Compliance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

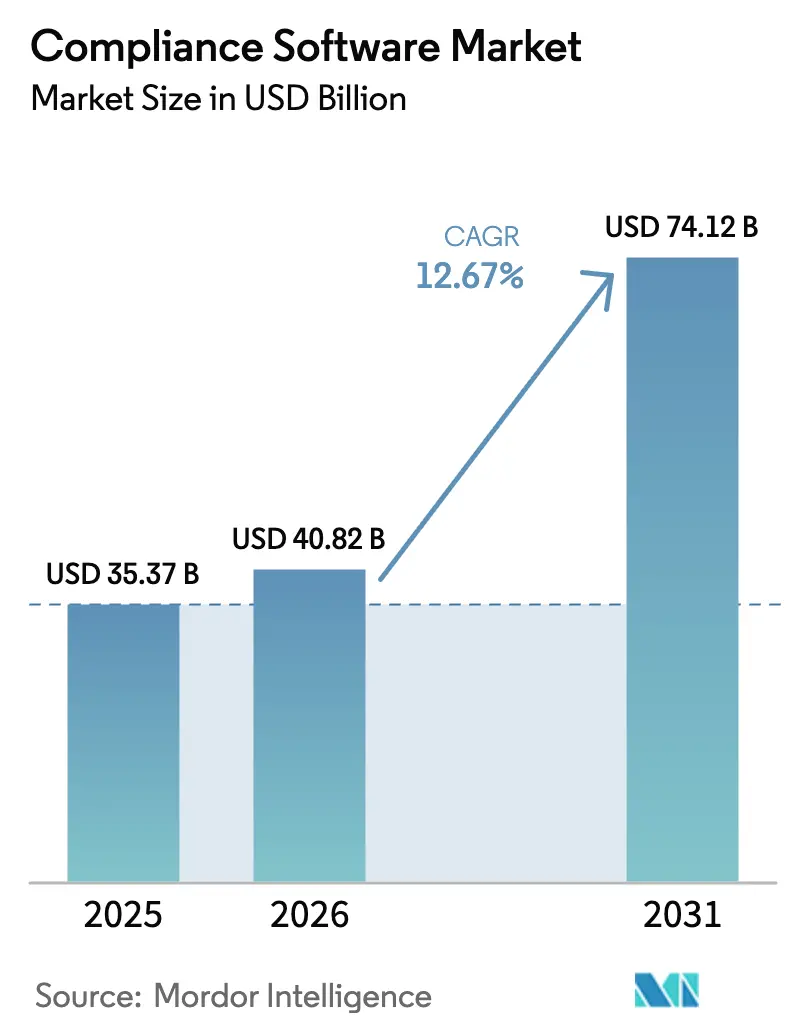

| Market Size (2026) | USD 40.82 Billion |

| Market Size (2031) | USD 74.12 Billion |

| Growth Rate (2026 - 2031) | 12.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compliance Software Market Analysis by Mordor Intelligence

The compliance software market size is expected to increase from USD 35.37 billion in 2025 to USD 40.82 billion in 2026 and reach USD 74.12 billion by 2031, growing at a CAGR of 12.67% over 2026-2031. This growth reflects a structural shift from episodic audits to continuous controls monitoring, spurred by global regulations that now penalize process gaps as stringently as outcome failures. Real-time incident-reporting mandates, soaring cyber penalties, and the convergence of environmental, social, and governance (ESG) disclosures with financial filings are intensifying the need for unified governance, risk, and compliance platforms. Cloud-native deployments dominate because sovereign-cloud regions meet data-residency requirements, while elastic compute reduces the cost of regulatory stress testing. Small and medium enterprises (SMEs) now adopt enterprise-grade suites as parity laws remove size-based exemptions, and artificial-intelligence (AI) engines that auto-generate audit trails reduce manual review hours, freeing scarce talent for higher-value analysis.

Key Report Takeaways

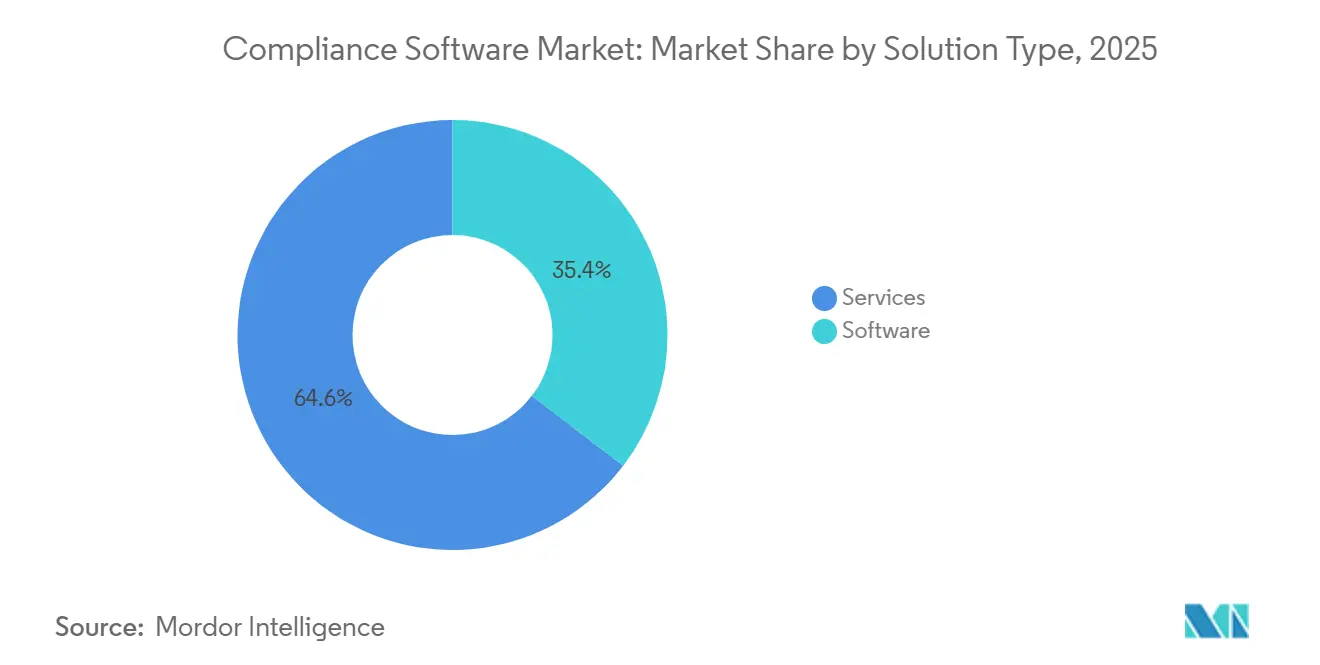

- By type, software accounted for 35.41% of revenue in 2025; services will lag as the software segment grows at a 12.91% CAGR through 2031.

- By deployment, cloud accounted for 69.23% of the compliance software market share in 2025 and is set to expand at a 13.19% CAGR through 2031.

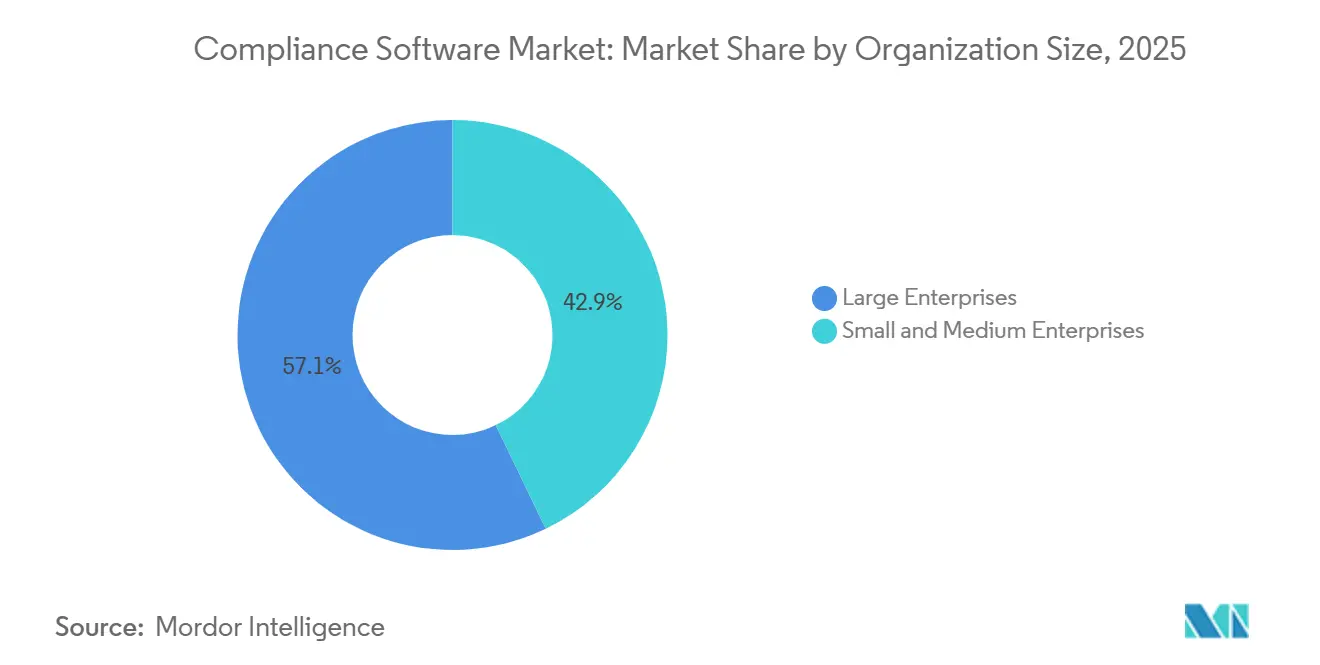

- By organization size, large enterprises accounted for 57.14% of the compliance software market share in 2025; small and medium enterprises are set to expand at a 12.96% CAGR through 2031.

- By end-user industry, healthcare is forecast to advance at a 14.12% CAGR through 2031, while banking, financial services, and insurance retained the highest 23.89% revenue share in 2025.

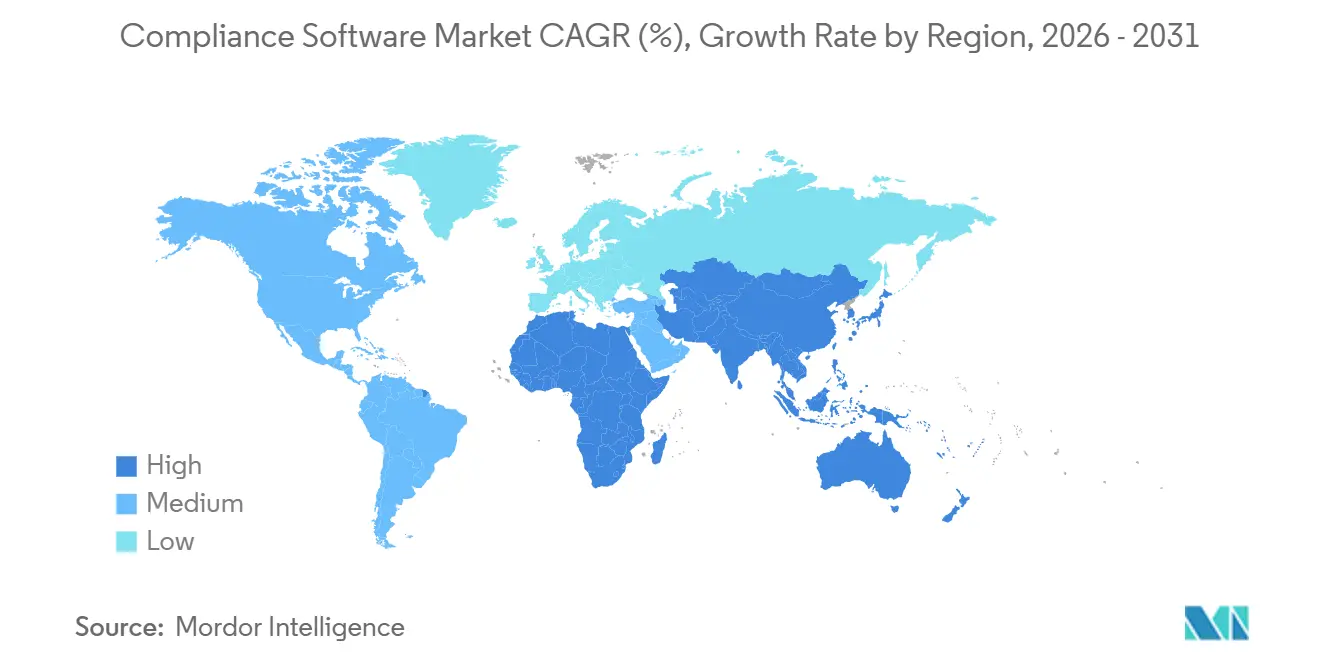

- By geography, North America accounted for 38.62% of revenue in 2025; Asia Pacific is set to expand at a 13.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compliance Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Regulatory Complexity Across Sectors | +2.8% | Global, with acute intensity in EU and North America | Medium term (2-4 years) |

| Rising Cyber-Regulatory Enforcement on Data Breaches | +2.3% | Global, led by North America, EU, and Asia-Pacific | Short term (≤ 2 years) |

| Growing Adoption of Cloud-Native Compliance Suites | +2.1% | North America and Europe core, rapid uptake in Asia-Pacific | Medium term (2-4 years) |

| Integration of AI-Driven Continuous Controls Monitoring | +1.9% | North America and EU early adopters, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Convergence of ESG and Financial Compliance Reporting | +1.6% | EU leadership, North America following, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Sector-Specific Mandates in Crypto and Digital Assets | +1.4% | EU (MiCA), Asia-Pacific (Singapore, Hong Kong), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Regulatory Complexity Across Sectors

Global regulators issued a record volume of new rules in 2024-2025, forcing enterprises to manage overlapping mandates through software that maps single controls to multiple citations. Revised HIPAA security amendments added mandates for multi-factor authentication and encryption, rendering legacy access-management tools obsolete.[1]U.S. Department of Health and Human Services, “HIPAA Security Rule Amendments,” HHS.GOV Financial institutions now juggle Pillar 3 credit-risk disclosures alongside climate-risk frameworks, a challenge impractical to solve with spreadsheets. Sector-specific regimes, such as export-control rules that now apply to software-as-a-service platforms, require audit trails that trace every data query to an authorized user. These compounded obligations accelerate the adoption of platforms that centralize policy libraries, automate evidence collection, and offer cross-regulation control mapping.

Rising Cyber-Regulatory Enforcement on Data Breaches

Penalties for cybersecurity lapses escalated sharply; European Union privacy fines reached EUR 2.1 billion (USD 2.24 billion) in 2024, a 34% jump over 2023.[2]European Data Protection Board, “GDPR Enforcement Statistics,” EDPB.EUROPA.EU The U.S. Federal Trade Commission sanctioned a healthcare provider with USD 4.75 million in March 2025 for slow patch remediation. States such as Colorado shortened breach-notification windows to 10 days, pressuring firms to implement real-time alerting. Compliance suites integrate vulnerability scanners and security information and event management feeds to automatically update risk registers, enabling organizations to meet rapid disclosure timelines while reducing false-positive alerts.

Growing Adoption of Cloud-Native Compliance Suites

Cloud captured the majority of the compliance software market revenue because regulators now accept shared-responsibility security models. Singapore’s monetary authority allowed banks to host customer data in public clouds, provided encryption keys remain institution-controlled.[3]Monetary Authority of Singapore, “Technology Risk Management Guidelines,” MAS.GOV.SG U.S. pipeline security directives drove critical infrastructure operators toward hybrid architectures that balance on-premises control with elastic analytics capacity. Multi-tenant platforms push regulatory updates to all customers simultaneously, and confidential-computing hardware mitigates concerns about provider access to sensitive data. Together, these advances lower deployment friction and total cost of ownership.

Integration of AI-Driven Continuous Controls Monitoring

Regulators released guidance that permits supervised entities to rely on machine-learning outputs for transaction monitoring, provided model risk governance is documented. Thomson Reuters cut false positives by 41% in pilot sanctions-screening projects, proving AI’s efficiency gains. Platforms now analyze incident tickets, change-management logs, and access-provisioning records to surface control gaps in real time, shifting assurance from quarterly tests to continuous oversight. Generative AI drafts policy updates and regulatory summaries, though adoption remains cautious due to hallucination risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Legacy-Heavy Firms | -1.7% | Global, acute in North America and Europe with aging infrastructure | Medium term (2-4 years) |

| Fragmented Global Regulatory Taxonomies | -1.3% | Global, particularly challenging for multinationals operating across EU, Asia-Pacific, and North America | Long term (≥ 4 years) |

| Scarcity of Domain-Skilled Compliance Talent | -1.1% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| Vendor Lock-In Risks With Proprietary Platforms | -0.9% | Global, affecting enterprises with complex multi-vendor ecosystems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Legacy-Heavy Firms

Enterprises running decades-old enterprise resource planning systems face integration costs that often eclipse compliance software license fees. Deloitte’s 2024 survey noted that 58% of financial institutions anticipate 18-24 months and consulting outlays up to USD 8 million to replace legacy governance, risk, and compliance stacks. Mainframes, common in insurance, require custom middleware, doubling support costs during transition. SMEs lacking in-house expertise must purchase managed services bundled with software subscriptions, thereby increasing ownership costs by as much as 60% compared with large enterprises. These expenses can delay modernization despite clear operational benefits.

Fragmented Global Regulatory Taxonomies

Multinationals juggle more than 180 data-protection regimes with divergent consent definitions, cross-border transfer rules, and enforcement philosophies. China blocks data exports absent security assessments, while Australia allows transfers to jurisdictions with similar protections. The European Union emphasizes process documentation, whereas the United States focuses on outcome-based liability, forcing compliance teams to design region-specific workflows. Vendors must embed jurisdictional logic that scales with every new country, inflating configuration complexity and prolonging implementation timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Software Dominance Anchored by Regulatory Automation

Software accounted for 35.41% of the compliance software market share in 2025 and will outpace services at a 12.91% CAGR through 2031. The compliance software market, excluding software alone, is expected to grow markedly as firms replace external consultants with configurable platforms that automate policy mapping and evidence capture. Data-privacy modules surged post-Digital Services Act, which imposes fines up to 6% of global revenue for non-compliance. Audit-management tools now support continuous assurance, in line with the Institute of Internal Auditors’ updated standards. Environmental, health, and safety (EHS) suites gained traction after OSHA’s new electronic recordkeeping rule, effective January 2025.

Services still play a role in complex projects that require legacy integration and regulatory change advisory. Professional services remain indispensable in aerospace and defense deployments that must interpret export-control classifications. Managed-service bundles appeal to SMEs by offering subscription pricing that combines licenses with monitoring. However, vendors emphasize recurring software revenue, demonstrated by SAP’s 29% jump in cloud-compliance subscriptions during fiscal 2024, while consulting declined.

By Deployment: Cloud Ascendancy Fueled by Regulatory Acceptance

Cloud held 69.23% market share in 2025 and is set to expand at a 13.19% CAGR to 2031. Cloud’s share of the compliance software market reflects regulators’ embrace of shared-responsibility security models and the proliferation of sovereign cloud regions. The U.S. FedRAMP program authorized more than 300 cloud offerings by the end of 2024. Hybrid architectures persist for latency-sensitive workloads, while confidential computing mitigates privacy concerns by encrypting data in use with hardware-based mechanisms.

On-premises deployments are shrinking but remain mandatory for critical-infrastructure operators subject to air-gapped network rules. Banks in India adopt hybrid models, supported by guidelines that require repatriation capability within 48 hours if regulations shift. Unified management consoles now synchronize policy rules across environments, reducing configuration drift and presenting a single compliance posture to auditors.

By Organization Size: SME Acceleration Driven by Regulatory Parity

Large enterprises accounted for 57.14% of revenue in 2025, yet SMEs are projected to post the fastest 12.96% CAGR. Once exempt from stringent oversight, SMEs now face identical obligations under parity laws such as the European Union’s Digital Operational Resilience Act. Subscription-based delivery lowers capital outlays, and pre-configured templates shorten deployment to weeks. The compliance software market segment for SMEs is further buoyed by grants from regulators such as Singapore’s Financial Sector Technology and Innovation scheme.

Large enterprises demand deep integrations with enterprise resource planning and human capital management systems to automate control evidence. Role-based access controls and multi-language interfaces facilitate collaboration across subsidiaries. While dedicated compliance teams harness advanced analytics, small and medium enterprises (SMEs) increasingly depend on vendor-managed services for real-time updates.

By End-User Industry: Healthcare Leads Growth Amid Clinical and Privacy Mandates

Banking, financial services, and insurance (BFSI) remained the largest adopter, accounting for 23.89% of revenue in 2025, driven by stringent supervisory oversight. Healthcare is forecast to be the fastest-growing vertical, with a 14.12% CAGR to 2031. The compliance software market size allocated to healthcare expands as clinical-trial diversity rules and genetic-privacy statutes multiply documentation burdens. Hospitals require automated consent management and audit trails that align with state DNA privacy acts.

Information-technology and telecommunications firms confront data-localization laws, such as Vietnam’s cybersecurity statute. Aerospace and defense contractors need attribute-based access controls to comply with export-control restrictions, while energy operators leverage EHS modules for greenhouse gas reporting under the U.S. Environmental Protection Agency’s program and the EU Emissions Trading System. Retail platforms integrate payment card compliance and subscription marketing rules into unified suites, reflecting the widening scope of regulated digital commerce.

Geography Analysis

North America accounted for 38.62% of global revenue in 2025, driven by early adoption of AI-driven anomaly detection and overlapping mandates from agencies such as the Securities and Exchange Commission and the Federal Trade Commission. U.S. banks reported 35-50% reductions in false positives after deploying natural-language processing to screen transaction narratives, showcased at the American Bankers Association’s 2024 risk conference. Canada amended PIPEDA in 2024 to include biometric data in its definitions of sensitive information, compelling upgrades to discovery tools. Mexico’s fintech law brought digital-lending platforms under prudential supervision, expanding the addressable market for vendors.

Europe held a roughly 28% share, with the Digital Operational Resilience Act fully enforceable from January 2025. Germany mandated board-level accountability for operational resilience, while the United Kingdom’s consumer-duty rules require proof of good customer outcomes. Russia’s 2024 data-localization expansion entrenched demand for hybrid deployment. Together, these frameworks solidify Europe's position as a stronghold in the compliance software market.

Asia-Pacific is projected to register a 13.63% CAGR to 2031, the fastest among regions. China’s Personal Information Protection Law entered active enforcement, with fines of up to CNY 50 million (USD 7 million) for non-compliance. India’s Digital Personal Data Protection Act enforces 30-day deletion rights, and Japan’s revised Act on the Protection of Personal Information imposes 72-hour breach reporting, aligning with EU norms. Australia’s impending privacy-act reforms will introduce a statutory tort for serious invasions of privacy. These policies spur enterprises to invest in localized modules that address extraterritorial reach.

The Middle East and Africa and South America remain nascent but are maturing rapidly. The United Arab Emirates enacted a comprehensive data-protection law in 2024, and Saudi Arabia issued cloud-computing controls aligned with international standards. Brazil’s national data-protection authority began levying meaningful penalties and published AI governance guidance in 2024, signaling a more assertive enforcement stance.

Competitive Landscape

The compliance software market is moderately fragmented; the top five vendors accounted for roughly 28% of combined revenue in 2025. Enterprise-software incumbents leverage existing customer bases to cross-sell compliance add-ons, such as SAP embedding governance modules into S/4HANA and IBM expanding OpenPages capabilities. Pure-play specialists differentiate through regulatory-content depth, with Thomson Reuters curating over 1.2 million obligations across 750 jurisdictions. Emerging vendors emphasize no-code configuration, reducing implementation from months to weeks for mid-size firms.

AI and machine-learning capabilities are the primary battleground. OneTrust filed a 2024 patent for generative AI that auto-produces data-protection impact assessments. NAVEX expanded its compliance-training offerings to 1,800 courses through acquisitions, enabling cross-selling to its governance platform. Vendors that lock data into proprietary models face pushback from buyers demanding interoperability and exportability guarantees. The Open Compliance and Ethics Group’s common data model is gaining traction as a neutral exchange format among forward-looking enterprises.

Vertical-niche opportunities persist. Crypto-asset compliance modules emerged after the Markets in Crypto-Assets Regulation took effect. Agriculture and gig-economy platforms are largely underserved but face rising regulatory scrutiny on environmental limits and worker protection, respectively. Strategic moves such as IBM’s USD 47 million U.S. federal contract and SAP’s AI-powered audit-response launch illustrate how leading providers secure anchor customers and embed advanced analytics at scale.

Compliance Software Industry Leaders

Fenergo Group Limited

ACTICO GmbH

ComplyAdvantage Ltd.

RegEd, Inc.

VComply Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Thomson Reuters Corporation announced the acquisition of a European regulatory-intelligence startup for EUR 180 million (USD 192 million), expanding ESG coverage and natural-language processing capability.

- November 2025: SAP SE launched an enhanced Cloud Compliance solution featuring AI that auto-generates audit responses for clients preparing for 2026 stress tests.

- October 2025: Workiva Inc. partnered with a major accounting firm to co-develop integrated assurance workflows linking financial audits with sustainability reviews.

- October 2025: International Business Machines Corporation won a USD 47 million U.S. federal contract to deploy OpenPages across 23 departments.

Global Compliance Software Market Report Scope

The Compliance Software Market Report is Segmented by Type (Software, and Services), Deployment (Cloud, On-Premises, Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Banking, Financial Services, and Insurance (BFSI), IT and Telecommunications, Healthcare, Aerospace and Defense, Energy and Utilities, Manufacturing, Retail and E-commerce, Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Software | Regulatory Compliance Management Software |

| Risk Management Software | |

| Audit Management Software | |

| Data Privacy Compliance Software | |

| Environmental, Health and Safety Compliance Software | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking, Financial Services, and Insurance (BFSI) |

| IT and Telecommunications |

| Healthcare |

| Aerospace and Defense |

| Energy and Utilities |

| Manufacturing |

| Retail and E-commerce |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Solution Type | Software | Regulatory Compliance Management Software | |

| Risk Management Software | |||

| Audit Management Software | |||

| Data Privacy Compliance Software | |||

| Environmental, Health and Safety Compliance Software | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) | ||

| IT and Telecommunications | |||

| Healthcare | |||

| Aerospace and Defense | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the compliance software market in 2031?

The market is forecast to reach USD 74.12 billion by 2031, growing at a 12.67% CAGR.

Which deployment model leads adoption?

Cloud deployments dominated with 69.23% revenue share in 2025 and are expanding at a 13.19% CAGR.

Why are SMEs adopting compliance platforms rapidly?

Regulatory parity laws now impose the same obligations on smaller firms, and subscription pricing with pre-configured templates lowers the entry barrier.

Which end-user industry is expected to grow fastest through 2031?

Healthcare is projected to register the highest 14.12% CAGR due to clinical-trial transparency and genetic-privacy mandates.

How are AI capabilities changing compliance workflows?

AI engines reduce false positives in sanctions screening, generate policy drafts, and enable continuous controls monitoring, cutting manual review hours significantly.

Page last updated on: