Companion Animal Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 5.40 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Companion Animal Vaccine Market Analysis by Mordor Intelligence

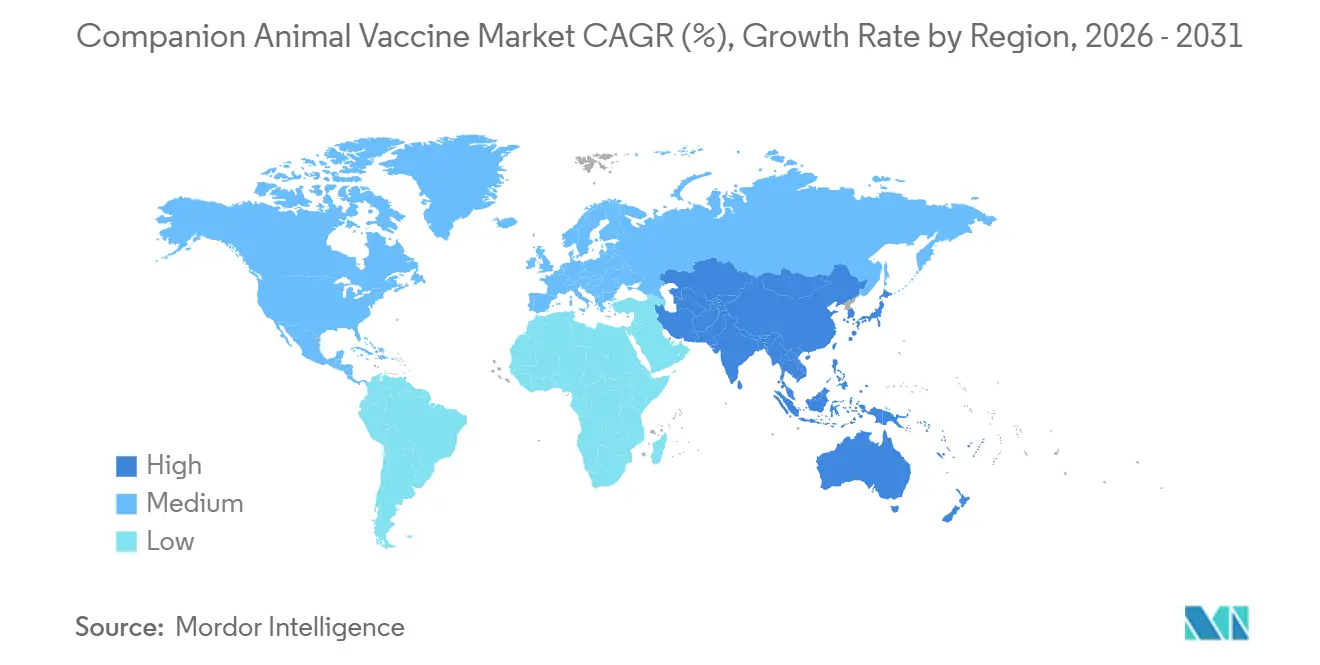

The companion animal vaccine market size is estimated to reach USD 4.03 billion in 2026, and is projected to climb to USD 5.40 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). Momentum stems from pet humanization, public health mandates that view canine rabies vaccination as essential, and steady improvements in vaccine technology, especially recombinant platforms. Core demand also benefits from the WHO Zero by 30 program, which has prompted more than 50 endemic countries to implement 70% canine vaccination coverage starting in 2024. In 2025, North America led with a 41.45% slice of global sales, while Asia-Pacific is on track for a 7.43% CAGR through 2031, due to rising dog and cat ownership in China and India. U.S. import rules finalized in August 2024 require proof of rabies immunization, microchipping, and serology for all dogs arriving from high-risk nations, effectively expanding pre-travel vaccination demand at the border.

Key Report Takeaways

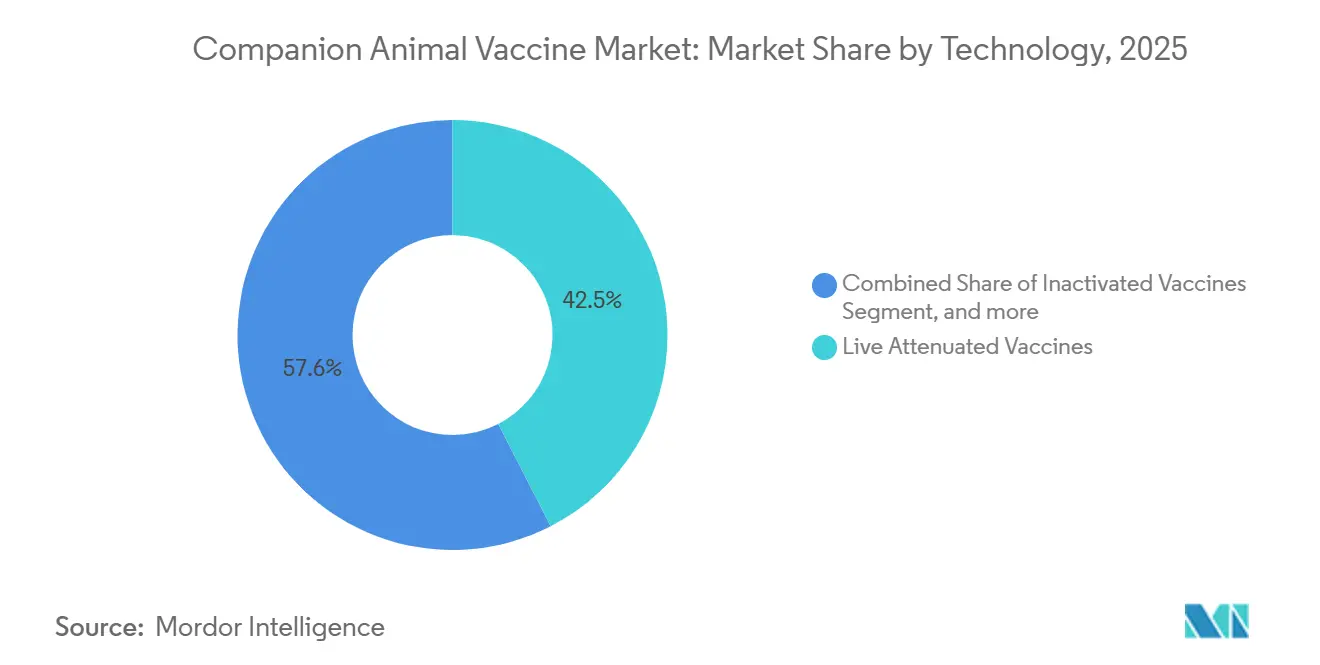

- By 2025, live attenuated products will lead the companion animal vaccines market with a 42.45% share, while recombinant vaccines are poised to post an 8.43% CAGR through 2031.

- By animal type, dogs accounted for 62.56% of the 2025 revenue, but the cat segment is forecasted to grow at an 8.65% CAGR through 2031.

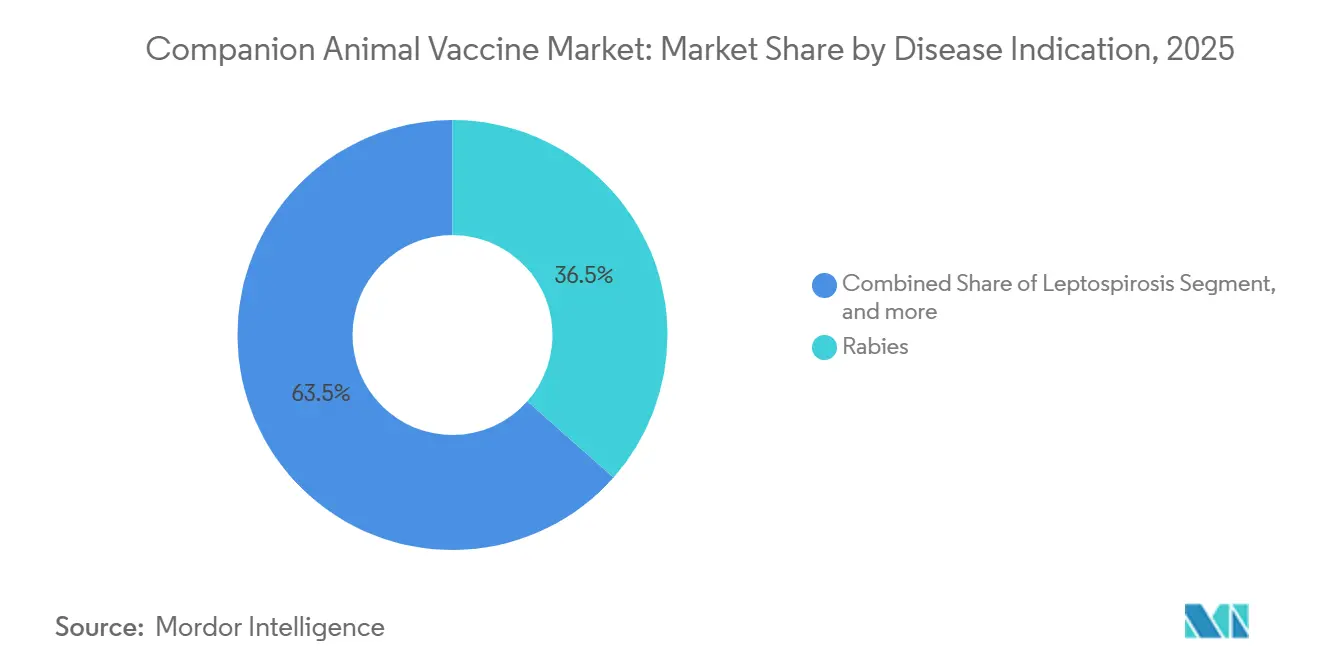

- By disease indication, rabies accounted for 36.54% of the global revenue in 2025; Lyme disease vaccines are expected to expand at a 9.32% CAGR during the same period.

- By end user, veterinary hospitals and clinics captured 55.43% of 2025 sales, yet e-commerce channels are projected to grow at a 9.65% CAGR through 2031.

- By geography, North America led with a 41.45% slice of global sales, while Asia-Pacific is on track for a 7.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Companion Animal Vaccine Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Companion Animals Globally | +1.2% | China, India, urban Latin America, United States, Canada | Medium term (2-4 years) |

| Increasing Incidence of Zoonotic Diseases and Public Health Campaigns | +1.0% | Sub-Saharan Africa, South Asia, Southeast Asia, United States | Short term (≤ 2 years) |

| Advancements in Vaccine Biotechnology Such as Recombinant Platforms | +0.9% | North America, Europe, Asia-Pacific premium segments | Long term (≥ 4 years) |

| Government Rabies Elimination Initiatives Mandating Canine Vaccination | +0.8% | Asia-Pacific, Middle East & Africa, Latin America | Short term (≤ 2 years) |

| Shelter Intake Protocols Requiring Rapid-Onset Vaccines | +0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Pet Insurance Expansion Covering Preventive Vaccination Costs | +0.7% | United States, Canada, Australia, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Companion Animals Globally

China counted 187 million dogs and cats in 2024, and India’s dog population climbed from 19.4 million in 2018 to 31 million by 2023, creating a durable base for routine immunization. Similar gains appeared in the United States, where the American Veterinary Medical Association (AVMA) recorded 89.7 million dogs and 73.8 million cats in households during 2024[1]American Veterinary Medical Association, “U.S. Pet Ownership Statistics 2024,” avma.org. Shelter adoptions advanced 12% year-over-year, and updated intake guidelines require vaccination within 48 hours, which boosts immediate demand for rapid-onset formulations. Urbanization elevates disposable income, allowing owners to treat pets as family and prioritize preventive care, including combination boosters. Manufacturers have responded with single-dose, high-titer vials that appeal to first-time owners seeking convenience.

Increasing Incidence of Zoonotic Diseases and Public Health Campaigns

Roughly 60% of emerging human pathogens are zoonotic, a statistic that underpins the CDC-WHO One Health framework. Rabies caused an estimated 59,000 human deaths in 2024, with dogs responsible for 99% of transmission, propelling the WHO Zero by 30 campaign. In the United States leptospirosis cases in dogs rose 18% between 2020 and 2024, prompting veterinary associations to reclassify the vaccine from optional to recommended in 32 states. New CDC import standards introduced in 2024 mandate rabies vaccination for dogs entering from high-risk countries, ensuring cross-border compliance. Meanwhile, India, the Philippines, and Kenya collectively allocated USD 120 million in 2024 for mass canine vaccination to curb human rabies exposure.

Advancements in Vaccine Biotechnology Such as Recombinant Platforms

Recombinant constructs eliminate the risk of reversion to virulence and simplify cold-chain logistics, enabling a wider geographic reach. Australia’s Office of the Gene Technology Regulator approved Nobivac Puppy DP Plus in 2024, marking the first genetically modified canine parvovirus vaccine[2]Office of the Gene Technology Regulator, “Decision Record: Nobivac Puppy DP Plus,” ogtr.gov.au. Oncept, a recombinant therapeutic for canine melanoma, has surpassed 50,000 administered doses since its approval by the USDA in 2010, underscoring the safety profile of subunit platforms. Peer-reviewed studies released in 2025 demonstrated that experimental mRNA rabies candidates delivered neutralizing titers equivalent to those of inactivated vaccines while remaining stable at 25 °C for 14 days, a breakthrough for resource-limited settings. Subunit manufacturing removes whole-pathogen culture, lowering production costs by up to 30% and shortening scale-up timelines during outbreaks.

Government Rabies Elimination Initiatives Mandating Canine Vaccination

Fifty countries updated legislation in 2024-2025 to require 70% canine vaccination, aligning with WHO targets. India earmarked INR 5 billion (approximately USD 60 million) in 2024 for urban dog campaigns, covering 30 million animals. Kenya partnered with the Global Alliance for Rabies Control to vaccinate 2 million dogs, resulting in a 40% year-over-year reduction in human rabies cases. The Philippines registered Rabisin and Felocell-4 in 2024, widening product access for municipal drives. Such multi-year tenders give manufacturers demand visibility and justify capacity expansion.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Vaccine Development and Regulatory Approvals | -0.6% | North America, Europe, global biotech start-ups | Long term (≥ 4 years) |

| Cold-Chain and Distribution Challenges in Emerging Economies | -0.4% | Rural Asia-Pacific, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Vaccine Hesitancy Among Some Owners Over Safety Concerns | -0.3% | United States, Canada, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Consolidation of Veterinary Clinics Pressuring Pricing | -0.3% | United States, Canada, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Vaccine Development and Regulatory Approvals

Bringing a new veterinary vaccine from discovery to USDA or FDA-CVM approval can require 5-7 years and USD 10-50 million, levels that deter smaller entrants[3]USDA Center for Veterinary Biologics, “Licensing Overview,” aphis.usda.gov. Mandatory efficacy studies in target species, pediatric safety assessments, and multi-temperature stability trials extend timelines compared with some human emergency pathways. Recombinant and mRNA constructs face extra scrutiny under GMO rules; Australia’s three-year Nobivac Puppy DP Plus review included environmental assessments and public comments before clearance in 2024. Patent cliffs loom for blockbuster portfolios, such as those of Vanguard and Nobivac, yet generics remain scarce because replicating live attenuated master seeds under current Good Manufacturing Practice (cGMP) conditions is technically demanding.

Cold-Chain and Distribution Challenges in Emerging Economies

Live attenuated and mRNA products must remain between 2 °C and 8 °C from plant to patient, a condition often unmet in rural areas where electricity is intermittent. WHO audits in India, Kenya, and the Philippines recorded temperature excursions in up to 40% of sampled shipments during 2024. Thermostable options are advancing; HIPRA’s ambient-stable rabies vaccine retained potency for 30 days and won Philippine approval in June 2024. Even so, lyophilized vials require reconstitution, which introduces handling errors and extra time in high-volume shelter clinics.

Segment Analysis

By Technology: Recombinant Platforms Gain Share Despite Live Attenuated Dominance

Live attenuated products held a 42.45% market share in the companion animal vaccines market in 2025, securing their role as cost-efficient options for core diseases such as distemper and parvovirus. The recombinant segment is projected to grow at an 8.43% CAGR from 2026 to 2031, driven by its safety edge, improved stability, and the newly validated regulatory path, as demonstrated by Australia’s 2024 approval of Nobivac Puppy DP Plus. Inactivated platforms remain important for rabies and leptospirosis, but face price pressure as recombinant titers reach parity. Toxoid, viral vector, and virus-like particle technologies collectively represented roughly 8% of sales in 2025, while DNA and mRNA candidates are still in pre-commercial phases, despite showing encouraging antibody profiles in 2025 peer-reviewed trials.

Future growth will hinge on lowering production costs and simplifying cold-chain logistics. Recombinant subunits can be produced in lower-biosafety fermenters, reducing capital expenditures, and single-dose packaging streamlines clinic workflow. Manufacturers are also exploring needle-free injectors and intranasal formats to minimize stress on animals and owners, factors that could further lift adoption. As patent protection wanes for legacy attenuated brands, recombinant developers expect more expansive room for price-mix gains and faster uptake of novel constructs within the companion animal vaccines market.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Feline Segment Accelerates as Urban Ownership Rises

Dogs generated 62.56% of 2025 revenue, mainly due to higher disease-coverage breadth and stricter rabies mandates. Nevertheless, the cat segment is forecasted to grow at an 8.65% CAGR through 2031, mirroring the shift toward apartment living and the widespread implementation of FVRCP protocols that require vaccination within two days of admission. Feline uptake also benefits from convenient combination vials that reduce the need for multiple clinic visits. Meanwhile, rabbits, birds, equines, and exotic pets together accounted for about 12% of spending in 2025, primarily tied to niche pathogens such as RHDV.

Guideline updates in 2024 reclassified FeLV from core to non-core for strictly indoor cats, temporarily reducing the vaccine’s unit volumes while freeing budgets for newer feline immunodeficiency and infectious peritonitis candidates. In canine medicine, Lyme and leptospirosis boosters are climbing as tick and rodent ranges expand. Continued urbanization in the Asia-Pacific region is expected to keep the cat portfolio growing faster than the dog segment, thereby reinforcing its role in the companion animal vaccines market.

By Disease Indication: Lyme Disease Vaccines Surge in Endemic Zones

Rabies dominated with a 36.54% share in 2025, sustained by government mandates and WHO funding streams. Lyme disease vaccines are on course for a 9.32% CAGR as Borrelia-infected tick populations spread beyond traditional hotspots, and AAHA guidelines reclassified the shot as recommended rather than optional in 15 U.S. states. The DAPP combination accounted for 22% of sales, while FVRCP controlled 14%, but lags because cat owners make fewer clinic visits.

Other indications, such as leptospirosis and Bordetella, track specific environmental and boarding-related risks. Notably, a 12% gain in leptospirosis vaccinations during 2024 followed a documented rise in U.S. canine cases. Emerging therapies for canine influenza and feline immunodeficiency remain small but could unlock new revenue streams once clinical data mature and labeling expands.

Note: Segment shares of all individual segments available upon report purchase

By End User: E-Commerce Disrupts Traditional Veterinary Distribution

Veterinary clinics commanded 55.43% of 2025 revenue and maintain clinical authority over initial puppy and kitten schedules. Yet online pharmacies and telehealth portals are projected to grow at a 9.65% CAGR to 2031, enabled by platforms such as Chewy Pharmacy and VetsterRx that link prescription issuance to home delivery. Brick-and-mortar retail accounted for 18% in 2025, pivoting toward weekend vaccination clinics staffed by contract veterinarians offering doses at prices 40% below hospital rates.

Shelters and rescues accounted for 12% of 2025 demand, supported by municipal budgets that secured bulk discounts. Corporate clinic consolidation, led by Mars Veterinary Health, National Veterinary Associates, and VCA, concentrates purchasing power, trimming per-dose prices and squeezing manufacturer margins. Direct-to-consumer subscription models are emerging, particularly in the United States, where preventive bundles cover annual boosters and heartworm pills, reinforcing recurring revenue in the companion animal vaccines market.

Geography Analysis

North America maintained a 41.45% share of global volume in 2025, driven by high ownership rates and CDC regulations that consider rabies vaccination a compulsory public health measure. Canada’s pet insurance coverage reached 4.5% in 2024, with 40% of policies covering preventive shots, a factor that translates into steadier order patterns. Corporate clinic chains dominate 25-30% of U.S. outlets, leveraging scale to pressure suppliers for rebates while still stocking premium recombinant brands.

Asia-Pacific is forecast for a 7.43% CAGR through 2031, buoyed by China’s 187 million pets and India’s aggressive rabies elimination budgets. Philippine approvals for Rabisin and Felocell-4 in 2024 broadened the catalogue for government procurement. Japan, South Korea, and Australia lead regional pet insurance uptake at 8-12%; these policies increasingly reimburse non-core vaccinations, nudging price mix higher.

Europe held roughly 28% of 2025 sales, aided by strict pet-travel rabies rules and EMA oversight that accelerates multi-antigen launches. The Middle East and Africa together captured 6%, with Kenya, Tanzania, and South Africa deploying USD 120 million in 2024 toward mass canine drives. South America represented 5%; Brazil and Argentina drive most volume, but face macroeconomic headwinds that slow the rollout of premium products. Cold-chain gaps persist in many rural areas, providing thermostable formulations with room to differentiate within the companion animal vaccines market.

Competitive Landscape

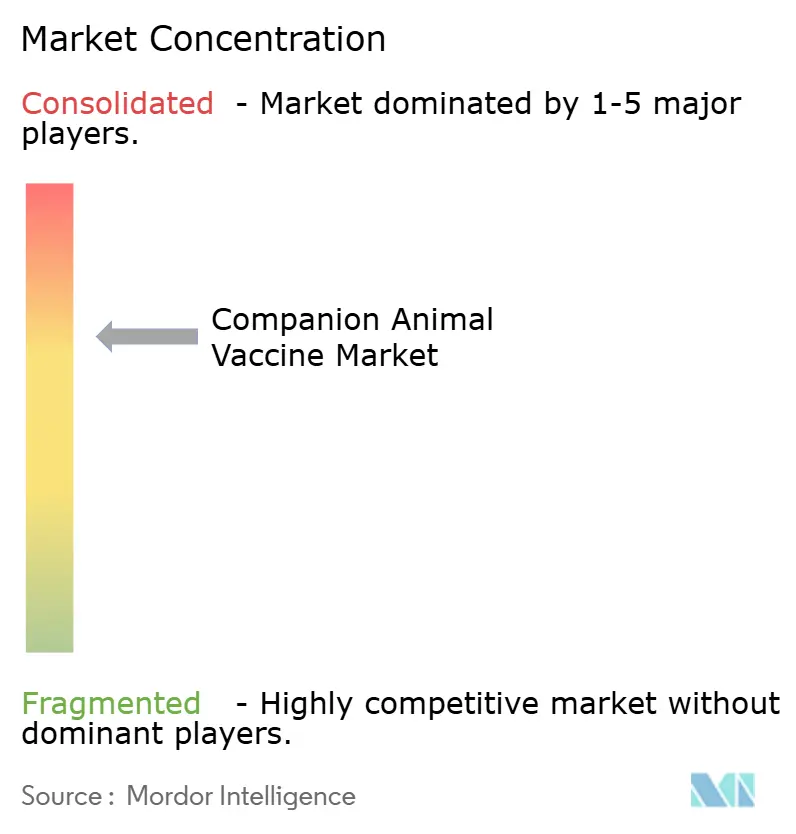

Market concentration is moderate. Zoetis, Boehringer Ingelheim, and Elanco collectively controlled about 60% of North American revenue in 2025; however, the Asian share is fragmenting as HIPRA, Indian Immunologicals, and Hester Biosciences win tenders with ambient-stable or lower-priced lines. Zoetis’s Vanguard and Boehringer’s Nobivac portfolios generated more than USD 1 billion in combined global sales during 2024, but looming patent expirations could shave 10-15% off margins by the late 2020s. Merck Animal Health and Virbac compete in niche areas such as feline leukemia and canine influenza, relying on regulatory first-mover status to defend price premiums.

Corporate clinic consolidation intensifies price negotiations, while e-commerce disruptors shrink in-clinic booster revenue. In October 2024, Zoetis earmarked USD 150 million to expand Kalamazoo capacity for recombinant and mRNA platforms, signaling an expectation that next-gen constructs will command a higher share by mid-decade.

Small biotech firms, such as Brilliant Bio Pharma, focus on mRNA candidates for canine influenza and FIV; however, capital constraints and lengthy approval timelines remain significant hurdles. Overall, supplier strategies focus on cold-chain innovation, combination dosing, and subscription partnerships that secure recurring revenue in the companion animal vaccines market.

Companion Animal Vaccine Industry Leaders

Elanco Animal Health Incorporated

Boehringer Ingelheim GmbH

Merck & Co. Inc.

Zoetis Inc.

Bioveta AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Zoetis launch of Vanguard Recombishield, a new injectable vaccine for Bordetella bronchiseptica, also known as kennel cough in the United States. Licensed by USDA on March 4, 2025, it is the first dog vaccine with pertactin protein for enhanced immunity. The vaccine uses recombinant technology to offer a more comfortable and minimally painful immunization experience for pets.

- August 2025: RUMA CA&E launched a new vaccine supply survey for companion animals and horses. This survey follows a previous questionnaire focused on livestock and agriculture. The initiative aims to assess vaccine availability and supply chain issues across different sectors.

- February 2025: Merck Animal Health announced that S&P Global Animal Health awarded the injectable BRAVECTO (fluralaner) the 2024 Best New Companion Animal Product. This formulation provides year-long protection against fleas and ticks with a single dose, lasting longer than any other parasiticide. It is approved in over 30 countries, but not yet in the United States.

Global Companion Animal Vaccine Market Report Scope

As per the report's scope of the report, companion animal vaccines are used to prevent infectious diseases caused by various disease-causing agents and protect animals from various life-threatening disorders.

The Companion Animal Vaccines Market Report is Segmented by Technology (Live Attenuated, Inactivated, Toxoid, Recombinant, DNA & mRNA, and Other Technologies), Animal Type (Dogs, Cats, and Other Companion Animals), Disease Indication (Rabies, DAPP, FVRCP, Leptospirosis, Lyme Disease, Bordetella & Canine Parainfluenza, and Other Disease Indications), End-User (Veterinary Hospitals & Clinics, Retail Pharmacies & Pet Stores, E-Commerce & Online Pharmacies, and Animal Shelters & Rescue Organizations), and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Live Attenuated Vaccines |

| Inactivated Vaccines |

| Toxoid Vaccines |

| Recombinant Vaccines |

| DNA & mRNA Vaccines |

| Other Technologies |

| Dogs |

| Cats |

| Other Companion Animals (Rabbits, Avian, Equine, Exotic) |

| Rabies |

| Canine Distemper / Adenovirus / Parvovirus (DAPP) |

| Feline Panleukopenia / Herpes / Calicivirus (FVRCP) |

| Leptospirosis |

| Lyme Disease |

| Bordetella & Canine Parainfluenza |

| Other Disease Indications |

| Veterinary Hospitals & Clinics |

| Retail Pharmacies & Pet Stores |

| E-Commerce & Online Pharmacies |

| Animal Shelters & Rescue Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Technology | Live Attenuated Vaccines | |

| Inactivated Vaccines | ||

| Toxoid Vaccines | ||

| Recombinant Vaccines | ||

| DNA & mRNA Vaccines | ||

| Other Technologies | ||

| By Animal Type | Dogs | |

| Cats | ||

| Other Companion Animals (Rabbits, Avian, Equine, Exotic) | ||

| By Disease Indication | Rabies | |

| Canine Distemper / Adenovirus / Parvovirus (DAPP) | ||

| Feline Panleukopenia / Herpes / Calicivirus (FVRCP) | ||

| Leptospirosis | ||

| Lyme Disease | ||

| Bordetella & Canine Parainfluenza | ||

| Other Disease Indications | ||

| By End-User | Veterinary Hospitals & Clinics | |

| Retail Pharmacies & Pet Stores | ||

| E-Commerce & Online Pharmacies | ||

| Animal Shelters & Rescue Organizations | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected value of the companion animal vaccines market in 2031?

Forecasts show the market reaching USD 5.40 billion by 2031, underpinned by a 6.02% CAGR driven by public-health mandates and technology upgrades.

Which technology segment is growing fastest?

Recombinant vaccines are expected to post an 8.43% CAGR to 2031, outpacing live attenuated and inactivated formats as safety and cold-chain benefits gain recognition.

Why are Lyme disease vaccines receiving more attention in the United States?

Tick expansion into 15 states led AAHA to reclassify Lyme vaccination as recommended, pushing the indication toward a 9.32% CAGR through 2031.

How will e-commerce impact vaccine distribution?

Online pharmacies and telehealth portals are set for a 9.65% CAGR, offering subscription models that shift booster sales away from traditional clinics.

What challenges limit vaccine rollout in emerging markets?

Cold-chain gaps, high regulatory costs, and limited veterinary infrastructure hinder coverage, although thermostable formulations aim to reduce these barriers.

Which companies dominate the competitive landscape?

Zoetis, Boehringer Ingelheim, and Elanco collectively hold about 60% of North American revenue, yet regional players such as HIPRA and Indian Immunologicals are gaining ground in Asia-Pacific.