Corn Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

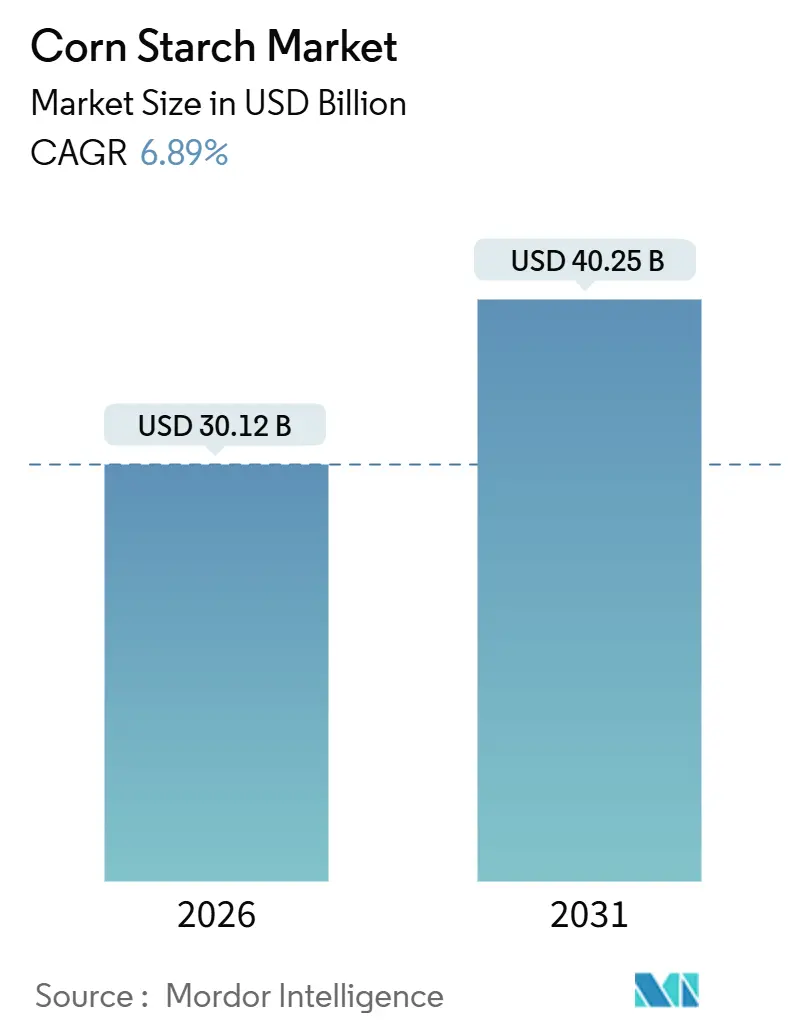

| Market Size (2026) | USD 30.12 Billion |

| Market Size (2031) | USD 40.25 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

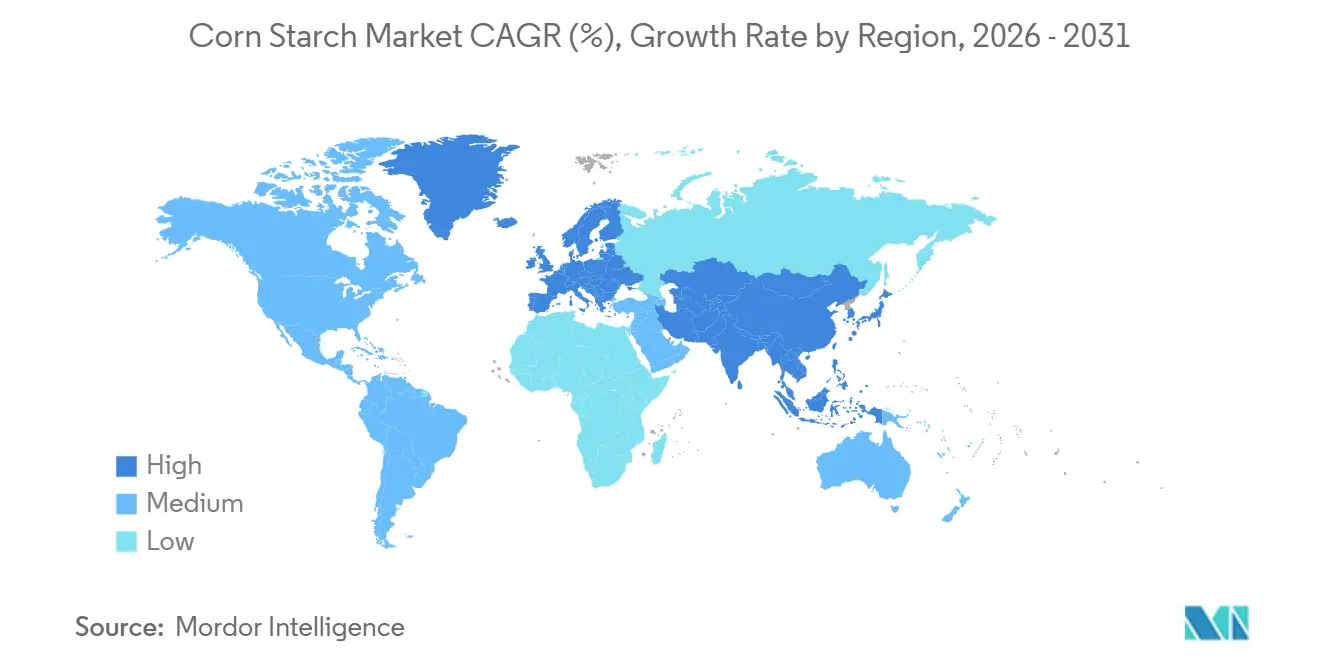

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Corn Starch Market Analysis by Mordor Intelligence

The corn starch market size stood at USD 30.12 billion in 2026 and is projected to reach USD 40.25 billion by 2031, advancing at a 6.89% CAGR during the forecast window. Rising clean-label mandates, a widening preference for bio-based industrial feedstocks, and regulatory support for natural excipients are reshaping procurement decisions across food, pharmaceutical, and paper value chains. North American consumption remains anchored by mature wet-milling assets, but Asia-Pacific is escalating capacity to capture demand from packaged-food and generic-drug producers. Patent activity in enzyme-assisted starch modification, up 22% year-over-year in 2025, signals a pivot from commodity tonnage to functional specialization. Meanwhile, federal procurement rules that favor ingredients with renewable-carbon content are cementing corn starch as a default input across adhesives, coatings, and biodegradable films. Margin expansion opportunities center on non-GMO and dual-certified grades, where customers continue to absorb premiums of 15–25% for supply-chain assurance and clean-label positioning

Key Report Takeaways

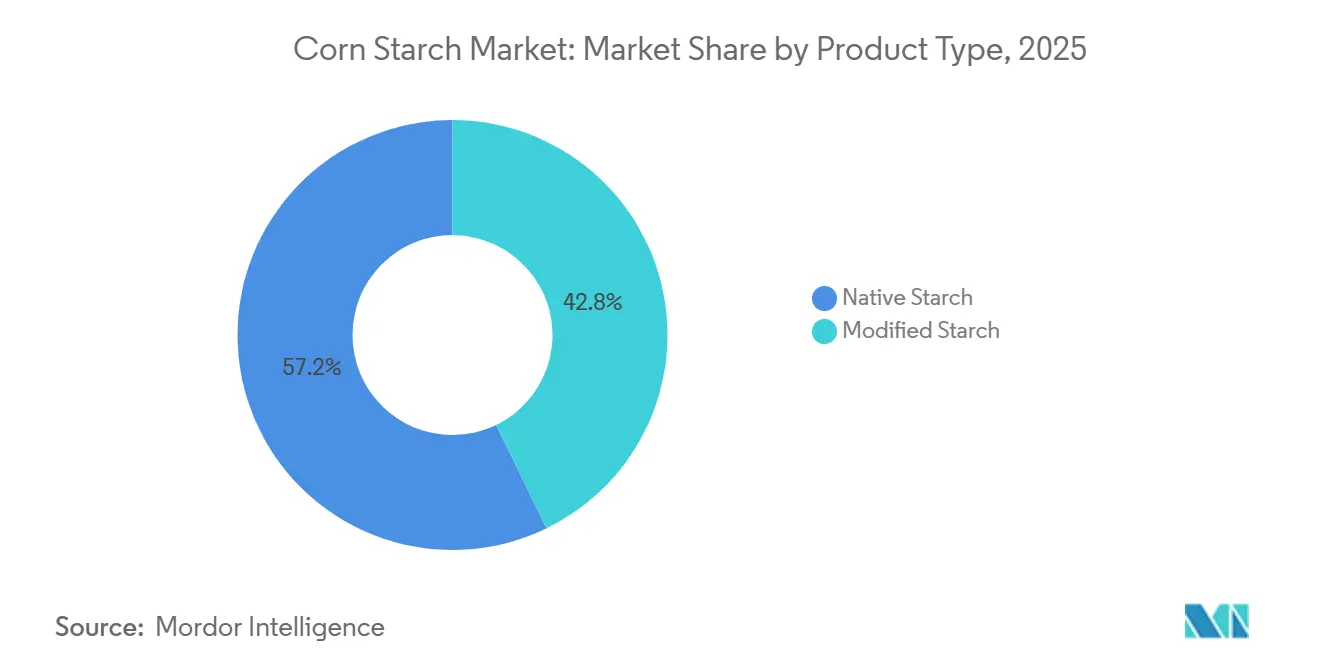

- By type, native starch captured 57.21% of value in 2025, while modified grades are forecast to expand at a 7.48% CAGR to 2031.

- By form, powder held 83.28% of volume in 2025; liquid starch is advancing at an 8.11% CAGR through 2031.

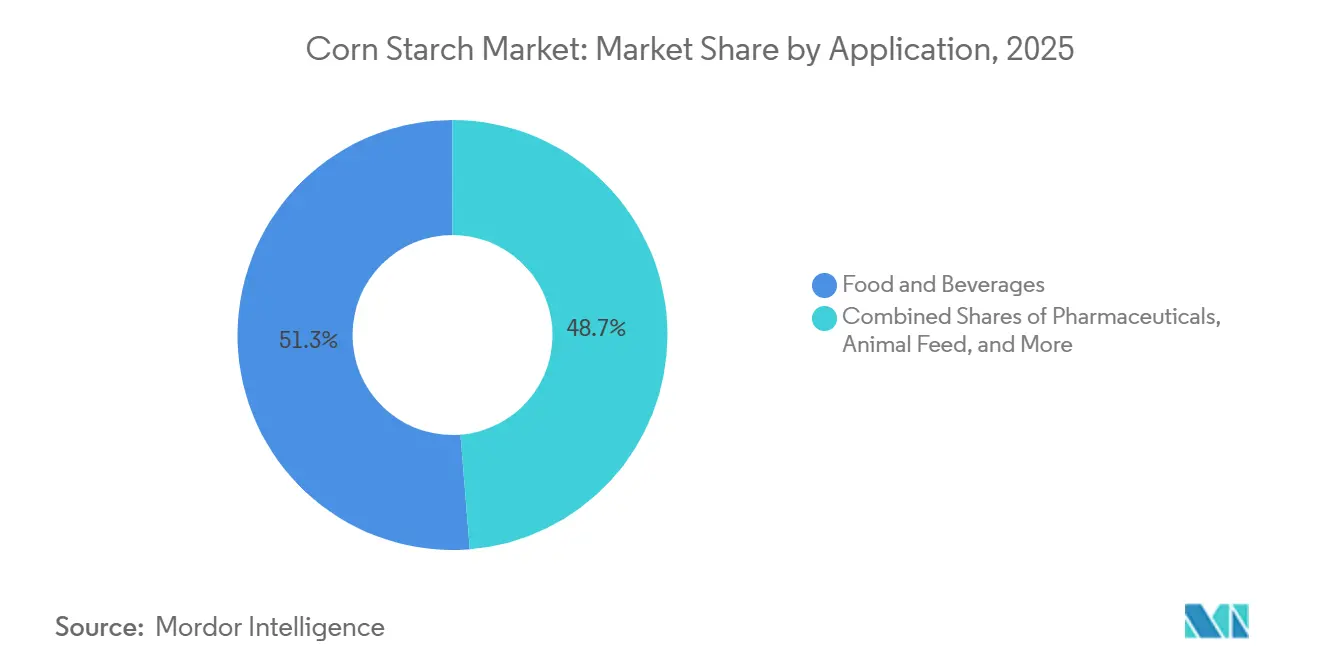

- By application, food and beverages led with 51.28% of revenue in 2025, whereas pharmaceuticals are set to rise at an 8.55% CAGR during 2026-2031.

- =By geography, North America commanded 35.46% of 2025 turnover, while Asia-Pacific is forecast to log an 8.42% CAGR to 2031.

Global Corn Starch Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for clean-label products to fuel native corn starch demand | +1.2% | Global, led by North America & Western Europe | Medium term (2–4 years) |

| High demand for gluten-free and allergen-free binders in processed food | +0.9% | North America, Europe, Australia | Short term (≤2 years) |

| Pharmaceutical sectors shift toward natural excipients fuels corn starch adoption | +1.5% | Asia-Pacific core, spillover to MEA | Long term (≥4 years) |

| Use of modified corn starch as a fat-replacer gains popularity in low-calorie products | +0.8% | North America, Western Europe | Medium term (2–4 years) |

| Government push for bio-based industrial raw material encourages corn starch usage | +1.1% | Global, strongest in U.S., EU, China | Long term (≥4 years) |

| Health-focused snacking spurs uptake of corn starch as ingredients | +0.7% | Global, urban centers in APAC & North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-Label Products Fuels Native Corn Starch Adoption

Brands are increasingly leveraging native corn starch as a strategic asset due to consumers' rising preference for recognizable ingredient lists. A 2025 survey by the International Food Information Council revealed that 68% of U.S. shoppers actively avoid products with chemical-sounding additives, up from 54% in 2022. Native corn starch, labeled simply as "corn starch," caters to this demand without compromising texture in sauces, soups, and dairy products. Additionally, early 2024 guidance from the European Food Safety Authority (EFSA) reaffirmed that native starches do not require an E-number designation[1]Source: European Food Safety Authority, “Scientific Opinion on Native Starches,” efsa.onlinelibrary.wiley.com. This offers formulators a compliance advantage in markets where avoiding E-numbers influences purchasing decisions, as noted in the EFSA Journal. However, native starch performs poorly under high shear or freeze-thaw conditions. Consequently, brands launching ambient-stable or frozen products continue to rely on modified grades. This has created a bifurcated demand pattern that benefits suppliers with dual production capabilities. Ingredion's Q3 2025 earnings call underscored this trend, reporting an 11% year-over-year growth in clean-label native starch volumes in North America, compared to a 4% increase in modified-starch volumes, highlighting the consumer-driven shift.

Pharmaceutical Sectors Shift Toward Natural Excipients Accelerates Corn Starch Uptake

Regulatory changes are driving generic-drug manufacturers to replace synthetic binders with pharmacopeial-grade corn starch. In June 2024, the U.S. FDA updated its Inactive Ingredient Database, identifying 23 synthetic disintegrants for increased post-market monitoring. Meanwhile, corn starch, a trusted component in oral solid dosage forms for over 70 years, remains unaffected by new restrictions. In March 2025, India's Central Drugs Standard Control Organisation introduced draft guidance requiring domestic tablet manufacturers to source at least 30% of excipients from plant-based or mineral origins by 2028, favoring corn-starch suppliers with ISO 9001 and Good Manufacturing Practice certifications. Similarly, in August 2025, China's National Medical Products Administration mandated that new generic applications justify the use of synthetic excipients over natural alternatives. This regulatory shift has created a structural demand boost: Roquette's pharma-starch division reported a 19% revenue growth in fiscal 2025, driven by Asian generic manufacturers transitioning from polyvinylpyrrolidone to pregelatinized corn starch.

Use of Modified Corn Starch as Fat Replacer Gains Traction in Low-Calorie Formulations

Governments are addressing rising obesity-related health costs by encouraging food product reformulations. Modified starches that replicate the texture of fat are gaining traction in reduced-calorie dairy, bakery products, and dressings. The U.S. Department of Health and Human Services' 2024–2030 dietary guidelines recommend limiting saturated fat to 10% of daily caloric intake. In response, food manufacturers are substituting 20–40% of butter or cream with enzymatically modified waxy corn starch, which provides a creamy texture at just one-ninth the caloric density. Tate & Lyle launched its clean-label fat replacer, CLARIA, in late 2023. By 2025, CLARIA generated USD 47 million in sales, with yogurt and ice-cream applications accounting for 62% of its volume, as reported in the company's annual report. In May 2025, the European Commission updated its Farm to Fork Strategy, targeting a 15% reduction in average per-capita saturated-fat intake by 2030. This update highlights the increasing regulatory demand for fat-mimetic ingredients across the EU's 27 member states. Additionally, fat replacers offer the benefit of extending shelf life by reducing lipid oxidation. This enables brands to lower preservative usage while enhancing their clean-label positioning. These combined advantages support a 20–30% price premium over conventional modified starches.

