Construction Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

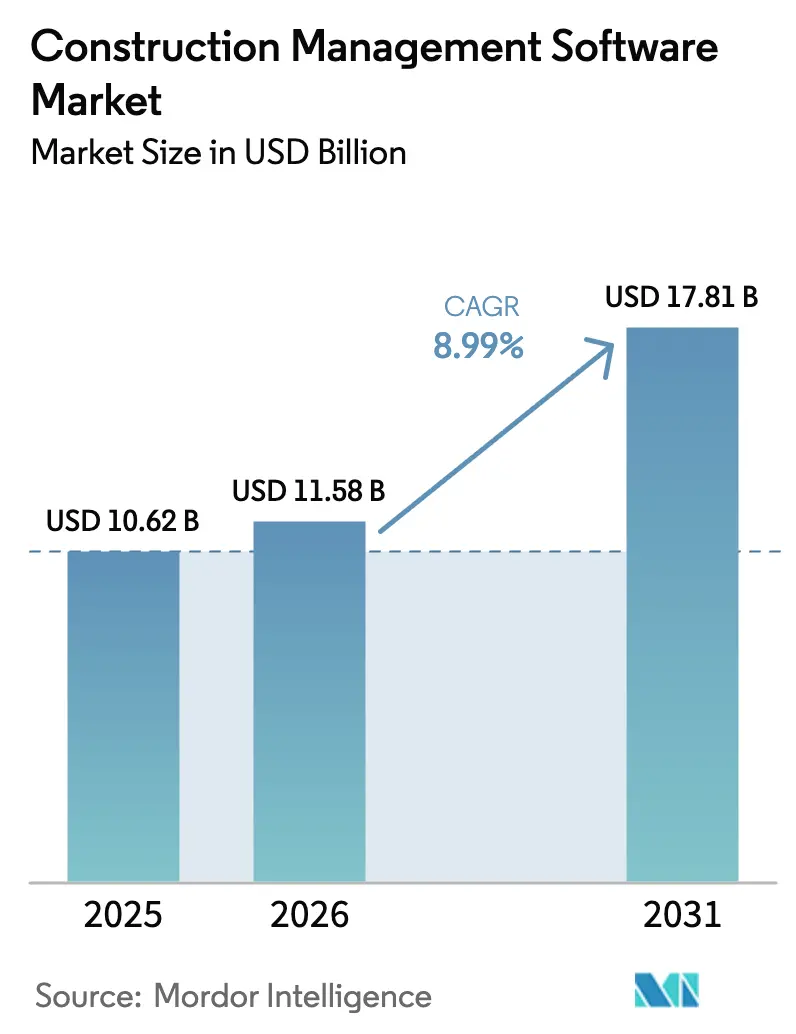

| Market Size (2026) | USD 11.58 Billion |

| Market Size (2031) | USD 17.81 Billion |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

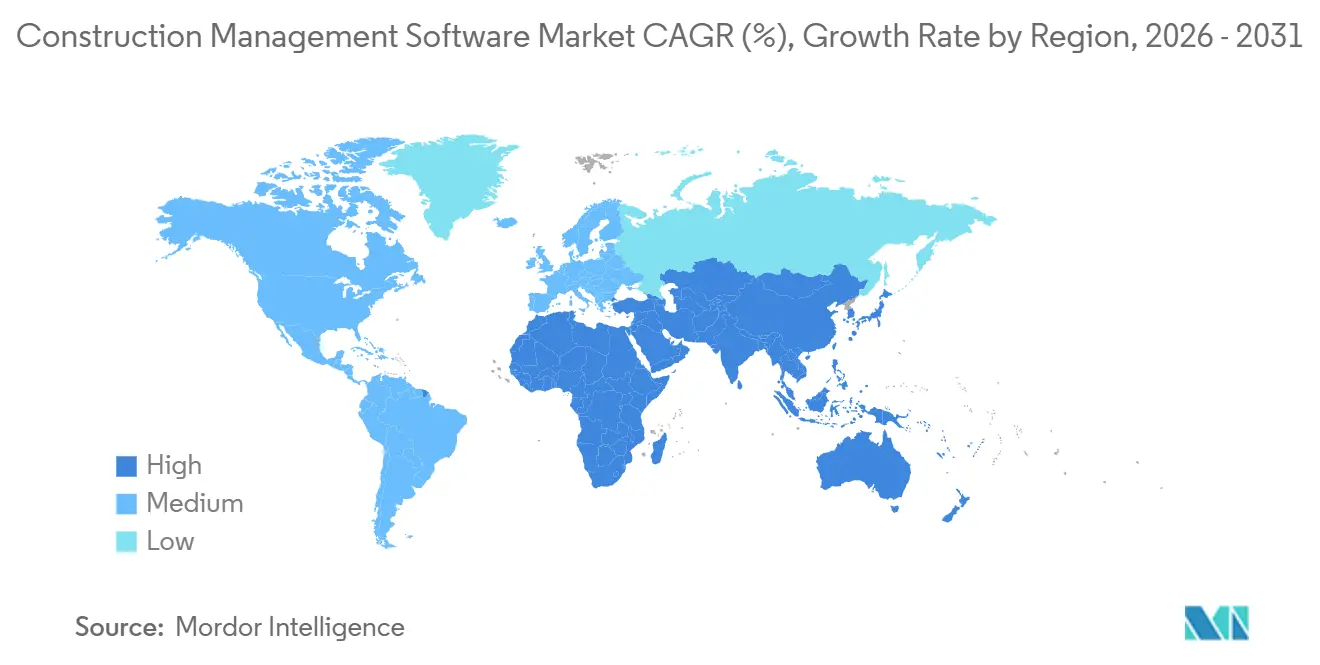

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Management Software Market Analysis by Mordor Intelligence

The construction management software market size is projected to expand from USD 10.62 billion in 2025 and USD 11.58 billion in 2026 to USD 17.81 billion by 2031, registering an 8.99% CAGR between 2026 and 2031. Early cloud‐first adopters have proven that subscription pricing lowers upfront costs, so spending increasingly concentrates on SaaS platforms that ship feature updates continuously. Owners now demand real-time cost and schedule visibility that connects design intent with field execution, a shift that accelerates buying decisions when large projects face labor shortages and material volatility. Vendors are embedding artificial-intelligence modules that predict risk and automate compliance documentation, easing the talent gap that has widened as veteran project managers retire. Governments on every continent have reinforced demand through tax incentives, embodied-carbon reporting mandates, and digital-twin requirements that make software a prerequisite for public tenders. As a result, consolidation is gathering pace as well-capitalized leaders acquire niche specialists to plug workflow gaps and to scale internationally.

Key Report Takeaways

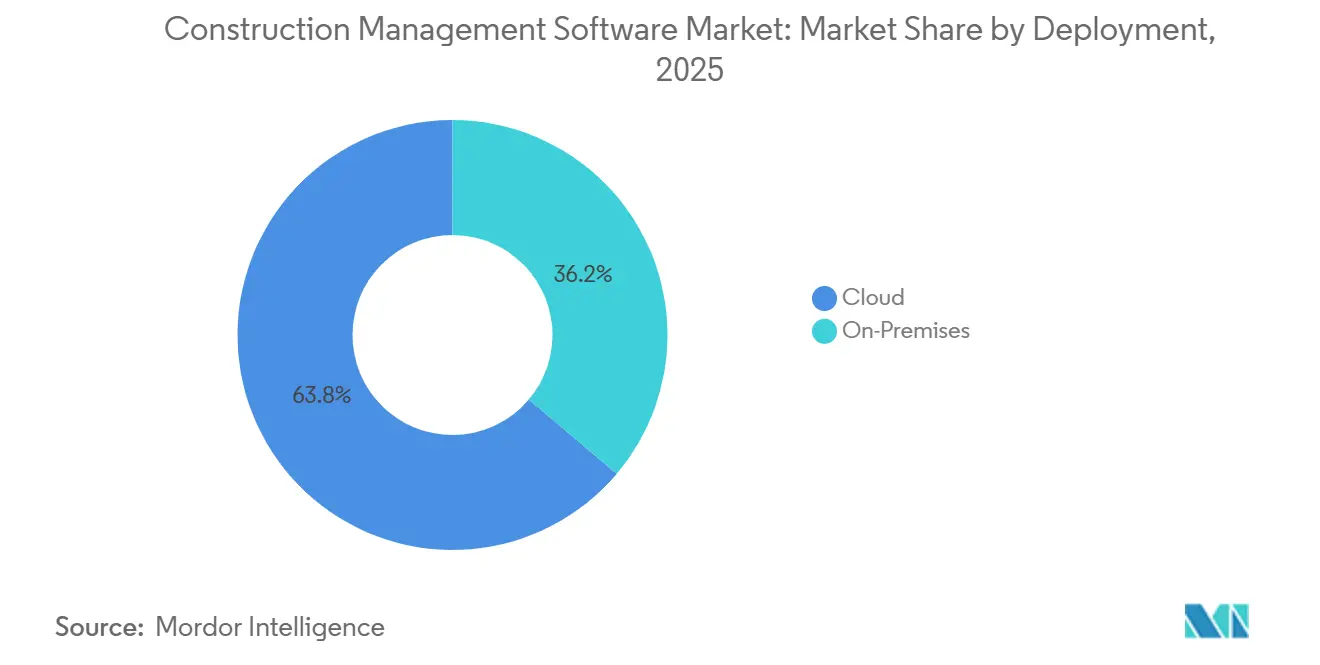

- By deployment, cloud commanded 63.83% of 2025 revenue, while on-premises environments are shrinking even in security-sensitive segments.

- By application, project management and scheduling captured 40.91% of the construction management software market share in 2025; design and BIM integration tools are forecast to grow at a 9.18% CAGR through 2031.

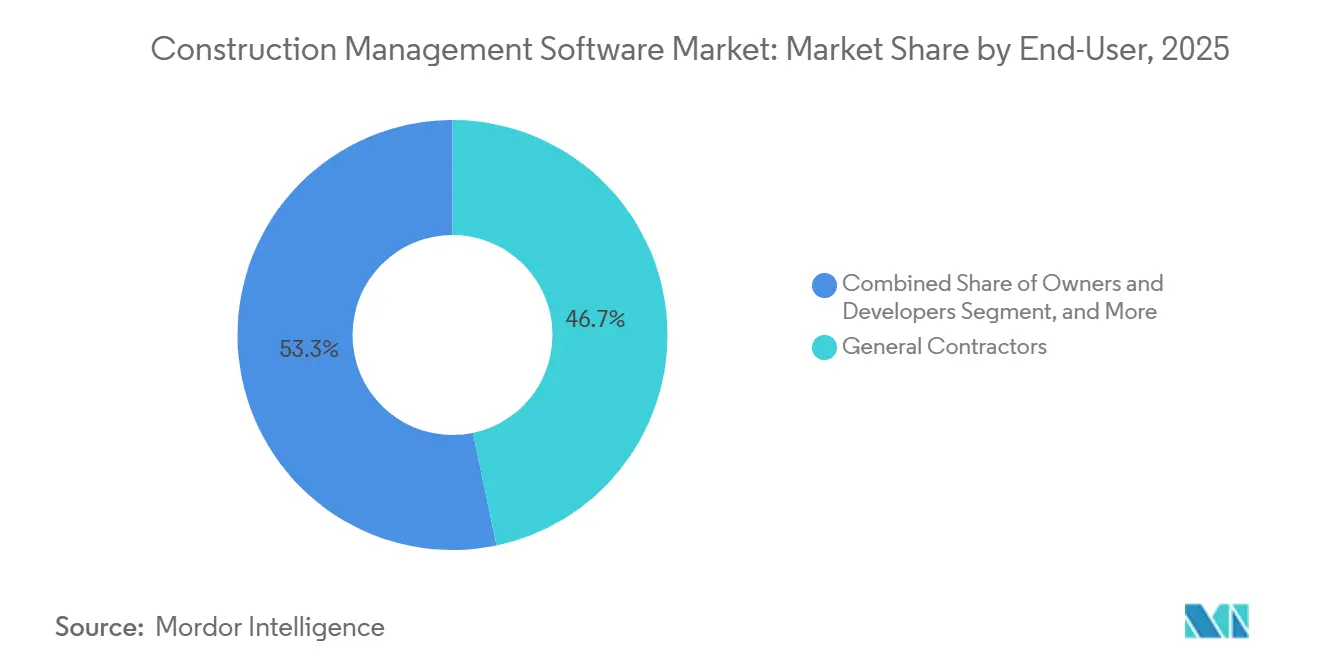

- By end-user, general contractors held 46.72% of 2025 spending, whereas architects and engineers are advancing at a 9.11% CAGR to 2031.

- By project size, mid-size projects between USD 50 million and USD 500 million accounted for 44.38% of 2025 deployments, but projects above USD 500 million are projected to grow at a 9.22% CAGR to 2031.

- By geography, North America led with 35.64% of 2025 value, yet Asia Pacific is on track for the fastest 9.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Construction Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digital-transformation budgets expanding post-COVID | +2.1% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Digital-twin adoption for risk-free pre-construction simulation | +1.8% | Asia Pacific megaprojects and European infrastructure | Medium term (2-4 years) |

| AI-enabled progress analytics cutting rework costs | +1.6% | North America and Europe lead, Asia Pacific following | Medium term (2-4 years) |

| Government construction-tech tax incentives | +1.3% | United States, European Union, Singapore | Medium term (2-4 years) |

| Skilled-labor scarcity forcing productivity software uptake | +1.2% | Global, most acute in developed economies | Long term (≥ 4 years) |

| Sustainability and embodied-carbon mandates driving BIM modules | +1.0% | Europe, North America, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digital-Transformation Budgets Expanding Post-COVID

Remote collaboration became routine during the pandemic, and the associated opex model convinced finance chiefs that subscription software delivers a faster return than capital-intensive servers. Construction and engineering firms subsequently lifted cloud budgets 18% year over year, reallocating savings from decommissioned hardware to mobile field tools. Interoperability has now overtaken price as the top evaluation criterion because manual data re-entry stalls monthly billing cycles. Vendor roadmaps therefore emphasize open APIs and regional data centers, exemplified by Microsoft’s Sovereign Cloud for Europe that satisfies GDPR residency rules.

Digital-Twin Adoption for Risk-Free Pre-Construction Simulation

Infrastructure owners rely on simulation to uncover clashes before crews mobilize, cutting average change-order costs by 15%. Public clients now mandate digital twins on major schemes, for example the United Kingdom’s requirement on projects above GBP 50 million and Japan’s highway program that expanded i-Construction criteria. Cloud platforms that stream sensor feeds into federated BIM models allow managers to validate cures, lifts, and pours against specifications in real time.

AI-Enabled Progress Analytics Cutting Rework Costs

Computer-vision modules compare 360-degree imagery with design intent, reducing rework incidents by 38% on pilot sites and saving roughly USD 1.2 million on a USD 100 million contract. Predictive scheduling algorithms now surface schedule slippage two weeks earlier than critical-path techniques, enabling lean crews to pivot before penalties accrue. Hardware partners such as NVIDIA accelerate adoption by packaging GPU acceleration that renders clash detection instantly on mobile devices.

Government Construction-Tech Tax Incentives

Policymakers view digitization as the fastest route to decarbonize and derisk built assets, so they fund software directly. The United States extended Section 179 deductions to cover construction solutions, allowing immediate expensing up to USD 1.16 million.[1]Internal Revenue Service, “Section 179 Deduction Limits 2024,” irs.gov The European Union’s Digital Europe Programme co-funds 40% of software purchases that enhance energy efficiency, while Singapore reimburses up to SGD 30,000 (USD 22,000) per firm to accelerate SaaS migration. These grants compress payback periods below two years even for mid-market contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contractor margin pressures delaying IT capital expenditure | -1.4% | North America and Europe where wage inflation exceeds 6% | Short term (≤ 2 years) |

| Data-silo and interoperability issues among legacy point solutions | -1.1% | Global, especially firms using software older than 10 years | Medium term (2-4 years) |

| Cyber-security and data-sovereignty concerns on multi-tenant clouds | -0.8% | Europe, China, Middle East | Medium term (2-4 years) |

| Low digital readiness of small and micro-contractors | -0.7% | Emerging Asia Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Contractor Margin Pressures Delaying IT Capital Expenditure

Operating margins slipped to 2.8% in 2024 as material and labor costs outpaced escalation clauses.[2]Construction Financial Management Association, “Quarterly Financial Survey 2024,” cfma.org Many firms postponed software upgrades even while acknowledging efficiency gains because cash is redirected toward bonding capacity and working-capital reserves. Small contractors, which make up 78% of establishments but only 23% of revenue, struggle most to amortize subscriptions when interest rates on construction loans surpassed 8%.

Data-Silo and Interoperability Issues Among Legacy Point Solutions

The average contractor runs 11 discrete applications yet just one-third exchange data without manual workarounds. Custom middleware can cost USD 50,000 per connection, so many firms delay adopting new tools despite clear ROI. Current industry data standards, such as IFC, do not extend to financial workflows, perpetuating gaps that inflate total cost of ownership. Suite vendors respond by pre-integrating ERP, project controls, and supply chain modules, but pricing often exceeds budgets for firms under USD 50 million turnover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominates as Data-Residency Mandates Reshape Architectures

Cloud services held 63.83% of 2025 construction management software market share and are growing faster than on-premises alternatives, reflecting universal demand for pay-as-you-go economics and remote access. Multinational contractors welcome regional data centers such as Microsoft’s new facilities in Germany, France, and Poland that satisfy sovereignty rules, thereby removing one of the last barriers to wholesale SaaS adoption.

Quarterly feature releases reinforce the preference for cloud because on-premises upgrades consume scarce IT labor. Vendors reported that retention exceeds 95% when customers receive AI risk-prediction, offline mobile modes, and automated compliance trackers without new license fees. Hybrid architectures persist only where latency-sensitive digital-twin rendering or classified financial data must remain on site, but even those workflows increasingly push archives to the cloud to reduce storage overhead.

By Application: Project Controls Lead While BIM Integration Surges on Carbon Compliance

Project management and scheduling tools commanded 40.91% of the construction management software market in 2025 because every project team needs budget tracking and critical-path oversight. Yet design and BIM integration modules post the fastest 9.18% CAGR through 2031, propelled by embodied-carbon calculators now embedded directly in modeling environments.

Safety, quality, and field-operations applications gain momentum as regulators tighten reporting rules; OSHA now requires digital injury logs on sites with 20 or more workers, and the EU’s revised Construction Products Regulation demands traceability of materials.[3]OSHA, “Electronic Injury Reporting Final Rule,” osha.gov Cost-accounting suites grow more slowly because many mid-size contractors still rely on spreadsheets, but cloud integrations with ERP systems are chipping away at that inertia.

By End-User: General Contractors Anchor Spending While Designers Accelerate

General contractors retained 46.72% of 2025 value for the construction management software market size, reflecting their central role in coordinating trades and finance. Owners and developers follow, prioritizing asset handover modules that link construction data with property-management systems.

Architects and engineers are expanding at 9.11% CAGR because statutes such as the UK Building Safety Act require digital records of fire-safety details, making BIM non-negotiable. Specialty trades adopt mobile task apps that remove paperwork, driving uptake even among firms with fewer than 20 employees.

By Project Size: Mid-Size Projects Dominate Installations While Megaprojects Justify Premium Suites

Projects valued between USD 50 million and USD 500 million accounted for 44.38% of 2025 deployments, the sweet spot where software setup effort aligns with project duration. Payback averages 14 months thanks to faster monthly billing and reduced change orders.

Large jobs above USD 500 million, however, show a 9.22% CAGR because even marginal schedule gains translate into multi-million-dollar savings. These mega-schemes demand enterprise-grade role-based access, multi-currency cost control, and predictive analytics that smaller contracts cannot justify, so vendors price premium modules accordingly.

Geography Analysis

North America retained 35.64% of 2025 spending for the construction management software market, supported by high broadband penetration and mature cloud culture. Federal tax incentives and rapid uptake of AI modules sustain growth even as the region approaches saturation. Contractors there report 89% cloud-only adoption, a rate far ahead of global peers.

Europe contributed 28.7% of 2025 revenue. GDPR compliance initially slowed multi-tenant migration, yet Microsoft’s Sovereign Cloud and EU grants now bridge that gap, so growth holds at 8.7% CAGR. Whole-life-carbon assessments mandated under the Energy Performance of Buildings Directive further stimulate BIM module sales.

Asia Pacific is projected to be the fastest-growing region at 9.43% CAGR to 2031, underpinned by China’s USD 1.4 trillion infrastructure drive, India’s National Infrastructure Pipeline, and Japan’s digital-twin mandates.[4]Asian Development Bank, “Asia Infrastructure Outlook 2025,” adb.org Government subsidies across Singapore, Australia, and South Korea narrow affordability gaps, while local data centers resolve sovereignty concerns.

Competitive Landscape

The construction management software market exhibits moderate concentration. The top five suppliers Oracle, Autodesk, Procore, Trimble, and Bentley Systems collectively captured roughly 45% of 2025 revenue, leaving ample space for specialists that focus on residential builders or owner-operator handover workflows. Oracle leverages its ERP backbone to upsell integrated suites that knit project controls with finance modules, a strategy that produced double-digit cloud growth in fiscal 2024.

Procore’s international revenue rose 35% year over year in Q3 2024 as it localized applications for European languages and Asia Pacific regulatory formats. Autodesk expanded upstream by acquiring Forma, moving earlier into feasibility and zoning analysis so that construction-phase competitors face an incumbent long before ground breaks.

Innovation hinges on AI and interoperability. Trimble partnered with NVIDIA to embed generative algorithms that automate equipment logistics, while Nemetschek bought GoCanvas to fuse mobile data capture with desktop BIM. Venture-backed newcomers such as STACK focus narrowly on estimating, raising USD 45 million to integrate supplier catalogs directly into take-offs. Patent filings show incumbents racing to protect AI progress-monitoring techniques, highlighting intensifying competition.

Construction Management Software Industry Leaders

Oracle Corporation (Construction and Engineering GBU)

Bentley Systems Incorporated

Procore Technologies Inc.

Microsoft Corporation

Trimble Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Autodesk released an AI-powered progress-tracking module that automates as-built versus BIM comparisons for projects above USD 500 million.

- January 2026: Procore’s preliminary Q4 2025 results showed annual revenue surpassing USD 1 billion, driven by 38% international growth.

- December 2025: Oracle added a digital-twin IoT module to its Construction and Engineering Cloud targeting infrastructure owners.

- November 2025: Trimble and NVIDIA launched a partnership to integrate generative AI for equipment-logistics planning.

Global Construction Management Software Market Report Scope

The Construction Management Software Market Report is Segmented by Deployment (On-Premises, Cloud), Application (Project Management and Scheduling, Cost Accounting and Estimation, Field Service and Site Operations, Safety, Quality and Reporting, Design/BIM Integration), End-User (General Contractors, Owners and Developers, Architects and Engineers, Sub-Contractors and Specialty Trades, Government and Infrastructure Agencies), Project Size (Small less than USD 50 Million, Mid-Size USD 50 Million to USD 500 Million, Large greater than USD 500 Million), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Project Management and Scheduling |

| Cost Accounting and Estimation |

| Field Service and Site Operations |

| Safety, Quality and Reporting |

| Design/BIM Integration |

| General Contractors |

| Owners and Developers |

| Architects and Engineers |

| Sub-Contractors and Specialty Trades |

| Government and Infrastructure Agencies |

| Small (Less Than USD 50 M) |

| Mid-Size (USD 50 M - 500 M) |

| Large (Greater Than USD 500 M) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Deployment | On-Premises | |

| Cloud | ||

| By Application | Project Management and Scheduling | |

| Cost Accounting and Estimation | ||

| Field Service and Site Operations | ||

| Safety, Quality and Reporting | ||

| Design/BIM Integration | ||

| By End-User | General Contractors | |

| Owners and Developers | ||

| Architects and Engineers | ||

| Sub-Contractors and Specialty Trades | ||

| Government and Infrastructure Agencies | ||

| By Project Size | Small (Less Than USD 50 M) | |

| Mid-Size (USD 50 M - 500 M) | ||

| Large (Greater Than USD 500 M) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the construction management software market be by 2031?

Forecasts indicate the market will reach USD 17.81 billion by 2031, advancing at an 8.99% CAGR from 2026 to 2031.

Which deployment model is growing fastest?

Cloud solutions expand at 9.34% CAGR thanks to pay-as-you-go pricing and quarterly feature updates that keep systems current.

Which application segment shows the strongest momentum?

Design and BIM integration modules lead growth with a 9.18% CAGR because carbon-tracking and digital-twin mandates make them essential.

What region will record the highest growth rate?

Asia Pacific is projected to expand at 9.43% CAGR, fueled by large infrastructure programs in China, India, and Japan.

Why are small contractors slower to adopt software?

Tight margins, limited IT support, and high integration costs deter smaller firms, although mobile-first tools are lowering entry barriers.

How competitive is the vendor landscape?

The top five vendors control around 45% of revenue, so rivalry is moderate and niche specialists still find room to differentiate.

Page last updated on: