| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.72 Billion |

| Market Size (2030) | USD 9.51 Billion |

| CAGR (2025 - 2030) | 4.25 % |

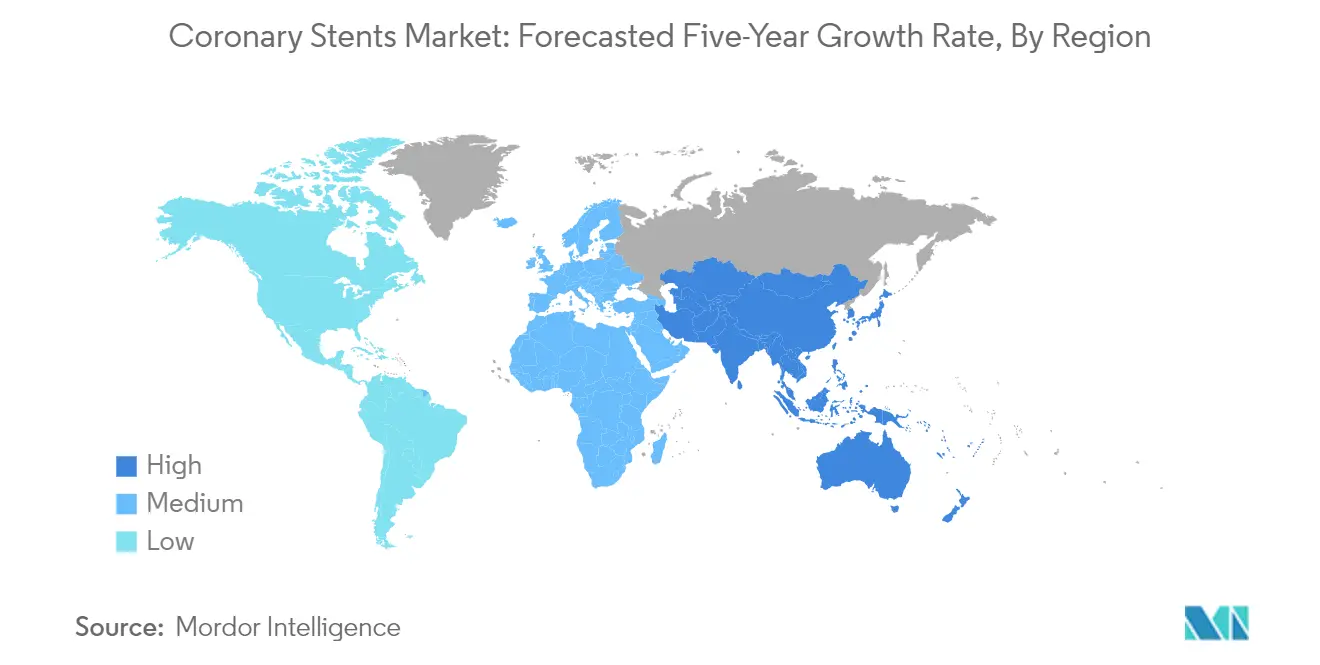

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

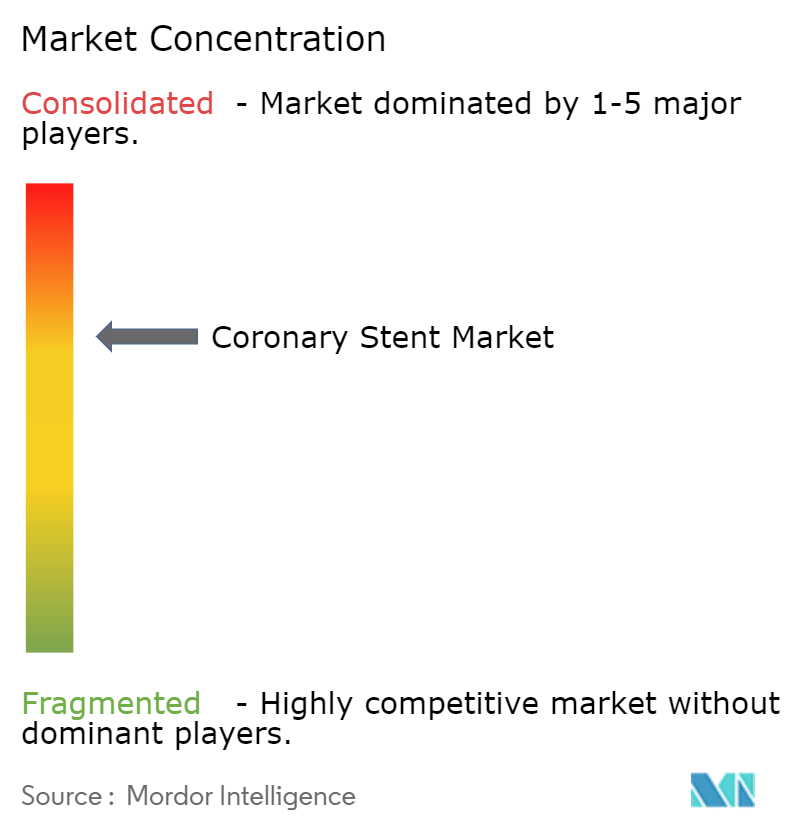

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Coronary Stent Market Analysis

The Coronary Stent Market size is estimated at USD 7.72 billion in 2025, and is expected to reach USD 9.51 billion by 2030, at a CAGR of 4.25% during the forecast period (2025-2030).

The coronary stent market is experiencing significant transformation driven by evolving healthcare infrastructure and an increasing focus on minimally invasive procedures. Healthcare systems worldwide are adapting their infrastructure to accommodate advanced cardiac procedures, with hospitals investing in state-of-the-art catheterization laboratories and hybrid operating rooms. According to the Centers for Disease Control and Prevention's 2022 statistics, heart disease accounts for one in every five deaths in the United States, highlighting the critical need for advanced cardiac care facilities and treatment options. This has led to healthcare facilities upgrading their capabilities to handle complex coronary interventions and emergency cardiac procedures.

The market landscape is being reshaped by strategic collaborations and consolidation activities among key industry players. Companies are increasingly focusing on expanding their geographical presence and strengthening their product portfolios through mergers, acquisitions, and partnerships. For instance, in April 2022, Translumina launched its dual drug polymer-free coated stent (DDCS) VIVO ISAR in various international markets, including Europe, demonstrating the industry's commitment to global expansion and innovation. These strategic movements are creating a more competitive environment while simultaneously improving access to advanced stent technologies across different regions.

Regulatory frameworks and reimbursement policies continue to play a crucial role in shaping market dynamics. Healthcare systems are implementing more stringent quality control measures and safety standards for coronary stents, while simultaneously working to make these devices more accessible through improved insurance coverage and reimbursement policies. The Heart and Stroke Foundation of Canada reported in 2022 that healthcare costs related to heart failure are expected to reach USD 2.8 billion annually by 2030, emphasizing the growing focus on cost-effective treatment options and the need for sustainable reimbursement models.

The industry is witnessing a shift towards value-based healthcare delivery models, with increasing emphasis on patient outcomes and cost-effectiveness. Healthcare providers are adopting evidence-based protocols for stent selection and placement, while also focusing on reducing hospital readmission rates and improving long-term patient outcomes. This trend is accompanied by the integration of digital health technologies for patient monitoring and follow-up care, creating a more comprehensive approach to cardiac care. The Asian Pacific Observatory's 2021 report indicates that by 2050, about one-fourth of the Asia-Pacific region's population will be 60 years or older, driving healthcare systems to adapt their cardiac care delivery models to meet the needs of an aging population while maintaining cost-effectiveness.

Coronary Stent Market Trends

Increasing Prevalence of Coronary Artery Diseases (CADs)

Coronary artery disease represents a significant global health burden, characterized by the narrowing or blockage of coronary arteries due to plaque buildup. According to the Centers for Disease Control and Prevention's latest statistics from 2022, approximately 697,000 people died from heart disease in the United States, accounting for one in every five deaths. The prevalence is particularly concerning as around 20.1 million adults aged 20 and older have coronary artery disease, representing approximately 7.2% of the adult population. This high disease burden is further emphasized by World Heart Federation data, which indicates that cardiovascular disease, including heart disease and stroke, is the most common non-communicable disease globally, responsible for nearly 18.6 million deaths.

The increasing prevalence of risk factors contributing to coronary artery disease presents a compelling driver for market growth. Recent studies have shown that approximately 28% of individuals aged 30-79 years in the general population have an abnormal carotid intima-media thickness of 1.0 mm and above, translating to just over one billion people globally. Additionally, around 21% of people aged 30-79 years have a carotid plaque, and 1.5% have carotid stenosis, equivalent to approximately 816 million people with carotid plaque and 58 million with carotid stenosis. These conditions are more prevalent among men than women, with common risk factors including smoking, diabetes, and hypertension contributing to both increased carotid intima-media thickness and carotid plaque formation.

Understand The Key Trends Shaping This Market

Download PDF

Rising Geriatric Population

The global demographic shift towards an aging population represents a significant driver for the coronary stent market, as older individuals are more susceptible to cardiovascular conditions. According to the World Population Ageing Highlight report, approximately 727 million people aged 65 years or more were living across the world, constituting about 9.3% of the total global population. This number is projected to reach approximately 1.5 billion people by 2050, representing about 16% of the global population. The dramatic increase in the elderly population, particularly in low- and middle-income countries, which are expected to house 80% of the older population by 2050, presents a substantial market opportunity for coronary stent manufacturers.

The impact of aging on cardiovascular health is particularly significant, as research indicates that aging can lead to heart and blood vessel stiffening, increasing exposure to various cardiovascular conditions in later years. Studies have shown that for persons aged 45 and over, the overall self-reported prevalence of diagnosed cardiovascular diseases is 29.4%, with the prevalence rate rising significantly from 22% in the 45-54 age group to 38% in the 70+ age group. This correlation between age and cardiovascular disease risk is further emphasized by regional demographic shifts, particularly in the Asia-Pacific region, where projections indicate that by 2050, about one-fourth of the population will be 60 years or older, primarily due to decreasing fertility rates and increasing longevity.

Technological Advancements in Coronary Stents

The coronary stents market trends are experiencing significant transformation through technological innovations, particularly in the development of advanced drug-eluting stents and bioabsorbable platforms. Recent advancements include the introduction of ultra-thin strut platforms, improved drug delivery systems, and enhanced coating technologies. For instance, the latest generation of drug-eluting stents features sophisticated designs that combine biocompatible polymers with controlled drug release mechanisms, allowing for better and faster healing with 90% of the drug released within 28 days. These innovations have led to the development of stents with improved deliverability, enhanced acute performance, and better patient outcomes, particularly in challenging cases.

The industry has witnessed several breakthrough technologies that are reshaping the landscape of coronary intervention. Notable innovations include the development of dual drug polymer-free coated stents that utilize advanced carrier systems for drug delivery, eliminating the need for traditional polymers. For example, recent developments have introduced stents utilizing Probucol, an antioxidant and lipid-lowering drug, as a carrier for releasing Sirolimus, creating a polymer-free drug-eluting stent platform. Additionally, manufacturers have made significant progress in developing biodegradable polymer coatings that provide controlled drug delivery over 12-14 weeks and degrade gently over one to two years, thereby helping to avoid increased inflammation and other complications associated with permanent polymer presence.

Moreover, the consideration of stent size for heart and heart stent size has become increasingly important in the design and application of these technologies, ensuring optimal fit and function within diverse patient anatomies.

Segment Analysis: By Product Type

Drug Eluting Stent Segment in Coronary Stents Market

Drug-eluting stents (DES) continue to dominate the coronary stents market, holding approximately 67% market share in 2024. This significant market position is attributed to their superior efficacy in preventing restenosis compared to other stent types. The segment's dominance is reinforced by continuous technological advancements in drug delivery mechanisms and coating materials. Major manufacturers are focusing on developing next-generation DES with enhanced biocompatibility and improved drug-elution profiles. The segment's strong performance is also supported by extensive clinical evidence demonstrating better patient outcomes and lower rates of repeat revascularization. Healthcare providers increasingly prefer DES for most coronary interventions due to their proven track record in reducing the risk of in-stent restenosis and their ability to promote better healing of the vessel wall. The presence of leading heart stent brands and top stent manufacturers worldwide further strengthens this segment.

Bioabsorbable Stent Segment in Coronary Stents Market

The bioabsorbable stent segment is emerging as the most dynamic segment in the coronary stents market, projected to grow at approximately 9% from 2024 to 2029. This remarkable growth is driven by increasing patient preference for non-permanent implants and the growing focus on developing advanced biodegradable materials. These innovative stents are designed to provide temporary scaffolding to the vessel wall while gradually dissolving over time, potentially reducing long-term complications associated with permanent implants. The segment's growth is further supported by ongoing research and development activities focused on improving the mechanical properties and absorption rates of these stents. Healthcare providers are showing increased interest in these devices due to their potential advantages in treating younger patients and complex lesions, where the absence of a permanent implant might be beneficial for future interventions.

Remaining Segments in Product Type Segmentation

The bare metal stents market, while representing a traditional approach to coronary intervention, continues to maintain its presence in specific clinical scenarios. These stents remain relevant in cases where patients have contraindications to prolonged dual antiplatelet therapy or in situations requiring shorter duration of antiplatelet medication. Despite facing competition from newer technologies, bare metal stents continue to serve as a viable option in certain geographic markets and specific patient populations. The segment's role in the market is evolving, with manufacturers focusing on improving their design and materials to maintain their relevance in contemporary cardiac care, particularly in markets where cost considerations play a significant role in healthcare decisions.

Segment Analysis: By Biomaterial

Metallic Biomaterial Segment in Coronary Stents Market

The metallic biomaterial segment continues to dominate the global coronary stents market, holding approximately 64% market share in 2024. This significant market position is primarily attributed to the superior mechanical properties and radiopacity of metallic biomaterials compared to their polymeric counterparts. Metallic stents, particularly those made from cobalt-chromium and stainless steel, demonstrate excellent endothelial cell compatibility and provide better radial strength and tensile properties. The segment's dominance is further reinforced by the widespread use of metallic biomaterials in both bare metal stents and drug-eluting stents, where they serve as the primary structural component. The development of advanced metallic stent materials, including new generations represented by stainless steel, magnesium, and zinc, continues to drive innovation in this segment, maintaining its leadership position in the market.

Polymeric Biomaterial Segment in Coronary Stents Market

The polymeric biomaterial segment is emerging as the fastest-growing segment in the coronary stents market, projected to grow at approximately 5% from 2024 to 2029. This growth is driven by increasing adoption of biodegradable polymers in drug-eluting stents and the development of innovative polymer-based coating technologies. The segment's expansion is supported by growing evidence suggesting that polymer-based stents demonstrate comparable safety and efficacy to traditional options, particularly in patients with high bleeding risk who undergo short-term dual antiplatelet therapy. The rise in research and development activities focusing on biodegradable polymers, coupled with technological advancements in polymer coating designs, is expected to further accelerate the segment's growth trajectory over the forecast period.

Remaining Segments in Biomaterial Segmentation

The natural biomaterial segment represents an emerging alternative in the coronary stents market, offering unique advantages in terms of biocompatibility and sustainability. Natural biomaterials, derived from biological sources such as tissue, cells, plants, or microorganisms, are gaining attention for their potential to reduce the risk of in-stent restenosis and promote better healing responses. The segment is particularly significant in the development of bioabsorbable stents, where natural biomaterials can provide a more physiological healing response. The growing focus on sustainable medical devices and the increasing research into natural polymer applications for cardiac tissue engineering continue to drive innovation in this segment.

Segment Analysis: By End User

Hospitals Segment in Coronary Stents Market

The hospitals segment continues to dominate the global coronary stents market, holding approximately 72% of the market value share in 2024. This significant market share can be attributed to hospitals being an integral part of healthcare systems worldwide, offering superior post-procedural care compared to other healthcare settings. The segment's dominance is reinforced by the comprehensive infrastructure and specialized cardiac care units available in hospitals, making them the preferred choice for complex coronary interventions. Hospitals also benefit from well-established reimbursement policies for coronary stent procedures and maintain strong relationships with stent manufacturers, ensuring a steady supply of the latest stent technologies. The segment is experiencing robust growth with a projected growth rate of around 4% from 2024 to 2029, driven by increasing investments in hospital infrastructure, a growing number of catheterization laboratories, and rising adoption of advanced stent technologies. Additionally, hospitals are increasingly focusing on establishing specialized cardiac centers and expanding their cardiovascular departments to meet the growing demand for coronary interventions, further solidifying their position in the market. The presence of leading coronary stent brands and cardiac stent brands in hospitals also contributes to their market leadership.

Ambulatory Surgical Centers Segment in Coronary Stents Market

The Ambulatory Surgical Centers (ASCs) segment represents a growing alternative for coronary stent procedures, offering more relaxing, convenient, and patient-focused experiences compared to traditional hospital settings. These centers are gaining popularity due to their cost-effectiveness for patients, providers, and insurance companies. The segment's growth is supported by recent improvements in Centers for Medicare & Medicaid Services (CMS) coverage for cardiac interventional treatments, including expanded coverage for procedures like pacemaker implantation, endovenous ablation, and catheterization. ASCs are increasingly adopting advanced cardiovascular devices and technologies, demonstrating their capability to handle complex coronary interventions. The trend of cardiologists moving percutaneous coronary interventions (PCI) to ASCs is expected to continue, though careful patient selection remains crucial. These centers are also benefiting from streamlined operations, shorter patient waiting times, and specialized focus on cardiac procedures, making them an attractive option for both healthcare providers and patients seeking coronary stent procedures.

Coronary Stent Market Geography Segment Analysis

Coronary Stents Market in North America

The North American coronary stents market demonstrates robust growth driven by advanced healthcare infrastructure, high adoption of innovative medical technologies, and increasing prevalence of cardiovascular diseases. The United States leads the regional market, followed by Canada and Mexico, with all three countries showing distinct market characteristics. The region benefits from the presence of major coronary stent companies, well-established reimbursement policies, and continuous technological advancements in stent development. Healthcare providers across these countries are increasingly adopting minimally invasive procedures, contributing to market expansion.

Coronary Stents Market in the United States

The United States dominates the North American coronary stents market, holding approximately 82% of the regional market share. The country's market leadership is attributed to its sophisticated healthcare system, high healthcare expenditure, and presence of leading medical device manufacturers. The market is characterized by strong research and development activities, with numerous clinical trials being conducted for next-generation stents. The high prevalence of cardiovascular diseases, coupled with the aging population and increasing obesity rates, continues to drive market growth. The country's robust healthcare infrastructure, including numerous specialized cardiac care centers and hospitals, supports the widespread adoption of advanced coronary stent technologies.

Coronary Stents Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected CAGR of approximately 1% from 2024-2029. The country's market growth is driven by its comprehensive healthcare system and increasing focus on cardiovascular disease treatment. Canadian healthcare authorities are actively promoting advanced cardiac care technologies and procedures, contributing to market expansion. The country's growing elderly population and rising incidence of cardiovascular diseases create sustained demand for coronary stents. Additionally, the presence of well-established medical device distribution networks and favorable reimbursement policies supports market growth.

Coronary Stents Market in Europe

The European coronary stents market exhibits significant growth potential, supported by advanced healthcare systems across Germany, the United Kingdom, France, Italy, and Spain. The region's market is characterized by strong regulatory frameworks, extensive research and development activities, and high adoption of innovative medical technologies. European countries demonstrate varying levels of market maturity and growth patterns, influenced by their respective healthcare policies and demographic factors. The presence of major medical device manufacturers and research institutions contributes to continuous technological advancements in stent development.

Coronary Stents Market in Germany

Germany maintains its position as the largest market for coronary stents in Europe, commanding approximately 25% of the regional coronary stent market share. The country's market leadership is supported by its robust healthcare infrastructure and high healthcare spending. Germany's strong manufacturing base in medical devices, coupled with significant investments in healthcare research and development, drives market growth. The country's healthcare system emphasizes quality cardiac care, supported by numerous specialized cardiac centers and hospitals. The presence of domestic and international medical device companies contributes to market expansion through continuous product innovations.

Coronary Stents Market in France

France demonstrates the highest growth potential in the European market, with a projected CAGR of approximately 3% from 2024-2029. The country's healthcare system prioritizes cardiovascular care, supporting the adoption of advanced stent technologies. French medical institutions actively participate in clinical research and development of innovative cardiac interventions. The country's aging population and increasing prevalence of cardiovascular diseases drive sustained market growth. Additionally, favorable reimbursement policies and strong healthcare infrastructure contribute to market expansion.

Coronary Stents Market in Asia-Pacific

The Asia-Pacific coronary stents market demonstrates dynamic growth potential, encompassing diverse healthcare markets across China, Japan, India, Australia, and South Korea. The region experiences rapid healthcare infrastructure development, increasing healthcare expenditure, and growing awareness of cardiovascular diseases. Each country in the region presents unique market opportunities, influenced by their healthcare policies, economic development, and demographic factors. The region's large patient population and improving access to advanced medical technologies drive market expansion.

Coronary Stents Market in China

China emerges as the dominant market in the Asia-Pacific region, driven by its large patient population and expanding healthcare infrastructure. The country's healthcare system undergoes continuous modernization, with an increasing focus on cardiovascular care. Government initiatives to improve healthcare access and growing private sector participation contribute to market growth. The presence of domestic manufacturers and international companies creates a competitive market environment, fostering innovation and market expansion.

Coronary Stents Market in India

India represents the fastest-growing market in the Asia-Pacific region, driven by rapid healthcare infrastructure development and increasing healthcare awareness. The country's growing middle class, improving healthcare access, and rising incidence of cardiovascular diseases contribute to market expansion. Indian manufacturers are increasingly focusing on developing cost-effective stent solutions while maintaining quality standards. Government initiatives to promote domestic medical device manufacturing and improve healthcare accessibility support market growth. The India coronary stent market is poised for significant expansion due to these factors.

Coronary Stents Market in the Middle East & Africa

The Middle East & Africa coronary stents market demonstrates steady growth potential, with GCC countries and South Africa leading regional development. The market benefits from improving healthcare infrastructure, increasing healthcare spending, and growing awareness of cardiovascular diseases. GCC countries emerge as the largest market in the region, supported by advanced healthcare facilities and strong healthcare investments. South Africa shows the fastest growth potential, driven by improving healthcare access and increasing adoption of advanced medical technologies. The region's market expansion is further supported by government initiatives to enhance healthcare services and growing medical tourism.

Coronary Stents Market in South America

The South American coronary stents market shows promising growth potential, with Brazil and Argentina emerging as key markets. The region's market development is driven by improving healthcare infrastructure, increasing healthcare awareness, and growing prevalence of cardiovascular diseases. Brazil leads the regional market both in terms of market size and growth rate, supported by its large patient population and developing healthcare system. The region's market expansion is influenced by government initiatives to improve healthcare access, increasing private sector participation, and growing adoption of advanced medical technologies. The surgical stents market in South America is also gaining traction due to these advancements.

Get Analysis on Important Geographic Markets

Download PDF

Coronary Stent Industry Overview

Top Companies in Coronary Stent Market

The coronary stent market is characterized by the strong presence of established players like Abbott Laboratories, Medtronic PLC, Boston Scientific Corporation, and Terumo Corporation, alongside emerging players such as Sahajanand Medical Technologies and Meril Life Sciences. The industry demonstrates a robust focus on product innovation, particularly in drug-eluting stents and biodegradable materials, with companies continuously investing in research and development to enhance their technological capabilities. Market leaders are pursuing operational excellence through strategic manufacturing facilities across key regions while maintaining stringent quality standards. Companies are increasingly engaging in strategic partnerships and collaborations to strengthen their market position and expand their geographical presence. The competitive landscape is further shaped by regional expansion strategies, particularly in emerging markets like India and China, where local manufacturers are gaining prominence through cost-effective solutions and government support.

Global Leaders Dominate Consolidated Market Structure

The coronary stent market exhibits a highly consolidated structure dominated by multinational medical device conglomerates with extensive product portfolios and global distribution networks. These established players leverage their strong financial capabilities, advanced research facilities, and long-standing relationships with healthcare providers to maintain their market positions. The market demonstrates a clear distinction between global leaders who offer comprehensive cardiovascular solutions and regional specialists who focus on specific market segments or geographical areas. The presence of local manufacturers is particularly strong in emerging markets, where they compete through cost advantages and an understanding of local healthcare needs.

The industry has witnessed significant merger and acquisition activities, primarily driven by large medical device companies seeking to expand their technological capabilities and geographical reach. These strategic moves often involve acquiring innovative startups or regional players to gain access to new technologies or market segments. The consolidation trend is particularly evident in emerging markets, where established global players are acquiring local manufacturers to strengthen their presence and adapt to regional healthcare requirements. This consolidation pattern has created entry barriers for new players while encouraging existing companies to focus on innovation and operational efficiency to maintain their competitive edge.

Innovation and Market Access Drive Success

Success in the coronary stent market increasingly depends on companies' ability to balance innovation with cost-effectiveness while maintaining strong relationships with healthcare providers and regulatory bodies. Incumbent players must focus on developing next-generation stent technologies while optimizing their manufacturing processes to maintain competitive pricing. Market leaders are investing in research and development to create differentiated products that address specific clinical needs while expanding their distribution networks to reach underserved markets. The ability to navigate complex regulatory environments and maintain strong quality management systems has become crucial for maintaining market position.

For contenders seeking to gain market share, success lies in identifying and exploiting niche market segments while building strong clinical evidence for their products. Companies must develop strategies to overcome the high concentration of buying power among healthcare institutions and insurance providers, who increasingly influence product selection and pricing. The threat of substitution remains relatively low due to the essential nature of coronary stents in cardiovascular treatment, but companies must stay ahead of emerging alternative technologies. Regulatory compliance continues to be a critical factor, with successful companies maintaining robust quality management systems and staying prepared for evolving regulatory requirements across different markets.

Coronary Stent Market Leaders

-

Boston Scientific Corporation

-

Medtronic Plc

-

BIOTRONIK SE & Co. KG

-

Biosensors International Group Ltd

-

Abbott

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Coronary Stent Market News

- August 2024: SMT (Sahajanand Medical Technologies) successfully completed patient enrolment for the Tuxedo 2 clinical trial in India. This pivotal trial seeks to assess the efficacy and safety of the Supraflex Cruz Drug-Eluting Stent (DES) specifically in diabetic patients suffering from multivessel coronary artery disease (CAD).

- May 2024: Abbott launched its XIENCE Sierra Everolimus Eluting Coronary Stent System in India. As a cutting-edge addition to the XIENCE family, the XIENCE Sierra stent caters to individuals grappling with blocked coronary arteries.

Coronary Stent Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Coronary Artery Diseases (CADs)

- 4.2.2 Rising Geriatric Population

- 4.2.3 Technological Advancements in Coronary Stents

-

4.3 Market Restraints

- 4.3.1 High Product Recalls

- 4.3.2 Stringent Approval Process for Stents

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - in USD)

-

5.1 By Product Type

- 5.1.1 Drug Eluting Stent

- 5.1.2 Bare Metal Coronary Stent

- 5.1.3 Bioabsorbable Stent

-

5.2 By Biomaterial

- 5.2.1 Metallic Biomaterial

- 5.2.2 Polymeric Biomaterial

- 5.2.3 Natural Biomaterial

-

5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 B. Braun SE

- 6.1.3 Biosensors International Group Ltd

- 6.1.4 BIOTRONIK SE & Co. KG

- 6.1.5 Boston Scientific Corporation

- 6.1.6 Cook Group

- 6.1.7 Medtronic PLC

- 6.1.8 Terumo Corporation

- 6.1.9 Translumina GmbH

- 6.1.10 Sahajanand Medical Technologies Limited

- 6.1.11 Lepu Medical Technology (Beijing) Co.,Ltd.

- 6.1.12 Bilakhia Holdings Pvt Ltd. (Meril Life Sciences)

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Coronary Stent Industry Segmentation

As per the report's scope, coronary stents are small elastic tubes used to treat narrowed and blocked coronary arteries in patients with coronary artery disease (CAD). The stent reduces the symptoms of chest pain (angina) and aids in treating a heart attack. These types of stents are also called heart stents or cardiac stents. They comprise metal mesh and are implanted in constricted coronary arteries during a technique known as percutaneous coronary intervention (PCI) or angioplasty.

The Coronary Stent Market is Segmented by product type, biomaterial, end-users, and geography. By product type, the market is segmented into drug-eluting stents, bare metal coronary stents, and bioabsorbable stents. By biomaterial, the market is segmented into metallic biomaterial, polymeric biomaterial, and natural biomaterial. By end-users, the market is segmented into hospitals and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD) for the above segments.

| By Product Type | Drug Eluting Stent | ||

| Bare Metal Coronary Stent | |||

| Bioabsorbable Stent | |||

| By Biomaterial | Metallic Biomaterial | ||

| Polymeric Biomaterial | |||

| Natural Biomaterial | |||

| By End User | Hospitals | ||

| Ambulatory Surgical Centers | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Coronary Stent Market Research FAQs

How big is the Coronary Stent Market?

The Coronary Stent Market size is expected to reach USD 7.72 billion in 2025 and grow at a CAGR of 4.25% to reach USD 9.51 billion by 2030.

What is the current Coronary Stent Market size?

In 2025, the Coronary Stent Market size is expected to reach USD 7.72 billion.

Who are the key players in Coronary Stent Market?

Boston Scientific Corporation, Medtronic Plc, BIOTRONIK SE & Co. KG, Biosensors International Group Ltd and Abbott are the major companies operating in the Coronary Stent Market.

Which is the fastest growing region in Coronary Stent Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Coronary Stent Market?

In 2025, the North America accounts for the largest market share in Coronary Stent Market.

What years does this Coronary Stent Market cover, and what was the market size in 2024?

In 2024, the Coronary Stent Market size was estimated at USD 7.39 billion. The report covers the Coronary Stent Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Coronary Stent Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Coronary Stent Market Research

Mordor Intelligence provides a comprehensive analysis of the coronary stent market, utilizing our extensive expertise in healthcare industry research. Our detailed report examines the entire ecosystem of cardiac stent technology. This includes innovations in bare metal stents, vascular stent advancements, and cutting-edge drug-eluting stent systems. The analysis highlights leading coronary stent companies and the best stent manufacturers in the world. It offers detailed insights into various cardiac stent brands and their technological specifications, such as heart stent size variations and the latest implementations of the stent boost technique.

Our expertly crafted report, available as an easy-to-download PDF, provides stakeholders with crucial insights into surgical stents market dynamics and emerging opportunities. The analysis includes detailed specifications like onyx stent size chart data and comprehensive information about stent brands across regions. We examine critical factors such as stent price in USA variations and international pricing trends. Additionally, we evaluate the expanding India coronary stent market. The report offers detailed technical specifications covering stent size for heart procedures and various arterial stents applications. This enables healthcare providers and industry participants to make informed decisions based on thorough market intelligence.