Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

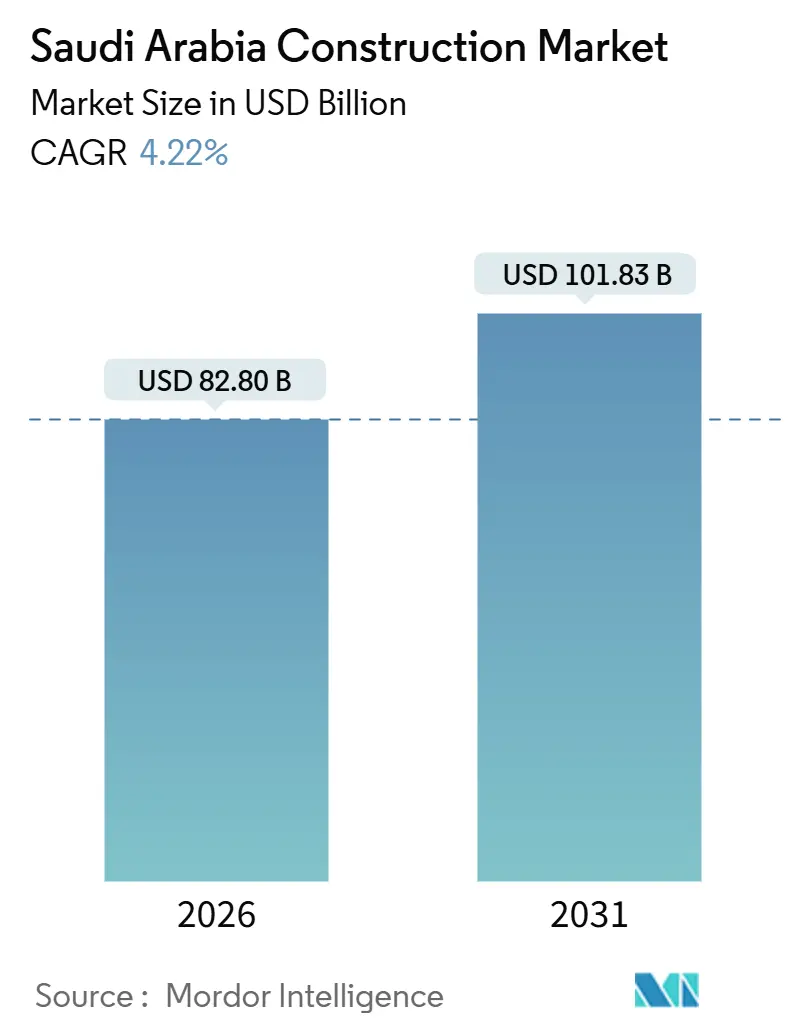

| Market Size (2026) | USD 82.80 Billion |

| Market Size (2031) | USD 101.83 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

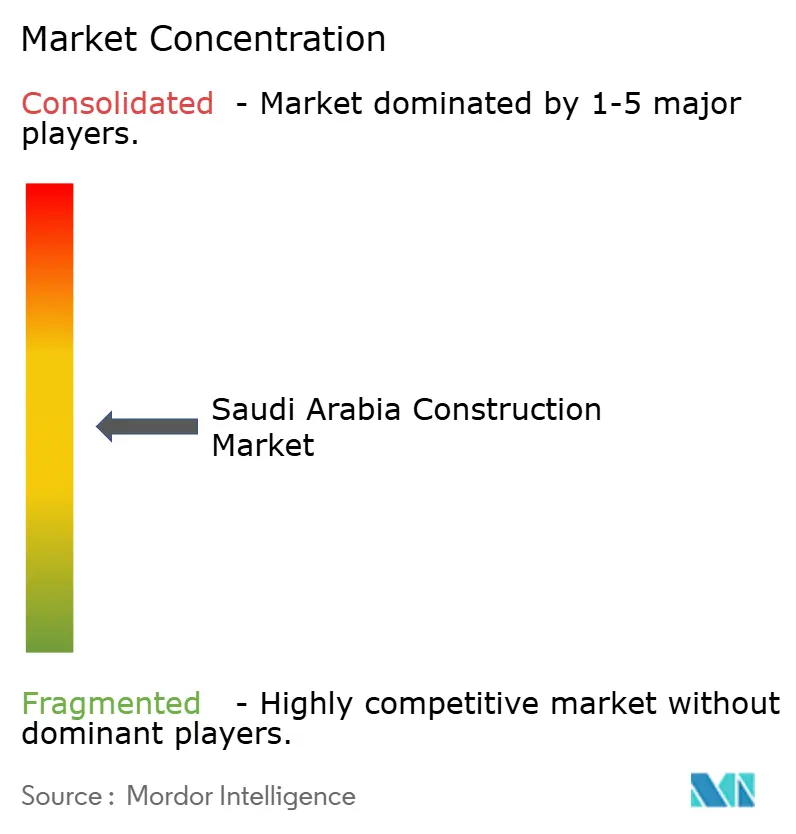

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Construction Market Analysis by Mordor Intelligence

The Saudi Arabia construction market size stands at USD 82.80 billion in 2026, and it is projected to reach USD 101.83 billion by 2031, advancing at a 4.22% CAGR over the forecast period. Robust public‐sector capital deployment under Vision 2030, the steady roll-out of giga-projects, and large-scale housing initiatives provide a multi-year pipeline that reduces exposure to oil-price swings and typical commodity cycles. Transport corridors such as the Riyadh Metro and the Land Bridge rail elevate logistics connectivity, while the Public Investment Fund’s USD 30 billion outlay in 2024 underscores the counter-cyclical role of sovereign spending. Residential demand is accelerating as Sakani nudges national homeownership toward 70%, and ROSHN commits to 400,000 units by 2030. Rising use of prefabrication, alongside mandatory BIM for mega-projects, is starting to compress schedules and ease labour bottlenecks.

Key Report Takeaways

- By sector, infrastructure led with a 60.26% revenue share in 2025, while residential is forecast to expand at a 4.10% CAGR through 2031.

- By construction type, new construction accounted for 85.10% of the Saudi Arabia construction market share in 2025, whereas renovation is the fastest-growing niche at a 4.12% CAGR to 2031.

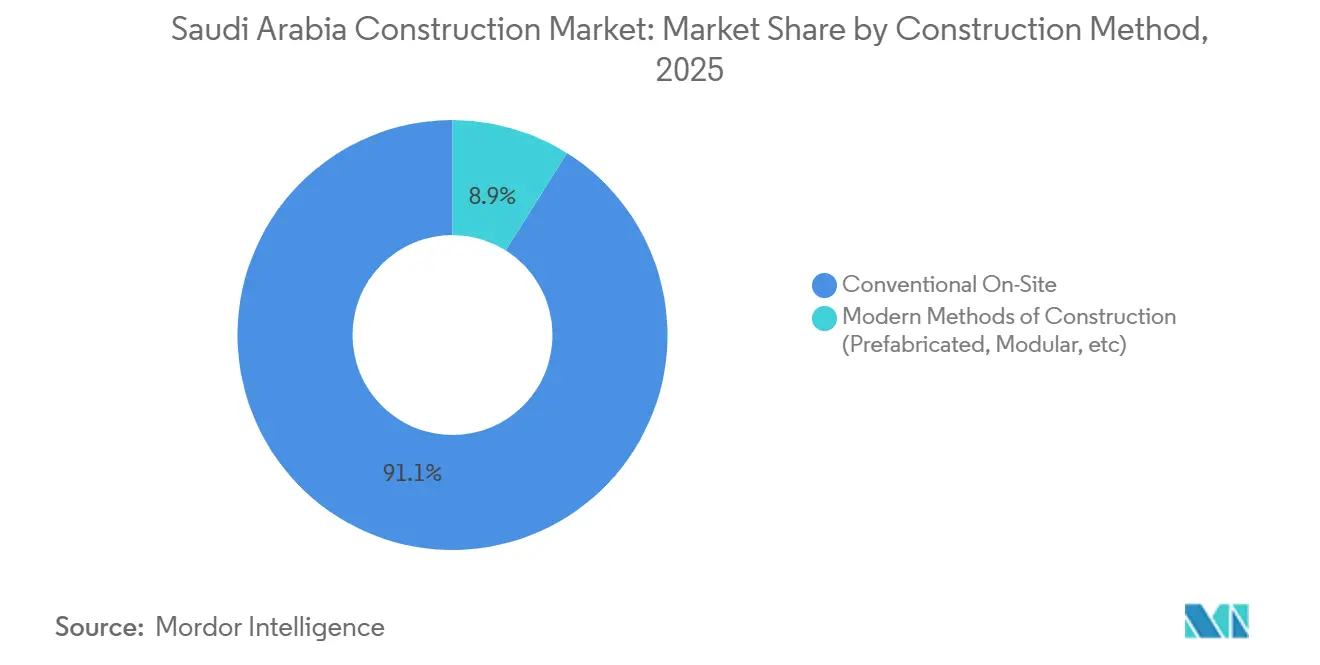

- By construction method, conventional on-site techniques held an 91.07% share in 2025, but modern methods of construction are poised to grow at a 5.53% CAGR to 2031.

- By investment source, public spending captured 63.29% of the 2025 value, yet private capital is projected to rise at a 4.18% CAGR through 2031.

- By city cluster, Riyadh commanded 24.41% of the 2025 value, while the Rest of Saudi Arabia—anchored by NEOM, the Red Sea, and Tabuk—should expand at a 4.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Construction Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga- and mega-projects anchoring multi-year pipelines across asset classes | +1.8% | National, concentrated in NEOM, Tabuk, Makkah, Riyadh | Long term (≥ 4 years) |

| Housing programs and community infrastructure supporting fast-growing urban populations | +1.4% | Riyadh, Jeddah, Makkah, Eastern Province cities | Medium term (2-4 years) |

| Transport and logistics expansion positioning KSA as a regional trade hub | +1.2% | Riyadh, Jeddah, Dammam Metropolitan Area, NEOM corridor | Medium term (2-4 years) |

| Energy transition capex driving civil and utility works | +0.9% | Northern Border, Tabuk, Eastern Province (Jafurah), Red Sea coast | Long term (≥ 4 years) |

| Water security investments enabling industrial and urban growth | +0.7% | Jubail, Yanbu, Tabuk, Jeddah, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Vision 2030 Giga- and Mega-Projects Anchoring Multi-Year Pipelines Across Asset Classes

Sovereign commitment to NEOM, Diriyah, Qiddiya, and the Red Sea guarantees steady bid flow. NEOM alone has released USD 20 billion in work since 2024, ranging from its USD 8.4 billion hydrogen plant to Oxagon’s quay walls, with completion milestones stretching to 2030[1]https://www.neom.com/en-us. Diriyah’s USD 16.9 billion tranche, including the USD 1.5 billion Arena Block, illustrates the scale that insulates contractors from private finance cycles. Prefabrication ratios of up to 80% at Red Sea Global further showcase the push for industrialised delivery. Together, these pipelines underpin baseline demand even when mortgage or retail segments soften.

Housing Programs and Community Infrastructure Supporting Fast-Growing Urban Populations

Sakani’s Q1 2024 delivery of more than 32,000 homes shows momentum. ROSHN’s master-planned communities, such as Sedra and Alarous, employ 30% prefab elements to cut handovers by three months and reduce skilled-labour exposure. Each large-scale residential scheme triggers parallel schools, clinics, and worship facilities, widening the scope for general contractors and FM providers.

Transport and Logistics Expansion Positioning KSA as a Regional Trade Hub

The USD 22.5 billion Riyadh Metro started carrying 1.2 million daily riders after its November 2024 launch, spurring station-adjacent housing and retail. The USD 7 billion Land Bridge rail will slash Jeddah–Riyadh freight times to under four hours by 2030. King Salman International Airport’s six-runway scheme broke ground in 2024, while Dammam and King Abdullah ports add nearly three million TEU of container capacity by 2027. These nodes embed long-term civil, MEP, and fit-out scope in the Saudi Arabia construction market.

Energy Transition Capex Driving Civil and Utility Works

Saudi commitments to 50% renewable electricity and global hydrogen leadership drive high-voltage interconnections, turbine foundations, and speciality balance-of-plant works. Siemens Energy’s USD 1.6 billion Rumah 2 and Nairyah 2 contracts and ACWA Power’s multi-GW solar projects illustrate the volume of EPC workload running through 2028.[2]https://www.siemens-energy.com/global/en/home.html

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery capacity constraints and skilled labor shortages amid simultaneous mega-program execution | -0.8% | National, acute in NEOM, Qiddiya, Diriyah zones | Short term (≤ 2 years) |

| Cost inflation and higher financing costs pressuring feasibility and contractor margins | -0.6% | National, most severe for fixed-price contracts | Short term (≤ 2 years) |

| Regulatory, land, and environmental permitting complexity extending timelines, especially in coastal and heritage zones | -0.4% | Jeddah, Red Sea coast, Diriyah, Tabuk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Delivery Capacity Constraints and Skilled Labor Shortages Amid Simultaneous Mega-Program Execution

The workforce crossed 13.4 million in 2024, yet concurrent execution of NEOM, Qiddiya, and Red Sea resorts strains welders, electricians, and project managers. Wage spikes of 8–12% are squeezing pre-2024 fixed-price contracts, prompting schedule resets and renegotiations. Saudization rules raise hiring friction, and remote sites incur premium logistics costs for 50,000-plus workers.

Cost Inflation and Higher Financing Costs Pressuring Feasibility and Contractor Margins

Steel jumped 15–20% and diesel 18% between early 2024 and late 2025, eroding gross margins to 4–6% on legacy jobs. Borrowing costs climbed in lockstep with U.S. rates, increasing working-capital facility expenses that mid-tier contractors rely on[3]https://www.sama.gov.sa/ar-sa/Pages/default.aspx. PPP frameworks help, but bank appetite still favors large consortia with balance-sheet depth.

Segment Analysis

By Sector: Infrastructure Dominates, Residential Accelerates

Infrastructure held 60.26% of 2025 value, confirming its anchor position in the Saudi Arabia construction market. Mega rail, airport, and port packages keep the order books of Grade 1 contractors full through 2031. Residential, however, logs the fastest trajectory at a 6.55% CAGR, riding Sakani incentives and ROSHN’s 400,000-home pledge. Apartments and condos are gaining ground in Riyadh and Jeddah thanks to metro connectivity, whereas villas still dominate secondary cities. Office and retail remain subdued, while logistics and light-industrial facilities linked to Dammam and NEOM record stable absorption. The Saudi Contractors Authority’s rigid license thresholds are nudging sub-Scale firms toward downstream housing and fit-out tasks, widening the performance gap within the sector.

Although public capital underwrites marquee infrastructure, private developers are injecting funds into gated communities and logistics sheds. Prefabrication helps residential contractors shave three months off delivery, while Red Sea Global demonstrates that 80% modular content is viable even for five-star resorts. Upgraded 2024 building codes raise the performance floor, lifting costs 3–5% but unlocking green-building premiums.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: New Construction Commands the Market

New construction controlled 85.10% of 2025 spending and is forecast to expand at a 4.12% CAGR, underscoring the Kingdom’s greenfield DNA. Retrofits constitute a niche, mostly heritage sites in Diriyah and core Jeddah, where mud-brick restoration can cost 50–80% more than comparable new-builds. The nascent retrofit space could scale after 2028 as older towers chase new energy-efficiency mandates.

For now, developers favour fresh land in Riyadh’s airport corridor, and NEOM’s virgin coastline, where title is clear, and approvals are faster. Nonetheless, the Saudi Green Building Code’s retrofit clauses may create an incremental pipeline once bank financing models mature.

By Construction Method: Conventional Still Prevails

Conventional techniques retained 91.07% of 2025 volumes, yet modern methods of construction are on track for a 4.09% CAGR to 2031, the fastest among all methods. ROSHN’s 30% prefab ratio in Sedra trimmed on-site labour by 20% and compressed schedules by four months. Qiddiya’s Six Flags rides adopted 40% off-site fabrication, while Red Sea resorts reached 80% modular content, albeit with six-week logistics buffers. Domestic suppliers such as Saudi Readymix are scaling capacity by 40% to meet precast demand.

Cast-in-place concrete remains the norm for deep foundations, tunnels, and thermal-mass requirements in high-rise towers. Still, BIM mandates and cost inflation encourage clients to specify volumetric bathroom pods and MEP modules where repetition is high.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Investment Source: Private Sector Participation Accelerates Despite Public Dominance

Public investment accounted for 63.29% of total spend in 2025, underpinned by the Public Investment Fund’s USD 30 billion annual deployment and Saudi Aramco’s USD 50 billion capex program, which together dominate infrastructure, energy, and giga-project construction. Private capital is projected to grow at a 4.18% CAGR through 2031, expanding from a 28.5% share in 2025 toward a targeted 35% by decade-end as revised PPP frameworks and PIF co-investment structures reduce risk.

The 2024 PPP law cut approval timelines to 12–15 months and standardized risk-allocation, improving bankability for international consortia. Private activity is concentrated in residential, hospitality, and logistics, while PPP uptake is rising in social infrastructure, supported by government offtake agreements but progressing more slowly than transport and energy.

Geography Analysis

Riyadh maintains the largest single-city concentration of projects, yet escalating land values are nudging some developers toward satellite corridors near King Salman International Airport, where logistics zoning and aerotropolis incentives apply. The Saudi Arabia construction market size allocated to the capital is fortified by long-cycle infrastructure, thereby supporting contractors’ backlog visibility.

Jeddah’s focus is twofold: heritage waterfront renewal and airport-linked logistics parks. The Central Development project engages both international design consultants and local marine specialists, integrating climate-resilient promenades that meet new 2024 coastal regulations. The city’s buildout benefits from constant Umrah pilgrim inflows, keeping hospitality pipelines active even as retail footprints rationalise around mixed-use clusters.

Northern and coastal territories, notably NEOM and the Red Sea, are absorbing a growing portion of civil works as giga-project phases stack up. Tabuk’s desalination plants and solar farms require specialised EPC packages, giving rise to local joint ventures that pair technical prowess with on-the-ground mobilisation agility. Dammam and Khobar round out the geography map through their container gateway expansions that funnel logistics demand into adjacent warehouse projects.

Competitive Landscape

Thousands of licensed firms operate nationwide, yet mega-project value is concentrated among a small set of top-tier players—creating a bifurcated landscape where scale determines access to billion-dollar packages. International EPC majors form joint ventures with Grade 1 local partners to leverage supply chains and satisfy Saudization metrics, especially on transport and energy assets. Domestic mid-tier players protect niches in residential and small commercial works by offering faster permit cycles and lower mobilisation overhead.

Technology adoption separates winners from laggards. Mandatory BIM for SR 500 million-plus schemes compels smaller firms to either invest in digital capability or subcontract coordination. Drones, IoT concrete sensors, and AI scheduling shave costs and mitigate rework; Bechtel’s pilot at Riyadh Metro reduced idle machinery time by 15%. Modular fabrication has become a strategic differentiator—Saudi Readymix’s capacity jump caters to NEOM’s steel packages, while niche startups deliver procurement marketplaces that trim project soft costs.

Cost escalation and labour constraints catalyse consolidation. Higher bonding thresholds sideline under-capitalised players, prompting mergers among Grade 3 and Grade 4 contractors. At the top end, joint-venture structures allow foreign EPCs to manage dollar financing risks while locals handle Arabic documentation and stakeholder outreach. Emerging opportunities lie in district cooling and smart-building retrofits, fields still thin on competition but rich in Vision 2030 support.

Saudi Arabia Construction Industry Leaders

Saudi Binladin Group

Nesma & Partners

Al Rashid Trading & Contracting

Almabani General Contractors

Al Ayuni Investment & Contracting

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Port of NEOM installed its first automated cranes, aiming for a 2026 launch powered entirely by renewables.

- May 2025: Bechtel selected to lead the King Salman International Airport expansion.

- April 2025: Parsons began a 25-month PMO contract for King Salman Park’s 21.6 km² redevelopment.

- March 2025: Public Investment Fund and Hyundai Motor agreed to build a USD 500 million automated vehicle plant.

Saudi Arabia Construction Market Report Scope

The construction market includes upcoming, ongoing, and growing construction projects in different sectors. These include but are not limited to geotechnical (underground structures) and superstructures in residential, commercial, and industrial structures, as well as infrastructure construction (like roads, railways, and airports) and power generation and transmission-related infrastructure.

A complete background analysis of the Saudi Arabia Construction market, which includes an assessment of the sector and the contribution of the industry to the economy, market overview, market size estimation for critical segments, key regions, and emerging trends in the market segments, market dynamics, and essential production and consumption statistics are covered in the report.

The Saudi Arabian construction market is segmented into residential, commercial, industrial, infrastructure (transportation), and energy and utility construction. The report provides market size and forecasts for the Saudi Arabian construction industry regarding value (USD) for all the above-mentioned segments.

By Sector

| Residential | Apartments / Condominiums | |

| Villas / Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial & Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure | Roadways |

| Railways | ||

| Airways | ||

| Others | ||

| Energy & Utilities | ||

| Others | ||

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site | |

| Modern Methods of Construction | Prefabricated |

| Modular | |

| Others |

By Investment Source

| Public |

| Private |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Sector | Residential | Apartments / Condominiums | |

| Villas / Landed Houses | |||

| Commercial | Office | ||

| Retail | |||

| Industrial & Logistics | |||

| Others | |||

| Infrastructure | Transportation Infrastructure | Roadways | |

| Railways | |||

| Airways | |||

| Others | |||

| Energy & Utilities | |||

| Others | |||

| By Construction Type | New Construction | ||

| Renovation | |||

| By Construction Method | Conventional On-Site | ||

| Modern Methods of Construction | Prefabricated | ||

| Modular | |||

| Others | |||

| By Investment Source | Public | ||

| Private | |||

| By City | Riyadh | ||

| Jeddah | |||

| DMA (Dammam Metropolitan Area) | |||

| Rest of Saudi Arabia | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Saudi Arabia construction market?

The Saudi Arabia construction market size is USD 112.35 billion in 2026 and is projected to rise to USD 148.71 billion by 2031.

Which segment is growing fastest within Saudi construction?

Residential construction is advancing at the quickest pace, posting a 6.55% CAGR through 2031 as Sakani and ROSHN catalyse homebuilding.

How large is public spending compared with private investment?

Public outlays represent 71.5% of 2025 value, while private capital is forecast to climb at a 7.10% CAGR and approach a 35% share by decade-end.

Which city captures the largest share of construction activity?

Riyadh leads with a 36.1% share in 2025, driven by its international airport program and metro extensions.

How fast are modern construction methods growing?

Modern methods of construction are set to expand at a 7.55% CAGR to 2031, driven by schedule and labor savings on large housing and resort projects.

What are the main cost pressures for contractors?

Steel prices rose 15–20%, diesel 18%, and higher interest rates lifted financing costs, cutting gross margins to 4–6% on legacy fixed-price contracts.