Government Push for Bio-Based Industrial Raw Materials Strengthens Corn Starch Demand

Policy frameworks in the U.S., E.U., and China are increasingly incorporating bio-based content mandates into public procurement and industrial subsidies. This development positions corn starch as a preferred feedstock for products such as adhesives, coatings, and biodegradable plastics. The U.S. Department of Agriculture's BioPreferred Program, reauthorized in the 2024 Farm Bill with a 40% budget increase, now requires federal agencies to prioritize purchasing products containing at least 25% bio-based carbon. Corn starch, being 100% plant-derived, automatically qualifies under this mandate. Similarly, the European Union's Circular Economy Action Plan, revised in February 2025, introduced a binding requirement for member states to source 20% of industrial polymers and binders from renewable feedstocks by 2030, with financial penalties for non-compliance. In China, the Ministry of Industry and Information Technology, in July 2025, classified corn-starch-based corrugating adhesives as a "priority green material," enabling paper mills transitioning from synthetic resins to access low-interest loans and tax rebates. Reflecting this trend, Cargill's 2025 sustainability report revealed a 27% year-over-year increase in bio-industrial starch sales. Corrugating adhesives and biodegradable film resins contributed equally to this growth, and Cargill expects policy-driven demand to sustain double-digit growth through 2028.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating corn prices impact market dynamics | -0.6% | Global, acute in North America & South America | Short term (≤2 years) |

| Challenges in native starch storage and functionality | -0.3% | Tropical & subtropical regions (APAC, MEA) | Medium term (2–4 years) |

| Regulatory restriction on GMO corn-based ingredients | -0.5% | EU, China, parts of Latin America | Long term (≥4 years) |

| Complex processing for modified starch raises manufacturing cost | -0.4% | Global, most acute in emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Corn Prices Inject Margin Volatility Across the Value Chain

During the first nine months of 2025, corn futures on the Chicago Mercantile Exchange ranged between USD 4.12 and USD 4.70 per bushel. This price volatility was driven by weather disruptions in the U.S. Corn Belt and fluctuating export demand from China. The 14% price variation has compressed margins for starch producers, as their customer contracts typically fix selling prices for six to twelve months. The U.S. Department of Agriculture's October 2025 World Agricultural Supply and Demand Estimates report projected a 3.2% decline in global corn ending stocks for the 2025–2026 marketing year[2]Source: U.S. Department of Agriculture, “WASDE October 2025,” usda.gov. This decline was attributed to below-trend yields in Argentina and Brazil, which together account for 22% of the global corn trade. Smaller starch producers without hedging programs or long-term grain contracts are under significant pressure. According to industry cost models, a 10% increase in corn costs results in a 6–7% reduction in gross margins. This is because starch conversion adds limited value, and energy costs are largely fixed. Larger companies like Archer Daniels Midland and Cargill mitigate these risks through vertical integration. For example, ADM's 2025 annual report stated that 68% of the corn it processes for starch is sourced from company-owned elevators or multi-year farmer contracts, protecting it from spot-market price spikes. Another strategy gaining momentum is the co-location of starch plants with ethanol facilities. This setup enables producers to sell corn oil and distillers' grains as co-products, effectively reducing the net cost of starch production by 8–12%.

Regulatory Restrictions on GMO Corn Tighten Supply Chains and Raise Costs

Under the European Union's stringent GMO-labeling regime, outlined in Regulation (EC) No 1829/2003 and enforced through random testing at ports of entry, starch importers are required to certify that any product containing more than 0.9% GMO material is labeled. However, most European food brands reject labeled ingredients, pushing suppliers to procure non-GMO corn at a premium of 15–25%. China's revised GB 2763 standard, which will take effect in January 2025, significantly lowers the allowable GMO-corn residue thresholds in food-grade starch from 5% to 0.5%. This stricter regulation forces Chinese importers to secure identity-preserved shipments with third-party certification, increasing landed costs by USD 18–22 per metric ton. In April 2025, India's Food Safety and Standards Authority proposed mandatory GMO disclosure for all starches used in packaged foods through a consultation paper. Despite this growth, non-GMO corn still accounts for only 2.3% of total U.S. corn plantings, creating a persistent supply-demand imbalance that keeps non-GMO premiums high. Producers who invest in dedicated non-GMO handling—such as separate silos, rigorous cleaning protocols, and detailed chain-of-custody documentation—can capture these premiums. However, the required capital investment, ranging from USD 3–5 million for a mid-sized wet mill, discourages smaller operators and consolidates non-GMO capacity among leading players.

