| Study Period | 2024 - 2030 |

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 1.01 Billion |

| CAGR (2025 - 2030) | 7.18 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Crew Oxygen Systems Market Analysis

The Crew Oxygen Systems Market size is estimated at USD 0.71 billion in 2025, and is expected to reach USD 1.01 billion by 2030, at a CAGR of 7.18% during the forecast period (2025-2030).

The global aviation industry is experiencing significant transformation driven by fleet modernization initiatives and technological advancements in aircraft safety systems. Major aircraft manufacturers have ramped up their production capabilities to meet growing demand, with Airbus and Boeing delivering 735 and 528 aircraft, respectively, in 2023, demonstrating robust industry recovery. The integration of advanced materials and smart technologies in aircraft oxygen systems components has become increasingly prevalent, with manufacturers focusing on lightweight materials and sensor-based monitoring systems. The aviation sector's emphasis on operational efficiency and safety has led to increased investment in next-generation aviation oxygen systems and components.

The military aviation sector continues to shape market dynamics through extensive modernization programs and technological upgrades. Global defense spending has shown substantial growth, with countries like China reaching USD 292 billion in 2022, marking a 4.3% increase from the previous year. Advanced military aircraft programs are driving innovation in oxygen delivery systems, particularly for high-altitude operations and extended mission durations. The development of sophisticated oxygen generation and delivery systems has become crucial for modern military aircraft, especially in response to evolving mission requirements and operational scenarios.

The industry has witnessed significant consolidation and strategic partnerships aimed at enhancing technological capabilities and market reach. In June 2023, Safran's acquisition of Air Liquide's aeronautical oxygen and nitrogen activities demonstrates the industry's focus on expanding product portfolios and technological expertise. The emergence of new market players and increased competition has led to accelerated innovation in crew oxygen system design and functionality, particularly in areas such as smart monitoring systems and integrated safety features.

The regulatory landscape continues to evolve with an enhanced focus on aircraft safety systems and certification requirements. International aviation authorities have implemented stringent safety standards for oxygen systems, influencing product development and certification processes. The industry has seen increased emphasis on sustainable manufacturing practices and environmentally conscious design approaches, with manufacturers exploring eco-friendly materials and energy-efficient production methods. Recent technological developments include the integration of IoT capabilities for real-time monitoring and predictive maintenance of aircraft oxygen systems, enhancing overall safety and operational efficiency.

Crew Oxygen Systems Market Trends

Surge in Commercial Flight Numbers to Increase the Demand for Oxygen Systems

The significant increase in global commercial flights has become a primary catalyst for the crew oxygen systems market. According to industry data, global passenger traffic witnessed remarkable growth, with international air traffic rebounding to 95.6% of pre-pandemic levels by July 2023. This surge in air travel has prompted airlines worldwide to expand their fleets, directly impacting the demand for essential safety equipment like aircraft oxygen systems. For instance, major aircraft manufacturers have responded to this increased demand, with Airbus delivering 735 aircraft and Boeing delivering 528 aircraft in 2023, representing significant increases from their 2022 deliveries of 663 and 480 aircraft, respectively.

The expansion of commercial aviation has led to substantial aircraft procurement programs by major airlines globally. In December 2023, United Airlines signed a contract worth USD 43 billion with Boeing for the procurement of 200 commercial aircraft, including 100 Boeing 787 Dreamliners and 100 737 MAXs. Similarly, EasyJet contracted Airbus for 157 more A320neo aircraft in December 2023, along with 100 purchase rights. These large-scale orders demonstrate the industry's robust growth trajectory and directly correlate with increased demand for crew oxygen systems, as each new aircraft requires comprehensive oxygen delivery systems for crew safety. The production rate of aircraft has also seen steady growth, with Airbus maintaining an A320 production rate of 45 aircraft per month since late 2021, and achieving an average monthly delivery of 48 A320s in 2023 compared to 43 in 2022.

Understand The Key Trends Shaping This Market

Download PDF

Stringent Safety Regulations and Increased Focus on Crew Safety to Drive the Market

The aviation industry's heightened emphasis on crew safety, coupled with stringent regulatory requirements, continues to be a significant driver for the aircraft oxygen systems market. The International Civil Aviation Organization (ICAO) Standards and Recommended Practices (SARPs) provide comprehensive guidelines for supplemental and emergency oxygen systems, establishing different requirements for pressurized and non-pressurized aircraft based on operational altitudes. These regulations mandate that the total number of oxygen delivery units must exceed the number of passenger and cabin crew seats by at least 10 percent in pressurized aircraft, ensuring redundancy and maximum safety during emergencies.

The industry has witnessed significant technological advancements in response to these safety requirements. In June 2022, Diehl Aviation introduced its own emergency oxygen supply generator for onboard passenger aircraft, which can be installed and retrofitted in all Airbus A320 family and Boeing B737 series aircraft. Additionally, recent innovations have focused on improving oxygen system efficiency and reliability. For instance, in 2023, Mission Systems received a USD 12 million contract to redesign and upgrade the existing onboard oxygen system GGU-12+ oxygen concentrator for the Australian F/A-18F program, highlighting the industry's commitment to enhancing crew safety through advanced oxygen delivery systems. These developments demonstrate how safety regulations continue to drive innovation and investment in pilot oxygen systems, ensuring airlines maintain the highest safety standards for their flight crews. Furthermore, the integration of OBOGS (On-Board Oxygen Generation Systems) in modern aircraft underscores the industry's focus on cutting-edge solutions for crew safety.

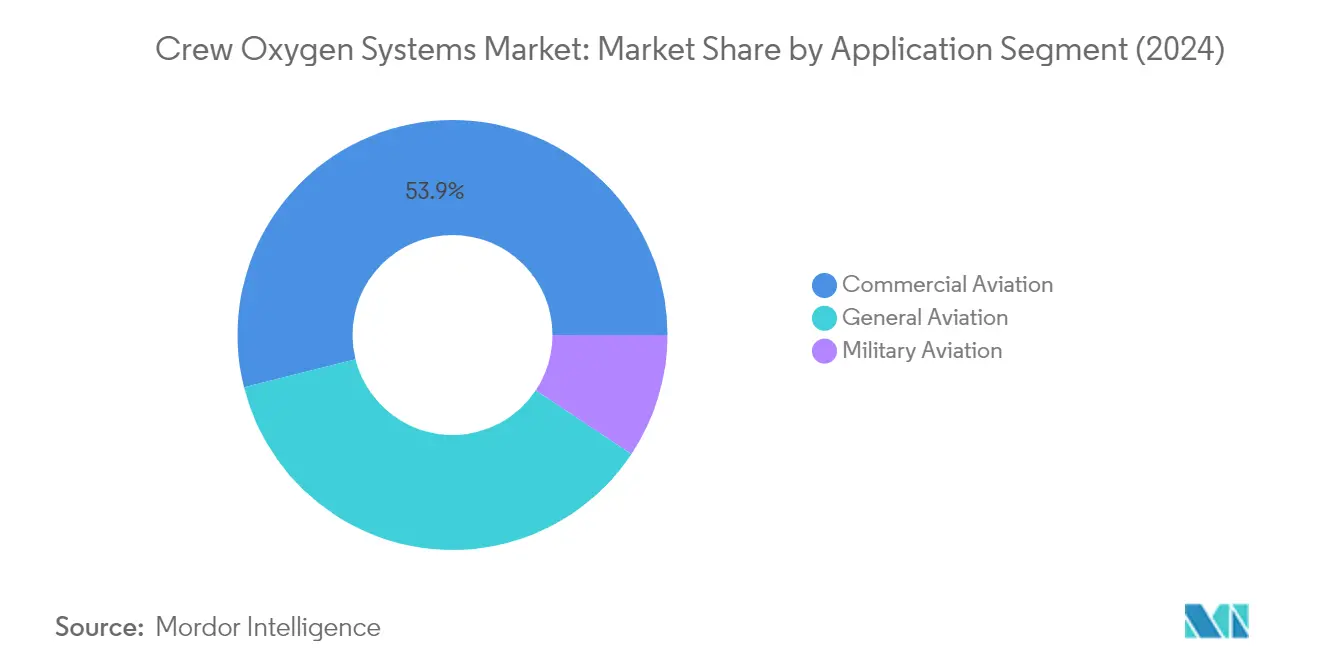

Segment Analysis: By Application

Commercial Aviation Segment in Crew Oxygen Systems Market

Commercial aviation dominates the crew oxygen systems market, commanding approximately 54% market share in 2024, driven by stringent safety regulations and the massive scale of commercial air operations. The segment's dominance is reinforced by major airlines' fleet expansion initiatives and the increasing focus on crew safety across international routes. Leading aircraft manufacturers like Airbus and Boeing are incorporating advanced aircraft oxygen systems in their new deliveries, with Airbus delivering 735 aircraft and Boeing delivering 528 aircraft in 2023. The growth in this segment is further supported by the recovery in global air traffic, with IATA reporting that global passenger traffic rebounded to 95.6% of pre-pandemic levels by July 2023. Airlines worldwide are prioritizing crew safety systems as part of their operational protocols, particularly for long-haul flights where reliable oxygen systems are crucial for both routine operations and emergency scenarios.

Military Aviation Segment in Crew Oxygen Systems Market

The military aviation segment is projected to exhibit the highest growth rate in the crew oxygen systems market during 2024-2029, with an expected CAGR of approximately 7%. This accelerated growth is primarily driven by increasing defense modernization programs across major military powers and the rising demand for advanced fighter aircraft with sophisticated life support systems. The segment's growth is further bolstered by technological advancements in oxygen generation systems, particularly in onboard oxygen generation systems (OBOGS) for high-performance military aircraft. Recent developments include significant military aircraft procurement programs, such as the F-35 program, which incorporates state-of-the-art oxygen systems. The emphasis on pilot safety and performance in extreme conditions, coupled with the increasing number of military aircraft orders worldwide, continues to drive innovation and investment in advanced oxygen systems for military applications.

Remaining Segments in Crew Oxygen Systems Market by Application

The general aviation segment represents a significant portion of the crew oxygen systems market, catering to business jets, private aircraft, and specialized aviation operations. This segment is characterized by its unique requirements for flexible and customizable oxygen systems that can accommodate varying flight profiles and passenger configurations. The segment benefits from the growing adoption of private aviation for business travel and the increasing number of high-net-worth individuals investing in private aircraft. Manufacturers are developing specialized oxygen systems for this segment that offer both reliability and convenience, with features such as portable oxygen solutions and integrated systems designed specifically for smaller aircraft operations.

Segment Analysis: By Component

Oxygen Storage Systems Segment in Crew Oxygen Systems Market

The oxygen storage systems segment dominates the crew oxygen systems market, commanding approximately 60% of the total market share in 2024. This significant market position is attributed to the critical role these systems play in storing and maintaining oxygen supplies aboard aircraft. The segment's dominance is reinforced by stringent safety regulations requiring reliable oxygen storage solutions across commercial, military, and general aviation sectors. Major manufacturers like Safran and Collins Aerospace have continued to innovate in this space, developing advanced storage solutions that offer improved capacity, reliability, and integration capabilities with modern aircraft systems. The segment's strong performance is further supported by the increasing focus on passenger and crew safety, particularly in long-haul flights and high-altitude operations where dependable oxygen storage is essential.

Oxygen Delivery Systems Segment in Crew Oxygen Systems Market

The oxygen delivery systems segment is projected to demonstrate robust growth during the forecast period 2024-2029. This growth is driven by technological advancements in oxygen delivery mechanisms, including the development of more efficient and reliable distribution systems. The segment is benefiting from increased investments in smart delivery solutions that incorporate sensors and monitoring capabilities, enabling real-time tracking of oxygen flow and system performance. Manufacturers are focusing on developing lightweight and compact delivery systems that maintain high performance while reducing the overall weight impact on aircraft. The integration of advanced materials and innovative design approaches is expected to further enhance the efficiency and reliability of oxygen delivery systems, making them increasingly essential components in modern aircraft oxygen systems.

Remaining Segments in Crew Oxygen Systems Market

The oxygen mask segment, while smaller in market share, plays a vital role in the overall crew oxygen systems ecosystem. This segment encompasses various types of masks designed for different aviation applications, from quick-donning crew masks to specialized military aviation masks. The segment's development is characterized by ongoing innovations in mask design, focusing on improved comfort, communication capabilities, and emergency response features. Manufacturers are incorporating advanced materials and ergonomic designs to enhance user comfort during extended wear periods, while also ensuring optimal oxygen delivery efficiency. The segment continues to evolve with the integration of features such as built-in microphones and enhanced sealing technologies to meet the diverse requirements of modern aviation operations. Additionally, the development of supplemental oxygen systems is becoming increasingly important for enhancing safety and comfort in various aviation scenarios.

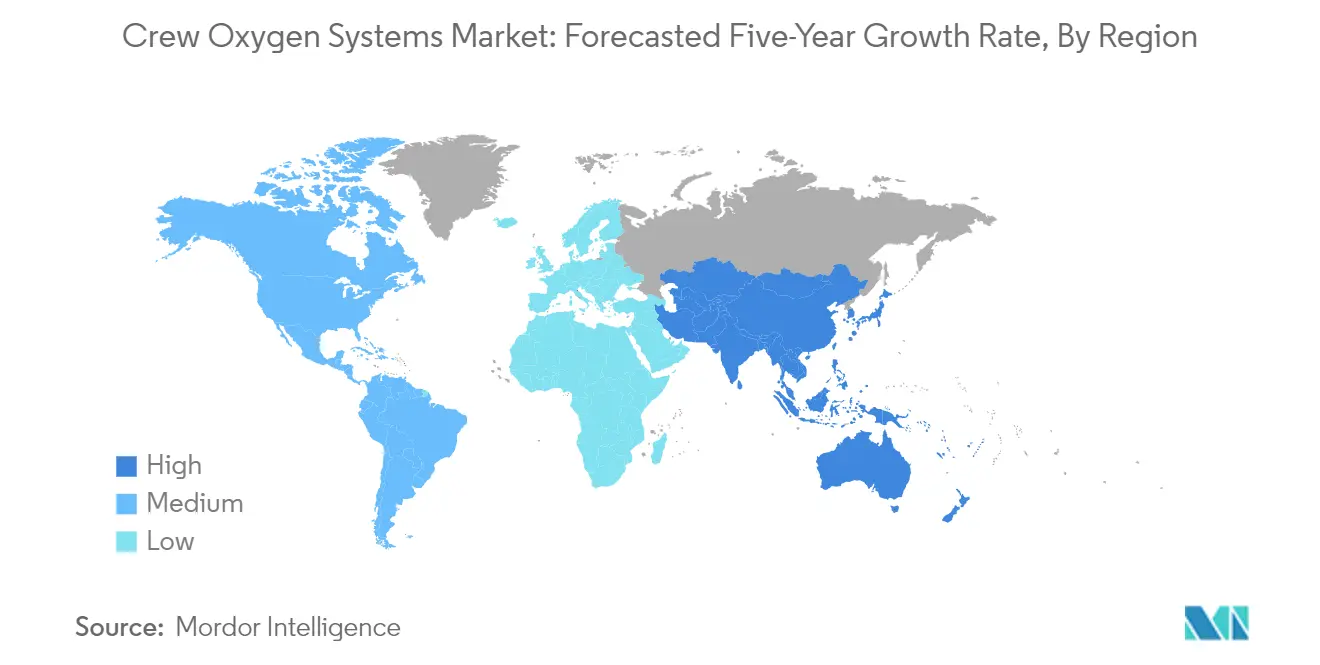

Crew Oxygen Systems Market Geography Segment Analysis

Crew Oxygen Systems Market in North America

North America represents a dominant force in the global crew oxygen systems market, driven by its robust aviation infrastructure and the presence of prominent market players. The region's market dynamics are shaped by significant fleet modernization initiatives across commercial, military, and general aviation sectors. Both the United States and Canada demonstrate strong commitment to aviation safety regulations and continuous technological advancement in aircraft oxygen systems. The presence of major aircraft manufacturers and an increasing focus on passenger safety further strengthens the regional market landscape.

Crew Oxygen Systems Market in United States

The United States leads the North American market with approximately 81% regional market share in 2024. The country's dominance is attributed to its large fleet size, significant investments in defense spending, and stringent safety regulations. The US market is characterized by the presence of major airlines undertaking fleet expansion initiatives and military modernization programs. The Federal Aviation Administration's strict safety mandates regarding crew oxygen systems, coupled with the country's position as a major hub for aircraft manufacturing and maintenance, reinforce its market leadership. The presence of key industry players and ongoing research and development activities in advanced oxygen delivery systems further solidify the US market position.

Crew Oxygen Systems Market Growth Analysis - United States

The United States demonstrates robust growth potential with a projected CAGR of approximately 6% during 2024-2029. This growth trajectory is supported by increasing air passenger traffic, ongoing fleet modernization programs, and rising defense expenditure. The country's emphasis on incorporating advanced safety features in new aircraft deliveries, coupled with the expanding general aviation sector, drives market expansion. The growing focus on developing smart aviation oxygen systems with enhanced monitoring capabilities and the integration of IoT technologies further accelerates market growth. Additionally, the increasing adoption of next-generation aircraft by major airlines contributes to the market's upward trajectory.

Crew Oxygen Systems Market in Europe

Europe maintains a strong position in the crew oxygen systems market, supported by its advanced aerospace industry and stringent safety regulations. The region's market landscape is shaped by countries including the United Kingdom, Germany, France, and Russia, each contributing significantly to market development. The European Union Aviation Safety Agency's comprehensive safety guidelines and the presence of major aircraft manufacturers drive market growth. The region's focus on technological innovation and sustainable aviation solutions influences the development of advanced oxygen delivery systems.

Crew Oxygen Systems Market in United Kingdom

The United Kingdom emerges as the largest market in Europe, commanding approximately 24% of the regional market share in 2024. The country's market leadership is driven by its well-established aerospace industry and the significant presence of key market players. The UK's robust regulatory framework, overseen by the Civil Aviation Authority, ensures high safety standards in aircraft oxygen systems. The country's active participation in international aviation programs and continuous investment in aerospace research and development activities reinforce its market position.

Crew Oxygen Systems Market Growth Analysis - Germany

Germany exhibits the highest growth potential in Europe with a projected CAGR of approximately 6% during 2024-2029. The country's market expansion is driven by its strong aerospace manufacturing base and increasing focus on aviation safety technologies. Germany's commitment to developing advanced aircraft systems, coupled with its significant investments in research and development, supports market growth. The presence of major airlines undertaking fleet modernization initiatives and the country's growing emphasis on military aircraft upgrades further accelerates market development.

Crew Oxygen Systems Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for crew oxygen systems, characterized by rapid aviation sector growth and increasing defense modernization initiatives. Countries including China, India, Japan, and South Korea are key contributors to regional market development. The region's expanding commercial aviation sector, coupled with rising defense expenditure, creates substantial opportunities for market growth. The increasing focus on domestic aircraft manufacturing capabilities and growing emphasis on aviation safety standards shapes the regional market landscape.

Crew Oxygen Systems Market in China

China emerges as the dominant force in the Asia-Pacific region, leading both in market size and growth potential. The country's market leadership is attributed to its rapidly expanding aviation sector and significant investments in aerospace manufacturing capabilities. China's commitment to developing its domestic aviation industry, coupled with increasing defense modernization initiatives, drives market growth. The presence of major airlines undertaking fleet expansion programs and the country's focus on incorporating advanced safety technologies reinforces its market position.

Crew Oxygen Systems Market Growth Analysis - China

China demonstrates exceptional growth potential in the Asia-Pacific region, driven by its ambitious aviation sector development plans and increasing focus on safety technologies. The country's market expansion is supported by substantial investments in aerospace manufacturing capabilities and rising demand for commercial and military aircraft. China's commitment to developing advanced aviation technologies and its growing emphasis on domestic aircraft production capabilities accelerates market growth. The increasing adoption of next-generation aircraft and rising focus on aviation safety standards further supports market development.

Crew Oxygen Systems Market in Latin America

Latin America demonstrates growing potential in the crew oxygen systems market, with Brazil emerging as both the largest and fastest-growing market in the region. The regional market is characterized by increasing air travel demand, fleet modernization initiatives, and a growing focus on aviation safety standards. The presence of major aircraft manufacturers and rising investments in aerospace infrastructure support market development. The region's expanding commercial aviation sector and increasing defense modernization programs create substantial opportunities for market growth.

Crew Oxygen Systems Market in Middle East & Africa

The Middle East & Africa region showcases significant potential in the crew oxygen systems market, with Saudi Arabia leading both in market size and growth rate. The region's market landscape is shaped by countries including Saudi Arabia, United Arab Emirates, and South Africa. The robust expansion of commercial aviation, coupled with significant investments in defense modernization, drives market growth. The region's position as a major aviation hub and increasing focus on incorporating advanced safety technologies in aircraft supports market development.

Get Analysis on Important Geographic Markets

Download PDF

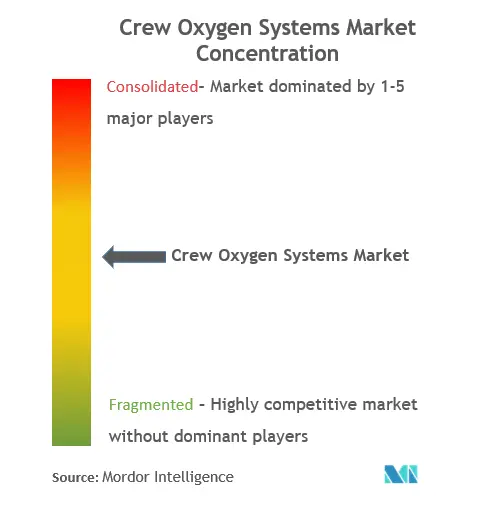

Crew Oxygen Systems Industry Overview

Top Companies in Crew Oxygen Systems Market

The crew oxygen systems market is characterized by intense, innovation-driven competition among established aerospace manufacturers and specialized oxygen system providers. Companies are increasingly focusing on developing lightweight, efficient systems that incorporate advanced materials and smart sensor technologies to enhance performance and safety features. Strategic partnerships and collaborations with airlines and aircraft manufacturers have become crucial for maintaining market position, while operational agility is demonstrated through customized solutions for different aircraft platforms. Market leaders are expanding their geographical presence through distribution networks and service centers, particularly in emerging aviation markets. The emphasis on research and development has led to the introduction of universal oxygen generators and modular storage systems, showcasing the industry's commitment to technological advancement and meeting evolving regulatory requirements.

Consolidated Market Led By Global Players

The crew oxygen systems market exhibits a high degree of consolidation, dominated by large aerospace conglomerates with diverse product portfolios and established relationships with major aircraft manufacturers. These industry leaders, including RTX Corporation, Safran SA, and Parker Hannifin Corporation, leverage their extensive manufacturing capabilities, technical expertise, and global presence to maintain their market positions. The market structure is further strengthened by high entry barriers due to stringent certification requirements and substantial investment needs in research and development.

Recent years have witnessed significant merger and acquisition activities, exemplified by Parker Hannifin's acquisition of Meggitt PLC, which has reshaped the competitive landscape. These strategic moves reflect the industry's trend toward consolidation to achieve economies of scale, expand product offerings, and enhance technological capabilities. Regional players and specialized manufacturers maintain their presence through niche market focus and specialized product offerings, though their market share remains relatively limited compared to global conglomerates.

Innovation and Integration Drive Future Success

Success in the aviation oxygen systems market increasingly depends on manufacturers' ability to integrate advanced technologies while maintaining cost competitiveness. Incumbent players must focus on developing next-generation aircraft oxygen systems that offer improved efficiency, reduced weight, and enhanced safety features while meeting stringent regulatory requirements. The ability to provide comprehensive aftermarket support, including maintenance services and rapid spare parts availability, has become crucial for maintaining customer relationships and market share.

For contenders seeking to gain ground, specialization in specific aircraft segments or focusing on innovative solutions for emerging aviation needs presents viable opportunities. The market's future trajectory is influenced by the concentrated nature of end-users, primarily commercial airlines and military operators, whose procurement decisions significantly impact market dynamics. While substitution risk remains low due to the safety-critical nature of oxygen systems, regulatory changes regarding aircraft safety standards and environmental considerations continue to shape product development and market strategies. Success will increasingly depend on manufacturers' ability to anticipate and adapt to these evolving requirements while maintaining strong relationships with key stakeholders in the aviation industry.

Crew Oxygen Systems Market Leaders

-

RTX Corporation

-

Safran

-

Parker-Meggitt (Parker Hannifin Corporation)

-

Rostec

-

Diehl Stiftung & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Crew Oxygen Systems Market News

- November 2023: SunExpress entered into a contract with Boeing for the delivery of 56 B737-8s and 34 B737-10s. The airline expressed its ambitious plan to double its fleet, aiming to acquire a total of 150 new aircraft by 2033. The crew oxygen systems incorporated in the B737 Max aircraft include Oxygen equipment valves sourced from Carleton Technologies Inc., crew/passenger oxygen system components provided by Safran, and oxygen systems supplied by Collins Aerospace.

