Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 141.42 Billion |

| Market Size (2031) | USD 179.21 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

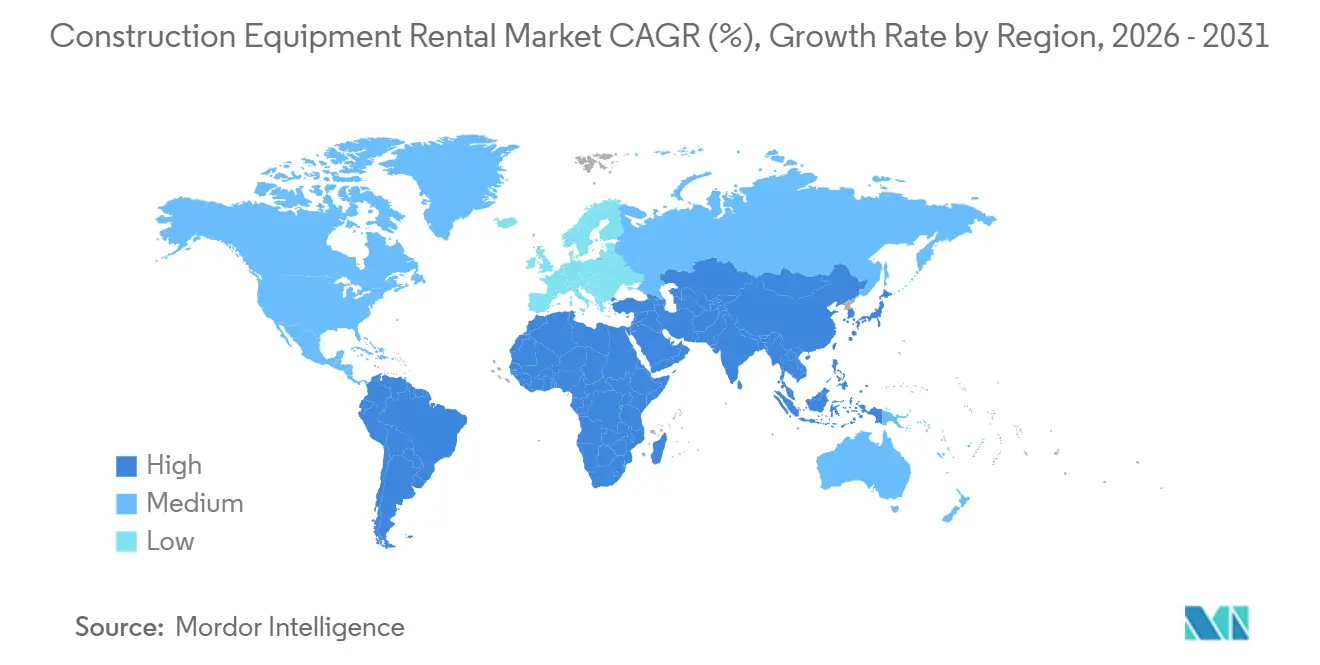

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction Equipment Rental Market Analysis by Mordor Intelligence

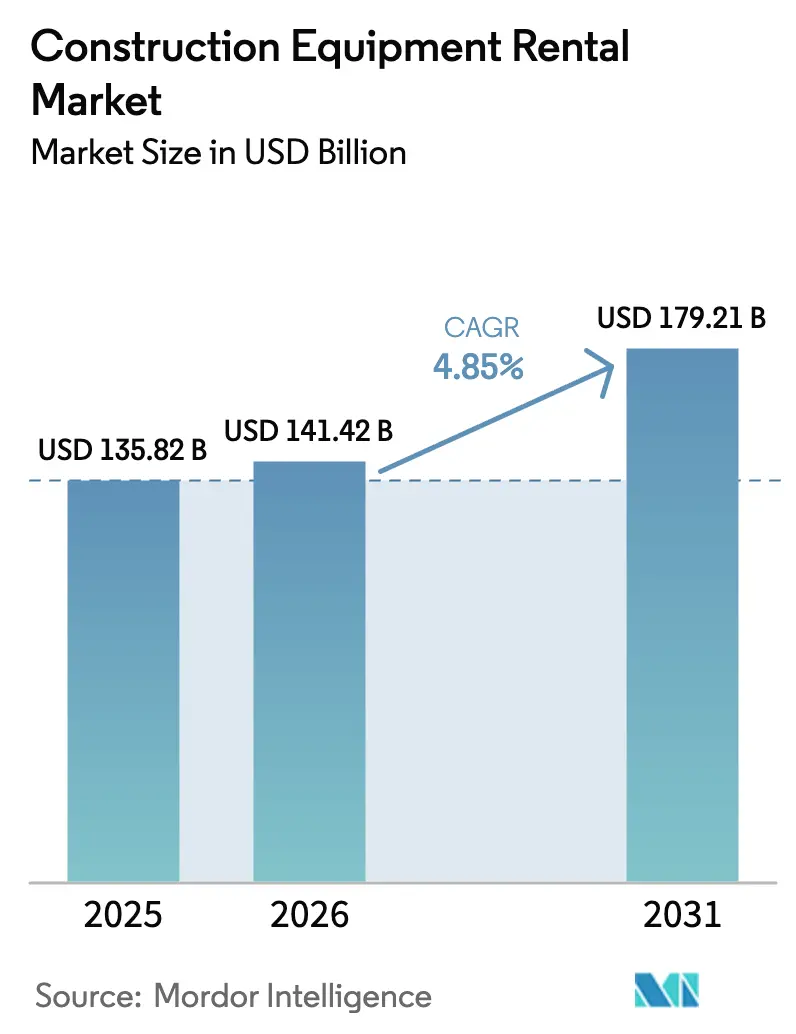

The construction equipment rental market size is projected to be USD 135.82 billion in 2025, USD 141.42 billion in 2026, and reach USD 179.21 billion by 2031, growing at a CAGR of 4.85% from 2026 to 2031. Contractors are shifting from ownership to rentals to conserve cash for labor and materials, while sovereign infrastructure pipelines in the Asia-Pacific and the Middle East provide multi-year demand visibility, encouraging rental operators to lock in medium-term contracts. The United States Infrastructure Investment and Jobs Act directed a significant amount to more than 60,000 projects through 2024, favoring rental models because they avoid residual-value risk. China’s issuance of local-government infrastructure bonds during 2024 similarly channels capital into transport corridors that suit flexible rental fleets. Add to this the ongoing ESG regulations and the rapid spread of digital marketplaces, and the growth trajectory for the construction equipment rental market appears firmly supported by both policy and technological levers.

Key Report Takeaways

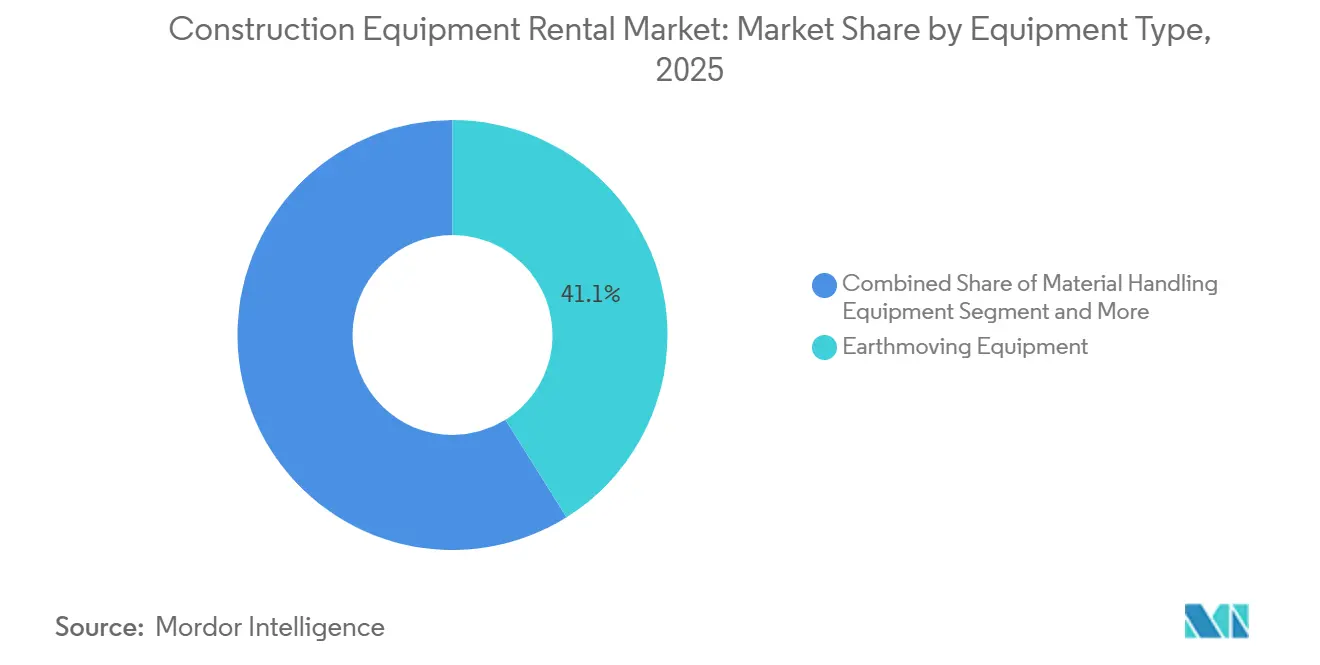

- By equipment type, earthmoving commanded 41.05% of the construction equipment rental market share in 2025 and is set to outpace the overall market with a 7.61% CAGR through 2031.

- By drive type, IC-engine machines dominated the mix with 86.13% in 2025, yet hydrogen fuel-cell models are scaling at a brisk 15.88% CAGR through 2031.

- By application, infrastructure projects accounted for 36.24% of revenue in 2025, while mining and quarrying were the fastest-growing sectors at a 5.94% CAGR through 2031.

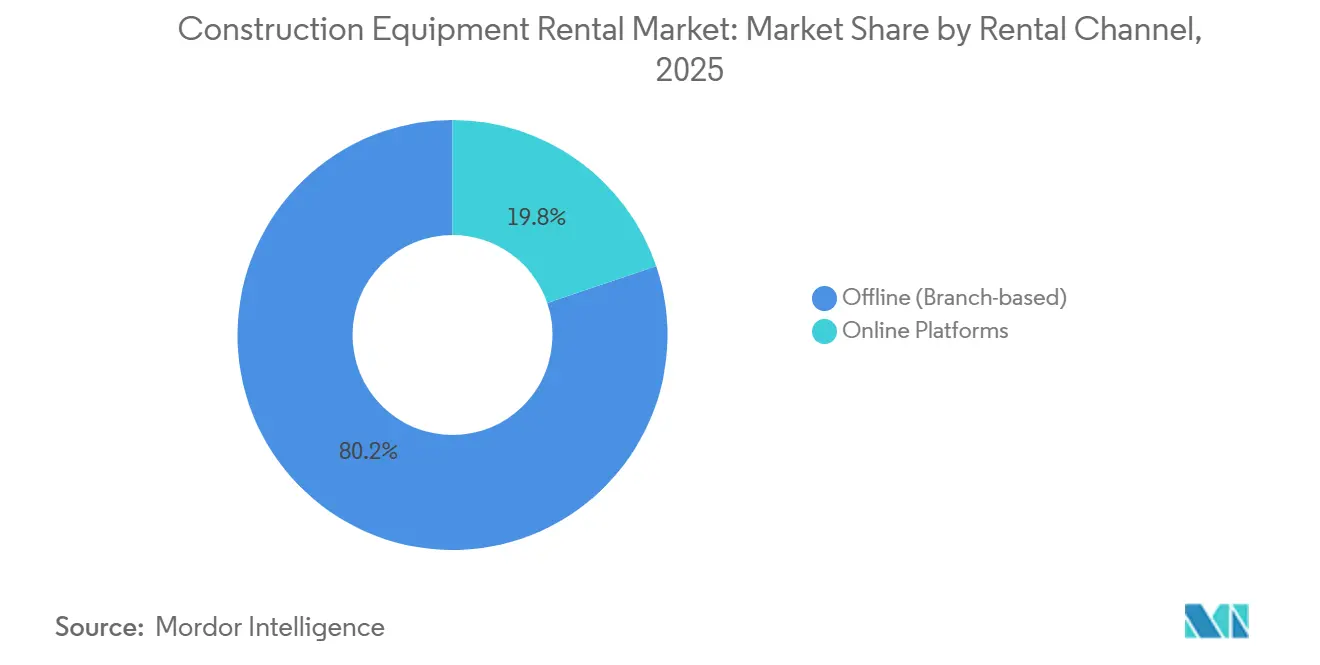

- By rental channel, offline branches captured an 80.22% share in 2025; online platforms showed the quickest rise, advancing at a 9.84% CAGR to 2031.

