| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.88 Billion |

| Market Size (2030) | USD 11.69 Billion |

| CAGR (2025 - 2030) | 8.22 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Conductive Silicone Market Analysis

The Conductive Silicone Market size is estimated at USD 7.88 billion in 2025, and is expected to reach USD 11.69 billion by 2030, at a CAGR of 8.22% during the forecast period (2025-2030).

The conductive silicone industry is experiencing significant transformation driven by rapid technological advancements and evolving end-user requirements across multiple sectors. The automotive sector, a major consumer of conductive silicone, has shown remarkable growth with global vehicle production reaching 93.54 million units in 2023, marking a 10.26% increase from the previous year. This surge in automotive production has been accompanied by a significant shift towards electric vehicles, with global EV sales reaching 14 million units in 2023, concentrated primarily in China, Europe, and the United States. The automotive industry's evolution towards more sophisticated electronic materials and advanced manufacturing processes has created new applications for conductive silicone materials.

The semiconductor industry's expansion has emerged as a crucial factor shaping the conductive silicone landscape. According to the Semiconductor Industry Association, global demand for semiconductor manufacturing capacity is projected to increase by 56% by 2030. This growth is supported by significant investments in new manufacturing facilities worldwide, with major players like GlobalFoundries receiving substantial incentives under initiatives such as the CHIPs and Science Act. The increasing complexity of semiconductor devices and the need for advanced thermal management solutions have created new opportunities for conductive silicone applications in chip manufacturing and packaging, particularly as thermal interface materials.

The construction and infrastructure sectors are witnessing substantial developments that influence the conductive silicone market. Major construction projects, particularly in emerging economies, are driving demand for advanced building materials and electronic systems that require conductive silicone components. The integration of smart building technologies and the growing emphasis on energy-efficient construction have created new applications for conductive silicone in building automation systems, thermal management solutions, and electronic installations.

The medical device industry is experiencing rapid innovation, particularly in the development of wearable technologies and advanced diagnostic equipment. Companies like Freudenberg Medical have made significant strides in combining silicone with conductive polymer fillers for applications in neurostimulation and pain treatment. The industry has seen breakthrough developments in non-surgical medical devices, including innovative applications such as mouthguards for treating periodontitis and wearable devices for managing Parkinson's disease symptoms. These advancements have opened new avenues for conductive silicone usage in medical applications, particularly in devices requiring both biocompatibility and electrical conductivity.

Conductive Silicone Market Trends

Growing Demand from the Electronics Industry

The electronics industry has emerged as a primary driver for conductive silicone demand, primarily due to its superior electrical conductivity, thermal management capabilities, and versatile applications in electronic devices. Conductive silicone's unique properties enable efficient transfer of electrical current, making it essential for applications requiring signal transmission, data transfer, and power distribution. The material's growing importance is evidenced by significant investments across major electronics manufacturing nations. For instance, Germany, Europe's largest electronics market, employs over 1.6 million workers in the electrical and electronics sector, with 30% of all R&D employees working specifically in electronics and microtechnology. Additionally, as part of the France 2030 investment plan, the French government has committed nearly EUR 800 million to support the academic research ecosystem for electronic technologies development by 2030.

The semiconductor and electronic components manufacturing sector has witnessed substantial expansion, particularly in Asia. This is exemplified by major projects such as Huahong Group's Wuxi facility, which planned a 12-inch specialty process production line with a monthly production capacity of 83,000 pieces in 2023. The growing sophistication of electronic devices has increased the demand for high-performance conductive materials, with conductive silicone being preferred for its reliability and effectiveness in thermal management applications. This trend is further supported by strategic initiatives like China's "Made in China 2025" plan, which aims to achieve an output of USD 305 billion by 2030 to meet 80% of domestic demand. The material's application in smartphones, TVs, and other personal electronic devices has become particularly crucial as these segments continue to show strong growth in production volumes.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Usage in the Solar Industry

The solar industry has become a significant growth driver for the conductive silicone market, primarily due to its essential role in solar panel manufacturing and installation. Conductive silicone serves as a crucial component in solar applications, providing thermal management, electrical conductivity, and environmental protection properties that are vital for solar panel efficiency and longevity. The material's resistance to UV rays, temperature changes, and superior transparency makes it particularly valuable in improving panel efficiency and reducing maintenance requirements. This is evidenced by substantial investments in solar energy infrastructure, such as China's commitment to install 230 GW of wind and solar capacity, announced in November 2023, supported by a significant investment of USD 140 billion in various wind and solar projects in 2023.

The integration of conductive silicone in solar applications has been further accelerated by grid modernization initiatives and energy storage developments. For instance, China has allocated USD 455 billion for grid investments from 2021-2025, representing a 60% increase from the previous decade, while also doubling its grid-connected energy storage capacity to reach 67 GW in 2023. Conductive silicone plays a vital role in these developments through its use as conductive encapsulant and conductive sealant in solar panel manufacturing, providing essential protection against environmental factors while maintaining optimal electrical and thermal performance. The material's ability to enhance the durability and efficiency of solar installations has made it an integral component in the renewable energy sector's continued expansion and technological advancement.

Segment Analysis: Product Type

Elastomers Segment in Conductive Silicone Market

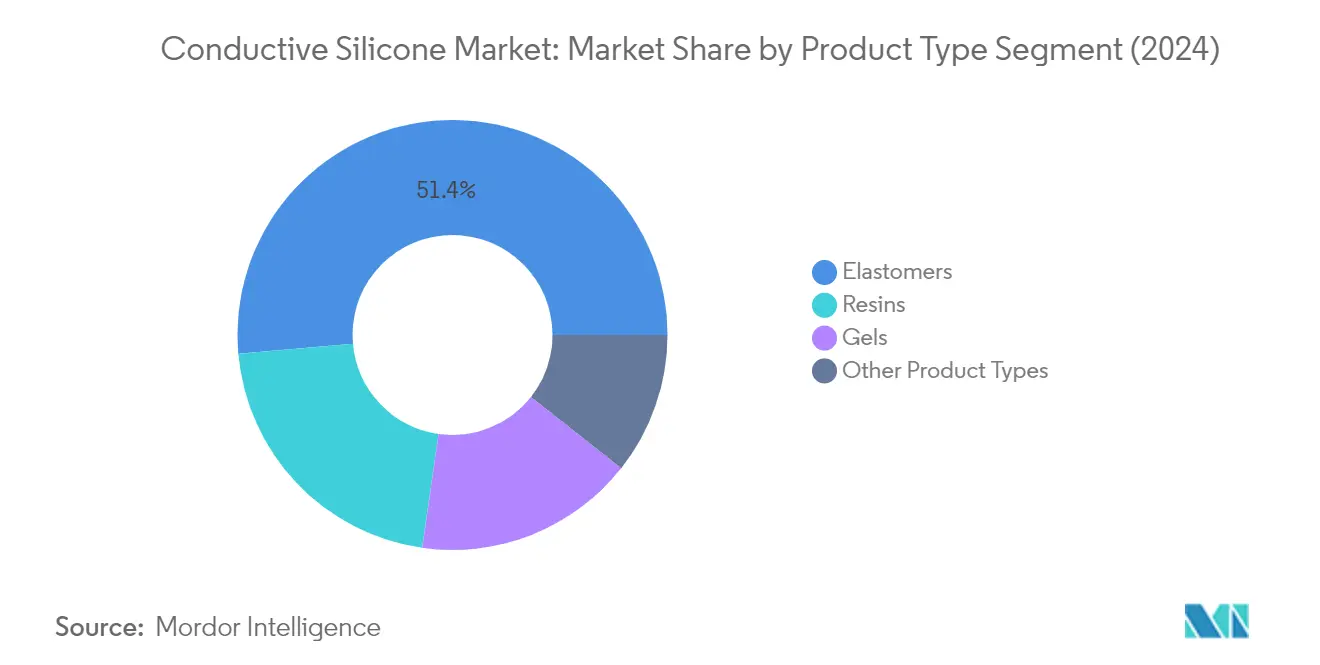

The conductive elastomers segment dominates the global conductive silicone market, accounting for approximately 51% of the total market share in 2024. This significant market position is attributed to elastomers' superior electrical insulation and fire-retardant properties, making them essential in various applications. The segment's growth is primarily driven by increasing demand from the automotive and electronics industries, where these materials are extensively used in manufacturing ignition wires, spark plug boots, and fuel injector seals. Additionally, the rising adoption of electric vehicles has further boosted the demand for elastomers in battery components and thermal management systems. The segment also benefits from its widespread use in EMI shielding applications across consumer electronics, telecommunications, and aerospace industries.

Gels Segment in Conductive Silicone Market

The gels segment is emerging as the fastest-growing category in the conductive silicone market, projected to expand at approximately 9% CAGR from 2024 to 2029. This remarkable growth is driven by the increasing adoption of silicone gels in electronic applications where high flexibility and encapsulation are critical requirements. The segment's expansion is further supported by the growing demand for thermal interface materials in advanced electronic devices and the rising need for protection against vibration, moisture, corrosion, harsh environments, and thermal and mechanical shock. The automotive electronics sector, particularly in electric vehicles, has become a significant growth driver for conductive silicone gels, as these materials are essential for protecting sensitive electronic components while ensuring optimal thermal conductivity.

Remaining Segments in Product Type

The resins and other product types segments, including pastes, gap fillers, adhesives, and greases, continue to play vital roles in the conductive silicone market. Resins are particularly valued for their superior heat stability, electrical conductivity, low surface energy, and biocompatibility properties, making them essential in semiconductor devices and wearable technology applications. The other product types segment, while smaller in market share, serves specialized applications such as thermal interface materials, potting compounds, and specialized adhesives. These segments are crucial in addressing specific industry requirements, particularly in emerging applications within the medical devices sector and advanced electronic manufacturing processes.

Segment Analysis: Application

Adhesives and Sealants Segment in Conductive Silicone Market

The adhesives and sealants segment dominates the global conductive silicone market, commanding approximately 45% of the market share in 2024, while also exhibiting the highest growth rate with a projected growth of nearly 10% from 2024 to 2029. This segment's prominence is primarily driven by its extensive application in the electronics industry, where conductive silicone adhesives and sealants play a crucial role in bonding and sealing electronic components while maintaining electrical conductivity. The automotive sector's increasing demand for these materials in electric vehicle manufacturing, particularly for battery assembly and thermal management systems, further strengthens this segment's position. Additionally, the growing adoption of conductive silicone adhesives in renewable energy applications, especially in solar panel manufacturing and wind turbine assembly, contributes significantly to its market leadership.

Remaining Segments in Application Market

The conductive silicone market encompasses several other significant application segments, including thermal interface materials, encapsulants and potting compounds, conformal coatings, and other specialized applications. Thermal interface materials represent a crucial segment, facilitating efficient heat dissipation in electronic devices and power systems. Encapsulants and potting compounds serve vital roles in protecting electronic components from environmental factors while maintaining electrical conductivity. Conformal coatings provide essential protection for printed circuit boards and electronic assemblies, particularly in harsh operating conditions. These segments collectively address diverse industry needs across automotive, electronics, aerospace, and medical device sectors, with each offering unique properties and advantages for specific applications.

Segment Analysis: End-User Industry

Electrical and Electronics Segment in Conductive Silicone Market

The electrical and electronics segment dominates the global conductive silicone market, commanding approximately 62% of the total market share in 2024, while also exhibiting the strongest growth trajectory for the forecast period 2024-2029 at around 9% CAGR. This segment's prominence is primarily driven by the extensive use of conductive silicone in electronic applications such as EMI/RFI shielding, conductive silicone gasket, and thermal interface materials. The segment's growth is further bolstered by the rapid expansion of semiconductor manufacturing facilities worldwide, with significant investments being made in countries like the United States, Japan, and South Korea. The increasing demand for electronic devices, coupled with the rising adoption of electric vehicles and the growing focus on renewable energy systems, continues to drive the demand for conductive silicone in this sector. Additionally, the segment benefits from the ongoing technological advancements in consumer electronics and the increasing integration of electronic components in various industries.

Remaining Segments in End-User Industry

The automotive sector represents the second-largest end-user segment, driven by the increasing adoption of electric vehicles and the growing integration of electronic components in modern vehicles. The power generation sector maintains significant market presence due to the expanding renewable energy sector, particularly in solar and wind energy applications where conductive silicone plays a crucial role in ensuring efficient power transmission and component protection. The construction industry utilizes conductive silicone in various applications, including sealants and adhesives for building materials and thermal insulation systems. Other end-user industries, including aerospace and defense, consumer goods, and medical devices, collectively contribute to the market's diversity through specialized applications such as EMI shielding in military equipment, electronic component protection in consumer devices, and the development of innovative medical devices. The medical sector, in particular, shows promising growth potential with the increasing adoption of wearable medical devices and advanced healthcare technologies utilizing conductive silicone components.

Conductive Silicone Market Geography Segment Analysis

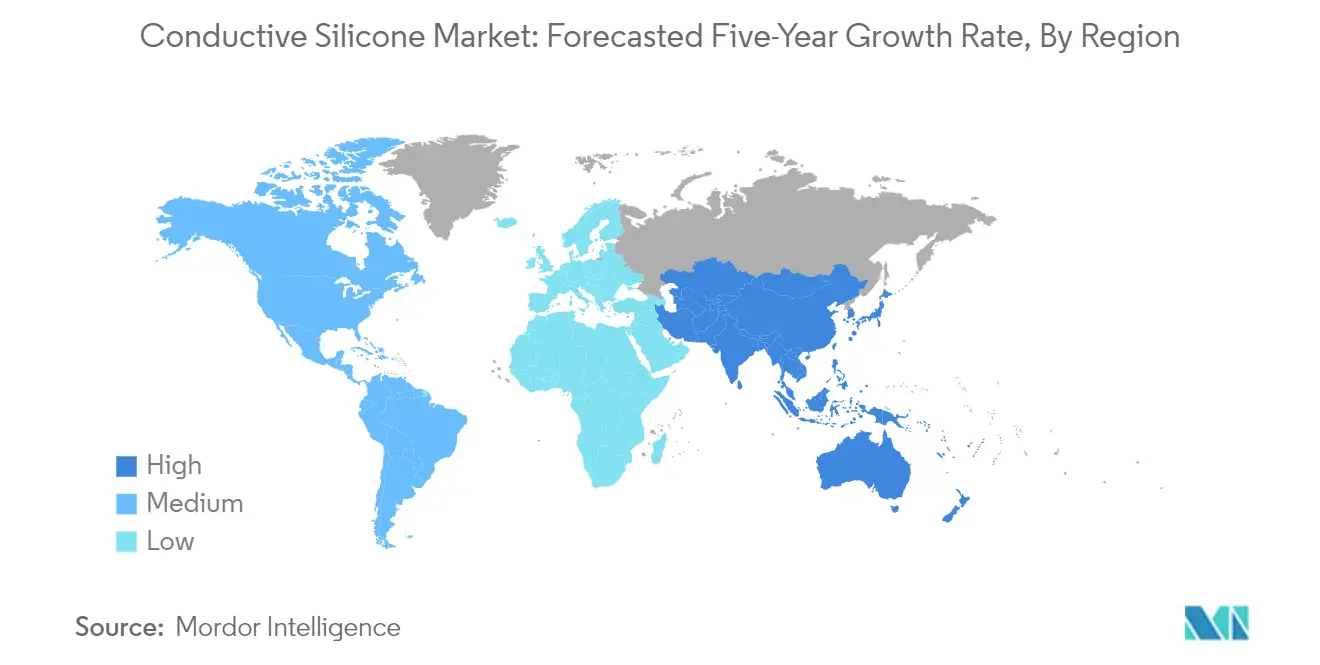

Conductive Silicone Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic conductive silicone market, driven by robust growth in electronics manufacturing, automotive production, and renewable energy sectors. Countries like China, India, Japan, and South Korea serve as major manufacturing hubs, while emerging economies such as Malaysia, Thailand, Indonesia, and Vietnam are witnessing increased industrial activities. The region's dominance is supported by favorable government policies promoting domestic manufacturing, particularly in semiconductors and electric vehicles, alongside significant investments in renewable energy infrastructure.

Conductive Silicone Market in China

China dominates the Asia-Pacific conductive silicone market, holding approximately 46% share of the regional market in 2024. The country's market leadership is driven by its position as the world's largest electronics manufacturing base and automotive market. China's semiconductor industry has seen substantial growth with major investments in chip manufacturing facilities. The country has also emerged as a leader in electric vehicle production, with numerous domestic and international manufacturers establishing production facilities. Additionally, China's commitment to renewable energy development, particularly in the solar and wind power sectors, continues to drive demand for conductive silicone materials.

Conductive Silicone Market Growth in India

India represents the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 11% from 2024 to 2029. The country's market expansion is fueled by increasing investments in electronics manufacturing, with the government's push toward making India a global electronics manufacturing hub. The automotive sector's growth, particularly in electric vehicle manufacturing, has attracted significant investments from major global manufacturers. Furthermore, India's ambitious renewable energy targets and the development of solar power projects across the country are creating substantial opportunities for conductive silicone applications.

Conductive Silicone Market in North America

North America represents a significant market for conductive silicone, characterized by advanced technological adoption and a strong presence in high-end applications. The region's market is primarily driven by developments in electronics, automotive, and renewable energy sectors across the United States, Canada, and Mexico. The presence of major manufacturers and ongoing investments in research and development contribute to the region's market sophistication, particularly in specialized applications for aerospace and medical devices.

Conductive Silicone Market in United States

The United States leads the North American market, commanding approximately 85% of the regional market share in 2024. The country's dominant position is supported by its robust electronics industry and significant investments in semiconductor manufacturing. The automotive sector's transformation toward electric vehicles, coupled with substantial investments in renewable energy projects, particularly in wind and solar power, continues to drive market growth. The country's strong focus on research and development in medical devices and aerospace applications further reinforces its market leadership.

Conductive Silicone Market Growth in United States

The United States also leads in terms of growth potential, with an expected growth rate of approximately 8% from 2024 to 2029. This growth is driven by increasing investments in domestic semiconductor manufacturing, supported by government initiatives like the CHIPS Act. The country's push toward electric vehicle production and renewable energy development creates sustained demand for conductive silicone materials. Additionally, innovations in medical devices and aerospace applications continue to open new opportunities for market expansion.

Conductive Silicone Market in Europe

The European market for conductive silicone is characterized by strong technological innovation and stringent quality standards. The region encompasses major industrial economies including Germany, the United Kingdom, France, Italy, Spain, Nordic countries, Turkey, and Russia. The market is driven by the region's strong automotive manufacturing base, growing renewable energy sector, and increasing focus on electronic component manufacturing, particularly in countries like Germany and France.

Conductive Silicone Market in Germany

Germany stands as the largest market for conductive silicone in Europe, with its strong industrial base and leadership in automotive manufacturing. The country's market is supported by its position as Europe's largest electronic industry and fifth-largest globally. Germany's commitment to electric vehicle production and renewable energy development, particularly in wind power, continues to drive market growth. The country's focus on Industry 4.0 and technological innovation further strengthens its market position.

Conductive Silicone Market Growth in France

France emerges as the fastest-growing market in Europe, driven by significant investments in electronics manufacturing and renewable energy sectors. The country's market growth is supported by government initiatives to develop its semiconductor industry and expand renewable energy capacity. France's automotive sector transformation and increasing focus on electric vehicle production create additional demand for conductive silicone materials. The country's investments in research and development for advanced electronics applications further contribute to market expansion.

Conductive Silicone Market in South America

The South American market for conductive silicone is experiencing steady growth, with Brazil, Argentina, and Colombia as key markets. Brazil emerges as both the largest and fastest-growing market in the region, supported by its substantial automotive manufacturing sector and increasing investments in renewable energy projects. The region's market development is driven by growing industrialization, increasing automotive production, and expanding electronics manufacturing capabilities. Government initiatives to promote domestic manufacturing and renewable energy development across these countries continue to create new opportunities for market growth.

Conductive Silicone Market in Middle-East and Africa

The Middle-East and Africa region presents an emerging market for conductive silicone, encompassing diverse economies including Saudi Arabia, Qatar, UAE, Nigeria, Egypt, and South Africa. South Africa emerges as both the largest and fastest-growing market in the region, driven by its relatively advanced manufacturing sector and increasing investments in renewable energy projects. The region's market growth is supported by ongoing infrastructure development, increasing industrial activities, and growing investments in renewable energy projects, particularly in solar power installations. The automotive sector's development and increasing electronics manufacturing activities in these countries further contribute to market expansion.

Get Analysis on Important Geographic Markets

Download PDF

Conductive Silicone Industry Overview

Top Companies in Conductive Silicone Market

The global conductive silicone market is led by major players including Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Momentive, and Avantor Inc. These companies are heavily focused on continuous product innovation, particularly in developing advanced thermally and electrically conductive silicone materials for emerging applications in the electronics and automotive sectors. Strategic expansions through new manufacturing facilities, especially in high-growth regions like Asia-Pacific, demonstrate their commitment to operational agility and market responsiveness. The industry witnesses regular product launches targeting specific end-user requirements, while companies maintain robust research and development initiatives to stay ahead of technological advancements. Market leaders are increasingly emphasizing sustainability in their product development processes while simultaneously strengthening their distribution networks and technical support capabilities to enhance customer relationships.

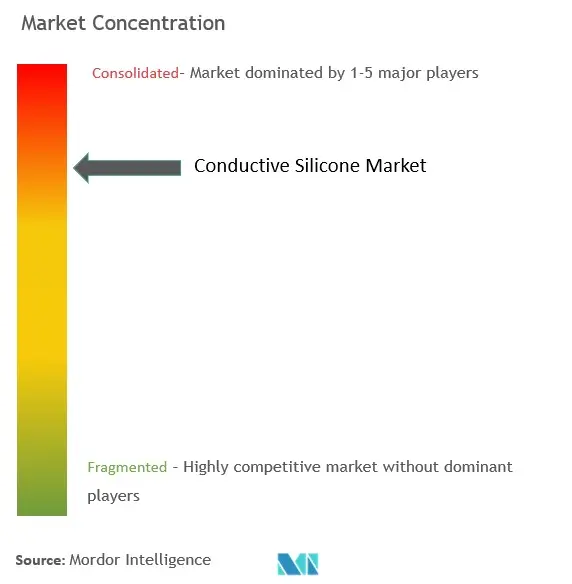

Consolidated Market with Strong Regional Players

The conductive silicone market exhibits a consolidated structure dominated by multinational conglomerates with diverse product portfolios and strong manufacturing capabilities. These major players benefit from backward integration in raw material production, particularly in silanes and siloxanes manufacturing, providing them significant cost advantages and supply chain control. The market has witnessed several strategic acquisitions, notably KCC Corporation's acquisition of Momentive, indicating a trend toward further consolidation and vertical integration in the industry.

Regional players maintain a significant presence in their respective territories through specialized product offerings and strong local distribution networks. The market's high entry barriers, including substantial capital requirements, technical expertise needs, and established customer relationships, contribute to its consolidated nature. Companies with established research and development capabilities and proven track records in delivering high-performance materials maintain dominant positions, while smaller players often focus on niche applications or specific geographic regions to maintain their market presence.

Innovation and Customization Drive Market Success

Success in the conductive silicone market increasingly depends on companies' ability to develop customized solutions for specific applications while maintaining cost competitiveness. Market leaders are strengthening their positions through investments in advanced manufacturing technologies, development of proprietary formulations, and expansion of technical support capabilities. The ability to provide comprehensive solutions, including product development support and application expertise, has become crucial for maintaining market share in high-value segments like electronics and automotive applications.

Companies seeking to gain ground must focus on developing specialized products for emerging applications while building strong relationships with key end-users in growing sectors like electric vehicles and renewable energy. The market's future success factors include the ability to navigate regulatory requirements, particularly regarding environmental compliance and safety standards. Players must also address the growing demand for sustainable products while maintaining performance characteristics. Building robust supply chain relationships and establishing strong technical service capabilities will be crucial for both established players and new entrants to succeed in this evolving market landscape.

Conductive Silicone Market Leaders

-

Wacker Chemie AG

-

Shin-Etsu Chemical Co., Ltd

-

Dow

-

Avantor Inc.

-

Momentive

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Conductive Silicone Market News

- May 2024: Momentive was acquired by KCC Corporation, which also resulted in the exit of minority shareholder SJL Partners LLC. KCC Corporation is now Momentive’s sole shareholder and would support its growth through its people, technology, and innovation.

- May 2024: Shin-Etsu Chemical decided to establish a new company, Shin-Etsu Silicone (Pinghu) Co. Ltd, in Zhejiang Province, China, and construct a new silicone products plant to expand its silicone business.

- December 2022: LegenDay developed conductive silicone components specifically for the healthcare and medical industries. These parts are made from high-quality silicone mixed with electrically conductive and inert particles and can be shielded from electromagnetic interference (EMI). LegenDay used conductive silicone that was less volatile and had a low ion content, which was especially good for highly sensitive medical electronic systems. This advanced composition made LegenDay's conductive silicone components well-suited for use in hermetically sealed, vacuum, or high-temperature environments, meeting the strict requirements of the healthcare and medical industries.

Conductive Silicone Market Report - Table of Contents

1. SCOPE OF THE REPORT

- 1.1 Scope of the Study

- 1.2 Study Assumptions and Market Definition

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Demand from the Electronics Industry

- 4.1.2 Increasing Usage in the Solar Industry

-

4.2 Restraints

- 4.2.1 Alternative to Conductive Silicone in EMI Shielding

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size In Value)

-

5.1 By Product Type

- 5.1.1 Elastomers

- 5.1.2 Resins

- 5.1.3 Gels

- 5.1.4 Other Product Types (Pastes, Gap Fillers, Adhesives, and Greases)

-

5.2 By Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Thermal Interface Materials

- 5.2.3 Encapsulant and Potting Compounds

- 5.2.4 Conformal Coatings

- 5.2.5 Other Applications (Biomedical and Photocatalysis)

-

5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Power Generation

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries (Industrial Machinery, Consumer Goods, and Aerospace)

-

5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Avantor Inc.

- 6.4.3 CHT Germany GmbH

- 6.4.4 Dongguan City Betterly New Materials Co. Ltd

- 6.4.5 Dow

- 6.4.6 Elkem ASA

- 6.4.7 Euro Technologies

- 6.4.8 Henkel AG & Co. Kgaa

- 6.4.9 Momentive

- 6.4.10 Parker Hannifin Corporation

- 6.4.11 Polymax Ltd

- 6.4.12 Shin-Etsu Chemical Co. Ltd

- 6.4.13 Silicone Solutions

- 6.4.14 Soliani Emc Srl

- 6.4.15 Specialty Silicone Products Inc.

- 6.4.16 Wacker Chemie AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technological Developments in Medical Devices

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Conductive Silicone Industry Segmentation

Conductive silicone comprises silicone materials infused with carbon, exhibiting commendable sensing characteristics. Its electrical resistance can be altered through compression or deformation, making it suitable for creating force or deformation sensors. The benefits of electrically conductive silicone materials encompass flexibility, resistance to heat and moisture, processability at low temperatures, simplified assembly, and their environmentally benign nature. Conductive silicone finds extensive utilization in diverse applications, spanning coating, printing, fastening, and bonding applications.

The conductive silicon market has been segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into elastomers, resins, gels, and other product types (pastes, gap fillers, adhesives, and greases). By application, the market is segmented into adhesives and sealants, thermal interface materials, encapsulants and potting compounds, conformal coatings, and other applications (biomedical and photocatalysis). Based on end-user industry, the market is segmented into automotive, construction, power generation, electrical and electronics, and other end-user industries (aerospace and defense, consumer goods, medical, and industrial machinery). The report also covers the market sizes and forecasts for the conductive silicone market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| By Product Type | Elastomers | ||

| Resins | |||

| Gels | |||

| Other Product Types (Pastes, Gap Fillers, Adhesives, and Greases) | |||

| By Application | Adhesives and Sealants | ||

| Thermal Interface Materials | |||

| Encapsulant and Potting Compounds | |||

| Conformal Coatings | |||

| Other Applications (Biomedical and Photocatalysis) | |||

| By End-user Industry | Automotive | ||

| Construction | |||

| Power Generation | |||

| Electrical and Electronics | |||

| Other End-user Industries (Industrial Machinery, Consumer Goods, and Aerospace) | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordic Countries | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Qatar | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Conductive Silicone Market Research FAQs

How big is the Conductive Silicone Market?

The Conductive Silicone Market size is expected to reach USD 7.88 billion in 2025 and grow at a CAGR of 8.22% to reach USD 11.69 billion by 2030.

What is the current Conductive Silicone Market size?

In 2025, the Conductive Silicone Market size is expected to reach USD 7.88 billion.

Who are the key players in Conductive Silicone Market?

Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd, Dow, Avantor Inc. and Momentive are the major companies operating in the Conductive Silicone Market.

Which is the fastest growing region in Conductive Silicone Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Conductive Silicone Market?

In 2025, the Asia Pacific accounts for the largest market share in Conductive Silicone Market.

What years does this Conductive Silicone Market cover, and what was the market size in 2024?

In 2024, the Conductive Silicone Market size was estimated at USD 7.23 billion. The report covers the Conductive Silicone Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Conductive Silicone Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Conductive Silicone Market Research

Mordor Intelligence provides a comprehensive analysis of the conductive silicone industry. We leverage our extensive expertise in electronic materials research. Our latest report examines the evolving landscape of ECS applications. These include thermal interface materials, EMI shielding materials, and flexible electronics. The analysis covers various product segments. These range from conductive silicone rubber and conductive elastomer solutions to specialized conductive silicone adhesive and conductive silicone gasket applications.

Stakeholders across the conductive polymer value chain benefit from our detailed examination of market dynamics. The report is available in an easy-to-download PDF format. The analysis encompasses emerging trends in electrically conductive silicone technologies, conductive sealant innovations, and conductive polymer composite developments. Our research provides strategic insights into the conductive silicone elastomer sector and conductive encapsulant applications. It also covers the broader ECS industry, offering valuable data for decision-makers in the electronic materials market and flexible electronics market.