Segment Analysis

By Type: Modified Starch Gains Ground on Functional Versatility

In 2025, native starch accounted for 57.21% of the market's value. However, modified grades are expected to grow at a strong 7.48% CAGR, indicating a shift in market trends by 2031. This growth highlights increasing demand for improved stability—whether heat, shear, or freeze-thaw—in frozen entrees and ready-to-eat desserts. The market for modified corn starch is projected to expand further, driven by pharmaceutical buyers favoring pregelatinized options that can cut compression time by up to 20%. Producers are offsetting higher conversion costs with price premiums ranging from 20% to 35%. They are also leveraging expanded Codex authorizations, which in 2024, added 18 new food categories.

While price-sensitive regions continue to rely on native starch for ambient snacks and bakery fillings, a significant shift is evident. By 2025, organized retail in India reached 14% penetration, boosting frozen and chilled product channels and creating opportunities for modified offerings. In China, wet-millers increased acetylated capacity by 22% between 2023 and 2025 to meet the growing demand from frozen-dumpling lines, which experienced 16% growth that year. As a result, the corn starch market is expected to follow a dual path: native starch will retain its scale, while modified grades will drive revenue and margin growth.

Note: Segment shares of all individual segments available upon report purchase

By Form: Powder Dominates, Yet Liquid Starch Gains in Just-in-Time Supply Models

In 2025, powder represented 83.28% of shipments due to its low moisture content, which provides shelf stability and compatibility with dry mixes, particularly in pharmaceuticals and snack production. Liquid starch, supplied as a 35–40% solids slurry, is experiencing an 8.11% CAGR. This growth is attributed to paper mills and beverage plants implementing continuous-feed systems, which not only eliminate dust exposure but also cut batch preparation time by 30 to 40 minutes. While powder will maintain its dominance in the corn starch market, the rising demand for liquid starch reflects advancements in process engineering for large-scale operations.

Infrastructure limitations keep powder prevalent in fragmented markets that lack bulk-tanker facilities. Furthermore, microbial-count restrictions under EU Regulation 2073/2005 require costly cold-storage or preservative solutions for liquid formats in ready-to-eat foods, hindering adoption among smaller processors. In Western Europe, bakeries are increasingly adopting hybrid procurement models, sourcing powder for dough and liquid for fillings. This trend highlights the application-specific decisions that enable both forms to coexist within the corn starch market.

By Application: Food and Beverages Lead, Pharmaceuticals Surge on Generic-Drug Expansion

In 2025, food and beverages represented 51.28% of demand, driven by categories such as bakery, dairy, confectionery, and sauces that depend on corn starch for thickening, gelling, and stabilizing. The pharmaceutical segment of the corn starch market is experiencing the fastest growth, with an 8.55% CAGR. This growth is fueled by regulatory support for natural excipients and increasing tablet production capacity in India, China, and Brazil. In personal care, the transition away from talc contributed to a 7.2% rise in corn starch usage in dry shampoos and powder foundations in 2025.

Paper and corrugating, which currently account for 12% of the volume, are benefiting from the growth of e-commerce packaging and the bio-content provisions of ISO 15361, which enhance starch adhesion compared to synthetic resins. However, animal feed trials face limited growth as they are perceived as a lower-cost carbohydrate alternative, though aquaculture pellets have established a stable niche. Mills are leveraging dual-certified starch that complies with both food and pharmaceutical standards, enabling them to manage order fluctuations more effectively. ADM has reported that 23% of the output from its Clinton plant now qualifies for pharmaceutical markets.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, North America contributed 35.46% of global corn starch revenue, driven by its well-established food-processing industry, robust pharmaceutical-excipient supply chains, and proximity to the U.S. Midwest, the world's largest corn-growing region. However, with a forecast CAGR of 5.9% through 2031, the region trails Asia-Pacific's 8.42%, indicating a shift towards premium products—such as clean-label, non-GMO, and organic grades—rather than volume growth. According to the U.S. Department of Agriculture's Economic Research Service in September 2025, domestic corn-starch consumption increased by just 2.1% year-over-year, while exports of specialty modified starches rose by 9%, highlighting a move toward higher-value offerings. Canada's food-processing sector, supported by trade agreements with the EU and Asia, is driving demand for pharma-grade starch. To meet this demand, Ingredion expanded its Cardinal plant in Ontario, Canada, in mid-2025 with a CAD 28 million investment, targeting both domestic tablet manufacturers and export markets. Meanwhile, Mexico's corn-starch market is growing at 6.7%, fueled by the nearshoring of food production for the U.S. and increased domestic consumption of snacks. Organized retail sales in Mexico grew by 11% in 2025, according to the Mexican Association of Retail Chains (ANTAD Mexico).

Asia-Pacific's strong 8.42% CAGR is primarily attributed to the rapid industrialization of food processing in China and India, government support for local excipient production, and growing middle-class demand for convenience foods. The China Starch Industry Association reported that China's corn-starch production reached 14.2 million metric tons in 2025, a 7% increase from 2024, driven by capacity expansions in Shandong and Jilin provinces. In India, domestic players like HL Agro Products and Gujarat Ambuja Exports increased production, supported by the government's Production-Linked Incentive scheme, which provides a 10% capital subsidy for starch-plant investments exceeding INR 500 million. This led to a 16% decline in starch imports in fiscal 2025. While Japan and Australia are smaller markets, they are growing at 5.1% and 6.3%, respectively, with clean-label and organic starches commanding premiums of 30–50% over conventional grades. Southeast Asia, particularly Indonesia, Thailand, and Vietnam, is emerging as a key growth area. Starch demand in the region rose by 9.8% in 2025, driven by increased production of instant noodles, snacks, and ready-to-drink beverages, according to the ASEAN Food Processors Association[3]Source: ASEAN Food Processors Association. "Regional Production Statistics 2025." aseanfood.info. .

Europe's corn starch market is growing at an annual rate of 6.1%, influenced by strict GMO regulations, ambitious sustainability targets, and a mature food industry that emphasizes functional innovation over volume growth. The European Starch Industry Association's 2025 annual review revealed that EU starch production reached 11.3 million metric tons, with corn starch accounting for 62% of the total. The share of non-GMO corn starch increased to 41% in 2025, up from 34% in 2023. Germany, France, and the Netherlands lead production, hosting facilities from major players like AGRANA, Tereos, and Avebe. Meanwhile, Eastern European countries such as Poland, Hungary, and Romania are attracting greenfield investments due to lower labor costs and proximity to non-GMO corn fields. In South America, a 7.3% CAGR is being driven by Brazil and Argentina. These countries, as major corn producers, are expanding domestic starch-processing capacity to capture value-added margins instead of exporting raw grain. Brazil's starch production grew by 12% in 2025, according to the Brazilian Starch Association. Lastly, while the Middle East and Africa represent the smallest region with a 4.9% CAGR, growth is evident in countries like Egypt, South Africa, and Saudi Arabia, where government-led food-security initiatives are boosting local ingredient production.

Competitive Landscape

The global corn starch market demonstrates moderate concentration, scoring 6 out of 10, with established multinational corporations operating alongside regional players in specialized application segments. Major players in the market include Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, Tate & Lyle PLC, and Roquette Freres.

Companies are competing through innovation in specialty starches, developing value-added products with enhanced functionality for specific applications. The clean-label segment has become a focus area, where manufacturers invest in physical modification techniques to improve performance while maintaining natural ingredient status. Companies are also differentiating themselves through sustainability initiatives, implementing responsible sourcing practices, and eco-friendly production methods to meet regulatory requirements and consumer preferences.

Regional manufacturers are strengthening their positions by utilizing local market knowledge and operational flexibility to serve niche markets, especially in emerging economies where proximity to demand centers offers logistical benefits. Companies are implementing backward integration strategies to control corn cultivation, ensuring quality and supply stability in volatile agricultural markets. Process optimization and quality control technologies have become essential for maintaining cost competitiveness in this price-sensitive market with narrow profit margins.

Corn Starch Industry Leaders

-

Cargill Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

Tate & Lyle PLC

-

Roquette Freres

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Linqing Deneng Golden Corn Bio Limited, a subsidiary of China Starch Holding Company, expanded its operations by opening two additional starch processing facilities. The company operates two cornstarch production lines at its existing facilities, with annual production capacities of 550,000 tonnes and 450,000 tonnes, respectively.

- March 2025: Cargill opened a new corn milling plant in Gwalior, Madhya Pradesh, operated by Indian manufacturer Saatvik Agro Processors, to meet increasing demand from India's confectionery, infant formula, and dairy industries.

- September 2024: Ingredion partnered with Austrian company Agrana to increase starch production in Romania, expanding its manufacturing presence in Eastern Europe to address the rising regional demand for specialty starches.

- August 2024: Al Ghurair Foods initiated construction of its Corn Starch Manufacturing Plant at Khalifa Economic Zones Abu Dhabi (KEZAD). The facility, which is the first corn starch plant in the region, aims to increase local food production capacity and support the UAE's National Strategy for Food Security.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the corn starch market as the total value of native and modified corn-derived starch supplied to food, feed, industrial, and pharmaceutical users worldwide, expressed in constant 2024 US dollars. We trace value from primary wet-milling output through to first sale by specialty converters and distributors.

Scope Exclusion: Bio-ethanol volumes monetized under fuel ethanol statistics are outside our valuation.

Segmentation Overview

- Type

- Native Starch

- Modified Starch

- Form

- Powder

- Liquid

- Application

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Animal Feed

- Paper and Corrugating

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- South Africa

- Saudi Arabia

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed starch processors, food formulators, feed compounders, and procurement managers in North America, Europe, and Asia-Pacific. The discussions clarified conversion yields, average selling prices by moisture level, and seasonality of demand, enabling us to cross-check secondary indicators and adjust regional elasticities.

Desk Research

We begin with public datasets from sources such as the United States Department of Agriculture, UN Comtrade, Eurostat, and the International Starch Institute, which reveal corn harvest volumes, trade flows, and end-use shares. Company 10-Ks, investor decks, and product catalogs help us benchmark starch pricing tiers and purity grades across regions. In addition, D&B Hoovers and Dow Jones Factiva supply revenue splits that anchor supplier roll-ups. Patent filings (Questel) and standards published by Codex Alimentarius and the FDA guide us on technological shifts and regulatory caps that influence ingredient substitution. These references are illustrative; many additional documents and databases were consulted to verify patterns, fill gaps, and challenge early assumptions.

Market-Sizing & Forecasting

A top-down and bottom-up blended model is applied. Global corn harvest and wet-milling utilization are reconstructed, then filtered through starch extraction rates, import-export balances, and application-specific penetration ratios. Supplier roll-ups and sampled ASP × volume checks validate totals and highlight anomalies. Key variables include Chicago corn futures (input cost), global processed food output, high-fructose syrup substitution rates, ethanol coproduct credits, and disposable income growth in emerging Asia. Forecasts employ multivariate regression, with corn price, per-capita snack intake, and industrial starch intensity as independent drivers, while scenario analysis captures weather shocks. Where country-level data lack granularity, regional proxies are scaled using population and manufacturing GDP weights.

Data Validation & Update Cycle

Outputs undergo variance checks against historical margins, peer ratios, and trade statistics before a two-step analyst review. We refresh every twelve months and trigger interim updates when corn price spikes, policy shifts, or large capacity additions move the market. A final pass is completed just before release.

Why Mordor's Corn Starch Baseline Commands Reliability

Estimates for corn starch often diverge because firms choose different inclusion rules, pricing ladders, and refresh cadences. Our team signals these drivers upfront so decision-makers understand why numbers rarely match line for line.

Key gap drivers include whether pharmaceutical-grade starch is counted, the treatment of sweetener derivatives, currency conversion dates, and the rigor with which supplier interviews adjust model defaults.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.79 B (2025) | Mordor Intelligence | - |

| USD 21.99 B (2024) | Regional Consultancy A | Excludes pharma grades and applies conservative ASPs |

| USD 24.06 B (2024) | Global Consultancy B | Relies largely on trade data, minimal industry verification |

| USD 24.22 B (2024) | Industry Journal C | Segregates sweetener derivatives; uniform regional growth rates |

The comparison shows that, by selecting the right scope, combining verified field insights with transparent modeling steps, and refreshing data annually, Mordor Intelligence delivers a balanced baseline that clients can reproduce and confidently use for planning.

Key Questions Answered in the Report

How large is the corn starch market in 2026?

The corn starch market size reached USD 30.12 billion in 2026 and is projected to approach USD 40.25 billion by 2031.

Which region will add the most incremental demand for corn starch by 2031?

Asia-Pacific is forecast to expand at an 8.42% CAGR, the fastest among all regions, driven by packaged-food and generic-drug capacity additions.

What factors drive modified corn starch adoption?

Demand for heat, shear, and freeze-thaw stability in frozen meals and low-calorie formulations is lifting modified grades at a 7.48% CAGR.

Which application segment is growing fastest?

Pharmaceuticals, used mainly as tablet binders and disintegrants, are projected to grow at an 8.55% CAGR through 2031.

Page last updated on: