Market Size of Continuous Testing Industry

| Study Period | 2019 - 2029 |

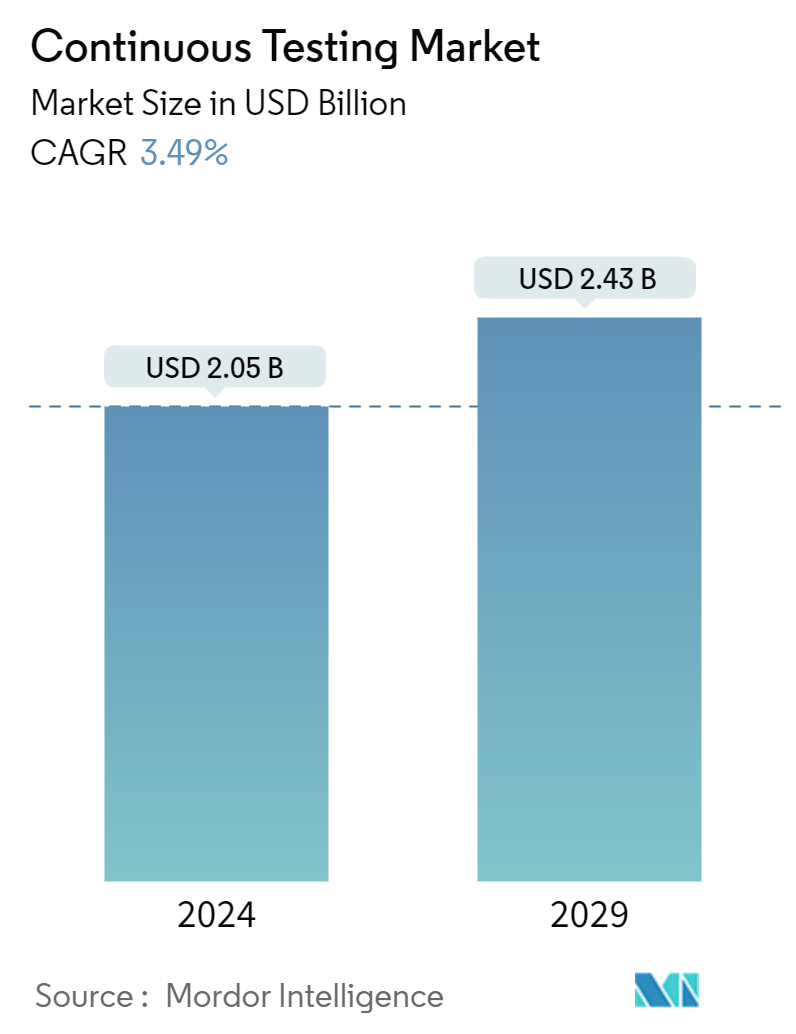

| Market Size (2024) | USD 2.05 Billion |

| Market Size (2029) | USD 2.43 Billion |

| CAGR (2024 - 2029) | 3.49 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Continuous Testing Market Analysis

The Continuous Testing Market size is estimated at USD 2.05 billion in 2024, and is expected to reach USD 2.43 billion by 2029, growing at a CAGR of 3.49% during the forecast period (2024-2029).

The development of the complex IT infrastructure combines physical systems and a virtualized environment, which needs continuous testing for proper feedback and continuous delivery. Continuous integration (CI) is already widespread in the industry. In contrast, there was some missing link in the deployment part, creating an opportunity for continuous testing and continuous deployment.

- The growing digitalization in businesses globally is creating the demand for software development. Also, developing companies are leaning toward increasing efficiency by automating their testing processes. Hence, the growing demand for continuous and timely delivery drives the market's growth.

- Adopting Agile and DevOps approaches for project management also boosts the market's growth. For instance, Tata Consultancy Services is adopting Agile and Business 4.0 concepts for their whole operations. These approaches include continuous testing rather than detecting a problem at the last stage and repeating the process.

- The dependency on traditional approaches and lack of skilled and experienced test automation workforce are hampering the growth of the continuous testing market.

- However, organizations face several challenges related to testing design for continuous testing in terms of proper integration between the different teams across the company, like business analyst teams, development, and QA teams. Although enterprises realize the importance of continuous testing, the deployment of CT has a vividly open landscape, and several companies have yet to adopt it. While there have been significant improvements in adopting continuous testing in each area of the software development lifecycle, enterprises still find it challenging to implement DevOps and continuous delivery.

- Due to the COVID-19 pandemic, several businesses had employees working from home, and the need to adopt CT tools for developers increased substantially. Companies have been increasingly moving their apps to the cloud or cloud-based platforms. Such instances necessitate the adoption of CT tools.

Continuous Testing Industry Segmentation

Continuous testing (CT) is a software development process in which applications are tested continuously throughout the entire software development life cycle (SDLC). The CT aims to improve software quality across the SDLC, providing timely and crucial feedback that will allow better quality and quicker delivery.

The scope of the study for the continuous testing market considers both cloud-based and on-premise deployment solutions provided by vendors in the IT industry globally as part of managed and professional services.

The continuous testing market is segmented by services (managed service and professional service), interface (web, desktop, and mobile), deployment type (on-premise and cloud-based), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Service | |

| Managed Service | |

| Professional Service |

| By Interface | |

| Web | |

| Desktop | |

| Mobile |

| By Deployment Type | |

| On-premise | |

| Cloud-based |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Continuous Testing Market Size Summary

The continuous testing market is poised for significant growth, driven by the increasing complexity of IT infrastructures that blend physical and virtual systems. This growth is fueled by the widespread adoption of Continuous Integration (CI) and the emerging need for Continuous Testing and Continuous Deployment to bridge gaps in deployment processes. As businesses worldwide embrace digitalization, there is a rising demand for efficient software development, prompting companies to automate their testing processes for timely delivery. The integration of Agile and DevOps methodologies further propels market expansion, as these approaches prioritize continuous testing throughout the software development lifecycle. However, challenges such as reliance on traditional methods and a shortage of skilled test automation professionals hinder market progress. Despite these obstacles, the COVID-19 pandemic has accelerated the adoption of continuous testing tools, particularly as companies transition to cloud-based platforms, necessitating quicker deployment and collaboration.

Cloud-based continuous testing plays a pivotal role in the market's growth, offering benefits like reduced time-to-market, seamless team collaboration, and mobile accessibility. The cloud's ability to provide 24/7 support and zero downtime enhances its appeal, as organizations increasingly shift to cloud-based services. This transition is supported by modern technologies and AI-driven solutions, which streamline testing processes and improve efficiency. North America is expected to be the largest contributor to the market, driven by its strong financial position and the need for rapid software development. The region's adoption of Agile and DevOps methodologies has significantly influenced testing activities, with major companies and government entities embracing continuous testing. The market dynamics indicate a growing adoption of continuous testing by enterprises, encouraging vendor activity and driving market growth. Strategic partnerships and acquisitions, such as IBM's acquisition of Red Hat and Tricentis's acquisition of Testim, highlight the industry's focus on enhancing cloud adoption and test automation capabilities.

Continuous Testing Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Intensity of Competitive Rivalry

-

1.3.5 Threat of Substitutes

-

-

1.4 Impact of COVID-19 on the market

-

-

2. MARKET SEGMENTATION

-

2.1 By Service

-

2.1.1 Managed Service

-

2.1.2 Professional Service

-

-

2.2 By Interface

-

2.2.1 Web

-

2.2.2 Desktop

-

2.2.3 Mobile

-

-

2.3 By Deployment Type

-

2.3.1 On-premise

-

2.3.2 Cloud-based

-

-

2.4 By Geography***

-

2.4.1 North America

-

2.4.2 Europe

-

2.4.3 Asia

-

2.4.4 Australia and New Zealand

-

2.4.5 Latin America

-

2.4.6 Middle East and Africa

-

-

Continuous Testing Market Size FAQs

How big is the Continuous Testing Market?

The Continuous Testing Market size is expected to reach USD 2.05 billion in 2024 and grow at a CAGR of 3.49% to reach USD 2.43 billion by 2029.

What is the current Continuous Testing Market size?

In 2024, the Continuous Testing Market size is expected to reach USD 2.05 billion.