Construction Estimating Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

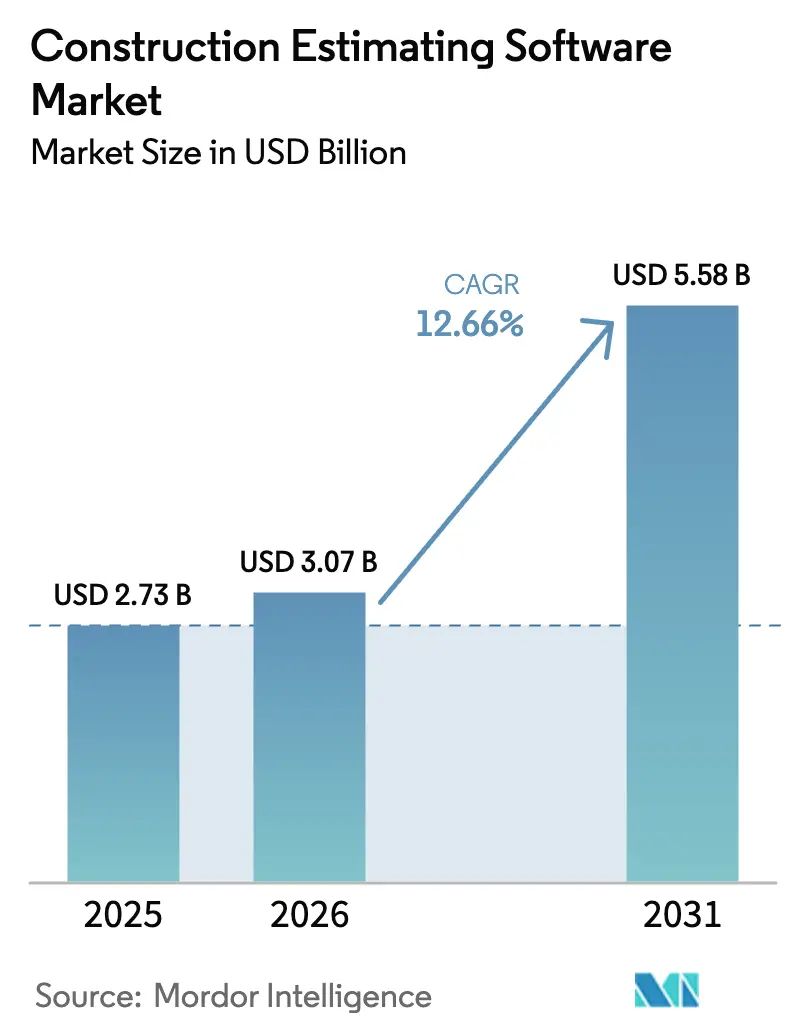

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 5.58 Billion |

| Growth Rate (2026 - 2031) | 12.66% CAGR |

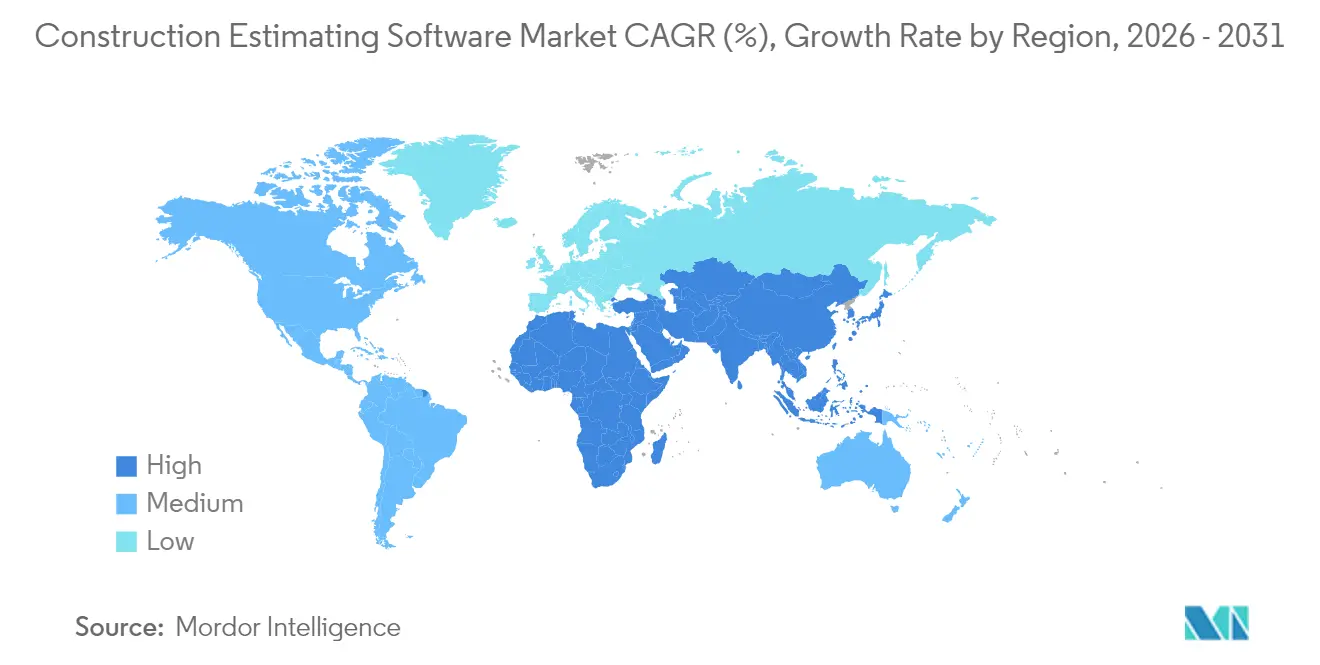

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

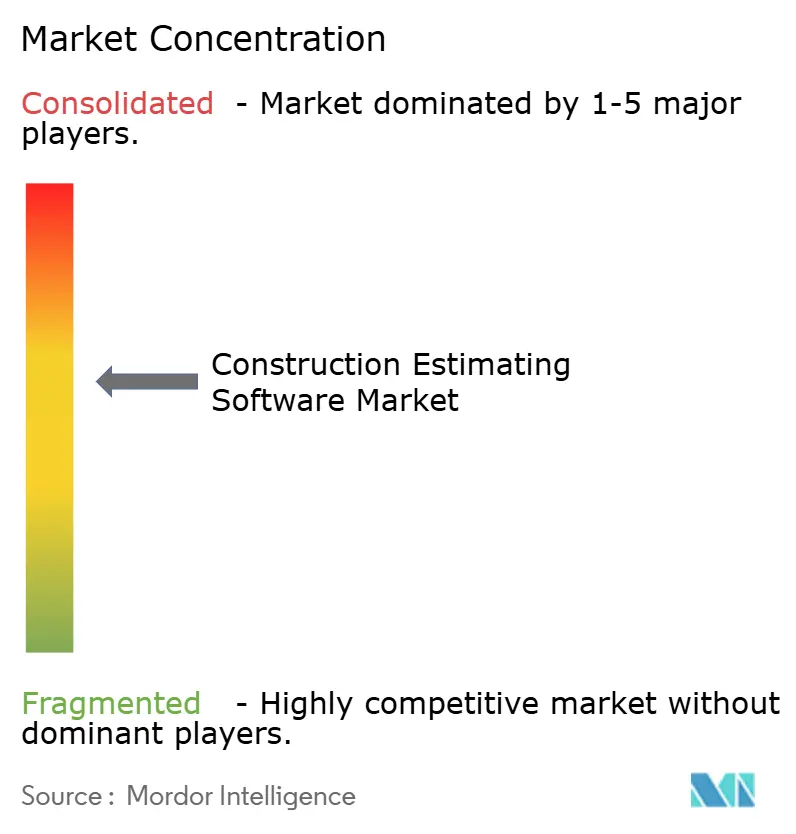

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Estimating Software Market Analysis by Mordor Intelligence

The construction estimating software market size in 2026 is estimated at USD 3.07 billion, growing from 2025 value of USD 2.73 billion with 2031 projections showing USD 5.58 billion, growing at 12.66% CAGR over 2026-2031. Rapid digitization across global construction, rising material-price volatility, and a shrinking skilled labor pool are amplifying the need for precise, data-rich bid preparation. Cloud platforms underpin this expansion by enabling distributed project teams to work from a single source of truth, while AI-supported cost libraries raise forecast accuracy and cut bid cycles. Government mandates for digital records, wider BIM uptake, and new ESG reporting needs further sustain demand across user segments. Vendors respond by embedding real-time pricing feeds, carbon modules, and seamless BIM connectors, which is reshaping competitive dynamics within the construction estimating software market.

Key Report Takeaways

- By deployment, cloud solutions held 68.14% of construction estimating software market share in 2025 and are forecast to grow at 11.18% CAGR through 2031.

- By solution type, integrated project suites accounted for 27.05% of the construction estimating software market size in 2025, and they post the fastest 13.32% CAGR to 2031.

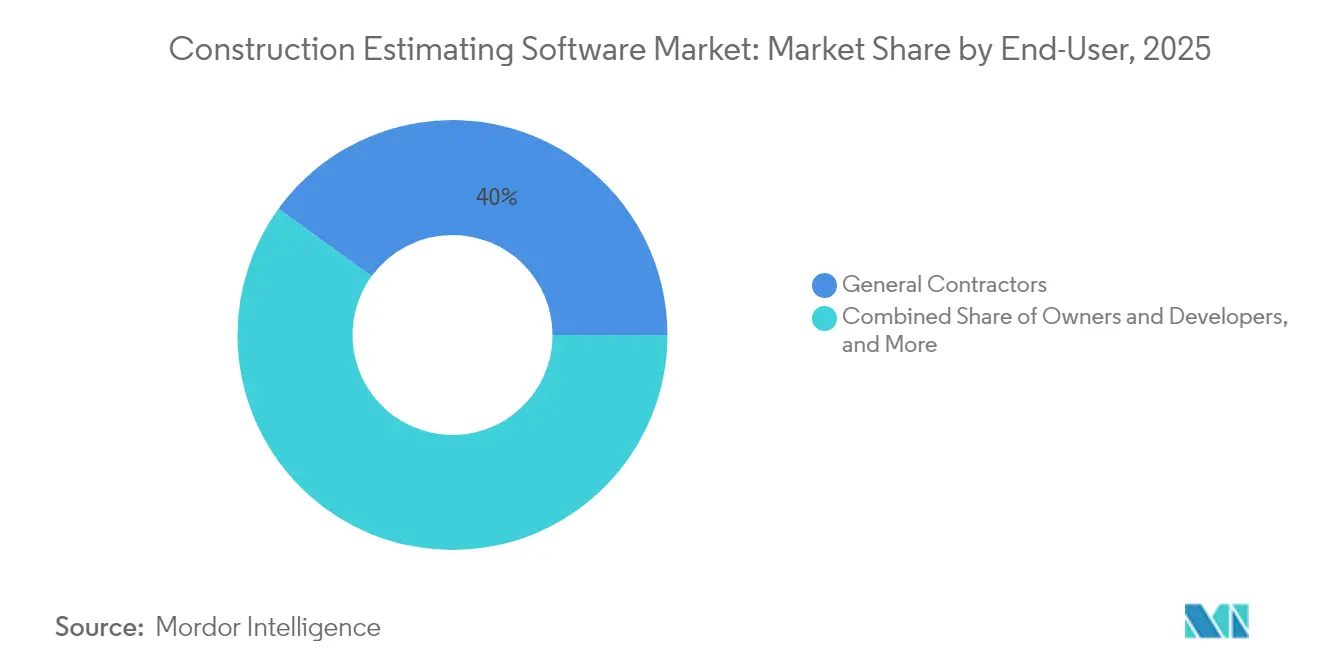

- By end-user, general contractors led with 40.02% revenue share in 2025, while specialty/sub-contractors record the highest 10.32% CAGR to 2031.

- By enterprise size, large enterprises captured 58.05% of 2025 revenue, yet small and medium enterprises expand at 22.74% CAGR to 2031.

- By geography, North America retained the largest 30.98% share in 2025; Asia-Pacific is the fastest-growing region at a 12.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Construction Estimating Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward cloud-based estimating platforms | +2.8% | Global, strongest in North America and EU | Medium term (2-4 years) |

| High demand for bid-price accuracy | +3.2% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Tight integration with BIM ecosystems | +2.1% | North America and EU lead, Asia-Pacific rising | Long term (≥ 4 years) |

| Government mandates for digital records | +1.9% | North America and EU, selective Asia-Pacific | Medium term (2-4 years) |

| AI-curated regional cost databases | +1.4% | North America and EU then global | Long term (≥ 4 years) |

| ESG / embodied-carbon estimating modules | +0.8% | EU leads, North America follows | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward cloud-based estimating platforms

Contractors value continuous updates, elastic computing for complex take-offs, and genuine real-time collaboration. Trimble’s free ProjectSight release in November 2024, complete with AI automation, illustrates growing competition for cloud share [1]Trimble, “Trimble Expands Access to Advanced Construction Project. Persistent barriers involve cybersecurity certification and data-sovereignty rules that still favor on-premise or hybrid models for select public-sector projects.

High demand for bid-price accuracy amid volatile materials cost

Material prices swung sharply in 2024, prompting contractors to prioritize bid accuracy tools capable of live database updates and scenario planning. AI-enabled platforms now deliver 85-90% price-forecast accuracy, trim bid preparation time by up to 40%, and help firms protect slim margins. Early adopters report the ability to model supplier performance trends, regional inflation, and logistics constraints within minutes, strengthening competitiveness in fast-moving tender cycles.

Tight integration with BIM and project-management ecosystems

BIM-driven quantity extraction replaces manual 2D methods and links design intent directly to cost. PennDOT’s Digital Delivery Directive 2025 mandates 3D models for state projects, accelerating demand for interoperable estimating tools [2]Pennsylvania Department of Transportation, “Digital Delivery Directive 2025,” penndot.pa.gov. Autodesk Construction Cloud recorded USD 809 million in Q1 FY26 revenue, reflecting a 20% annual jump supported by BIM-to-estimate workflows [3]Autodesk Inc., “Autodesk Announces Fiscal 2026 First Quarter Results,” autodesk.com. Persistent IFC data-loss issues, however, force contractors to validate model integrity, and vendors race to refine cross-platform connectors that secure a single data thread from design through procurement.

Government mandates for digital construction records

Regulators increasingly tie funding to digital documentation. The US General Services Administration requires BIM deliverables across every federal milestone. Separately, USD 16.6 million in federal grants awarded to eight US states for digital technologies underscores public-sector momentum. Compliance drives captive demand for certified estimating suites that integrate cybersecurity standards such as CMMC, forcing vendors to offer audit-ready data trails while retaining ease of use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps with legacy tools | -1.8% | Global, most acute in mature markets | Medium term (2-4 years) |

| Workforce skill deficit in digital estimation | -2.1% | Global, severe in North America and EU | Short term (≤ 2 years) |

| Cyber-security and data-sovereignty concerns | -1.2% | Global with regional regulatory nuances | Medium term (2-4 years) |

| AI accuracy limits for mega-projects | -0.9% | Global, felt on large infrastructure programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability gaps with legacy tools

NIST estimates the US capital-facilities sector loses billions annually due to poor interoperability between systems. Cross-platform IFC transfers still drop phase or material metadata, forcing costly manual rework. Nearly 85% of contractors cite seamless data flow to accounting and ERP packages as a purchase criterion, yet many still export and re-enter numbers, duplicating effort and raising error risk. The resulting inefficiencies temper the construction estimating software market’s growth momentum, particularly among firms running bespoke legacy stacks.

Workforce skill deficit in digital estimation

The talent crunch remains acute: 94% of US firms reported vacancies in 2024, and 41% of the workforce may retire by 2031. Technology skills lag most; 75% of contractors list digital proficiency as a top barrier to software rollouts, despite USD 1.6 billion invested in upskilling during 2023. SMEs feel the pinch hardest because they lack formal training budgets, limiting the uptake of advanced modules and slowing the overall expansion of the construction estimating software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates

Cloud platforms controlled a dominant 68.14% slice of the construction estimating software market in 2025 and are expanding at an 11.18% CAGR to 2031. This momentum illustrates the broad preference for subscription pricing and instant scalability that frees estimators from hardware limits. The model also supports automatic updates, which close security gaps and add new features without IT downtime. On-premise systems linger in segments that must satisfy stringent government data rules, yet hybrid approaches now blend local data vaults with cloud analytics to strike a compliance-performance balance. Vendors that master hybrid orchestration widen their addressable customer base while protecting growth in the construction estimating software market.

The surge in cloud also enables continuous data capture from IoT sensors on job sites, feeding real-time cost dashboards. As these feeds enrich AI models, bid accuracy improves and change-order risk drops. The construction estimating software industry is responding by baking predictive alerts into dashboards so teams act before overruns materialize. Over the forecast horizon, cloud penetration is set to push legacy client-server deployments into niche status, especially as 5G coverage and edge processing lower latency for large model uploads.

By Solution Type: Integrated Suites Drive Consolidation

Integrated project suites held 27.05% share in 2025 and deliver the fastest 13.32% CAGR to 2031. The trend reflects contractor impatience with fragmented point solutions that require duplicate data entry. Full-stack suites combine take-off, cost databases, bid management, and project controls behind one sign-on and one data model, which lowers manual-entry error rates and accelerates approvals. Cost libraries inside these suites refresh nightly using regional feeds, keeping bids aligned with market conditions and strengthening the construction estimating software market’s stickiness.

Take-off and estimating modules retain the largest discrete revenue slice, yet their value now climbs when bundled inside suites that also handle downstream payment workflows. Autodesk’s acquisition of Payapps illustrates this convergence and signals how cash-flow controls are becoming as vital as initial bid accuracy. As a result, new entrants differentiate on open APIs, allowing clients to plug best-of-breed accounting or field-execution tools into an otherwise unified costing spine.

By End-User: Specialty Contractors Embrace Digital Transformation

General contractors led 2025 revenue with 40.02%, but specialty/sub-contractors are the sprint segment, rising at a 10.32% CAGR. The spread of SaaS pricing removes the capital barrier that once prevented smaller trade firms from harnessing enterprise-grade analytics. Roofing, electrical, and mechanical subcontractors now rely on AI-driven assemblies to calibrate bids quickly for a high volume of small projects, taking advantage of the construction estimating software market’s democratization.

Owners and developers are also adopting estimating software to verify third-party bids and analyze feasibility. Quantity surveyors leverage multi-project benchmarking dashboards, while architects reference embedded carbon modules during early design. These use-case expansions prove that the construction estimating software industry now caters to the full value chain rather than a single estimator persona.

By Enterprise Size: SMEs Lead Adoption Surge

Large enterprises owned 58.05% of 2025 revenue, yet SMEs post a striking 22.74% CAGR to 2031. This tilt highlights how greenfield IT environments let smaller firms sidestep legacy lock-in and deploy cloud suites within weeks. Vendors promote starter plans, free trials, and low-code template libraries that slash configuration times. Consequently, the construction estimating software market size attributable to SMEs is set to climb sharply, narrowing the digital divide with tier-one contractors.

Larger enterprises still wield custom integrations that weave estimating outputs into corporate ERPs and risk dashboards, but they struggle with organizational change-management hurdles. Progressive CIOs are forming cross-functional squads that pair seasoned estimators with data scientists to unlock value from extensive historical cost archives. Over time, the resulting insight loops should raise productivity while protecting the incumbents’ share of the construction estimating software market.

Geography Analysis

North America retained 30.98% share in 2025, supported by mature vendor ecosystems, early BIM mandates, and consistent government funding for digital-first infrastructure. Federal grants worth USD 16.6 million to eight US states highlight ongoing momentum, though skill shortages restrict the pace of platform rollouts. Canada and Mexico contribute steady growth as public procurement bodies formalize digital documentation protocols, reinforcing regional demand for compliant suites in the construction estimating software market.

Asia-Pacific is the fastest-growing region at a 12.46% CAGR through 2031, propelled by large-scale infrastructure pipelines in China, India, and Indonesia. Government programs emphasize smart cities and transparent procurement, making cloud estimating solutions a practical choice for tracking costs across multi-phase developments. Japanese and South Korean contractors push the envelope on 5D BIM, demanding tight integrations that cover schedule and cost in a unified model. As smartphone penetration rises, mobile-first interfaces gain favor among site engineers, broadening the user base throughout the construction estimating software market.

Europe posts stable growth aided by mandatory BIM use on public projects and strict carbon-reporting rules. Germany’s transport ministry phases in full BIM for federal roads and rail, while the UK targets 50% faster project delivery by 2025 under its Level 2 BIM framework. Vendors race to incorporate embodied-carbon calculators, meeting EU taxonomy disclosure needs. Southern Europe and the Nordics follow suit, mirroring best practices that shorten tender validation cycles and keep cross-border projects on budget. The Middle East and Africa show emergent demand, with the UAE and Saudi Arabia using mega-projects to attract global suppliers who require unified estimating and procurement platforms compliant with local data laws.

Competitive Landscape

The construction estimating software market is moderately consolidated, yet MandA activity continues to compress the field. Leaders like Procore extend end-to-end capabilities, leveraging 95% gross revenue retention to cross-sell adjacent modules. Revenue expansion hinges on AI that forecasts material price shifts and flags scope gaps instantly, transforming cost data into actionable intelligence.

Mid-tier players differentiate through depth in niche verticals such as off-site timber or heavy civil infrastructure, often pairing with BIM specialists to form co-marketing bundles. RIB Software’s alliance with 2050 Materials delivers carbon metrics alongside cost data, addressing ESG-minded contractors. Such partnerships create data moats that are difficult for generic providers to replicate, sustaining competitive tension within the construction estimating software market.

Start-ups challenge incumbents with mobile-first workflows and browser-native 3D viewers that run smoothly on modest hardware. Some focus on emerging markets where language localization and regional cost databases remain underserved. Incumbents counter with developer marketplaces, letting third parties build niche add-ons atop established platforms. Over the outlook period, success will turn on an ability to harmonize open APIs, robust security frameworks, and predictive analytics, ensuring customer lock-in without sacrificing interoperability.

Construction Estimating Software Industry Leaders

Procore Technologies, Inc.

Autodesk, Inc.

Oracle Corporation

Trimble Inc.

RIB Software

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Reconstruct received strategic investment from Nemetschek Group to expand AI-driven visual reality digital twins for capital asset management.

- February 2025: Kahua launched an asset-centric project-management platform that reorganizes handover data around long-term asset performance.

- December 2024: Valsoft Corporation broadened its construction software footprint by acquiring Buildsoft, signalling continued roll-up activity.

- December 2024: hsbcad secured majority investment from Maguar Capital to accelerate off-site timber software aligned with Autodesk Revit integrations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the construction estimating software market as licensed applications that convert drawings or BIM models into quantity take-offs, cost databases, and bid proposals for building and infrastructure projects, whether the solution sits in the cloud or on-premise.

Scope exclusion: stand-alone spreadsheet templates, generic project management suites with no built-in estimating engine, and one-off in-house scripts remain outside this review.

Segmentation Overview

- By Deployment

- Cloud

- On-Premise

- By Solution Type

- Take-off and Estimating

- Bid Management

- Cost Databases and Analytics

- Integrated Project Suites

- By End-User

- General Contractors

- Specialty/Sub-contractors

- Owners and Developers

- Architects and Engineers

- Cost Consultants / Quantity Surveyors

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed quantity surveyors, regional contractors, software product managers, and cloud resellers across North America, Europe, the Gulf, and Asia-Pacific. Short web surveys gauged the share of bids prepared digitally versus manually, refining adoption ratios and upgrade cycles.

Desk Research

We began with public indicators such as U.S. Census Construction Put-in-Place tables, Eurostat building permits, and Statistics Canada investment data. We then paired these with trade body insights from the Associated General Contractors of America and the Chartered Institute of Building. Patent analytics delivered via Questel flagged emerging AI-pricing modules, while supplier price sheets and 10-Ks captured average seat costs. Dow Jones Factiva news archives and tender feeds from Tenders Info helped us trace adoption events across 35 countries. The sources listed illustrate our approach; numerous additional feeds supported data checks.

Market-Sizing & Forecasting

A top-down model converts national construction output into a spend pool, applying adoption and spend-per-seat factors that vary by enterprise size, deployment type, and region. Selective supplier roll-ups of licensed seats provide a bottom-up check that adjusts totals. Key variables include residential versus non-residential starts, cloud penetration, average subscription price, tender volume, and BIM usage share. A multivariate regression supported by expert consensus projects 2025-2030 outcomes, and scenario analysis stress-tests material-price shocks. Gaps in supplier data are bridged with median price bands captured during interviews.

Data Validation & Update Cycle

Outputs pass variance screening, senior analyst review, and peer sign-off. Models refresh each year, with interim updates when regulations, major M&A, or price swings above five percent trigger a re-contact round. A final sweep before publication ensures clients receive the latest view.

Why Mordor's Construction Estimating Software Baseline Commands Reliability

Published values often diverge because firms select different scopes, price assumptions, and refresh cadences. This is where Mordor Intelligence's disciplined variable selection and annual fieldwork keep numbers aligned with reality.

Key gaps arise when other publishers omit on-premise licenses, apply uniform price points, or stretch historic CAGRs without fresh interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.73 B | Mordor Intelligence | - |

| USD 1.61 B | Regional Consultancy A | Counts subscription licenses only, ignores on-premise sales |

| USD 1.56 B | Trade Journal B | Relies on archival filings, no current interviews, single inflation factor |

| USD 1.29 B (2024) | Industry Association C | Tracks contractor seats only, excludes architect and owner users |

These contrasts show that our blended top-down model, corroborated with supplier roll-ups and yearly interviews, delivers a balanced, transparent baseline that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the current size of the construction estimating software market?

The market is valued at USD 3.07 billion in 2026.

How fast is the construction estimating software market expected to grow?

It is projected to expand at a 12.66% CAGR, reaching USD 5.58 billion by 2031.

Which deployment model leads the market?

Cloud deployment accounts for 68.14% of 2025 revenue and maintains the fastest 11.18% CAGR.

Why are specialty contractors adopting estimating software rapidly?

SaaS pricing, simpler onboarding, and competitive pressure push specialty trades to digitize, giving this segment a 10.32% CAGR through 2031.

What are the main barriers to wider software adoption?

Interoperability gaps with legacy tools and a shortage of digitally skilled estimators remain the primary constraints.

What years does this Construction Estimating Software Market cover, and what was the market size in 2025?

In 2025, the Construction Estimating Software Market size was estimated at USD 3.07 billion. The report covers the Construction Estimating Software Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Construction Estimating Software Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: