Market Overview

| Study Period | 2021 - 2030 |

|---|---|

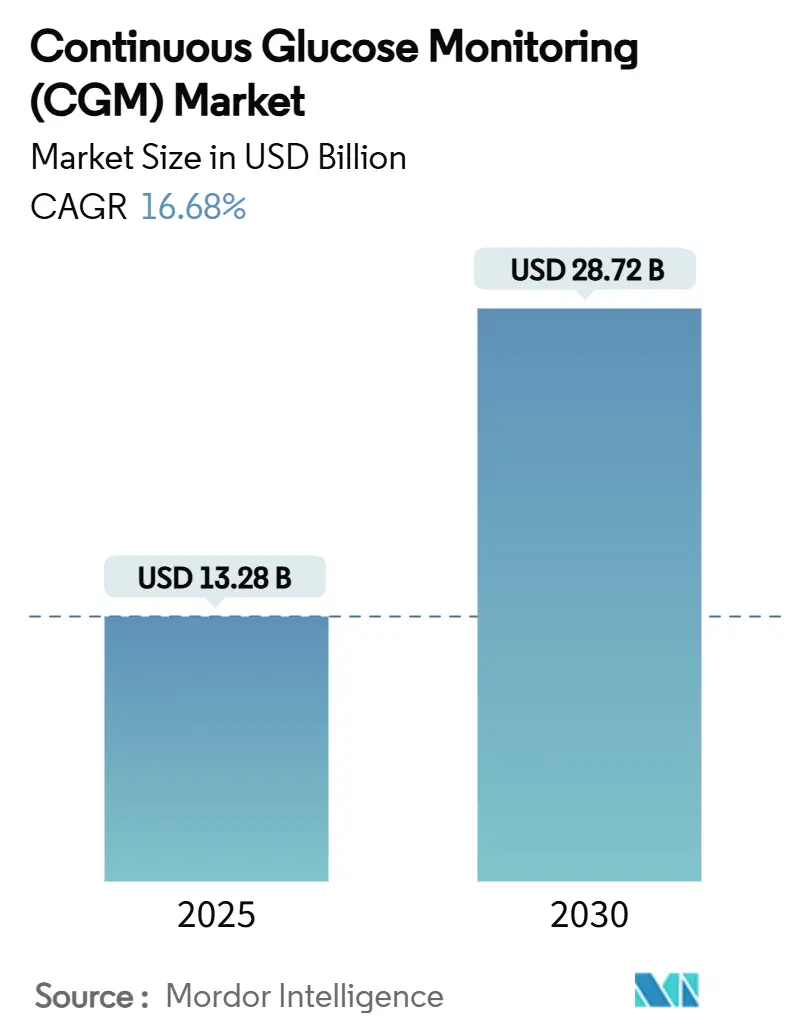

| Market Size (2025) | USD 13.28 Billion |

| Market Size (2030) | USD 28.72 Billion |

| Growth Rate (2025 - 2030) | 16.68% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

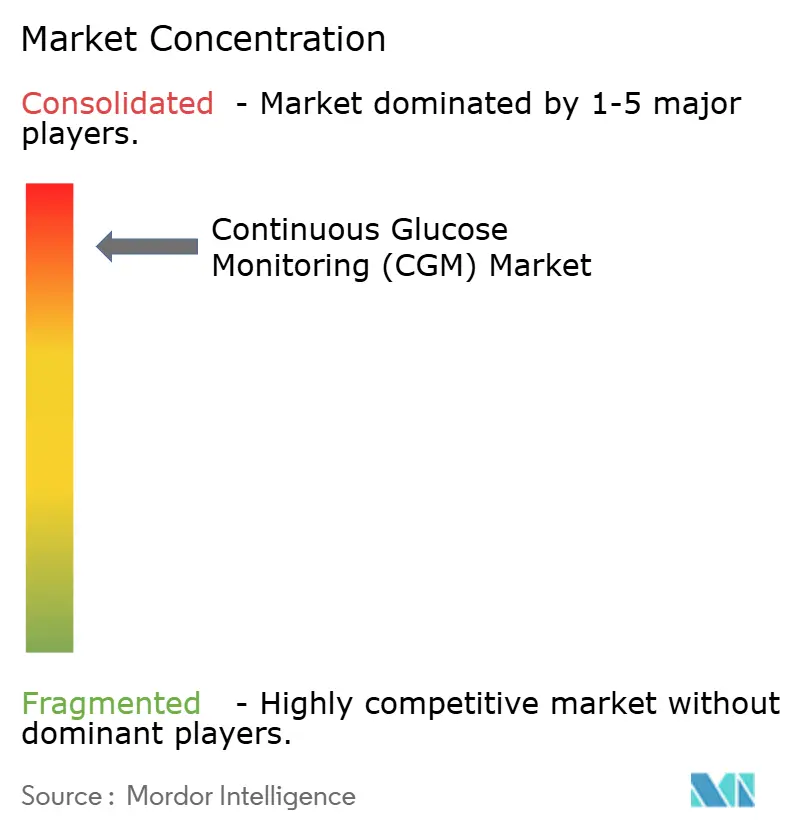

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Continuous Glucose Monitoring (CGM) Market Analysis by Mordor Intelligence

The continuous glucose monitoring market size stands at USD 13,275.19 million in 2025 and is set to reach USD 28,715.26 million by 2030, advancing at a 16.68% CAGR. Robust growth stems from sensor miniaturization, supportive reimbursement, and the blending of consumer wellness with medical necessity. North America leads revenue generation, but Asia Pacific records the fastest uptake as smartphone penetration and diabetes prevalence converge. Ongoing device–software convergence creates recurring revenue streams that entice incumbents to bundle hardware with analytics subscriptions. Meanwhile, implantable and non-invasive prototypes foster expectations that the continuous glucose monitoring market will broaden into preventive and wellness-oriented use cases.

Key Report Takeaways

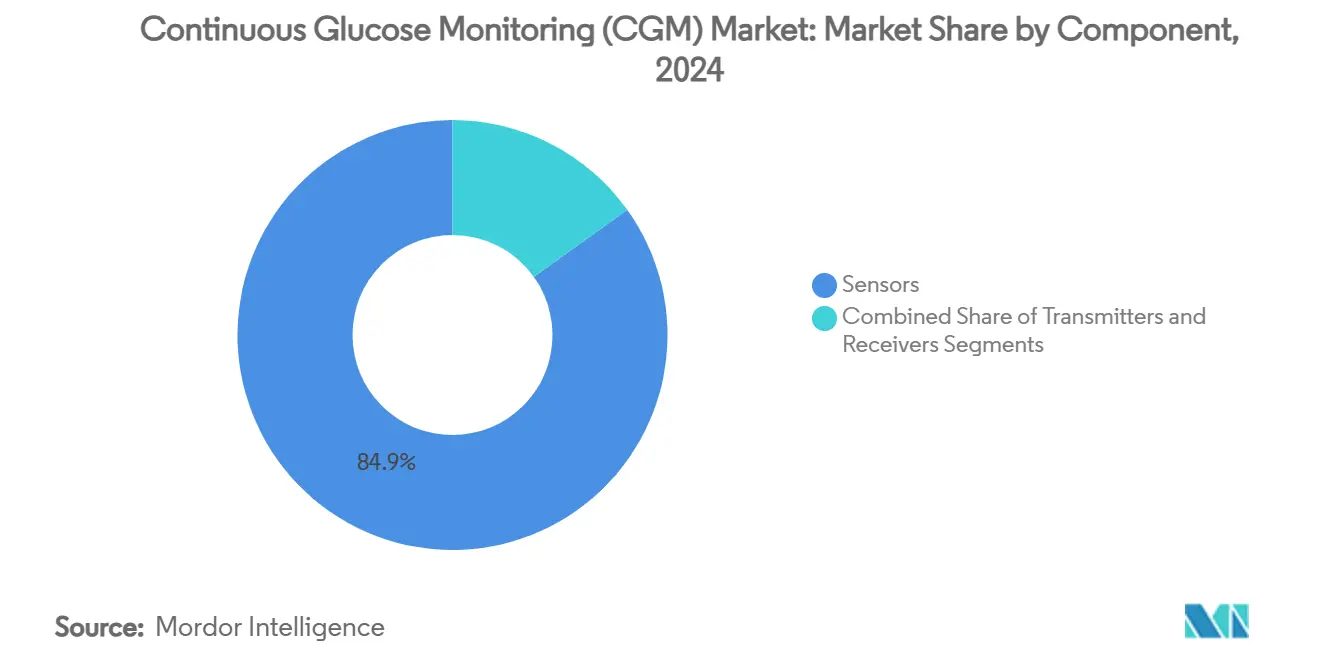

- By component, sensors captured 84.89% of the continuous glucose monitoring market share in 2024; transmitters posted the fastest unit cost declines but only a 6.19% CAGR through 2030.

- By end user, home and personal use commanded a 74.27% share of the continuous glucose monitoring market in 2024, while hospital adoption is projected to expand at an 18.75% CAGR to 2030.

- By demography, pediatric users accounted for 34.27% of 2024 revenue and are advancing at an 18.41% CAGR through 2030.

- By geography, North America retained 51.01% revenue share in 2024; Asia Pacific is forecast to post a 16.08% CAGR to 2030.

- Abbott Laboratories (56.74%), Dexcom (35.20%), and Medtronic (6.88%) together controlled 98.8% of 2024 shipments, underscoring the market’s high concentration.

Global Continuous Glucose Monitoring (CGM) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes and earlier diagnosis | +3.5% | Global; strongest in Asia Pacific and North America | Long term (≥ 4 years) |

| Rapid uptake of remote monitoring and tele-health integration | +2.8% | North America and EU lead; Asia Pacific catching up | Medium term (2-4 years) |

| Sensor miniaturization and accuracy breakthroughs | +2.2% | Global; R&D hubs in North America and Europe | Medium term (2-4 years) |

| Favorable reimbursement expansion in OECD & China | +2.0% | OECD nations and China; spreading to select emerging markets | Short term (≤ 2 years) |

| Consumer-wellness expansion beyond diagnosed diabetes | +1.8% | North America and Europe first movers; global proliferation underway | Long term (≥ 4 years) |

| Subscription pricing lowering LMIC entry barriers | +1.2% | LMIC regions, especially Asia Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes and Earlier Diagnosis

Accelerating incidence underpins structural demand because type 2 accounts for 96% of cases and is trending younger in Asia Pacific, where the median onset now falls below 45 years, creating decades-long monitoring horizons, IDF. Enhanced screening powered by artificial intelligence identifies at-risk cohorts earlier, prompting preventive sensor use. Medicare’s 2024 policy opened access for type 2 patients with hypoglycemic episodes, instantly raising the insured base. Pediatric adoption, already growing at 18.41% CAGR, rides this wave as caregivers view continuous tracking as a safety net for school and sports environments.

Rapid Uptake of Remote Monitoring and Tele-Health Integration

Real-time data streams allow clinicians to manage more people without extra staff, and U.S. CPT-code reimbursements reward providers who deploy remote patient-monitoring kits. Rural patients in the United States and across Europe gain specialist oversight without long drives, improving adherence and glycemic control. Smartphone-native apps cut dedicated receiver costs, lifting barriers for younger, tech-savvy users.

Sensor Miniaturization and Accuracy Breakthroughs

Incremental advances in electrochemical design lowered Mean Absolute Relative Difference readings by up to 30%, increasing clinical trust and loosening calibration schedules. Eversense’s 365-day implantable sensor signals a move from disposable wearables to durable, low-maintenance solutions [1]Senseonics Holdings, “Eversense E3 CGM System,” senseonics.com. Organic electrochemical transistor prototypes are now coin-sized, pointing to future subcutaneous or even fully non-invasive form factors that promise to widen the continuous glucose monitoring market beyond diabetes alone.

Favorable Reimbursement Expansion in OECD & China

The introduction of new HCPCS supply codes in April 2024 lets U.S. providers bill on 90-day cycles, smoothing refill logistics and reducing patient drop-off. In China, provincial payers have begun folding sensors into chronic-disease benefit catalogs, mirroring steps taken earlier in Japan and Germany. Unified European Union expectations for pre-market review simplify cross-border launches and shrink compliance costs. Collectively, policy movement trims out-of-pocket exposure and catalyzes volume growth across insured populations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device and consumable costs | -1.5% | Global; strongest in LMIC and uninsured cohorts | Short term (≤ 2 years) |

| Calibration / data-overload usability concerns | -0.8% | Global; older adults and tech-averse users most affected | Medium term (2-4 years) |

| GLP-1 weight-loss drugs reducing test frequency | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Cyber-security and data-privacy vulnerabilities | -0.4% | Global; high-regulation markets impose stricter mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device and Consumable Costs for Payers and Patients

Sensors that require replacement every 10–14 days cost USD 100–200 per month for U.S. Medicare beneficiaries after coinsurance, straining fixed incomes[2]Centers for Medicare & Medicaid Services, “2024 Medicare Part B—Durable Medical Equipment Rates,” cms.gov . In low- and middle-income countries, unsubsidized retail prices exceed average monthly wages. Although subscription models lower entry costs, they remain out of reach for many. Innovative pay-per-use or outcomes-based contracts could mitigate financial hurdles, yet broad implementation is still nascent.

GLP-1 Weight-Loss Drugs Reducing Glucose Testing Frequency

Blockbuster GLP-1 receptor agonists improve glycemic variability, potentially cutting the perceived need for constant monitoring. Early evidence, however, suggests pairing CGM data with titrated GLP-1 dosing boosts adherence and weight management outcomes. Providers now tap glucose curves to personalize drug regimens, turning an apparent substitute into a complementary demand driver. Nevertheless, some patients with well-controlled numbers may defer sensor upgrades, marginally tempering the continuous glucose monitoring market growth through 2030.

Segment Analysis

By Component: Sensors Dominate as Value Shifts to Data-Rich Interfaces

Sensors delivered 84.89% revenue in 2024, underpinning a 17.84% CAGR that reflects their role as the indispensable physiological touchpoint. Continuous material innovation increased wear life from 10 to 14 days on mainstream disposables, while implantable variants promise annual exchange intervals. Extended longevity directly lowers lifetime ownership costs, making the continuous glucose monitoring market size for sensors the primary engine of topline expansion. Transmitter hardware, by contrast, booked just a 6.19% CAGR as Bluetooth Low Energy modules and direct-to-phone architecture commoditize that layer. Platform vendors now bundle transmitter functions into sensor housings or smartphone apps, pressuring unit margins but captivating consumers through simplified setups.

Second-generation sensor chemistry leverages enzyme stabilization and polymer membranes to curtail drift, enabling more aggressive insulin dosing algorithms and automated insulin delivery integration. Implantable solutions from Glucotrack and Senseonics highlight a migration toward low-profile, maintenance-light devices that could open occupational and athletic niches previously underserved. As sensors evolve into semi-implantable assets, software analytics and cloud subscriptions accrue increasing wallet share, pivoting value creation away from hardware toward longitudinal data services.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Home Care Builds Self-Management Culture

Home and personal users already account for 74.27% of 2024 revenue and are trending at a 15.92% CAGR through 2030. The FDA’s move to allow over-the-counter sensor purchases eliminates prescription friction, letting consumers upgrade directly when new features launch[3]U.S. Food & Drug Administration, “Over-the-Counter Continuous Glucose Monitoring Systems,” fda.gov. Remote patient-monitoring reimbursements also motivate clinicians to prescribe sensors for proactive rather than crisis care, ensuring the continuous glucose monitoring market size expands in tandem with virtual-care infrastructure. Hospital settings, while smaller at 25.73% share, show faster dollar momentum—18.75% CAGR—as continuous readings gain acceptance in perioperative and critical-care workflows where hyperglycemia lengthens stays.

At-home adoption hinges on intuitive apps that gamify targets and alert caregivers in real time. Cloud APIs feed data into tele-diabetes coaching services, transforming episodic finger-stick charts into dynamic behavioral insights. On the inpatient side, staff shortages make continuous feeds attractive because they slash manual testing rounds. Combined, both settings consolidate users around unified data clouds, raising switching costs and reinforcing the duopolistic software ecosystems run by Abbott and Dexcom.

By Demography: Pediatrics Lead High-Growth Cohort

Pediatrics represented 34.27% of 2024 turnover yet advanced at an 18.41% CAGR, outpacing the adult segment’s 15.75% trajectory. Schools, sports teams, and parental monitoring apps underscore how pediatric workflows diverge from adult norms, driving tailored product features such as extended Bluetooth range and discreet profiles. Public-health campaigns that champion early diagnosis further enlarge the continuous glucose monitoring market size within this cohort, as lifetime monitoring needs commence soon after disease onset. Adult uptake remains material but increasingly weighted toward newly diagnosed emerging-market patients and older adults on polypharmacy regimens that heighten hypoglycemia risk.

Pediatric progress also reflects regulatory recognition, such as the U.S. FDA cleared factory-calibrated sensors for patients aged two and above, removing prior age-based prescriptions. In Europe, CE-marked systems integrate with insulin pumps to automate basal adjustments, lightening caregiver burdens. Broadening school health-plan coverage complements these moves, ensuring early access and embedding CGM familiarity that translates into long-term brand loyalty.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North America retained 51.01% share in 2024, supported by entrenched insurance frameworks and high device literacy. The region is forecast to add USD 7.3 billion in incremental sales at an 18.24% CAGR to 2030. Medicare’s April 2024 policy expanded eligibility to type 2 diabetics with documented hypoglycemia, unlocking a latent adult cohort and ensuring sustained unit growth. Canada’s single-payer system aligns formularies nationally, smoothing provincial disparities, while Mexico’s social-security reforms broaden device reimbursement in urban centers.

Asia Pacific, now at 18.18% share, records the steepest CAGR of 16.08%. China’s National Reimbursement Drug List began piloting sensor inclusion in 2025, and domestic manufacturers are scaling to meet tier-2 city demand. India’s high smartphone penetration, coupled with pay-as-you-go insurance apps, lowers household entry barriers. Japan and South Korea maintain high per-capita uptake because consumer-electronics majors embed glucose modules into multipurpose wearables, a trend likely to ripple across Southeast Asia.

Europe offers mid-single-digit growth underpinned by universal coverage and coordinated procurement. Germany champions CGM as the standard of care for type 1 patients, while the United Kingdom’s NHS Long-Term Plan subsidizes hardware upgrades to factory-calibrated models. Eastern European markets emerge as white space; Czechia and Poland introduced pilot funding in 2025, leveraging EU structural funds to modernize diabetes care.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The continuous glucose monitoring market is highly concentrated: Abbott controls 56.74% of 2024 revenue, Dexcom accounts for 35.20%, and Medtronic represents 6.88%. Collectively, the top three own 98.8%, leaving merely 1.2% for niche or emergent players. Such dominance funds large-scale R&D, which is evident in Abbott’s launch of its fourth-generation sensor with integrated ketone readings, which was announced in June 2025. Dexcom counters with a vertically integrated cloud ecosystem that layers predictive analytics onto raw glucose curves to enhance clinician workflow.

Strategic alliances reinforce incumbent moats. Abbott and Medtronic signed a global data-sharing and pump-integration agreement in August 2024, allowing Libre sensors to drive Medtronic’s closed-loop systems. Concurrently, Tandem Diabetes linked with Abbott to co-develop dual-analyte sensors covering glucose and ketones for comprehensive metabolic oversight. Patent détente between Abbott and Dexcom in early 2025 curtailed litigation and opened cross-licensing that accelerates miniaturization and wear-time objectives.

Emerging disruptors target technological white space. Senseonics secured CE-mark for a year-long implantable sensor; RSP Systems published peer-reviewed validation of its optical GlucoBeam in Nature Scientific Reports, reporting accuracy comparable to fingerstick references. Glucotrack advanced a minimally invasive implantable device that uses impedance spectroscopy and obtained Australian HREC approval for its pivotal trial in May 2025. Still, heavy regulatory barriers and clinical-evidence demands keep wide-scale competition limited, sustaining premium pricing and high gross margins for the leading duopoly.

Continuous Glucose Monitoring (CGM) Industry Leaders

-

Medtronic Plc

-

Dexcom, Inc.

-

Abbott Laboratories

-

Senseonics Holdings, Inc.

-

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Tandem Diabetes and Abbott began co-developing a glucose-ketone sensor platform aimed at mitigating diabetic ketoacidosis risk.

- May 2025: Glucotrack gained Australian HREC approval to commence clinical trials for its implantable continuous blood glucose monitor.

- April 2025: RSP Systems’ optical GlucoBeam secured peer-review validation in Nature Scientific Reports, evidencing non-invasive accuracy on par with capillary sampling.

- August 2024: Abbott and Medtronic formalized a partnership to link FreeStyle Libre sensors with Medtronic’s insulin pumps for automated therapy.

- February 2024: The U.S. FDA issued a warning letter citing manufacturing deficiencies at Dexcom’s San Diego plant, prompting a quality-improvement roadmap.

Global Continuous Glucose Monitoring (CGM) Market Report Scope

As per the scope of the report, patients can manage type 1 or type 2 diabetes with the use of continuous glucose monitoring (CGM) devices by performing fewer fingerstick tests. Blood sugar levels are continuously monitored by a sensor located just under the skin. Results are sent via a transmitter to a cell phone or wearable technology. The continuous glucose monitoring market is segmented by component, end user, and geography. By component, the market is segmented into sensors and durables. The end user segment is further divided into hospitals/clinics and home/personal. The report also covers the market sizes and forecasts for major countries across different regions. The market size is provided for each segment in terms of value (USD).

By Component

| Sensors |

| Transmitters |

| Receivers |

By End User

| Hospitals / Clinics |

| Home / Personal |

By Demography

| Adult |

| Paediatric |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | Japan |

| South Korea | |

| China | |

| India | |

| Australia | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Philippines | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| Iran | |

| Egypt | |

| Oman | |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Sensors | |

| Transmitters | ||

| Receivers | ||

| By End User | Hospitals / Clinics | |

| Home / Personal | ||

| By Demography | Adult | |

| Paediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| South Korea | ||

| China | ||

| India | ||

| Australia | ||

| Vietnam | ||

| Malaysia | ||

| Indonesia | ||

| Philippines | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| Iran | ||

| Egypt | ||

| Oman | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the continuous glucose monitoring market?

The continuous glucose monitoring market size is USD 13.28 billion in 2025, with a projected 16.68% CAGR to 2030.

Which component segment is growing fastest?

Sensors, which already hold 84.89% share, are advancing at 17.84% CAGR due to longer wear life and higher accuracy.

Why is North America the largest regional market?

Medicare coverage expansion, high technology adoption, and established reimbursement structures support a 51.01% revenue share and an 18.24% CAGR outlook.

How do GLP-1 weight-loss drugs affect CGM demand?

While better glycemic control might reduce testing frequency, providers increasingly pair CGM with GLP-1 therapy for precision titration, mitigating any negative impact.

What advances are expected in CGM technology by 2030?

Implantable 365-day sensors and validated non-invasive optical monitors are in late-stage development, promising greater comfort and broader wellness applications.

Page last updated on: