| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 10.55 Billion |

| Market Size (2030) | USD 5.92 Billion |

| CAGR (2025 - 2030) | -10.90 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

COVID Rapid Diagnostic Test Market Analysis

The Global COVID Rapid Diagnostic Test Market size is estimated at USD 10.55 billion in 2025, and is expected to decline to USD 5.92 billion by 2030.

The global diagnostic testing landscape has undergone significant transformation with the evolution of healthcare infrastructure and testing protocols. According to the World Health Organization's January 2023 data, the cumulative number of confirmed COVID-19 cases reached approximately 753 million globally, highlighting the continued need for robust testing mechanisms. Healthcare facilities worldwide have adapted their testing protocols to accommodate high-volume screening requirements while maintaining accuracy and efficiency. The integration of COVID-19 rapid diagnostic tests into routine healthcare workflows has become increasingly standardized, with healthcare providers implementing dedicated testing zones and specialized staff training programs.

Technological innovation in diagnostic testing has accelerated dramatically, with manufacturers focusing on developing more sophisticated and user-friendly testing platforms. The FDA has authorized approximately 400 tests and collection kits since the start of the pandemic, comprising 235 molecular tests, 88 antibody tests, and 34 antigen tests, demonstrating the diverse range of testing solutions available in the COVID testing kit market. Advanced features such as automated result interpretation, digital reporting capabilities, and improved sample processing methods have enhanced the overall testing experience. These innovations have particularly focused on reducing result turnaround times while maintaining high accuracy levels.

The market has witnessed significant consolidation through strategic partnerships and collaborations between diagnostic companies, healthcare providers, and research institutions. Major market players are increasingly focusing on expanding their product portfolios through both internal development and strategic acquisitions. For instance, in June 2022, Kaneka Corporation received authorization to manufacture and sell their new immunochromatography-based antigen test kit, exemplifying the ongoing innovation in the sector. These collaborations have facilitated knowledge sharing and accelerated the development of more effective testing solutions by COVID rapid testing companies.

The regulatory landscape continues to evolve with authorities implementing more structured frameworks for test validation and approval. Government initiatives have played a crucial role in promoting accessibility to testing solutions, as evidenced by various national programs supporting the development of affordable diagnostic tools. For example, the Indian government's initiative through IIT to develop cost-effective rapid antigen test kits demonstrates the growing focus on making testing more accessible. International health organizations have also established clearer guidelines for test validation and implementation, helping standardize testing protocols across different regions and healthcare settings. The presence of COVID RDT solutions has further emphasized the importance of regulatory support in ensuring widespread availability.

COVID Rapid Diagnostic Test Market Trends

Increasing Number of Approvals for New and Advanced COVID-19 Rapid Diagnostic Tests

The rapid diagnostic test market is experiencing significant momentum driven by continuous technological advancements and increasing regulatory approvals for innovative testing solutions. Technology plays a central role in expanding healthcare accessibility, with rapid diagnostic devices offering mobility and simplicity as particularly compelling features for use outside formal healthcare facilities. These tests can be performed with limited training, relatively independent of supporting infrastructure, and can accommodate high patient loads and staff shortages. For instance, in May 2022, BD launched a new high-throughput molecular diagnostic combination test for SARS-CoV-2 and Influenza A/B on the BD SARS-CoV-2/Flu assay for the BD COR System, providing automated multiplexed real-time RT-PCR results from a single nasal sample.

The regulatory landscape has been actively supporting the introduction of advanced diagnostic solutions, as evidenced by numerous approvals throughout 2022 and 2023. In June 2022, Kaneka Corporation received authorization to manufacture and sell "Kaneka Immunochromatography SARS-CoV-2 Ag," while Genes2Me Pvt. Ltd launched the CoviEasy Self-Test Rapid Antigen test kit supported by an AI-driven mobile app delivering over 98% accuracy. Additionally, in January 2023, Health Canada granted authorization to commercialize Response Biomedical's RAMP COVID-19 Antigen Test under the Emergency Use Interim Order, demonstrating the continued regulatory support for innovative diagnostic solutions. These approvals are complemented by strategic collaborations, such as LordsMed's exclusive partnership with Sensing Self Pte. Ltd in August 2022 to launch COVID-19 saliva-based rapid antigen test kits in India. The increasing availability of COVID-19 antigen test kits is a testament to the market's growth.

Understand The Key Trends Shaping This Market

Download PDF

Rising Cases of COVID-19 and Its New Variants

The emergence of new COVID-19 variants and the continuous evolution of the virus has created an urgent need for rapid and accurate diagnostic testing capabilities. According to the World Health Organization, as of January 2023, there were significant concerns about new variants, particularly the highly contagious Omicron XBB.1.5 variant. The latest data from January 2023 shows that XBB.1.5 had a projected prevalence of 49.1% in some regions, followed by BQ.1.1 with a projected prevalence of 26.9%, highlighting the rapid spread of new variants and the consequent demand for accurate testing solutions.

The healthcare system's response to these emerging variants has been bolstered by the development of more sophisticated testing capabilities. For instance, in January 2023, the National Institutes of Health, in collaboration with the Administration for Strategic Preparedness and Response (ASPR) at the United States Department of Health and Human Services, launched the "Home Test to Treat" program, providing free COVID-19 health services and at-home rapid tests in selected communities. This initiative demonstrates the growing emphasis on accessible testing solutions to combat new variants. Additionally, various countries have implemented mandatory testing requirements for international travelers in response to new variant concerns, such as Italy's December 2022 mandate for COVID-19 antigenic swabs and molecular testing for virus sequencing for all passengers arriving from China, further driving the demand for rapid diagnostic tests. The rise in rapid coronavirus test usage is a direct response to these variant challenges, with COVID-19 molecular test solutions playing a crucial role in accurate detection.

Segment Analysis: By Type

Antigen Tests Segment in Global COVID Rapid Diagnostic Test Market

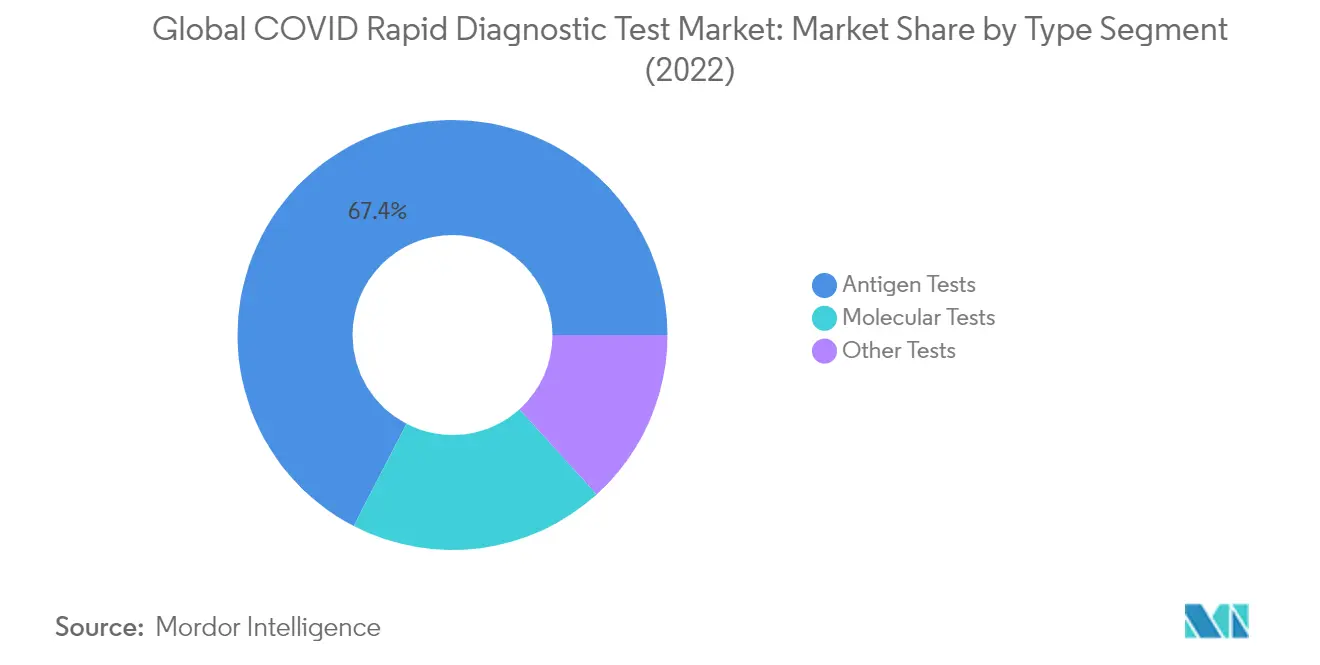

The COVID antigen test segment continues to dominate the global COVID rapid diagnostic test market, holding approximately 67% market share in 2024. This significant market position is attributed to several key advantages, including quick turnaround time, low cost, and ease of use in both clinical and home settings. The segment's dominance is further strengthened by the widespread adoption of these tests for mass screening programs at various passenger transit points like airports, offices, and manufacturing units. Additionally, the increasing availability of technologically advanced COVID antigen tests with improved sensitivity and specificity, coupled with growing regulatory approvals worldwide, has helped maintain this segment's leading position in the market.

Other Tests Segment in Global COVID Rapid Diagnostic Test Market

The other tests segment, which primarily includes antibody tests and serological surveys, is projected to show the most resilient performance in the market from 2024 to 2029. While the overall market is experiencing a decline, this segment is expected to demonstrate relatively better stability with an approximate decline rate of 10% during the forecast period. The segment's resilience is primarily driven by its crucial role in determining COVID-19 prevalence in larger communities through serological surveys, which help authorities devise effective infection containment strategies. The segment is also benefiting from increasing adoption in seroepidemiological surveillance studies and its complementary role alongside COVID molecular tests for comprehensive COVID-19 diagnosis and monitoring.

Remaining Segments in COVID Rapid Diagnostic Test Market

The COVID molecular test segment represents a crucial component of the COVID rapid diagnostic test market, offering highly precise and selective testing capabilities. This segment is particularly valued for its gold-standard status in COVID-19 testing, as recommended by various global health authorities, including the World Health Organization and the Food and Drug Administration. Despite its higher cost and requirement for specialized laboratory settings, the segment maintains its importance in the market due to its superior accuracy and ability to detect even minute levels of viral genetic material. The segment continues to evolve with technological advancements, particularly in areas such as RT-PCR testing and isothermal amplification technologies.

Segment Analysis: By End User

Hospitals & Clinics Segment in COVID Rapid Diagnostic Test Market

The hospitals and clinics segment continues to dominate the COVID rapid diagnostic test market, commanding approximately 60% market share in 2024. This significant market position is attributed to hospitals being well-equipped with advanced diagnostic kits, reagents, and instruments for detecting infectious diseases, making them the backbone of healthcare systems globally. The substantial increase in outpatient services, coupled with affordable care and diagnostic benefits, has further strengthened this segment's market leadership. Additionally, the high risk of infection outbreaks in hospital settings has necessitated routine testing for both healthcare staff and patients, driving the demand for COVID-19 rapid diagnostic tests in these facilities. The segment's growth is also supported by the rise in the number of hospitals, especially in developing countries, and continued improvements in healthcare infrastructure through new investments from both government and private entities.

Hospitals & Clinics Segment Growth in COVID Rapid Diagnostic Test Market

Despite the overall market contraction, the hospitals and clinics segment demonstrates relatively stable performance in the COVID rapid diagnostic test market. The segment's trajectory is supported by ongoing healthcare infrastructure developments and increasing patient footfall in hospitals and clinics worldwide. Healthcare facilities continue to maintain COVID-19 testing protocols, particularly for high-risk patients and healthcare workers, ensuring sustained demand for rapid diagnostic tests. The segment's resilience is further reinforced by the emergence of new COVID-19 variants and the integration of rapid testing into routine hospital protocols. Additionally, the increasing adoption of point-of-care testing in hospital settings and the expansion of hospital networks in emerging markets contribute to the segment's market position.

Remaining Segments in End User Market

The laboratories and diagnostics centers segment represents a significant portion of the COVID rapid diagnostic test market, offering specialized testing services with high-quality equipment and faster turnaround times compared to hospitals. These facilities play a crucial role in handling high volumes of COVID-19 tests, particularly during surge periods, and are often preferred for their dedicated testing expertise and efficient processing capabilities. The segment's market presence is strengthened by its ability to handle large-scale screening programs and provide accurate results through well-equipped facilities and specialized staff. The expansion of laboratory networks and the increasing number of diagnostic centers globally continue to influence the market dynamics in this segment.

Global COVID Rapid Diagnostic Test Market Geography Segment Analysis

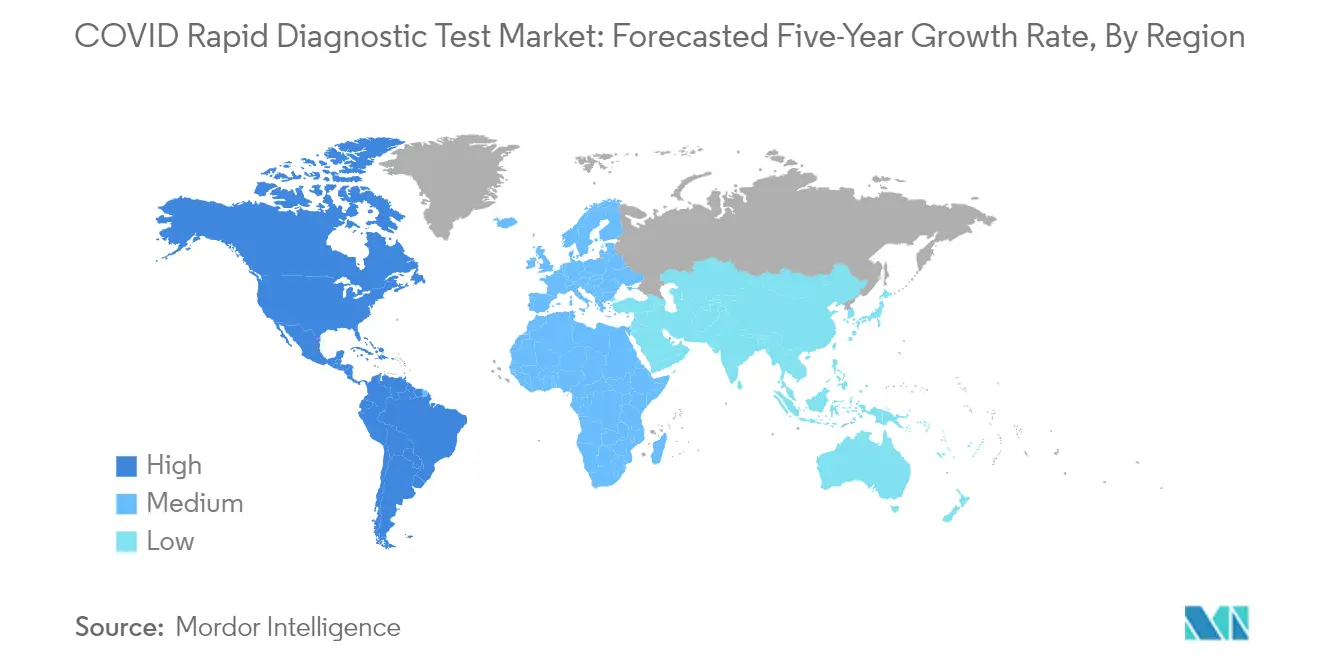

COVID Rapid Diagnostic Test Market in North America

The North American COVID rapid diagnostic test market encompasses the United States, Canada, and Mexico, with each country exhibiting distinct market characteristics and healthcare infrastructure capabilities. The region benefits from advanced healthcare systems, strong regulatory frameworks, and high adoption rates of innovative diagnostic technologies. The presence of major market players, extensive distribution networks, and significant investment in research and development activities has strengthened North America's market position in the global landscape. The COVID-19 rapid testing initiatives have been pivotal in maintaining the region's market leadership.

COVID Rapid Diagnostic Test Market in the United States

The United States dominates the North American market, holding approximately 89% share of the regional market. The country's market leadership is driven by its robust healthcare infrastructure, extensive testing capabilities, and strong presence of key market players such as Abbott Laboratories and Thermo Fisher Scientific. The US market benefits from continuous technological advancements in diagnostic testing, widespread availability of testing facilities, and supportive government policies for rapid diagnostic testing implementation. The COVID antigen test and COVID molecular test are integral components of the US's comprehensive testing strategy.

COVID Rapid Diagnostic Test Market in Canada

Canada emerges as the fastest-growing market in North America, with a forecasted decline rate of approximately -7% during 2024-2029, representing the most moderate decline in the region. The country's market growth is supported by its universal healthcare system, strong emphasis on preventive healthcare, and strategic initiatives by both government and private sectors. Canada's market is characterized by increasing accessibility to rapid testing solutions, growing awareness about early detection, and continuous efforts to enhance testing infrastructure across provinces. The COVID testing kit market in Canada is expanding as part of these strategic initiatives.

COVID Rapid Diagnostic Test Market in Europe

The European COVID rapid diagnostic test market comprises key countries including Germany, the United Kingdom, France, Italy, and Spain, each contributing significantly to the regional market dynamics. The region demonstrates strong market fundamentals supported by advanced healthcare infrastructure, robust regulatory frameworks, and high awareness levels about diagnostic testing. The European market benefits from coordinated healthcare policies, strong research and development capabilities, and effective distribution networks. The COVID-19 rapid testing efforts across Europe have been instrumental in managing the pandemic effectively.

COVID Rapid Diagnostic Test Market in France

France maintains its position as the largest market in Europe, commanding approximately 23% of the regional market share. The country's market leadership is attributed to its comprehensive healthcare system, extensive testing infrastructure, and strong government support for diagnostic testing programs. France's market is characterized by high adoption rates of innovative diagnostic solutions, widespread availability of testing facilities, and strategic collaborations between healthcare providers and diagnostic companies. The COVID antigen test plays a crucial role in France's testing strategy.

COVID Rapid Diagnostic Test Market in Spain

Spain emerges as the fastest-growing market in Europe, with a forecasted decline rate of approximately -9% during 2024-2029, representing the most moderate decline in the region. The Spanish market demonstrates resilience through its comprehensive healthcare system, increasing focus on rapid testing solutions, and continuous efforts to enhance testing accessibility. The country's growth is supported by strategic healthcare initiatives, improving testing infrastructure, and growing awareness about the importance of early detection. The COVID testing kit market in Spain is witnessing significant advancements as part of these efforts.

COVID Rapid Diagnostic Test Market in Asia-Pacific

The Asia-Pacific COVID rapid diagnostic test market encompasses major economies including China, Japan, India, Australia, and South Korea, representing a diverse and dynamic market landscape. The region demonstrates significant market potential driven by large population bases, improving healthcare infrastructure, and increasing healthcare expenditure. The APAC market is characterized by varying levels of healthcare development across countries, growing emphasis on preventive healthcare, and increasing adoption of rapid diagnostic solutions. The COVID-19 rapid testing initiatives are crucial in addressing the diverse healthcare needs of the region.

COVID Rapid Diagnostic Test Market in China

China maintains its position as the largest market in the Asia-Pacific region, demonstrating strong market fundamentals and extensive testing capabilities. The country's market leadership is supported by its large population base, comprehensive testing infrastructure, and significant manufacturing capabilities for diagnostic products. China's market is characterized by strong government support, extensive distribution networks, and continuous technological advancements in diagnostic testing. The COVID molecular test is a key component of China's testing strategy, ensuring comprehensive coverage and accuracy.

COVID Rapid Diagnostic Test Market in South Korea

South Korea emerges as the fastest-growing market in the Asia-Pacific region, demonstrating resilience and adaptability in its testing approach. The country's growth is driven by its advanced healthcare infrastructure, strong technological capabilities, and efficient testing protocols. South Korea's success is attributed to its systematic approach to testing, strong research and development capabilities, and effective integration of diagnostic testing into its healthcare system. The COVID antigen test is widely utilized in South Korea's testing protocols, contributing to its rapid response capabilities.

COVID Rapid Diagnostic Test Market in Middle East & Africa

The Middle East & Africa market encompasses diverse economies including GCC countries and South Africa, presenting unique market dynamics and opportunities. The region demonstrates varying levels of healthcare infrastructure development and testing capabilities across different countries. Within this region, GCC countries represent the largest market segment, while South Africa shows the fastest growth potential, driven by improving healthcare infrastructure and increasing awareness about the importance of diagnostic testing. The COVID-19 rapid testing efforts are crucial in enhancing the region's healthcare response to the pandemic.

COVID Rapid Diagnostic Test Market in South America

The South American COVID rapid diagnostic test market, primarily represented by Brazil and Argentina, shows distinct characteristics influenced by regional healthcare policies and infrastructure development. The market demonstrates potential for growth despite economic challenges in various countries. Brazil emerges as both the largest and fastest-growing market in the region, supported by its extensive healthcare system, large population base, and increasing focus on diagnostic testing capabilities. The COVID testing kit market in Brazil is expanding rapidly, driven by these factors.

Get Analysis on Important Geographic Markets

Download PDF

COVID Rapid Diagnostic Test Industry Overview

Top Companies in COVID Rapid Diagnostic Test Market

The COVID rapid diagnostic test market is characterized by the presence of established players like Abbott, bioMérieux, Siemens Healthineers, Roche, and Quest Diagnostics leading the competitive landscape. Companies are heavily investing in research and development to enhance their product portfolios with more accurate and faster COVID-19 rapid testing solutions, particularly focusing on detecting new variants of the virus. Strategic collaborations with healthcare institutions and government bodies have become increasingly common to ensure wider distribution networks and market penetration. Operational agility has been demonstrated through rapid scaling of production capabilities and streamlined supply chain management to meet sudden demand surges. Market leaders are also expanding their geographical presence through strategic partnerships and acquisitions, while simultaneously investing in digital solutions to complement their diagnostic offerings.

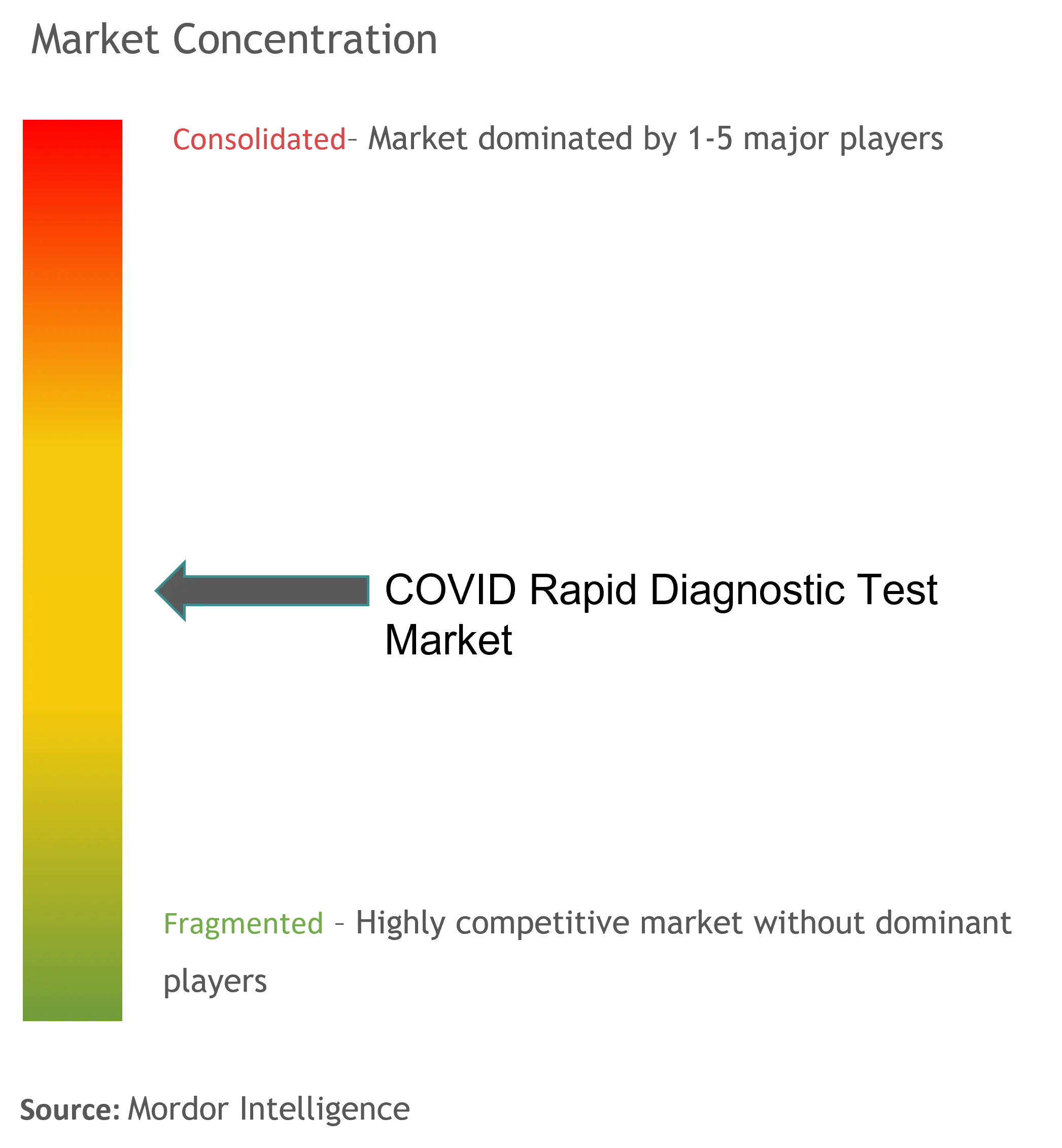

Consolidated Market with Strong Global Players

The COVID testing kit market exhibits a relatively consolidated structure dominated by large multinational healthcare conglomerates with diverse product portfolios. These major players leverage their established research capabilities, manufacturing infrastructure, and extensive distribution networks to maintain their market positions. The market has witnessed significant merger and acquisition activities, particularly involving smaller innovative companies being acquired by larger corporations to enhance technological capabilities and expand product offerings. Regional players, while present, primarily focus on serving specific geographical markets through localized distribution networks and regulatory compliance expertise.

The competitive dynamics are shaped by the presence of both pure-play diagnostic companies and diversified healthcare corporations, each bringing unique strengths to the market. Pure-play companies excel in specialized testing solutions and rapid innovation, while larger conglomerates benefit from economies of scale and integrated healthcare solutions. Market consolidation continues through strategic partnerships and joint ventures, particularly in emerging markets where local expertise is crucial for market access and regulatory navigation.

Innovation and Adaptability Drive Future Success

Success in the COVID RDT market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and regulatory compliance. Market leaders are focusing on developing comprehensive testing solutions that can detect multiple variants and provide faster results, while also investing in automation and digital integration capabilities. The ability to quickly adapt to changing healthcare needs and regulatory requirements, while maintaining product quality and reliability, has become crucial for maintaining market position. Companies are also emphasizing the development of user-friendly testing solutions that can be effectively deployed in various healthcare settings.

For new entrants and smaller players, success lies in identifying and serving niche market segments or specific geographical regions where larger players may have limited presence. Building strong relationships with healthcare providers and maintaining high product quality standards while offering competitive pricing are essential strategies for gaining market share. The regulatory landscape continues to evolve, requiring companies to maintain robust quality management systems and stay compliant with varying regional requirements. Additionally, companies need to focus on developing sustainable supply chain strategies and maintaining strong relationships with key stakeholders to ensure long-term success in the COVID rapid testing companies market.

COVID Rapid Diagnostic Test Market Leaders

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd

-

Quest Diagnostics Incorporated

-

Siemens Healthcare AG

-

bioMerieux SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

COVID Rapid Diagnostic Test Market News

- In January 2023, the Government of Canada approved Artron Laboratories COVID-19 Antigen Home Test, a rapid self-testing of COVID antigens.

- In January 2023, the Government of Canada approved the Biomedomics Cov-scan Rapid Antigen Test for point-of-care tests.

COVID Rapid Diagnostic Test Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Number of Approvals for New and Advanced COVID-19 Rapid Diagnostic Tests

- 4.2.2 Rising Cases of COVID-19 and its New Variants

-

4.3 Market Restraints

- 4.3.1 Product Recalls Due to Quality Control Issues

- 4.3.2 Stringent Regulations and Policy

-

4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Type

- 5.1.1 Molecular Tests

- 5.1.2 Antigen Tests

- 5.1.3 Other Tests

-

5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Laboratories and Diagnostics Centers

- 5.2.3 Other End Users

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Thermo Fisher Scientific Inc.

- 6.1.3 Cue Health Inc.

- 6.1.4 Acon Laboratories, Inc.

- 6.1.5 Danaher Corporation (Beckman Coulter, Inc.)

- 6.1.6 F. Hoffmann-La Roche Ltd

- 6.1.7 Siemens Healthcare AG

- 6.1.8 Quidel Corporation

- 6.1.9 bioMerieux SA

- 6.1.10 Quest Diagnostics Incorporated

- 6.1.11 PerkinElmer Inc.

- 6.1.12 Creative Diagnostics

- 6.1.13 CTK Biotech

- 6.1.14 QIAGEN

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

COVID Rapid Diagnostic Test Industry Segmentation

As per the scope of the report, rapid diagnostic tests (RDTs), also known as rapid tests, are easy-to-use tests that provide quick results. These tests are used to diagnose severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2) infection. The COVID Rapid Diagnostic Test Market is Segmented by Type (Molecular Tests, Antigen Tests, and Other Tests), End User (Hospitals and Clinics, Laboratories and Diagnostics Centers, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD million) for the above segments.

| By Type | Molecular Tests | ||

| Antigen Tests | |||

| Other Tests | |||

| By End User | Hospitals and Clinics | ||

| Laboratories and Diagnostics Centers | |||

| Other End Users | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

COVID Rapid Diagnostic Test Market Research FAQs

What is the current Global COVID Rapid Diagnostic Test Market size?

In 2025, the Global COVID Rapid Diagnostic Test Market size is expected to reach USD 10.55 billion.

Who are the key players in Global COVID Rapid Diagnostic Test Market?

Abbott Laboratories, F. Hoffmann-La Roche Ltd, Quest Diagnostics Incorporated, Siemens Healthcare AG and bioMerieux SA are the major companies operating in the Global COVID Rapid Diagnostic Test Market.

Which is the fastest growing region in Global COVID Rapid Diagnostic Test Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global COVID Rapid Diagnostic Test Market?

In 2025, the North America accounts for the largest market share in Global COVID Rapid Diagnostic Test Market.

What years does this Global COVID Rapid Diagnostic Test Market cover, and what was the market size in 2024?

In 2024, the Global COVID Rapid Diagnostic Test Market size was estimated at USD 11.70 billion. The report covers the Global COVID Rapid Diagnostic Test Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global COVID Rapid Diagnostic Test Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Global COVID Rapid Diagnostic Test Market Research

Mordor Intelligence offers a comprehensive analysis of the covid 19 rapid testing industry. This analysis combines an extensive research methodology with deep market insights. Our expert analysts provide detailed coverage of covid antigen test technologies, covid molecular test developments, and various covid immunoassay platforms. The report examines the evolution of coronavirus rapid test methods. It includes a detailed analysis of covid 19 rapid diagnostic test (COVID RDT) technologies, all available in an easy-to-read report PDF for download.

This strategic industry analysis benefits stakeholders by providing detailed profiles of leading covid rapid testing companies and their innovations in the rapidly evolving market for COVID testing kits. The report delivers actionable insights into testing methodologies, regulatory frameworks, and emerging opportunities across global regions. Our comprehensive coverage helps healthcare providers, manufacturers, and investors understand market dynamics, technological advancements, and future growth potential in the diagnostic testing sector.