| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.29 % |

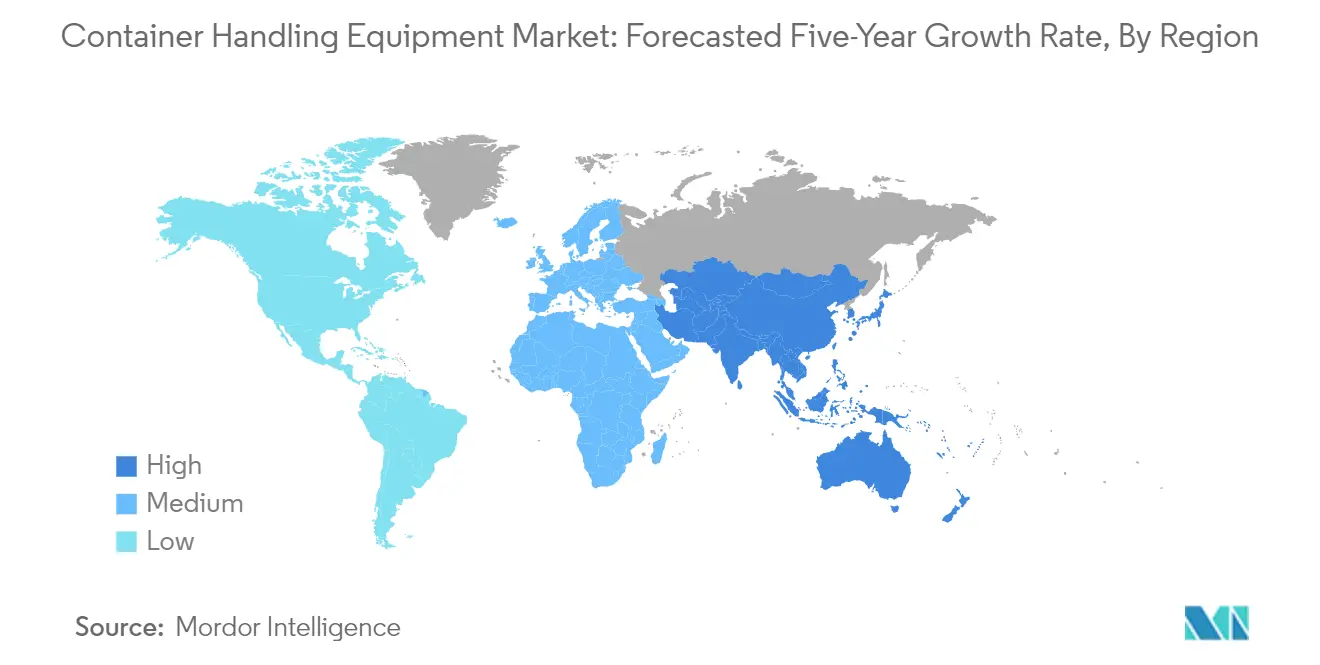

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

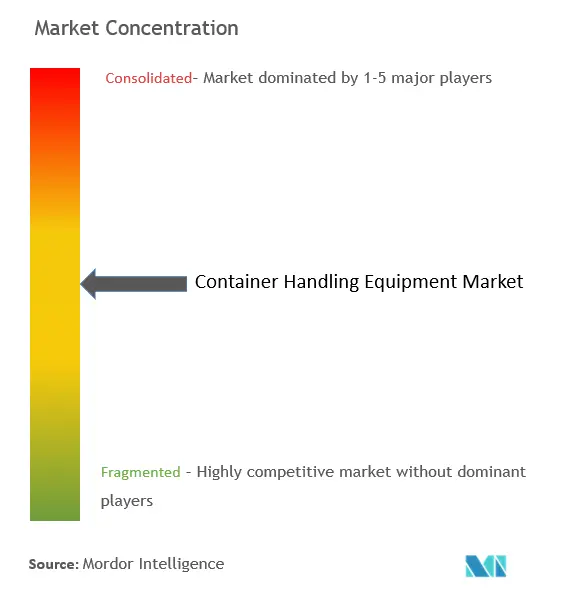

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Container Handling Equipment Market Analysis

The Container Handling Equipment Market is expected to register a CAGR of 4.29% during the forecast period.

The container handling equipment industry continues to evolve amid transformative global trade dynamics and technological advancements. Maritime shipping remains the backbone of international commerce, with seaborne transport accounting for over 60% of global trade value, highlighting the critical role of efficient container handling equipment infrastructure. The industry is witnessing significant expansion in port infrastructure worldwide, particularly in emerging economies, to accommodate growing trade volumes. This expansion is driven by the projection that global freight volumes will triple over the next three decades, necessitating substantial investments in modern container handling equipment and infrastructure.

The industry is experiencing a dramatic shift toward automation and digital transformation, revolutionizing traditional port operations. Terminal operators are increasingly adopting automated solutions, from automated stacking cranes to self-driving container handling transport vehicles, to enhance operational efficiency and safety. This trend is exemplified by recent developments such as ZPMC's introduction of the AI-Strad autonomous straddle carrier in late 2023, representing the next generation of intelligent container handling equipment solutions. The integration of artificial intelligence and IoT technologies is becoming increasingly prevalent in modern port operations, enabling predictive maintenance and real-time monitoring capabilities.

Environmental sustainability has emerged as a central focus in the container handling equipment sector, driving significant innovations in equipment design and power systems. Terminal operators are actively transitioning to eco-friendly solutions, as demonstrated by SSA Marine's successful retrofit project that achieved a remarkable 95% reduction in diesel emissions through the conversion to battery power. This shift towards sustainable operations is reshaping the industry's approach to equipment design and procurement, with container handling equipment manufacturers increasingly focusing on developing zero-emission alternatives to traditional diesel-powered equipment.

The industry is witnessing a fundamental transformation in equipment propulsion technologies, with a clear trend toward electrification and hybrid solutions. Major ports and terminal operators are investing heavily in electric and hybrid port handling equipment to reduce their environmental impact while simultaneously lowering operational costs. This transition is supported by technological advancements in battery systems and charging infrastructure, enabling longer operating hours and improved performance. The industry's commitment to sustainability is further evidenced by the growing adoption of regenerative energy systems in modern container handling equipment, which can recover and reuse up to 40% of the energy generated during operations, significantly reducing overall energy consumption.

Container Handling Equipment Market Trends

Growing Global Trade and Maritime Cargo Volumes

The substantial increase in international trade volumes continues to be a primary driver for the container handling equipment market. Maritime cargo transport accounts for more than 60% of the total global trade value, representing an enormous demand for efficient container handling infrastructure at ports worldwide. This dominance of sea freight transportation has led countries to make significant investments in developing their shipping processes and port infrastructure, including modernizing their container handling operations. The steady growth trajectory is evidenced by the increase in global goods loaded, which rose from 5.683 billion metric tons in 1999 to 11.076 billion metric tons in 2019, demonstrating the expanding scale of maritime commerce.

The future outlook appears even more promising, with projections indicating that global freight volumes will triple over the next three decades. This anticipated surge in cargo movement is compelling ports and terminals worldwide to enhance their operational capabilities through advanced container handling equipment. As countries strive to increase their trade-based economic growth, they are investing heavily in port infrastructure development projects. These investments encompass not only the expansion of existing facilities but also the implementation of more efficient and technologically advanced container handling systems to manage the growing cargo volumes effectively.

Understand The Key Trends Shaping This Market

Download PDF

Growing Emphasis on Electrification and Environmental Efficiency

The container handling equipment industry is experiencing a transformative shift toward electrification and environmental sustainability, driven by increasingly stringent emission regulations and operational cost considerations. Port operators and terminal managers worldwide are actively seeking ways to reduce their environmental impact while simultaneously lowering operational costs. This trend is exemplified by successful implementations such as the Port of Oakland's initiative, where the retrofitting of rubber-tired gantry (RTG) cranes to battery power achieved a remarkable 95% reduction in diesel emissions, eliminating approximately 1,200 metric tons of greenhouse gas emissions annually per crane.

The industry's commitment to eco-efficiency is further demonstrated by technological innovations in electric and hybrid systems. Modern electric container handling equipment can now produce and recover its own energy, with some systems achieving up to a 40% reduction in energy consumption through innovative energy recovery mechanisms during load lowering operations. This advancement is complemented by the development of new products, such as Sarens' electric ring crane, which combines maximum load handling capabilities with environmentally friendly operations. The trend toward electrification is also supported by port authorities' ambitious environmental goals, with many facilities implementing comprehensive emission reduction plans and transitioning their equipment fleets to electric power. These initiatives are further bolstered by new emission standards from environmental protection agencies, requiring newly purchased yard equipment to meet stringent Tier 4 final off-road engine specifications or equivalent modern standards.

Segment Analysis: Equipment Type

Forklift Truck Segment in Container Handling Equipment Market

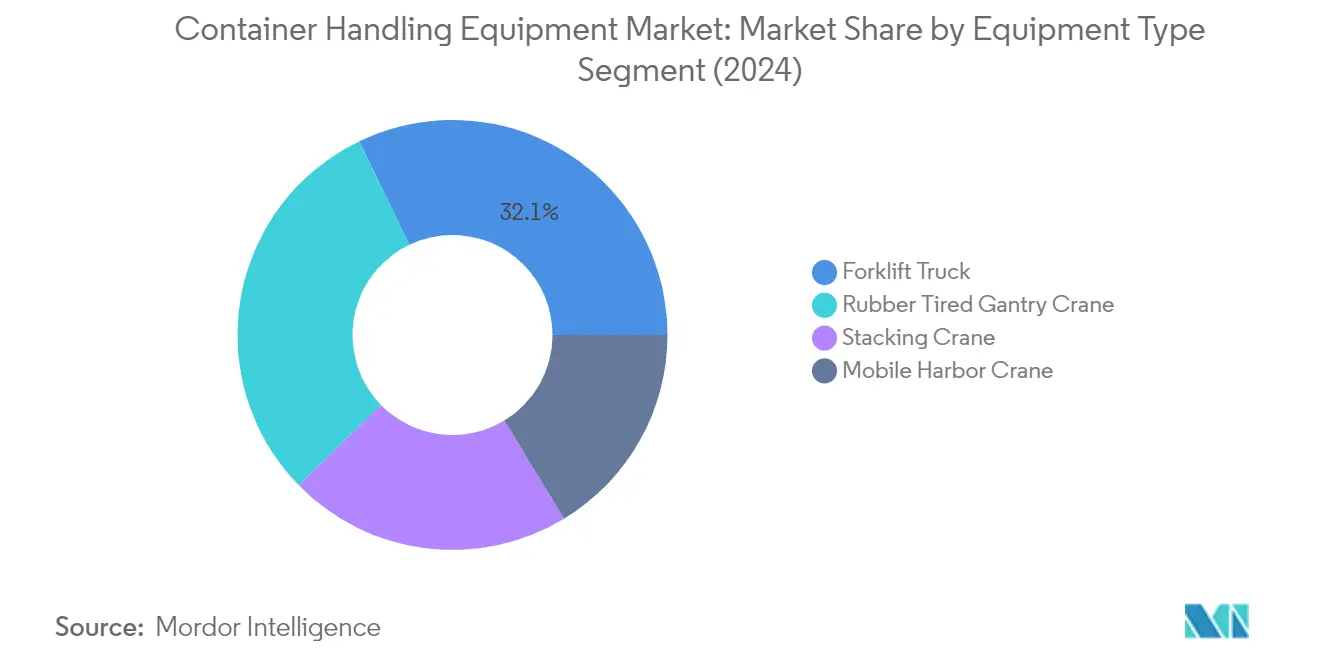

The forklift truck segment maintains its dominant position in the container handling equipment market, commanding approximately 32% of the total market share in 2024. This leadership position is attributed to the segment's versatility and wide-ranging applications across different fields, including construction, manufacturing, and port-handling operations. The rapid expansion of e-commerce, retail, and logistics industries, especially in developing economies such as India, Brazil, Singapore, and Mexico, has significantly boosted forklift truck demand. Many manufacturers are actively introducing new electric and hybrid models to meet growing environmental concerns and efficiency requirements, with features like improved travel speeds, enhanced lift capabilities, and increased run-time efficiency compared to conventional models. The segment's strong performance is further supported by the high level of activity in sectors such as food and beverages, transport and storage, and retail and wholesale distribution.

Rubber Tired Gantry Crane Segment in Container Handling Equipment Market

The rubber-tired gantry (RTG) crane segment is projected to experience the highest growth rate in the container handling equipment market from 2024 to 2029. This growth trajectory is driven by the increasing adoption of RTG cranes in the world's largest container terminals and container storage yards for efficient stacking operations. The segment's expansion is further supported by the rising trend toward automation and electrification of port equipment, with several terminals implementing automated RTG systems to enhance operational efficiency and reduce environmental impact. Major ports worldwide are investing in RTG crane installations as part of their modernization efforts, with many opting for eco-efficient variants, including electric and hybrid models that offer substantial reductions in emissions and operational costs. The segment's growth is also bolstered by technological advancements in RTG designs, including the integration of remote control capabilities and automation features.

Remaining Segments in Equipment Type

The stacking crane and mobile harbor crane segments continue to play vital roles in the container handling equipment market, each serving specific operational needs in port and terminal operations. Stacking cranes offer unique advantages with their ability to move materials above existing loads and provide 360-degree swivel capabilities, making them essential for space-efficient storage operations. Mobile harbor cranes, on the other hand, provide the flexibility needed for maritime applications such as loading and unloading containers to or from ships and handling shipyard materials. Both segments are witnessing technological advancements, particularly in areas of automation and electrification, contributing to improved operational efficiency and reduced environmental impact in port operations.

Segment Analysis: Propulsion Type

Diesel Segment in Container Handling Equipment Market

The diesel propulsion segment continues to dominate the container handling equipment market, commanding approximately 64% of the total market share in 2024. This significant market position is primarily attributed to diesel engines' high power density and cost advantages compared to hybrid/electric systems. In the world of power transmission systems, fluid power systems remain popular due to their reliability and proven performance in heavy-duty applications. Diesel-powered equipment maintains its dominance particularly in high-power container material handling equipment applications where the power requirements are too substantial for pure electric alternatives. The segment's strength is further reinforced by the continuous improvements in engine efficiency and the implementation of advanced Tier 4 engine technology, which has helped reduce emissions while maintaining the robust performance characteristics required in port operations.

Hybrid Segment in Container Handling Equipment Market

The hybrid propulsion segment is emerging as the fastest-growing category in the container handling equipment market, projected to grow at approximately 6% during the forecast period 2024-2029. This accelerated growth is driven by the increasing focus on sustainability and the advantages offered by diesel-electric hybrid systems, which allow equipment to operate with smaller engines at lower RPMs, resulting in improved fuel efficiency and reduced emissions. The segment's growth is further propelled by stringent emission regulations across major ports worldwide and the rising demand for eco-friendly equipment solutions. Hybrid systems are particularly gaining traction in container terminal handling equipment types like forklifts, mobile harbor cranes, and rubber-tired gantry cranes, where they offer an optimal balance between power requirements and environmental considerations.

Remaining Segments in Propulsion Type

The electric propulsion segment, while currently holding a smaller market share, represents a significant area of technological advancement in the container handling equipment market. This segment is characterized by fully electric solutions that offer zero-emission operations, making them particularly attractive for ports and terminals focusing on environmental sustainability. The development of electric container material handling equipment has been progressing steadily, with manufacturers introducing new models and technologies. The segment's growth is supported by various government incentive programs and the increasing focus on port electrification initiatives, particularly in developed markets where electrical infrastructure is more advanced. Despite current limitations in power output compared to diesel alternatives, electric propulsion systems are gaining acceptance, especially in smaller capacity equipment and specific applications where continuous power supply infrastructure is readily available.

Container Handling Equipment Market Geography Segment Analysis

Container Handling Equipment Market in North America

North America represents a significant container handling equipment market, driven by extensive port infrastructure development and modernization initiatives across the United States and Canada. The region's market is characterized by the increasing adoption of automated container handling equipment solutions and a strong focus on environmental sustainability in port operations. The presence of major ports along both the Pacific and Atlantic coasts contributes to steady demand for advanced port cargo handling equipment, while ongoing investments in port expansion projects continue to shape market dynamics.

Container Handling Equipment Market in the United States

The United States dominates the North American container handling equipment market, holding approximately 80% market share in 2024. The country's leadership position is supported by its extensive network of over 20 container ports, with the Port of Los Angeles being the busiest. The market is driven by significant investments in port automation technologies and the increasing adoption of zero-emission container handling equipment. Major ports across the country are actively transitioning towards more sustainable operations, with several facilities implementing battery-electric and hybrid handling equipment to reduce their environmental impact.

Growth Dynamics in the United States

The United States is also leading the region's growth trajectory, with a projected CAGR of approximately 4% from 2024 to 2029. This growth is primarily driven by ongoing port modernization initiatives and the increasing focus on automated container handling services. The country's ports are actively investing in advanced technologies such as automated stacking cranes and electric container handling equipment. The implementation of stringent emission regulations and the push towards sustainable port operations are further catalyzing the adoption of new-generation container handling equipment across major US ports.

Container Handling Equipment Market in Europe

Europe represents a mature container handling equipment market, characterized by advanced port infrastructure and a strong emphasis on technological innovation. The region's market is driven by significant investments in port automation and sustainable handling solutions across Germany, the United Kingdom, and France. European ports are at the forefront of adopting electric and hybrid container handling equipment, reflecting the region's strong commitment to reducing environmental impact in port operations.

Container Handling Equipment Market in Germany

Germany leads the European container handling equipment market, commanding approximately 39% market share in 2024. The country's dominance is supported by its extensive network of ports, including Hamburg, Bremerhaven, and Wilhelmshaven, which serve as major transshipment and gateway ports. The German market is characterized by high adoption rates of automated container handling equipment solutions and significant investments in port infrastructure development.

Growth Dynamics in Germany

Germany, along with the United Kingdom, demonstrates strong growth potential with a projected CAGR of approximately 4% from 2024 to 2029. The growth is driven by ongoing port expansion projects and the increasing adoption of automated container handling systems. German ports are actively investing in electric and hybrid handling equipment, reflecting the country's commitment to sustainable port operations. The market is further supported by strong manufacturing capabilities and technological innovation in the container handling equipment sector.

Container Handling Equipment Market in Asia-Pacific

The Asia-Pacific region represents a dynamic container handling equipment market, driven by rapid industrialization and expanding international trade activities. Countries like China, India, Japan, and South Korea are making significant investments in port infrastructure development and modernization. The region is witnessing increasing adoption of automated container handling equipment solutions and sustainable equipment, particularly in major maritime hubs.

Container Handling Equipment Market in China

China maintains its position as the dominant force in the Asia-Pacific container handling equipment market. The country's leadership is supported by its extensive network of 34 container ports and 2,000 minor ports, with Shanghai being the world's largest port. China's market is characterized by significant investments in port automation technologies and indigenous manufacturing capabilities for container handling equipment.

Growth Dynamics in India

India emerges as the fastest-growing market in the Asia-Pacific region. The country's growth is driven by ambitious port development initiatives under the Sagarmala Programme and an increasing focus on port modernization. Indian ports are actively adopting advanced container handling equipment technologies and sustainable equipment solutions to enhance operational efficiency and reduce environmental impact.

Container Handling Equipment Market in Rest of the World

The Rest of the World region, encompassing Brazil, the United Arab Emirates, and other countries, presents diverse opportunities in the container handling equipment market. This region is characterized by ongoing port development projects and increasing investments in modern port handling equipment infrastructure. Brazil stands out as a significant market with its extensive maritime terminal network, while the United Arab Emirates leads in terms of technological adoption and port automation. The region demonstrates varying levels of market maturity, with some areas focusing on basic infrastructure development while others are advancing towards automated and sustainable handling solutions.

Get Analysis on Important Geographic Markets

Download PDF

Container Handling Equipment Industry Overview

Top Companies in Container Handling Equipment Market

The container handling equipment market features several prominent players, including Konecranes, Liebherr, SANY Group, Hyster-Yale, Cargotec, and ZPMC, leading the industry through continuous innovation and strategic expansion. These container handling companies are increasingly focused on developing automated and electric equipment solutions to meet growing environmental regulations and efficiency demands. The industry is witnessing a strong trend toward smart port solutions, with manufacturers integrating IoT and AI capabilities into their product offerings. Companies are expanding their global footprint through strategic partnerships and local manufacturing facilities, particularly in emerging markets. Product development efforts are centered on enhancing operational efficiency, reducing emissions, and improving safety features, while service networks are being strengthened to provide comprehensive after-sales support and maintenance services.

High Consolidation with Strong Regional Players

The container handling equipment market exhibits a relatively consolidated structure dominated by large multinational corporations with extensive manufacturing capabilities and established distribution networks. These major players possess significant advantages through their integrated operations, spanning research and development, manufacturing, and after-sales services. The market is characterized by a mix of global conglomerates offering complete port equipment solutions and specialized manufacturers focusing on specific equipment categories. Regional players maintain strong positions in their respective markets through local manufacturing facilities and established customer relationships.

The industry has witnessed significant merger and acquisition activity aimed at expanding product portfolios and geographical reach. Notable among these is the planned merger between Konecranes and Cargotec, indicating a trend toward further market consolidation. Companies are increasingly pursuing strategic partnerships to enhance their technological capabilities and expand their market presence. The high barriers to entry, including substantial capital requirements and technical expertise, have limited the emergence of new players, contributing to the market's consolidated nature.

Innovation and Service Network Drive Success

Success in the container handling equipment manufacturers market increasingly depends on manufacturers' ability to develop innovative solutions that address automation, sustainability, and efficiency requirements. Companies must invest heavily in research and development to create products that comply with stringent environmental regulations while meeting the growing demand for automated port operations. The establishment of comprehensive container handling services networks and the ability to provide integrated solutions, including equipment monitoring and maintenance services, have become crucial differentiating factors. Market leaders are focusing on developing digital capabilities and implementing predictive maintenance solutions to enhance their competitive position.

For new entrants and smaller players, success lies in identifying and serving specific market niches or geographical regions where they can establish strong positions. The development of specialized products addressing specific customer needs and the ability to provide competitive pricing and superior local support services are essential strategies. Companies must also consider the increasing importance of end-user relationships, as port operators and terminal management companies exercise significant influence over equipment selection. The risk of substitution remains relatively low due to the specialized nature of container handling equipment, though manufacturers must continue to innovate to maintain their market positions and address evolving customer requirements.

Container Handling Equipment Market Leaders

-

SANY Group

-

Liebherr Group

-

Konecranes

-

Cargotec Corporation

-

Hyster-Yale Materials Handling, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Container Handling Equipment Market News

- May 2023: Toyota Material Handling introduced three new electric forklift models. The new electric product consists of features a Side-Entry End Rider, a Center Rider Stacker, and an Industrial Tow Tractor.

- April 2023: Clark Material Handling Company expanded its GEX20-30L and GEX40-50 electric forklift series to include models with an 80 V lithium-ion battery (Li-ion). The new series extended the product range in the segment of electric counterbalance trucks with Li-ion technology.

Container Handling Equipment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Growing Emphasis on The Electrification of Container Handling Equipment

-

4.2 Market Restraints

- 4.2.1 High Capital Cost And Increasing Complexity of Container Handling Equipment

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Value (USD))

-

5.1 By Equipment Type

- 5.1.1 Forklift Truck

- 5.1.2 Stacking Crane

- 5.1.3 Mobile Harbor Crane

- 5.1.4 Rubber-tired Gantry Crane

-

5.2 By Propulsion Type

- 5.2.1 Diesel

- 5.2.2 Electric

- 5.2.3 Hybrid

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 south America

- 5.3.4.2 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles*

- 6.2.1 Cargotec Corp.

- 6.2.2 Liebherr Group

- 6.2.3 SANY Group

- 6.2.4 Shanghai Zhenhua Heavy Industries Co. Ltd (ZPMC)

- 6.2.5 Hyster-Yale Materials Handling Inc.

- 6.2.6 Anhui HELI Forklifts Group Co. Ltd

- 6.2.7 Hoist Material Handling Inc.

- 6.2.8 CVS Ferrari SpA

- 6.2.9 Lonking Holdings Limited

- 6.2.10 Konecranes

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Container Handling Equipment Industry Segmentation

Container handling equipment is used to transport the container from one place to another. Container handling equipment is widely used in ports, logistics and warehouse industries, and others.

The container handling equipment market is segmented by equipment type, propulsion type, and geography. By equipment type, the market is segmented into forklift trucks, stacking cranes, mobile harbor cranes, and rubber-tired gantry cranes. By propulsion type, the market is segmented into diesel, electric, and hybrid. By geography, the market is segmented as North America, Europe, Asia-Pacific, and the rest of the world. For each segment, the market sizing and forecast are done based on the value (USD).

| By Equipment Type | Forklift Truck | ||

| Stacking Crane | |||

| Mobile Harbor Crane | |||

| Rubber-tired Gantry Crane | |||

| By Propulsion Type | Diesel | ||

| Electric | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | south America | ||

| Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Container Handling Equipment Market Research FAQs

What is the current Container Handling Equipment Market size?

The Container Handling Equipment Market is projected to register a CAGR of 4.29% during the forecast period (2025-2030)

Who are the key players in Container Handling Equipment Market?

SANY Group, Liebherr Group, Konecranes, Cargotec Corporation and Hyster-Yale Materials Handling, Inc. are the major companies operating in the Container Handling Equipment Market.

Which is the fastest growing region in Container Handling Equipment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Container Handling Equipment Market?

In 2025, the Asia Pacific accounts for the largest market share in Container Handling Equipment Market.

What years does this Container Handling Equipment Market cover?

The report covers the Container Handling Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Container Handling Equipment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Container Handling Equipment Market Research

Mordor Intelligence provides a comprehensive analysis of the container handling equipment market. We leverage extensive expertise in port equipment market research and consulting. Our detailed report covers the full spectrum of container handling equipment. This includes port handling equipment, cargo handling equipment, and specialized container material handling equipment. The analysis includes major container handling equipment manufacturers and their innovations in port cargo handling equipment. It provides crucial insights into container handling services and operational efficiency.

Stakeholders across the industry, from container handling companies to end-users seeking container handling equipment for sale, benefit from our thorough examination of market dynamics. The report is available as an easy-to-download PDF. It provides detailed analysis of port container handling equipment trends, container terminal handling equipment developments, and emerging opportunities in container port equipment segments. Our research covers comprehensive evaluations of hoist container handlers, port material handling equipment, and various equipment container solutions. This offers valuable insights for strategic decision-making in the evolving logistics landscape.