- By service type, medium-term rentals (1–12 months) accounted for 48.26% of the construction equipment rental market in 2025; however, short-term rentals (<1 month) are expected to grow at a 7.13% CAGR through 2031.

- By geography, Asia-Pacific held a 40.11% share in 2025, while the Middle East and Africa will advance at a 6.72% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Construction Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Stimulus Megaproject Pipeline | +1.2% | Global, high in Asia-Pacific, the Middle East, and Africa | Long term (≥ 4 years) |

| Contractors Shifting Capex to Opex | +0.9% | North America and Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| ESG Targets Driving Electric Rentals | +0.7% | Europe, California, urban Asia-Pacific | Medium term (2-4 years) |

| Digital Rental-Platform Growth | +0.6% | Asia-Pacific core, spill-over to the Middle East, Africa, and South America | Short term (≤ 2 years) |

| Outcome Based Usage Contracting Models | +0.5% | North America, early adoption in Europe | Short term (≤ 2 years) |

| Data Driven Fleet Optimization | +0.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Stimulus Megaproject Pipeline

Large public spending programs turn speculative demand into firm, multi-year rental contracts. The United States has already committed significant investment to over 60,000 infrastructure projects under the Infrastructure Investment and Jobs Act. In 2024, China significantly increased its deployment of provincial bonds, focusing primarily on transport corridors and urban renewal projects. India budgeted INR 11.11 lakh crore (USD 133 billion) for infrastructure in fiscal 2024-25 [1]“National Infrastructure Pipeline,” Ministry of Finance, India, indiabudget.gov.in . Saudi Arabia’s Vision 2030 includes multiple giga-projects (e.g., NEOM, Qiddiya) that are sustaining construction demand and equipment utilization. Preliminary damage assessments for Türkiye indicate needs above USD 100 billion, supporting sustained reconstruction activity. These pipelines feed directly into medium-term rentals, already generating notable revenue.

Shift from CAPEX-to-OPEX Among Contractors

In a bid to preserve liquidity, construction firms are increasingly turning to rentals instead of relying on owned fleets. United Rentals maintained a significant annual capex program in 2024, with a focus on minority-financing specialty and electric assets for rental purposes. Sunbelt Rentals committed substantial resources in fiscal 2025 for fleet expansion, simultaneously inaugurating numerous new outlets across the United States. Herc Rentals, in 2024, enhanced its fleet value significantly, honing in on specialty niches. As tighter credit markets emerge in North America and Europe, there's a noticeable shift towards operating leases over capital purchases. This financial strategy is now being rolled out to contractors in the Asia-Pacific region.

Stringent ESG Targets Accelerating Electric Rentals

Rental agencies, driven by environmental mandates, are electrifying their inventories even before contractors demand it. California has identified several models of zero-emission equipment. Boels has set a long-term target to transition the majority of its fleet to electric. Sunbelt reports that a growing portion of its clients are now willing to pay a premium for zero-emission equipment. Volvo’s L120 and L90 electric loaders deliver diesel-parity performance without tailpipe emissions[2]“L120 Electric Loader Factsheet,” Volvo Construction Equipment, volvoce.com . Europe and California anchor this trend, which is spreading into Asian megacities adopting low-emission zones.

Digital Rental-Platform Explosion in Emerging Markets

Online marketplaces are reducing discovery times and improving equipment utilization. EquipmentShare, which operates numerous sites, uses its T3 platform to provide real-time utilization and maintenance alerts. United Rentals enhances asset efficiency through its Total Control portal, which integrates booking, invoicing, and predictive maintenance. Digital channels are growing significantly faster than the overall market, driven by their convenience and efficiency. In the Asia-Pacific region, where branch networks are limited, there is a strong preference for app-based ordering. Consequently, rental firms are making substantial investments in user-friendly interfaces and telematics to meet the needs of a younger, digitally-savvy customer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Operator Scarcity | −0.8% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Multi-Brand Maintenance Complexity | −0.6% | Global, acute in fragmented European fleets | Medium term (2-4 years) |

| Direct Rental Market Cannibalization | −0.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Residual Value Volatility for Lithium | −0.3% | Europe and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Operator Scarcity Elevates Downtime Risk

Rental equipment often sits idle because trained operators are unavailable when demand surges. In 2026, the U.S. Bureau of Labor Statistics projects continued annual openings for construction equipment operators over the next decade, driven mainly by replacement needs. This gap becomes more pronounced during peak construction months, as retirements outpace new certifications. Similar shortages are also evident in Germany and Japan, where aging workforces drive up wage premiums and lengthen recruitment cycles, thereby inflating project costs and extending schedules. Rental firms attempt to mitigate the risk by bundling operator training into contracts and partnering with vocational schools; however, class backlogs still mean contractors wait weeks for certified personnel. Idle machinery erodes utilization metrics, forcing rental companies to maintain larger fleets to meet service-level guarantees, thereby tying up capital that could be used to fund electrification or digital upgrades. Unless training pipelines expand materially, operator scarcity will continue to depress adequate fleet availability and place downward pressure on rental margins through at least the medium term.

High Multi-Brand Maintenance Complexity

Rental fleets include Caterpillar, Komatsu, Volvo, and JCB, each with its own proprietary diagnostics. Trackunit and similar telematics can cut unplanned downtime, yet full integration remains elusive. Cross-trained technicians are scarce, especially in Europe, where fleets draw from many OEMs and operations cross borders. Rental firms incur higher service costs to maintain the brand diversity that clients demand. Until unified diagnostics gain traction, maintenance complexity continues to weigh on profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Earthmoving Dominates Infrastructure Buildout

Earthmoving equipment secured 41.05% of the construction equipment rental market share in 2025, and its 7.61% CAGR through 2031 exceeds the overall market pace. Excavators, loaders, and bulldozers remain indispensable for road, rail, and mining projects. Backhoe loaders serve utilities and residential work where versatility matters. Excavators, especially tracked units, lead demand for heavy soil removal, while wheeled variants gain ground in urban sites where mobility is prized.

Material-handling gear forms the next-largest slice, driven by cranes and telehandlers used in high-rise and logistics developments. Concrete and road machinery rise with highway spending, and power equipment—such as generators and compressors—meets intermittent site needs. Telematics-enabled earthmovers differentiate rental fleets on uptime rather than price, reinforcing their central role in the construction equipment rental market.

By Drive Type: Hydrogen Fuel Cells Emerge From Niche

Internal Combustion (IC) engine machines accounted for 86.13% of the mix in 2025, as diesel refueling networks remain ubiquitous. Hybrid models blend diesel and electric to navigate low-emission zones. Battery electric equipment gains momentum, helped by a significant number of zero-emission models listed in California.

Hydrogen fuel-cell units, such as Hyundai’s HW155H excavator unveiled at Bauma 2025, are growing at a 15.88% CAGR by 2031 and attract projects that need zero emissions without battery-range limits. JCB’s hydrogen-combustion engines offer a drop-in diesel alternative. IC dominance will persist this decade; however, regulatory pressure and falling total cost of ownership will tilt the longer-term curve toward electric and hydrogen technologies.

By Application: Mining and Quarrying Outpace Traditional Construction

Infrastructure works accounted for 36.24% of 2025 revenue, driven by sovereign stimulus in the Asia-Pacific and Middle East regions. Residential builders rent compact machines to avoid idle capital, while commercial developers rely on cranes and concrete gear for multi-story timelines.

Mining and quarrying exhibit the fastest growth rate of 5.94% to 2031, as commodity price volatility encourages operators to shift fixed equipment costs into variable rental outlays. Epiroc noted that mining represented a notable share of its 2024 orders, underscoring the opportunity. Oil and gas contractors similarly prefer rentals for specialized, high-capex machines needed only episodically.

By Rental Channel: Online Platforms Gain Share

Offline branches retained an 80.22% hold in 2025 because many contractors still value face-to-face service and instant availability. Same-day delivery and on-site maintenance remain decisive for complex gear.

Online platforms, however, are projected to grow at a 9.84% CAGR by 2031, significantly outpacing the overall construction equipment rental market. EquipmentShare’s T3 and United Rentals’ Total Control platforms illustrate how telematics and real-time availability enhance customer ROI. Adoption is fastest in the Asia-Pacific and Middle East regions, where mobile-first users are bypassing legacy branch models.

By Service Type: Short-Term Rentals Accelerate

Medium-term contracts (1–12 months) accounted for 48.26% of 2025 revenue, as they align with typical infrastructure project lengths. Long-term rentals underpin predictable mining and industrial operations, enabling volume discounts.

Short-term rentals of less than one month exhibit the steepest CAGR of 7.13% from 2026 to 2031. Project volatility, tighter credit, and the rise of gig-economy builders make daily and weekly rentals attractive. Operators counter higher logistics costs by leveraging telematics to maximize asset utilization and by charging premium pricing to protect their margins.

Geography Analysis

Asia-Pacific captured a 40.11% share in 2025 and is tracking a notable CAGR to 2031. China’s local infrastructure bonds, India’s significant pipeline, and Japan’s construction budget anchor demand. South Korea’s considerable program and Australia’s mining-plus-renewables mix likewise favor rentals. The region’s mix of urbanization and mega-projects sustains the construction equipment rental market.

The Middle East and Africa log the fastest CAGR of 6.72%, led by Saudi Vision 2030’s USD 1.3 trillion slate spanning NEOM, the Red Sea, and Qiddiya. Projects in the United Arab Emirates, such as Etihad Rail Phase 2, require continuous rotations [3]“Phase 2 Milestones,” Etihad Rail, etihadrail.ae. Turkey’s USD 100 billion reconstruction and South Africa’s renewable-energy program add depth.

North America and Europe experience a steady, albeit slow, growth. The United States continues its strong infrastructure push with significant investments. While Canada prioritizes transit and power lines, Germany channels its construction efforts towards electric fleets, aligning with urban low-emission mandates. The United Kingdom construction sector also leans into specialty rentals to ensure compliance.

Regulatory Landscape

Safety and emissions compliance is a key determinant of rental fleet eligibility across major end markets, with requirements covering operator safety, machine guarding, and on-road circulation of non-road mobile machinery. In the United States, OSHA construction standards (including 29 CFR 1926.600 and related provisions) govern equipment operation safeguards and jobsite practices, while 29 CFR 1926.1001 links certain equipment manufactured on or after 15 July 2019 to ISO 3471:2008 performance requirements for roll-over protective structures (ROPS). This affects what fleets can supply into higher-risk earthmoving and site-prep applications.

In Europe, the regulatory pathway is shifting from legacy directives to updated regulations that increase the compliance surface for connected equipment. Regulation (EU) 2025/14, published in January 2025, sets an EU type-approval regime for non-road mobile machinery circulating on public roads, with most provisions applicable from 29 January 2028 and providing a clearer framework for cross-border movement of rental assets. Separately, the EU Machinery Regulation (EU) 2023/1230 becomes fully applicable on 20 January 2027, introducing requirements relevant to connected systems (including cybersecurity and AI-related considerations). For rental operators, it influences how telematics and digital controls are specified in new fleet purchases.

Value Chain Analysis

The construction equipment rental value chain starts with OEM design and manufacturing (including powertrains, hydraulics, and electronics), moves through dealer and distributor networks as well as OEM captive channels, and then into rental operators that own, service, and dispatch fleets to contractors and industrial users. Given the market definition excludes rentals bundled with full-time operators, value is concentrated in fleet financing and procurement, maintenance and parts logistics, branch and delivery operations, and increasingly in digital layers such as telematics, customer portals, and integration into construction management workflows.

The main friction points relate to equipment availability and lifecycle cost control. Multi-brand fleets increase diagnostic and technician complexity, while electronics supply constraints can extend lead times for new builds, putting pressure on fleet planning and refurbishment cycles. Rental operators use associations and industry bodies (such as the American Rental Association and Associated Equipment Distributors) to align practices on safety, training, and asset utilization benchmarks. They also rely on telematics providers to reduce unplanned downtime and improve utilization. As ESG and local emissions rules tighten in major metros, compliance responsibility shifts toward rental fleets, accelerating the mix shift toward electric or alternative-power assets and increasing emphasis on charging solutions, preventative maintenance, and residual-value management.

Competitive Landscape

North America is more consolidated than other regions, with United Rentals and Sunbelt Rentals together holding a notable share of the construction equipment rental market. In Q3 2024, United Rentals reported significant revenue growth, supported by its extensive fleet. Looking ahead, the company plans to make substantial investments in specialty and electric assets. Meanwhile, Sunbelt demonstrated strong performance in Q1 FY 2025, with a notable commitment to fleet expansion and the addition of numerous new sites across the United States.

Europe remains fragmented: Loxam, Boels, and Cramo push electric fleets and digital portals but face OEM-captive rentals encroaching on their base. Caterpillar’s Cat Rental Stores exploit manufacturer-grade service to win clients directly.

Asia-Pacific operators such as Kanamoto and Coates Hire focus on local service density and specialized equipment. EquipmentShare marries telematics with 373 depots, leveraging data analytics to cut downtime. M&A activity is likely to intensify as big players acquire regional specialists to expand their footprint, gain scale in procurement, and amortize digital-platform investments.

Construction Equipment Rental Industry Leaders

Herc Rentals Inc.

United Rentals Inc.

Ashtead Group plc (Sunbelt Rentals)

Loxam Group

Caterpillar Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity lies in embedding rental workflows into the software stack used to plan and run jobsites, which reduces friction from planning to dispatch and supports higher fleet utilization. United Rentals announced a telematics integration with Procore that syncs rental equipment data into Procore Resource Management, and it also launched an AI-powered Equipment Agent experience accessible within ChatGPT to assist customers with equipment planning. Together, these moves point to whitespace for rental operators and platforms to differentiate through interoperability (construction management software, ERP, permitting, and telematics), rather than competing only on day rates and proximity.

Another opportunity is specialty-led network expansion supported by sustained fleet investment and bolt-on deals, especially in areas where contractors outsource compliance and uptime risk to rental partners. In February 2026, Herc Holdings outlined gross rental capital expenditures of USD 800 million to USD 1.1 billion for 2026 as part of its fleet strategy, reinforcing continued modernization of rental inventories. Sunbelt Rentals' expansion into modular space through its Reliant Asset Management acquisition under the Aries Building Systems brand also signals how specialty lines can broaden addressable demand beyond general construction equipment, supporting bundled offers across infrastructure, commercial builds, and industrial sites.

Recent Industry Developments

- May 2026: United Rentals launched its AI-powered Equipment Agent within ChatGPT to help customers plan and select rental equipment for projects. The step extends the rental journey into a widely used interface, compressing time from planning to ordering and strengthening digital stickiness beyond branch-only interactions.

- October 2025: EquipmentShare opened its sixth Oregon branch in Redmond, adding local capacity and signaling plans to expand further within the state. The additional branch density supports faster delivery and service coverage, improving competitiveness for time-sensitive earthmoving and jobsite support rentals.

- January 2024: BigRentz partnered with Billd to offer financing options that cover material and labor needs for rental customers. Packaging equipment access with financing reduces purchasing friction for smaller contractors and can lift conversion for short-term and project-based rentals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from renting construction equipment to end users for a defined time period, ranging from short hires to longer agreements. It includes rental fees linked to heavy equipment used on construction and infrastructure sites, counted in USD terms.

Scope exclusions: Tool-only rental outlets and leasing arrangements that are packaged with full-time operators are excluded from this sizing.

Segmentation Overview

- By Equipment Type

- Earthmoving Equipment

- Backhoe Loaders

- Loaders

- Excavators

- Bulldozers

- Skid-Steer Loaders

- Other Earthmoving

- Material Handling Equipment

- Cranes

- Forklifts

- Dump Trucks

- Telehandlers

- Other Material Handling

- Concrete and Road Construction Equipment

- Power and Energy Equipment

- Other Equipment

- Earthmoving Equipment

- By Drive Type

- IC Engine

- Hybrid

- Electric

- Hydrogen Fuel Cell

- By Application

- Residential Construction

- Commercial Construction

- Industrial / Manufacturing

- Infrastructure (Roads, Bridges, Ports)

- Mining and Quarrying

- Oil and Gas

- By Rental Channel

- Offline (Branch-based)

- Online Platforms

- By Service Type

- Short-Term Rental (less than 1 Month)

- Medium-Term Rental (1 - 12 Months)

- Long-Term Rental (Over 1 Year)

- By Geography

- North America

- United States

- Canada

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base for construction activity and equipment demand signals, and then linking it back to rental usage. We typically refer to public sources such as construction spending and permits from the US Census Bureau, infrastructure and investment indicators from the World Bank, macro and price series from the IMF, and labor and cost data from the US Bureau of Labor Statistics.

To keep the model grounded, we also review customs and trade statistics (where applicable) from UN Comtrade, plus safety and equipment guidance from bodies such as OSHA, along with association publications and reputable press coverage on fleet trends and utilization. Company annual reports, investor presentations, and earnings transcripts are used to understand rental mix, pricing behavior, and regional exposure, and a paid subscription for company financials and news helps cross-check reported revenue lines and corporate actions. This list is illustrative, and many other sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test pricing and utilization assumptions, and to verify what is actually counted as rental revenue in different regions. We speak with rental operators, dealers, fleet managers, contractors, and industry experts across major demand centers, and then reconcile differences in definitions such as bare rental versus bundled services and attachments.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 46% |

| Mid tier: 40% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 21% | Managers: 50% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where construction output and project pipelines are converted into an equipment demand pool, which is then adjusted by rental penetration rates to arrive at rental market revenue. Once that structure is in place, the totals are corroborated with selective bottom-up checks, such as sampled rental rate cards and average utilization days applied to indicative fleet counts, followed by channel checks on how quickly rates are moving in key metros.

Inputs that tend to matter most include construction spending trends, infrastructure program timings, fleet utilization, average rental rates by major equipment classes, and equipment replacement cycles that influence rental availability and pricing. For forecasting, we use scenario analysis supported by a small set of macro and construction indicators, and the assumptions are tuned using what interviewees expect for utilization and rate progression. When bottom-up signals are incomplete for smaller countries or informal operators, we use proxy indicators such as construction intensity and equipment import patterns, and then review those adjustments again during validation.

Data Validation & Update Cycle

Outputs are checked against independent signals such as regional construction growth, reported rental revenue trends, and observable changes in utilization and the rate environment. If a country or equipment class shows a sharp jump that does not match these signals, the drivers are traced back to the model inputs, and follow-up conversations are triggered to confirm the assumption.

Before sign-off, the work goes through multi-step analyst review with variance checks across regions and time, and the final file is inspected for currency timing and consistent definitions. Reports are refreshed annually, and interim updates are made when material events occur, such as major infrastructure stimulus, demand shocks, or notable pricing shifts. Right before delivery, a fresh pass is done so the latest public releases and key field feedback are reflected.

Mordor Intelligence's Construction Equipment Rental Market Sizing Compared With Other Published Estimates

Published market sizes for construction equipment rental can look far apart, even when they use similar market names, because the counted revenue lines are not always the same. The spread usually comes from how firms treat bundled services, whether operator-included hiring is added, and how rental rates and utilization are rolled forward into the forecast years.

Some external estimates fold in broader rental activity that can include operator-led contracting style hires and adjacent rental categories, which inflates the comparable total. In Mordor Intelligence's model, the count is limited to rental revenue for construction equipment hired without an operator, and tool-hire outlets are not included, which shifts the 2025 total versus broader definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 135.82 B (2025) | |

| Global Consultancy A | USD 213.68 B (2025) | Uses a wider definition of construction equipment rental that also references mining use cases, and the public summary does not clarify exclusions such as operator-included hires or tool-only rental, which can raise the addressable revenue pool. |

| Industry Publisher B | USD 132.35 B (2025) | Stays closer on the year but applies a different growth path, likely driven by faster rate escalation and utilization assumptions and a broader service-contract reading that may include more bundled items beyond bare rental. |

Looking across the table, the biggest differences come from how wide the rental definition is and how rental rate and utilization assumptions are carried into future years. By keeping inclusions explicit and then checking the totals against construction activity and operator feedback, we keep the estimate traceable to repeatable inputs instead of hidden scope add-ons.

Key Questions Answered in the Report

What is the projected value of the construction equipment rental market in 2031?

It is forecast to reach USD 179.21 billion, growing at a 4.85% CAGR from 2026 to 2031.

Which segment leads by construction equipment rental market share?

Earthmoving equipment commanded 41.05% share in 2025 and is still growing faster than the overall market.

Why are contractors shifting to equipment rentals?

Rentals convert capital outlays into operating expenses, preserve liquidity, and align costs with project timelines.

Which geography is expanding the fastest?

The Middle East and Africa show a 6.72% CAGR to 2031, driven by mega-projects under Saudi Vision 2030.

How big is the opportunity for online rental platforms?

Online platforms are advancing at 9.84% CAGR, almost double the overall market pace, thanks to mobile-first adoption in Asia-Pacific and the Middle East.

Page last updated on: