (IoT) integration in defense operations has emerged as a crucial driving factor for implementing cyber warfare frameworks in this sector. Military organizations are increasingly focusing on protecting intellectual property and safeguarding critical systems that monitor and control national defense capabilities. The development of new technologies such as unmanned vehicles and hypersonic weapons, which are highly dependent on data and connectivity, has further accelerated the need for robust cyber warfare solutions in the defense sector.

Government Segment in Cyber Warfare Market

The government segment is projected to exhibit the highest growth rate of approximately 22% during the forecast period 2024-2029. This accelerated growth is attributed to the increasing digitization initiatives by governments worldwide to enhance service transparency and accessibility for citizens. The sector faces persistent challenges from sophisticated cyber threats, necessitating continuous updates to cybersecurity solutions to protect critical infrastructure and sensitive citizen data. Cloud security has become a key priority as government sectors increasingly migrate to cloud-based systems, driving the adoption of advanced encryption, multi-factor authentication, and network segmentation technologies. The implementation of comprehensive collaboration suites and their cloud-based capabilities has created additional demand for robust cyber warfare solutions. Government agencies are adopting a proactive approach to cybersecurity by investing in new technologies, focusing on incident response planning, and strengthening supply chain security measures.

Remaining Segments in End-User Industry

The cyber warfare market encompasses several other vital segments, including aerospace, BFSI, corporate, power and utilities, and other end-user industries. The aerospace sector plays a crucial role due to its heavy reliance on digital technology across flight operations and air traffic control systems. The BFSI sector demonstrates significant demand driven by the digitalization of banking services and increasing regulatory requirements. The corporate segment continues to evolve with the adoption of IoT devices and digital transformation initiatives. The power and utilities sector maintains strategic importance due to the critical nature of infrastructure protection and the increasing integration of smart grid technologies. These segments collectively contribute to the market's dynamic growth, each bringing unique security requirements and challenges that shape the evolution of cyber warfare solutions.

Cyber Warfare Market Geography Segment Analysis

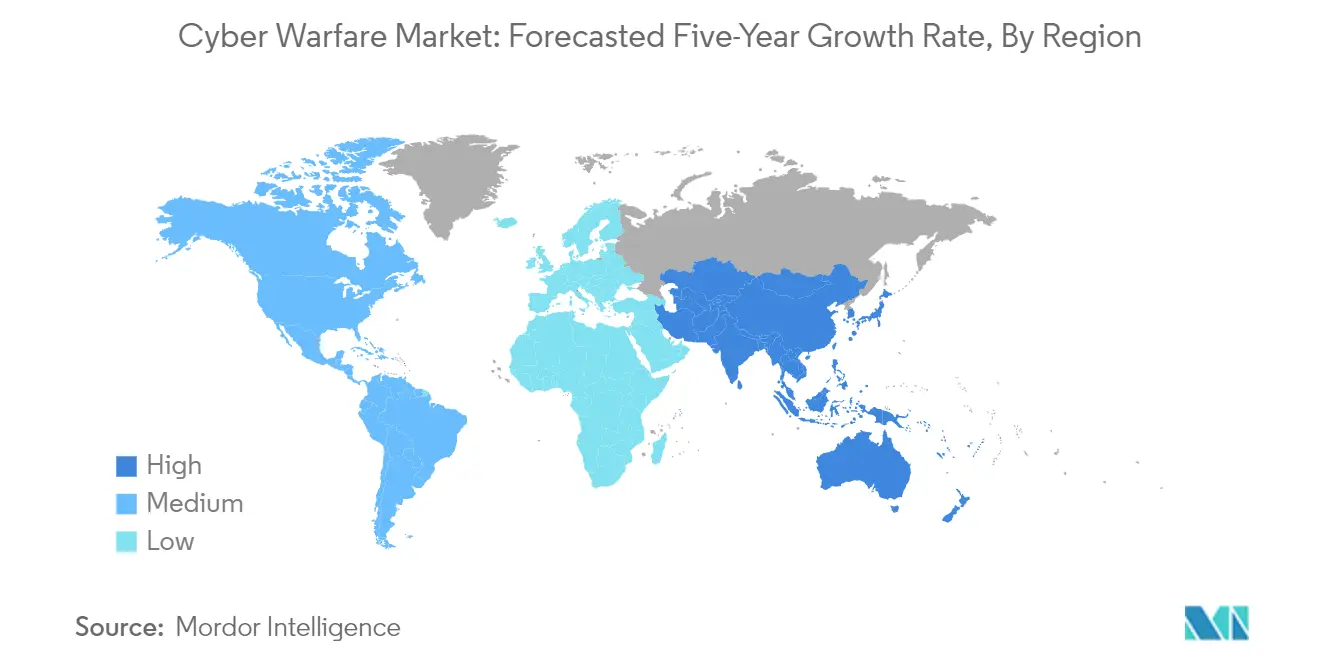

Cyber Warfare Market in North America

North America continues to dominate the global cyber warfare market, commanding approximately 35% of the total market share in 2024. The region's leadership position is primarily driven by substantial investments in cybersecurity infrastructure across defense, government, and private sectors. The digitalization trends in public and private sector organizations in the USA and Canada are increasing the vulnerability of the region's digital infrastructures, which has accelerated the adoption of sophisticated cyber warfare solutions. The region's market is characterized by robust government initiatives, particularly in strengthening national cyber defense capabilities through strategic investments and regulatory frameworks. The BFSI sector has emerged as a significant contributor to market growth, with financial institutions prioritizing their cybersecurity strategies to combat increasing cyber threats. Commercial banks and government regulators have been implementing advanced cybersecurity protocols, while the aerospace sector's growing digital transformation has further amplified the demand for comprehensive cyber warfare solutions. The presence of major market vendors and continuous technological innovations has reinforced North America's position as the epicenter of global cyber warfare capabilities.

Cyber Warfare Market in Europe

The European cyber warfare market has demonstrated robust growth, with an estimated growth rate of approximately 17% during 2019-2024. The region's market dynamics are significantly influenced by the increasing prioritization of cyber defense mechanisms across defense, government, and finance sectors, particularly in countries like the United Kingdom, Germany, and France. The European Union's comprehensive approach to cybersecurity, including various policy initiatives and funding programs, has created a strong foundation for market growth. The defense sector has emerged as a crucial contributor to market expansion, with countries increasingly investing in advanced cyber warfare capabilities. The region's market is characterized by strategic partnerships between major industry players and continuous technological innovations in cyber defense solutions. The integration of cyber warfare capabilities into traditional defense frameworks has become a key focus area for European nations, supported by collaborative initiatives through organizations like NATO. The emphasis on protecting critical infrastructure and financial systems has led to increased adoption of sophisticated cyber warfare solutions across various sectors.

Cyber Warfare Market in Asia-Pacific

The Asia-Pacific cyber warfare market is positioned for exceptional growth, with a projected growth rate of approximately 22% during 2024-2029. The region's market is experiencing rapid transformation driven by accelerated digital adoption across government and private sectors, particularly in countries like China, India, Japan, Singapore, South Korea, and Taiwan. The increasing focus on national cybersecurity and digital sovereignty has led to substantial investments in cyber warfare capabilities. The industrial sector's prominence in countries like Taiwan, China, and Vietnam has made the region particularly vulnerable to cyber espionage and intellectual property theft, driving the demand for advanced cyber warfare solutions. The government sector has emerged as a significant market driver, with various countries implementing comprehensive cybersecurity frameworks and regulations. The rapid adoption of digital technologies across various sectors, coupled with increasing cyber threats, has created a robust environment for market expansion. The region's growing emphasis on developing indigenous cyber warfare capabilities and the presence of emerging technology hubs have positioned Asia-Pacific as a crucial market for cyber warfare solutions.

Cyber Warfare Market in Latin America

The Latin American cyber warfare market is experiencing significant transformation driven by the evolving digital landscape in countries like Argentina, Mexico, and Brazil. The region's market is characterized by increasing vulnerabilities in digital infrastructure across government and private enterprises, necessitating robust cyber warfare solutions. The BFSI sector has emerged as a key growth driver, with the digitalization of banking services creating new security challenges and opportunities. The market is witnessing increased participation from global technology service providers and advisory companies, who are expanding their cyber defense capabilities through strategic investments and acquisitions. The government and defense sectors are showing growing awareness of cyber threats, leading to increased investments in cybersecurity infrastructure. The region's market is also benefiting from partnerships between local and international cybersecurity firms, enabling knowledge transfer and technological advancement. The increasing adoption of digital transformation initiatives across various sectors has created a strong foundation for the growth of cyber warfare solutions in Latin America.

Cyber Warfare Market in Middle East and Africa

The Middle East and Africa cyber warfare market is witnessing substantial growth driven by increasing digitalization initiatives and cybersecurity concerns. The region's market is particularly dynamic in countries like Saudi Arabia, UAE, and South Africa, where government-led digital transformation programs are creating new opportunities for cyber warfare solutions. The oil and gas sector's critical infrastructure protection needs have emerged as a significant driver for market growth, especially in Gulf countries. The implementation of comprehensive cybersecurity strategies by governments across the region has created a strong foundation for market expansion. The banking and financial services sector is increasingly adopting advanced cyber warfare solutions to protect against sophisticated cyber threats. The region's market is characterized by growing investments in cybersecurity education and training programs to develop local talent pools. The emphasis on protecting critical national infrastructure and the increasing adoption of smart city initiatives have further accelerated the demand for advanced cyber warfare solutions across the region.

Get Analysis on Important Geographic Markets

Download PDF

Cyber Warfare Industry Overview

Top Companies in Cyber Warfare Market

The cyber warfare market features prominent players including BAE Systems, Boeing, General Dynamics, Lockheed Martin, Raytheon Technologies, Mandiant (now part of Google Cloud), Leonardo, Booz Allen Hamilton, DXC Technology, and Airbus SE. These cyber warfare companies are driving innovation through advanced AI and machine learning integration into their cyber defense solutions, while also focusing on developing quantum-resistant cryptography systems. The industry witnesses continuous product development in areas like threat intelligence, automated defense mechanisms, and cyber resilience frameworks. Companies are demonstrating operational agility by establishing dedicated cybersecurity divisions and innovation labs, while also pursuing strategic partnerships with technology firms and government agencies. Market expansion strategies include geographic diversification into emerging markets, particularly in the Asia-Pacific and Middle East regions, alongside investments in building comprehensive cyber warfare capabilities through both organic growth and strategic acquisitions.

Market Dominated by Defense Technology Conglomerates

The cyber warfare market structure is characterized by the dominance of large defense and aerospace conglomerates that leverage their established relationships with government agencies and military organizations. These major players possess extensive research and development capabilities, sophisticated technological infrastructure, and deep integration with national security frameworks. The market demonstrates moderate consolidation, with leading companies controlling significant market share through their comprehensive solution portfolios spanning hardware, software, and services. The competitive landscape is further shaped by the presence of specialized cybersecurity firms that bring focused expertise in specific areas such as threat intelligence, incident response, and digital forensics.

The market is witnessing active merger and acquisition activity as established players seek to enhance their technological capabilities and expand their service offerings. Large defense contractors are particularly focused on acquiring innovative cybersecurity startups and specialized firms to strengthen their position in emerging technology areas like AI-driven threat detection and quantum computing security. Strategic partnerships and collaborations between defense prime contractors and technology companies are becoming increasingly common, creating an ecosystem that combines traditional defense expertise with cutting-edge digital capabilities.

Innovation and Adaptability Drive Market Success

Success in the cyber warfare market increasingly depends on companies' ability to maintain technological leadership while demonstrating agility in responding to evolving threats. Incumbent players are focusing on developing proprietary technologies, investing in research and development, and building strong intellectual property portfolios to maintain their competitive advantage. Market leaders are also emphasizing the importance of building long-term relationships with government clients while expanding their presence in the commercial sector. Companies are increasingly adopting platform-based approaches that allow for rapid integration of new capabilities and technologies, while also focusing on developing specialized solutions for specific industry verticals.

For new entrants and challenger firms, success strategies center around identifying and exploiting niche market segments, developing innovative solutions that address specific cybersecurity challenges, and building strong partnerships with established players. The market's high barriers to entry, particularly in terms of security clearances and compliance requirements, make strategic partnerships crucial for growth. Regulatory frameworks, particularly those related to national security and data protection, continue to shape market dynamics and create opportunities for companies that can effectively navigate complex compliance requirements. The concentration of end-users in government and defense sectors necessitates a strong focus on building credibility and establishing track records in handling sensitive projects.

Cyber Warfare Market Leaders

-

BAE Systems PLC

-

The Boeing Company

-

General Dynamics Corporation

-

Lockheed Martin Corporation

-

Raytheon Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Cyber Warfare Market News

- May 2024 - Fortinet contributed to NATO's annual Exercise Locked Shields, a premier cyber warfare event. This exercise was recognized as the world's largest and most intricate live-fire cyber-defense event. It aimed to enhance the cyber-warfare skills of cybersecurity professionals from allied nations. Participants exchange optimal strategies to safeguard their national IT systems and critical infrastructure during live cyberattacks.

- August 2023 - The Department of Homeland Security announced the availability of USD 374.9 million in grant funding for the FY 2023 State and Local Cybersecurity Grant Program (SLCGP). In its second year, the SLCGP became a cybersecurity grant program for state, local, and territorial (SLT) governments across the nation and helped them strengthen their cyber resilience. The funding allotment for FY 2023 represented a significant increase from the USD 185 million allotted in FY 2022.

Cyber Warfare Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Concerns Regarding National Security

- 5.1.2 Increase in Defense Spending

-

5.2 Market Challenges

- 5.2.1 Lack of Cyber Warfare Professionals

6. MARKET SEGMENTATION

-

6.1 By End-user Industry

- 6.1.1 Defense

- 6.1.2 Aerospace

- 6.1.3 BFSI

- 6.1.4 Corporate

- 6.1.5 Power and Utilities

- 6.1.6 Government

- 6.1.7 Other End-user Industries

-

6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 BAE Systems PLC

- 7.1.2 The Boeing Company

- 7.1.3 General Dynamic Corporation

- 7.1.4 Lockheed Martin Corporation

- 7.1.5 Raytheon Technologies Corporation

- 7.1.6 Mandiant Inc. (fireeye Inc.)

- 7.1.7 Leonardo SpA

- 7.1.8 Booz Allen Hamilton Inc.

- 7.1.9 DXC Technology Company

- 7.1.10 Airbus SE

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report Asia, Australia and New Zealand will be studied together as Asia Pacific.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Cyber Warfare Industry Segmentation

Cyberwarfare comprises the actions taken by a nation-state or international organizations against another nation's computers or information networks, primarily through computer viruses or denial-of-service (DDoS) attacks.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from the various solutions that are being used across end-user industries. In addition, the study provides the global cyber warfare market trends, along with key vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

The cyber warfare market is segmented by end-user industry (defense, aerospace, BFSI, corporate, power and utilities, government, and other end-user industries) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By End-user Industry | Defense |

| Aerospace | |

| BFSI | |

| Corporate | |

| Power and Utilities | |

| Government | |

| Other End-user Industries | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Cyber Warfare Market Research FAQs

How big is the Cyber Warfare Market?

The Cyber Warfare Market size is expected to reach USD 92.33 billion in 2025 and grow at a CAGR of 19.08% to reach USD 221.08 billion by 2030.

What is the current Cyber Warfare Market size?

In 2025, the Cyber Warfare Market size is expected to reach USD 92.33 billion.

Who are the key players in Cyber Warfare Market?

BAE Systems PLC, The Boeing Company, General Dynamics Corporation, Lockheed Martin Corporation and Raytheon Technologies Corporation are the major companies operating in the Cyber Warfare Market.

Which is the fastest growing region in Cyber Warfare Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Cyber Warfare Market?

In 2025, the North America accounts for the largest market share in Cyber Warfare Market.

What years does this Cyber Warfare Market cover, and what was the market size in 2024?

In 2024, the Cyber Warfare Market size was estimated at USD 74.71 billion. The report covers the Cyber Warfare Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Cyber Warfare Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Cyber Warfare Market Research

Mordor Intelligence provides a comprehensive analysis of the cyber warfare market. We leverage extensive expertise in cyber security and electronic warfare research. Our detailed report examines the evolving landscape of cyber operations and cyber intelligence. It includes critical aspects of cyber espionage and military cyber security. The analysis covers emerging cyber weapons technologies and cyber defense strategies. It also highlights the growing significance of the digital battlespace. This provides stakeholders with crucial insights into information warfare dynamics and network warfare capabilities.

The report is available in an easy-to-read PDF format for download. It offers stakeholders valuable intelligence on cyber defense solutions and cyber countermeasures. Our analysis covers key aspects of cyber command and control systems and cyber deterrence strategies. It also explores developments in the cyber battlefield. The research provides detailed insights into cyber warfare companies and their technological innovations. It examines future trends in cyber warfare and their impact on the cyber security industry. Stakeholders benefit from our thorough assessment of digital warfare technologies and emerging cyber weapons market opportunities. This is supported by extensive data and expert analysis of the evolving cyber security market.