- May 2023: Collins Aerospace, a subsidiary of RTX Corporation, introduced its cutting-edge OXYJUMP NG oxygen supply system designed specifically for high-altitude jumps by parachutists. The OXYJUMP NG system incorporates advanced technology that not only extends mission capabilities with a longer gliding distance but also enhances jumper safety. Notably, it offers substantial advantages in terms of size and weight compared to traditional legacy systems. This innovative solution from Collins Aerospace signifies a significant leap forward in supporting parachutists in high-altitude scenarios.

Crew Oxygen Systems Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porters' Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Application

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.1.3 General Aviation

-

5.2 Component

- 5.2.1 Oxygen Mask

- 5.2.2 Oxygen storage system

- 5.2.3 Oxygen Delivery system

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Cobham Limited

- 6.2.2 Safran

- 6.2.3 RTX Corporation

- 6.2.4 Parker-Meggitt (Parker Hannifin Corporation)

- 6.2.5 Rostec

- 6.2.6 Aeromedix, LLC

- 6.2.7 Aviation Oxygen Etc.

- 6.2.8 Aerox Aviation Oxygen Systems, LLC

- 6.2.9 Precise Flight, Inc.

- 6.2.10 PFW Aerospace GmbH

- 6.2.11 Caeli Nova

- 6.2.12 Diehl Stiftung & Co. KG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Crew Oxygen Systems Industry Segmentation

Crew oxygen systems provide oxygen to the crew inside an operational aircraft. There are several components used in aircraft oxygen systems, such as oxygen storage, oxygen delivery, and oxygen masks.

The crew oxygen systems market is segmented by application, component, and geography. By application, the market is segmented into commercial aviation, military aviation, and general aviation. By component, the market is segmented into oxygen mask, oxygen storage system, and oxygen delivery system. The report also covers the market sizes and forecasts for the crew oxygen systems market in major countries across different regions.

For each segment, the market size is provided in terms of value (USD).

| Application | Commercial Aviation | ||

| Military Aviation | |||

| General Aviation | |||

| Component | Oxygen Mask | ||

| Oxygen storage system | |||

| Oxygen Delivery system | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Crew Oxygen Systems Market Research FAQs

How big is the Crew Oxygen Systems Market?

The Crew Oxygen Systems Market size is expected to reach USD 0.71 billion in 2025 and grow at a CAGR of 7.18% to reach USD 1.01 billion by 2030.

What is the current Crew Oxygen Systems Market size?

In 2025, the Crew Oxygen Systems Market size is expected to reach USD 0.71 billion.

Who are the key players in Crew Oxygen Systems Market?

RTX Corporation, Safran, Parker-Meggitt (Parker Hannifin Corporation), Rostec and Diehl Stiftung & Co. KG are the major companies operating in the Crew Oxygen Systems Market.

Which is the fastest growing region in Crew Oxygen Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Crew Oxygen Systems Market?

In 2025, the North America accounts for the largest market share in Crew Oxygen Systems Market.

What years does this Crew Oxygen Systems Market cover, and what was the market size in 2024?

In 2024, the Crew Oxygen Systems Market size was estimated at USD 0.66 billion. The report covers the Crew Oxygen Systems Market historical market size for years: 2024. The report also forecasts the Crew Oxygen Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Crew Oxygen Systems Market Research

Mordor Intelligence provides a comprehensive analysis of the crew oxygen system industry. With decades of expertise in aircraft oxygen systems research, our detailed study covers the entire ecosystem. This includes everything from basic aviation oxygen systems to advanced On-Board Oxygen Generation Systems (OBOGS). The report extensively examines aircraft safety systems, such as emergency oxygen systems and supplemental oxygen systems. It offers stakeholders crucial insights into technological advancements and regulatory requirements.

Our research benefits manufacturers, suppliers, and operators by offering a detailed analysis of pilot oxygen systems and oxygen systems for military aircraft. The report, available as an easy-to-download PDF, provides comprehensive coverage of market dynamics, emerging technologies, and future growth opportunities. Stakeholders gain valuable insights into the evolution of aviation oxygen systems. This includes the latest developments in safety protocols and system integration strategies. The analysis covers both commercial and military applications, ensuring decision-makers have access to the most relevant and actionable intelligence for strategic planning.