Confectionary Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 14.18 Billion |

| Market Size (2030) | USD 17.58 Billion |

| Growth Rate (2025 - 2030) | 4.38% CAGR |

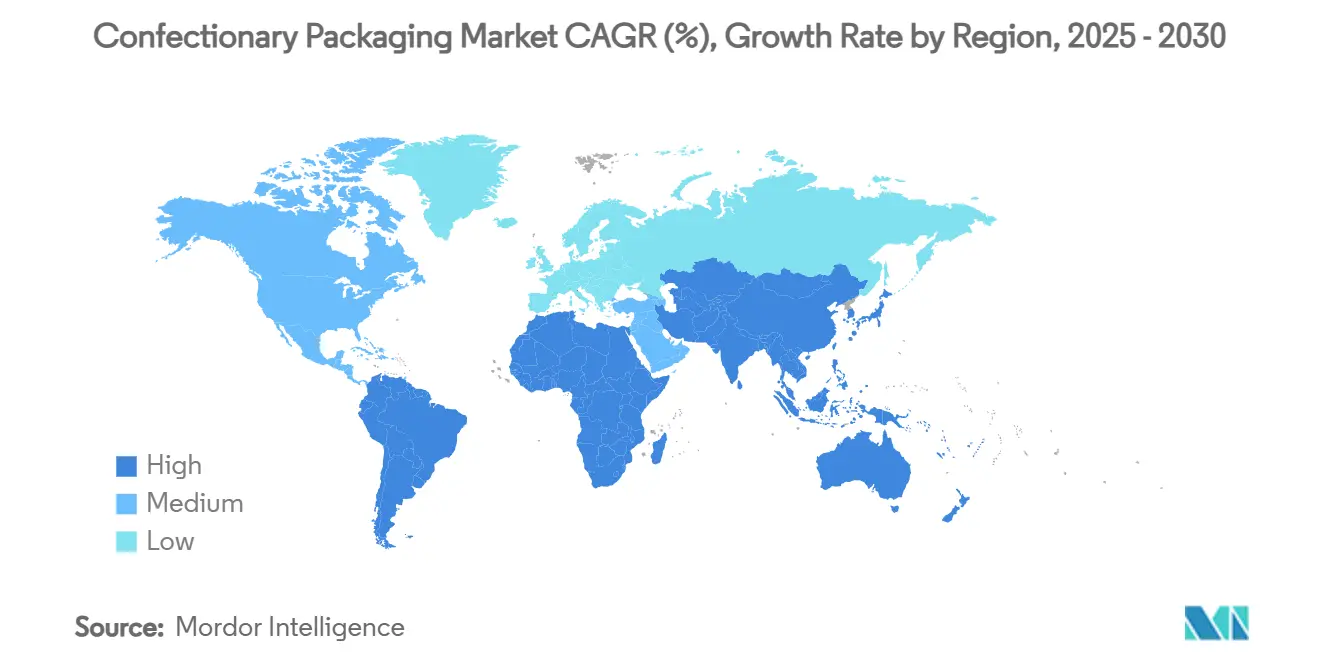

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Confectionary Packaging Market Analysis by Mordor Intelligence

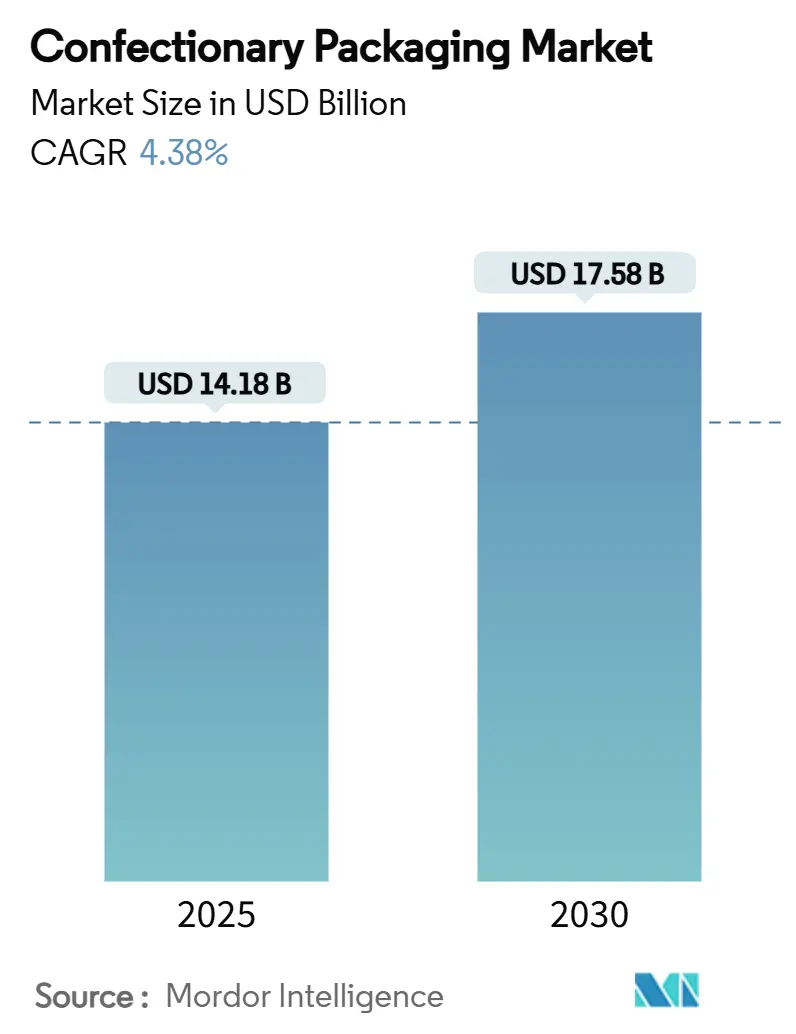

The confectionery packaging market size is valued at USD 14.18 billion in 2025 and is forecast to reach USD 17.58 billion by 2030, growing at a 4.38% CAGR. The confectionery packaging market is expanding as brands respond to stricter sustainability rules, premiumization of gifting formats, and rapid advances in digital printing that allow quick SKU launches. Flexible materials remain central because stand-up pouches and portion packs answer convenience and portion-control needs. EU and North American regulations mandating higher recycled content are steering investments toward bio-based films and recyclable paper, while QR-enabled smart packs satisfy traceability obligations and deepen consumer engagement. Raw-material price swings and tariffs on aluminum foil are squeezing margins, pushing producers to diversify substrates and redesign packs for cost efficiency.

Key Report Takeaways

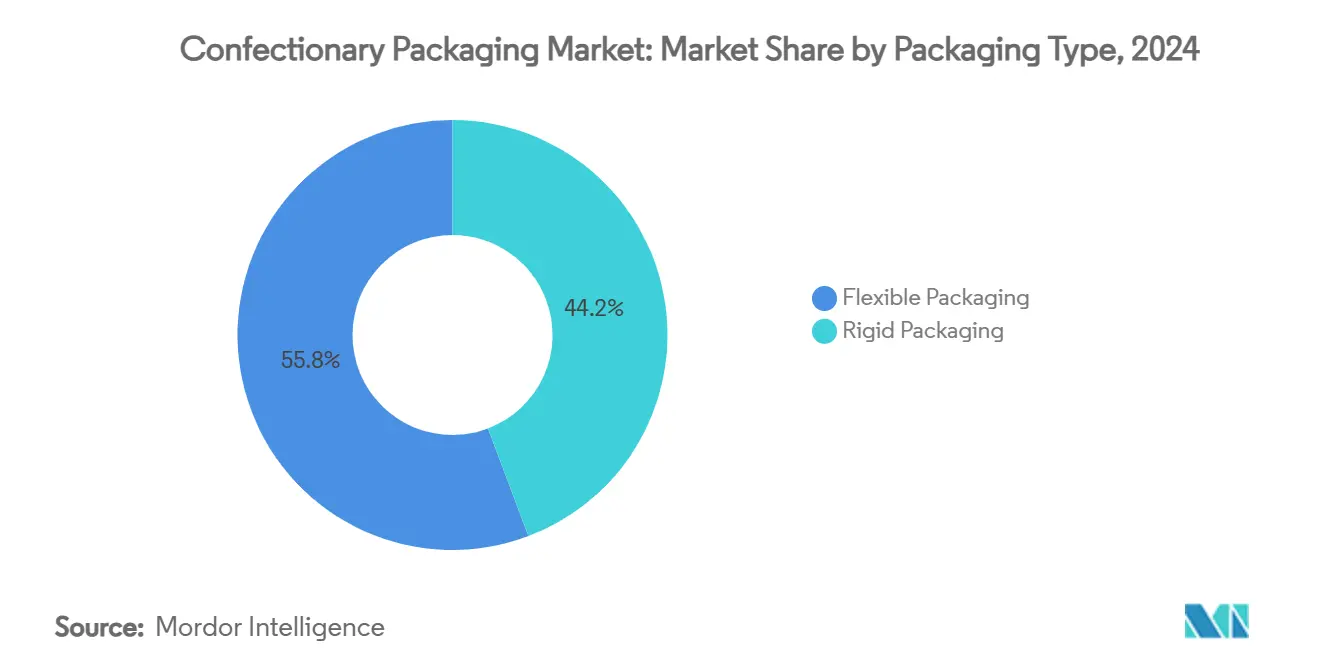

- By packaging type, flexible solutions led with 54.64% confectionery packaging market share in 2024; rigid formats are projected to grow fastest at a 5.87% CAGR through 2030.

- By material, plastics held 60.12% share of the confectionery packaging market size in 2024; bio-based and compostable films will expand at 7.43% CAGR to 2030.

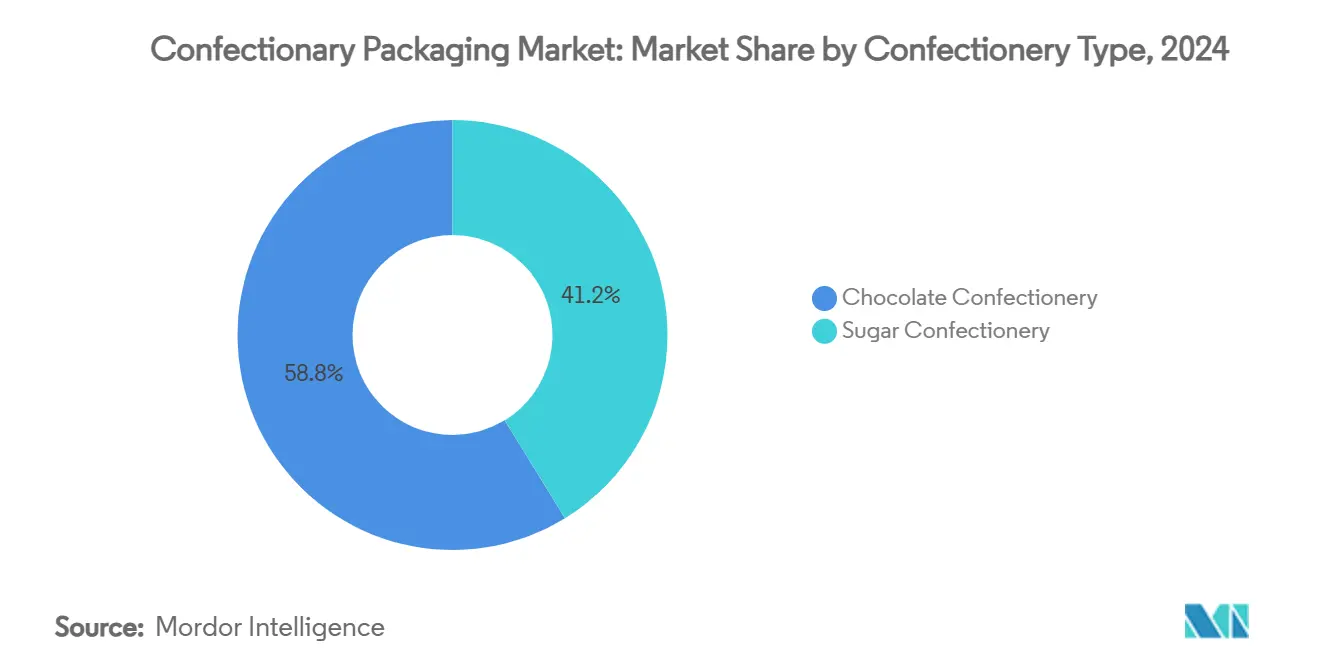

- By confectionery type, chocolate accounted for 58.76% of the confectionery packaging market in 2024, while sugar confectionery is advancing at a 5.87% CAGR.

- By distribution channel, direct sales dominated 65.34% of the confectionery packaging market in 2024; indirect sales record the highest projected CAGR at 5.65% through 2030.

- North America commanded 34.54% share of the confectionery packaging market in 2024; Asia-Pacific posts the fastest regional CAGR at 8.01% to 2030.

Global Confectionary Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of gifting formats | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Eco-friendly material shift | +0.9% | EU-led, expanding to North America and Asia-Pacific | Long term (≥ 4 years) |

| Boom in stand-up pouches and portion packs | +0.8% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Digital printing for seasonal SKUs | +0.4% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| QR-enabled traceability packaging | +0.3% | EU-driven, global adoption following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Gifting Formats

Luxurious multi-sensory designs—such as laser-cut boxes with origami inserts or magnetic closures—are redefining consumer expectations of seasonal products. Packaging can account for 15–20% of product cost in premium lines, far above mass-market ratios, yet shoppers willingly pay for distinctive unboxing experiences. Interactive elements like Cadbury’s thermochromic wrappers or audio tins extend storytelling into social channels, translating pack aesthetics into viral content. [1]Packaging Insights, “Cadbury releases color-changing chocolate bar wraps for summer range,” packaginginsights.comArtisanal brands leverage these design cues to challenge multinational rivals by imbuing provenance narratives and limited-edition collectability.

Eco-friendly Material Shift

The EU Packaging and Packaging Waste Regulation stipulates 65% recycled content in plastic packs by 2040 and full recyclability by 2030, triggering large investments in cellulosic films and mono-material laminates. Clarifoil cellulosic structures and paper wraps for 419 Smarties SKUs exhibit technical viability, yet current 20–30% cost premiums limit adoption capacity for smaller converters. [2]Celanese, “BioPolymer Solutions,” celanese.com Early movers are unlocking supply-chain advantages and reputational gains.

Boom in Stand-up Pouches and Portion Packs

Stand-up pouches improve shelf visibility and ship-ability, prompting Hershey and Mars to redesign product lines around resealable formats with twist-wrap or zipper closures.[3]Snack and Bakery, “How the Hershey Company continues to innovate,” snackandbakery.com Portion packs dovetail with calorie-cap pledges under Always-A-Treat, enabling indulgence within mindful consumption guidelines. Enhanced convenience accelerates retail velocity across e-commerce and c-store channels.

Digital Printing for Seasonal SKUs

Eliminating plates lets mid-sized confectioners print small-lot Christmas or Valentine runs without incurring high setup costs, shrinking time-to-shelf from weeks to days. Transition to 2D barcodes adds regulatory data and anti-counterfeit functions while retaining vibrant graphics, democratizing premium aesthetics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Compliance costs of new EU plastics rules | -0.6% | EU primary, spillover to global suppliers | Medium term (2-4 years) |

| Aluminum-foil supply disruption risk | -0.4% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Shelf-life limits of compostable films | -0.3% | EU-driven, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material Price Volatility

Tariffs have lifted aluminum-foil import costs by 25%, while resin swings of 10–15% per quarter strain flexible-pack budgets. Cardboard increased USD 70 per ton in January 2025, and a 400% cocoa price jump has forced reformulations altering portion sizes and barrier needs. SMEs lacking hedging tools face erosion in profitability.

Compliance Costs of New EU Plastics Rules

Recycled PET thresholds of 30% by 2030 and 50% by 2040 require major quality-assurance upgrades, while PFAS bans eliminate specific coating chemistries. Extended Producer Responsibility fees and reporting expand overhead, tilting advantage toward large players with robust compliance systems.

Segment Analysis

By Packaging Type: Flexible Solutions Drive Innovation

Flexible formats capture 54.64% confectionery packaging market share in 2024, buoyed by consumer desire for portability and resealability. Stand-up pouches, boosted by 5.87% CAGR forecasts, align with e-commerce shipping needs and deliver high-impact graphics that elevate brand visibility. The segment’s dynamism stems from zipper and spout innovations that extend freshness while supporting portion-controlled indulgence. Wrappers and bags remain essential for individual pieces and family packs, respectively, but brands are shifting SKUs toward pouches to balance shelf impact and material use.

Rigid solutions maintain relevance for premium gifting where structural integrity and tactile cues shape perceived value. Folding cartons dominate rigid volume thanks to efficient die-cutting and superior printability; corrugated boxes protect larger assortments moving through last-mile networks. Paper-based rigid packs benefit from recyclability perceptions, while molded pulp inserts replace plastic trays to meet eco mandates. Glass jars and gift tins serve niche luxury SKUs, leveraging weight and acoustics to communicate heritage and quality.

By Material Type: Sustainability Pressures Reshape Preferences

Plastics retained 60.12% share of the confectionery packaging market in 2024, but bio-based and compostable films top growth tables at 7.43% CAGR due to mandatory recycled-content clauses and heightened consumer scrutiny. Advances in mono-material PE/PP laminates and chemical recycling promise to extend plastics’ reign by easing recyclability, yet rising compliance fees are narrowing cost gaps with paper. Paperboard’s recyclability and tactile naturalness make it a favored premium medium; the Smarties paper transition underscores feasibility at industrial scale.

Metal foil excels in light and gas barrier but is vulnerable to tariff-driven price shocks and carbon-footprint concerns. Suppliers are down-gauging thickness and upping recycled content to retain relevance. Glass, though heavy, underpins limited-edition pralines and origin stories where reusability justifies cost.

By Confectionery Type: Chocolate Dominance Faces Sugar Innovation

Chocolate lines employ high-barrier wraps and rigid boxes to safeguard sensory attributes in diverse climates, owning the largest 58.76% share of the confectionery packaging market. Seasonal assortments exploit elaborate rigid packs with embossing and gloss varnishes to justify premium outlays during Valentine’s and Easter campaigns. Tablets and bars rely on aluminum-paper laminates for grease resistance, yet mono-material PE solutions are entering trials to meet recyclability goals.

Sugar confectionery’s 5.87% CAGR is powered by social-media-fueled hits such as freeze-dried candy, worth USD 2.4 billion globally, prompting flexible pack upgrades for texture protection. Gummies and jellies migrate to resealable pouches, while mints adopt slim roll-wraps that slip into pockets. Lollipop producers test compostable sticks and PLA flow-wraps to match sustainability pledges.

By Distribution Channel: Direct Sales Maintain Dominance

Direct contracts with supermarkets and discounters underpin 65.34% of 2024 revenue, granting brands modulation of pack sizes for endcap and seasonal displays. Eye-catching secondary packs amplify impulse purchases, and joint promotions acquaint shoppers with limited flavors. The confectionery packaging market size tied to direct shelf presence will keep rising but at a slower pace than online alternatives.

Indirect channels—e-commerce marketplaces, c-stores, vending, and specialty shops—clock a 5.65% CAGR, spurring design tweaks for parcel durability and click-and-collect efficiencies. Shippers adopt corrugated crash-lock cartons with internal cushioning to reduce breakage claims, while portion-controlled packs diversify c-store impulse offerings. Brands are trialing minimal void fills and paper-based dunnage to harmonize sustainability objectives with last-mile fulfillment constraints.

Geography Analysis

North America retains 34.54% share of the confectionery packaging market in 2024, buoyed by a mature gifting culture and swift uptake of interactive packs. Significant capex, such as Mars’ USD 70 million Hackettstown innovation studio, channels R&D into recyclable multilayers and smart labels. Extended Producer Responsibility frameworks in US states are compelling earlier adoption of recycled content and transparent fee structures.

Europe is navigating the most comprehensive regulatory overhaul, with the Packaging and Packaging Waste Regulation cementing recycled-content quotas and recyclability definitions. Capital spending on cellulosic films, paper wraps, and mechanical recycling lines is reshaping supplier contracts and accelerating joint development projects between converters and brand owners. Investments such as Mondelez’s CHF 65 million upgrade to its Toblerone site in Bern demonstrate commitment to local production compliant with the new rule set.

Asia-Pacific records the swiftest 8.01% CAGR as urbanization widens exposure to global confectionery brands and e-commerce unlocks rural demand. China’s USD 84.05 billion candy sector champions premium gift boxes and festival assortments, while Indonesia’s projected doubling to USD 2.01 billion by 2029 spurs micro-packs priced for value seekers. Varied recycling infrastructures force adaptive pack designs: Japan prefers mono-material PP trays for efficient sorting, whereas India pushes compostable wraps to meet emerging plastic-waste rules.

Competitive Landscape

The confectionery packaging market exhibits moderate fragmentation, with global leaders Amcor, Mondi, and Sealed Air leveraging multinational footprints and diversified substrate portfolios. These players co-develop recycle-ready laminates like AmPrima for Cadbury’s 300 million sharing bars, achieving 80% recycled content and securing retailer acceptance. Mid-tier challengers such as Accredo specialize in bio-based pouches that sequester CO₂, capturing environmentally conscious contracts.

Strategic moves concentrate on vertical integration and M&A: Mars’ USD 35.9 billion acquisition of Kellanova expands in-house packaging R&D assets. Constantia Flexibles’ sale signals ongoing portfolio optimization among private-equity holders, potentially shifting supplier alliances. Investment in pilot lines and digital-print modules allows both majors and niche players to meet rapid artwork changeovers demanded by social-media campaigns.

Emerging opportunities reside in compostable barrier coatings and refill systems suited for zero-waste retail. Yet challenges persist: supply instability in aluminum foil, compliance complexity, and the cost of scaled chemical recycling. Players capable of balancing performance, sustainability, and cost through continuous innovation are positioned to strengthen share.

Confectionary Packaging Industry Leaders

Amcor Group

Huhtamaki Oyj

Constantia Flexibles Holding GmbH

Sonoco Products Company

Mondi Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Green Bay Packaging expanded its US facility to bolster confectionery pack capacity.

- May 2025: Bakers invested GBP 5 million in Galaxy Packtech pouch-maker machines to scale mono-material pouches.

- May 2025: Mars allocated USD 70 million to an R&D studio and packaging lab at Hackettstown, New Jersey.

- April 2025: Hershey opened a 250,000 sq ft Reese Chocolate Processing plant as part of a USD 1 billion supply-chain upgrade.

- March 2025: Wendel Group exited Constantia Flexibles, triggering speculation on consolidation paths.

Global Confectionary Packaging Market Report Scope

Confectionery packaging refers to the materials and processes used to package sweet products such as candies, chocolates, gummies, cookies, and other sugar-based treats. The primary goal of confectionery packaging is to protect the product, maintain its freshness, and make it visually appealing to consumers. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The confectionery packaging market is segmented by packaging type ((Flexible Packaging (Wrappers, Sackets, Liners and Pouches) and Rigid Packaging (Folding Cartons, Corrugated Boxes, Trays and Containers)), by material type (Paper, Plastic, Metal, Aluminum and Glass), by confectionary type ((Chocolate Confectionary (Slabs/Bars/Blocks, Boxed Assortments, and Other Chocolate Confectionaries), Sugar Confectionary (Jellies, Mints, Toffees, Lollipops and Other Sugar Confectionaries)) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Flexible Packaging | Wrappers |

| Bags | |

| Pouches | |

| Other Flexible Packaging | |

| Rigid Packaging | Folding Cartons |

| Corrugated Boxes | |

| Trays | |

| Other Rigid Packaging |

| Paper and Paperboard |

| Plastic |

| Metal |

| Glass |

| Bio-based and Compostable Films |

| Chocolate Confectionery | Slabs/Bars/Blocks |

| Boxed Assortments | |

| Other Chocolate Confectionery | |

| Sugar Confectionery | Jellies and Gummies |

| Mints | |

| Toffees and Caramels | |

| Lollipops | |

| Other Sugar Confectionery |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Type | Flexible Packaging | Wrappers | |

| Bags | |||

| Pouches | |||

| Other Flexible Packaging | |||

| Rigid Packaging | Folding Cartons | ||

| Corrugated Boxes | |||

| Trays | |||

| Other Rigid Packaging | |||

| By Material Type | Paper and Paperboard | ||

| Plastic | |||

| Metal | |||

| Glass | |||

| Bio-based and Compostable Films | |||

| By Confectionery Type | Chocolate Confectionery | Slabs/Bars/Blocks | |

| Boxed Assortments | |||

| Other Chocolate Confectionery | |||

| Sugar Confectionery | Jellies and Gummies | ||

| Mints | |||

| Toffees and Caramels | |||

| Lollipops | |||

| Other Sugar Confectionery | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the confectionery packaging market?

The confectionery packaging market size stands at USD 14.18 billion in 2025 and is projected to reach USD 17.58 billion by 2030 at a 4.38% CAGR.

Which packaging type leads global revenue?

Flexible solutions hold 54.64% confectionery packaging market share in 2024, driven by stand-up pouches and portion-controlled packs.

Why is Asia-Pacific the fastest-growing region?

Urbanization, expanding middle classes, and strong e-commerce penetration push Asia-Pacific’s confectionery packaging market to an 8.01% CAGR through 2030.

How are EU regulations affecting material choices?

The EU Packaging and Packaging Waste Regulation mandates higher recycled content and full recyclability, accelerating adoption of bio-based films, paper wraps, and mono-material plastics.

What role does digital printing play in seasonal confectionery?

Digital printing cuts plate costs, enabling economical short runs for holiday SKUs and supporting rapid response to social-media trends.

How volatile are raw-material costs for confectionery packaging?

Tariffs, resin price swings, and cocoa shortages have raised aluminum foil and plastic costs by double-digit percentages, pressuring pack redesigns and alternative substrates.