Companion Animal Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

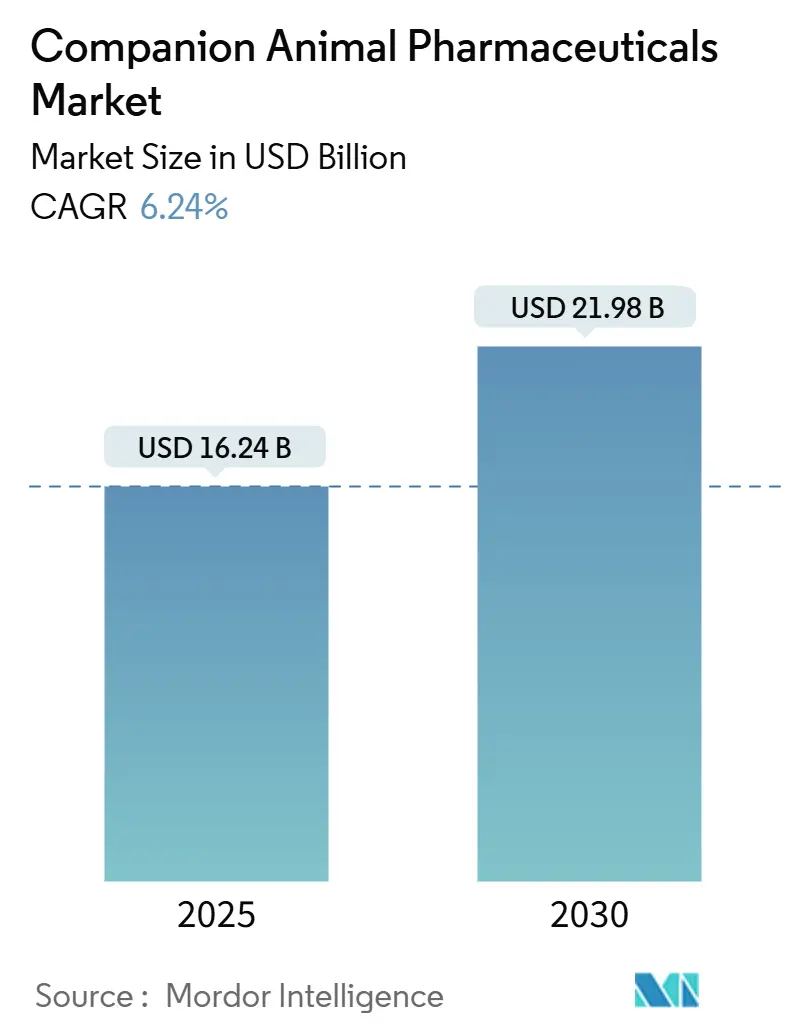

| Market Size (2025) | USD 16.24 Billion |

| Market Size (2030) | USD 21.98 Billion |

| Growth Rate (2025 - 2030) | 6.24% CAGR |

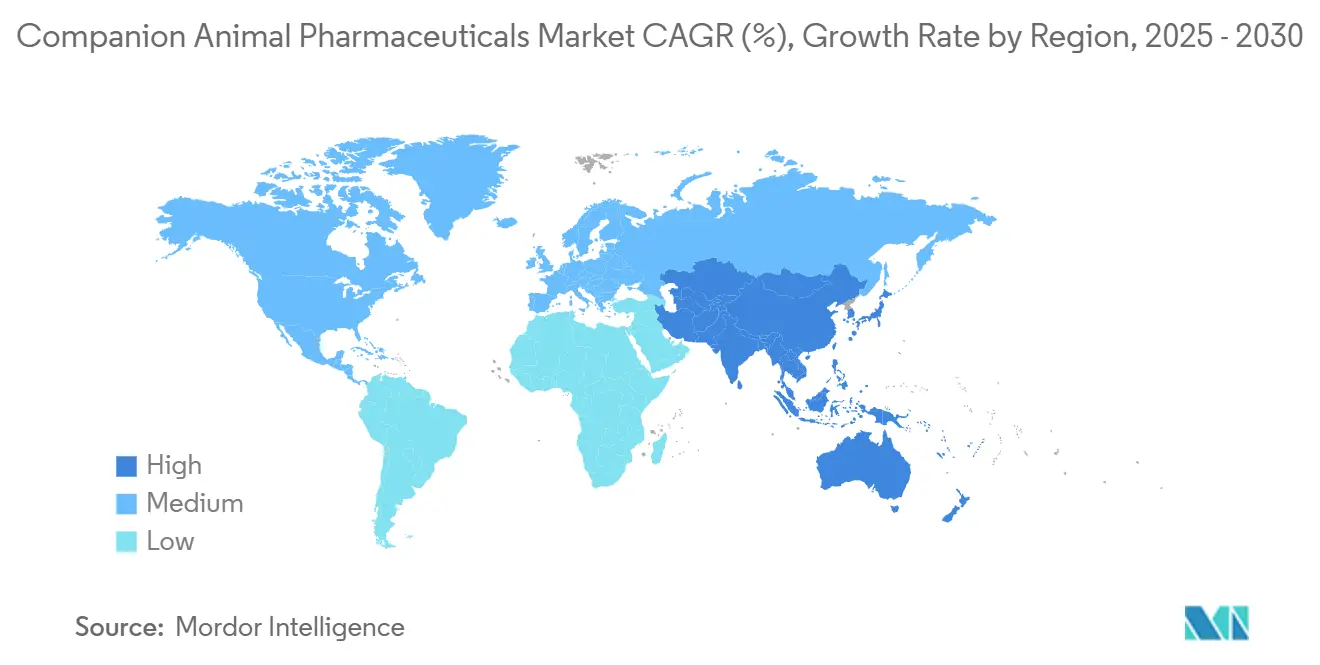

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Companion Animal Pharmaceuticals Market Analysis by Mordor Intelligence

The companion animal pharmaceuticals market size stood at USD 16.24 billion in 2025 and is forecast to reach USD 21.98 billion by 2030, reflecting a 6.24% CAGR over the period. Growth is catalyzed by a surge in human-grade therapies for pets, wider pet insurance coverage, and expanding regulatory pathways that accelerate drug approvals. The market benefits from rising disposable incomes, deeper human–animal bonds, and steady innovation pipelines that bring monoclonal antibodies, JAK inhibitors, and long-acting injectables into routine veterinary use[1]U.S. Food and Drug Administration, “CVM new animal drug approvals,” fda.gov. Competitive dynamics favor firms that pair therapeutics with diagnostics and digital tools, giving practitioners integrated care platforms. Meanwhile, online pharmacies, corporate clinics, and telehealth services open fresh access points, creating omnichannel ecosystems that reinforce prescription adherence and price transparency.

Key Report Takeaways

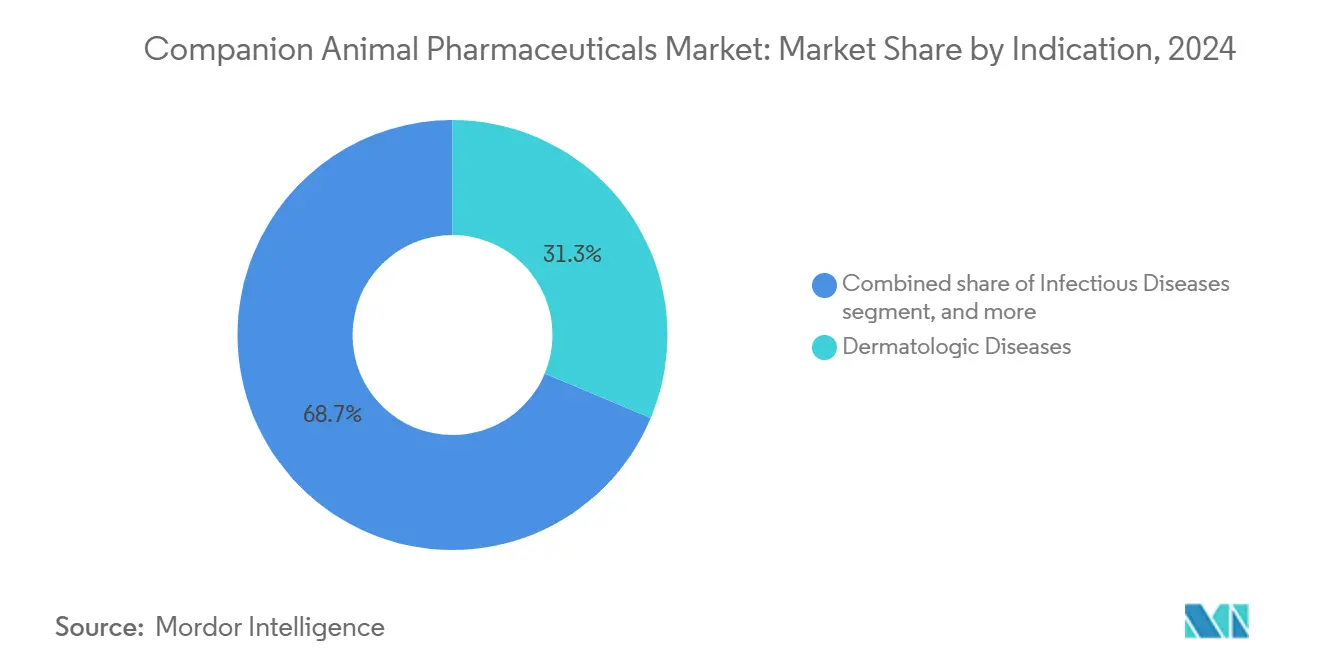

- By indication, dermatologic diseases led with 31.34% of the companion animal pharmaceuticals market share in 2024, while neurologic disorders are forecast to expand at an 8.45% CAGR to 2030.

- By product type, parasiticides captured 29.45% of the companion animal pharmaceuticals market size in 2024, whereas anti-inflammatory analgesics are advancing at a 7.92% CAGR through 2030.

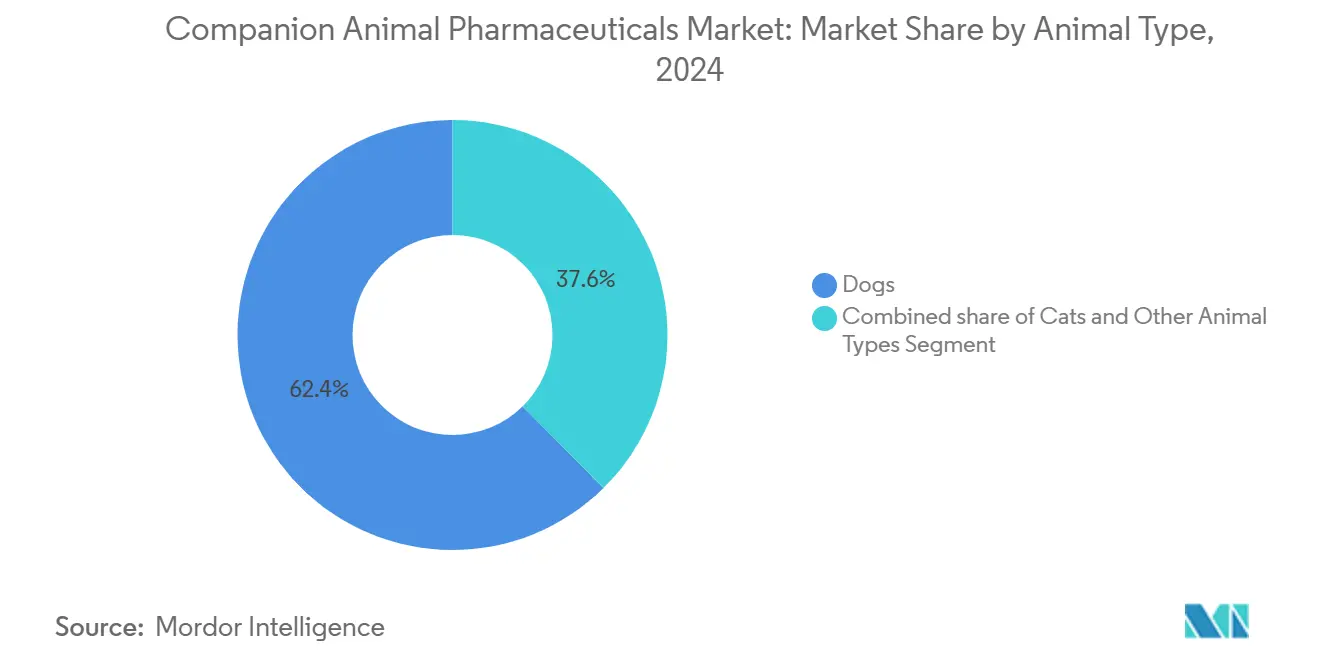

- By animal type, dogs dominated revenue with 62.45% in 2024; cats represent the fastest-growing cohort at a 6.99% CAGR through 2030.

- By distribution channel, veterinary hospitals held 54.56% of 2024 revenue, while e-commerce is projected to rise at a 9.34% CAGR to 2030.

- North America accounted for 42.32% of 2024 sales; Asia-Pacific is projected to grow at 7.43% CAGR, led by China’s rapidly maturing pet economy.

Global Companion Animal Pharmaceuticals Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing pet ownership and human–animal bond | +1.8% | Global with strongest effect in Asia-Pacific | Long term (≥ 4 years) |

| Rising pet insurance adoption and spend | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| Advances in companion animal drug innovations and approvals | +1.5% | Global led by US and EU | Medium term (2–4 years) |

| Growing veterinary healthcare expenditure | +1.0% | Global premium markets | Long term (≥ 4 years) |

| Expansion of telehealth-enabled veterinary pharmacies | +0.7% | North America core, spill-over to developed markets | Short term (≤ 2 years) |

| Emergence of precision genomics and personalized pet medicine | +0.9% | Premium markets in North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Pet Ownership and Human–Animal Bond

Global pet numbers climbed sharply during the pandemic as younger households embraced companion animals as family members, often prioritizing pet care over discretionary spending. High-value therapeutics such as Librela for osteoarthritis have quickly gained traction, treating more than 1 million dogs within two years of launch. The resilience of the wider pet economy is illustrated by its projected USD 279 billion value in 2030, delivering steady demand even when macroeconomic conditions tighten. Yet significant headroom remains, especially in feline health where only 40% of cats receive annual veterinary visits compared with 82% of dogs. Species-specific innovations such as the anxiety therapy Bonqat begin to unlock this latent potential.

Rising Pet Insurance Adoption and Spend

North American premiums more than doubled to USD 4.5 billion in 2024, boosting owners’ capacity to pursue advanced diagnostics and specialty drugs[2]North American Pet Health Insurance Association, “2024 State of the Industry Report,” insurancejournal.com. Insured pets undergo a greater volume of imaging and lab work, fueling prescription growth for chronic conditions. Financial-sector confidence is evident in the 90% market concentration among the top 10 insurers, though recent exits by select carriers reveal the need to balance actuarial risk with escalating veterinary costs. The interplay of rising coverage limits and cost containment will shape therapeutic adoption rates in the medium term.

Advances in Companion Animal Drug Innovations and Approvals

US and EU regulators accelerated approval timelines in 2024 and 2025, with conditional authorizations enabling first-in-class therapies like the feline hypertrophic cardiomyopathy drug Felycin-CA1 to reach clinics sooner. Monoclonal antibodies such as Librela and Solensia deliver durable pain relief while long-acting otic formulations reduce dosing burdens, lifting compliance to new highs. Prioritized review pathways and extended patent lives encourage sustained R&D investment, ensuring a robust pipeline of neurologic and immunomodulatory candidates.

Growing Veterinary Healthcare Expenditure

Average companion animal practice revenue exceeded USD 600,000 in 2025, helped by rising procedure intensity and integration of AI-based diagnostics. Corporate consolidators now control roughly 30% of clinics, leveraging scale to negotiate pharmaceutical purchasing and drive protocol adoption. AI-enhanced imaging platforms such as Vetscan Imagyst detect subtle pathologies, justifying premium-priced therapeutics and supporting higher average transaction values. Workforce shortages remain a constraint, signaling further demand for digital triage and targeted medical solutions that reduce in-clinic time.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval frameworks | -0.8% | Global, intensity varies by jurisdiction | Medium term (2–4 years) |

| Growing antimicrobial stewardship pressures | -0.6% | Developed markets lead adoption | Long term (≥ 4 years) |

| High development and compliance costs | -0.7% | Global, highest in US and EU | Medium term (2–4 years) |

| Price transparency platforms squeezing brand premiums | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Frameworks

Complex global dossiers drive development costs higher, especially for first-in-class modalities that require new safety endpoints. Updated US labeling rules standardize content but extend documentation timelines, while VICH harmonization efforts still leave region-specific variations that complicate launch sequencing. Conditional approvals grant earlier revenue but oblige sponsors to supply post-marketing efficacy data inside a five-year window, adding economic uncertainty. Smaller innovators feel the burden most and often partner with larger firms or focus on niche indications to manage risk.

Growing Antimicrobial Stewardship Pressures

Regulators moved medically important antibiotics behind prescription control in 2023 to curb resistance, reducing volume demand for broad-spectrum agents[3]AVMA Government Relations, “Implementation of FDA Guidance #263,” avma.org. Veterinary feed directives and standardized daily-dose monitoring systems widen surveillance, with South Korea’s program demonstrating early success in tracking clinic-level usage. Research emphasis is shifting toward narrow-spectrum or pathogen-specific alternatives, yet development costs and proof-of-concept hurdles are higher than for legacy molecules.

Segment Analysis

By Indication: Neurologic Disorders Drive Innovation

Dermatologic diseases captured 31.34% of the companion animal pharmaceuticals market share in 2024 thanks to blockbuster brands Apoquel and Cytopoint that deliver rapid itch relief and long treatment durations. Sales growth remains resilient, but neurologic disorders are forecast to expand faster at an 8.45% CAGR as clinicians adopt multi-drug epilepsy protocols and FDA-approved anxiolytics such as Bonqat reach specialty and general practices. Combination therapies that include levetiracetam and zonisamide broaden seizure control, although liver monitoring is essential when phenobarbital remains part of the regimen.

Rising awareness of the gut–brain axis encourages adjunctive ketogenic diets and probiotic supplementation, offering non-pharmacologic support that complements prescription drugs. Genetic tests identify breed predispositions to idiopathic epilepsy, guiding preventive counseling and earlier intervention. These diagnostics deepen case volumes and reinforce the companion animal pharmaceuticals market as owners pursue holistic management plans.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Anti-Inflammatory Surge Challenges Parasiticide Dominance

Parasiticides accounted for 29.45% of the companion animal pharmaceuticals market size in 2024, anchored by broad-spectrum chewable combinations such as Simparica Trio that now include flea tapeworm prevention claims. The segment faces rising price competition from generics, yet branded franchises continue to innovate through extended-spectrum indications. Anti-inflammatory and analgesic drugs are projected to grow at 7.92% CAGR, propelled by revised feline NSAID guidelines that endorse chronic use of meloxicam and robenacoxib beyond acute scenarios.

Monoclonal antibodies targeting nerve growth factor or IL-31 provide month-long relief and avoid traditional NSAID contraindications, expanding the eligible patient pool and supporting premium price points. Biodegradable polymer formulations reduce dosing frequency for otic and dermatologic therapy, improving adherence and clinic efficiency.

By Animal Type: Feline Market Awakening

Dogs continue to represent 62.45% of 2024 revenue, yet cats deliver the strongest incremental contribution at 6.99% CAGR through 2030 as manufacturers tailor formulations to feline physiology and palatability. Bonqat’s launch as the first FDA-approved feline anxiety drug signals a shift toward cat-specific neurobehavioral care. Likewise, Felycin-CA1 for hypertrophic cardiomyopathy and Varenzin-CA1 for CKD-related anemia meet long-standing therapeutic gaps.

Urban apartment living, particularly in Asia-Pacific, favors cat ownership and boosts preventive care uptake. Exotic and minor species gain regulated options via the FDA Indexing program, opening niche opportunities for specialized antiparasitic and anti-infective products that command high margins.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates

The companion animal pharmaceuticals market size allocated to veterinary hospitals reached 54.56% in 2024, underscoring their role as diagnostic hubs and prescription gatekeepers. Nonetheless, e-commerce platforms are projected to grow at 9.34% CAGR, driven by seamless integration of teleconsultation, pharmacy fulfillment, and home delivery. Leading online retailers now invest in physical clinics, creating hybrid service models that leverage data analytics for personalized reminders and loyalty incentives.

Traditional retail pharmacies broaden veterinary offerings, yet clinical insight remains critical for chronic disease management, guiding regulatory bodies toward clearer telehealth protocols that maintain animal welfare standards. Strategic acquisitions of distribution networks by private equity signal confidence in the scalability of omnichannel supply chains.

Geography Analysis

North America generated 42.32% of 2024 revenue, anchored by pet insurance penetration above 3% of total pets and rapid uptake of novel biologics. The FDA’s efficient review system enables early-cycle launches, giving local operations such as Zoetis and Elanco a home-field advantage that accelerates brand momentum. Corporate practice chains negotiate volume rebates, yet independent clinics still capture significant share by emphasizing concierge-style service.

Asia-Pacific delivers the fastest growth at 7.43% CAGR to 2030, propelled by China’s pet economy which is expanding at 12.9% CAGR to reach RMB 756.5 billion by 2030. Veterinary infrastructure investment is catching up, illustrated by a rising number of tier-one city specialty hospitals with MRI and CT capacity. Regulatory frameworks mature quickly; South Korea’s antimicrobial surveillance system and Japan’s centralized MAFF approvals create predictable environments for multinationals to launch premium lines.

Europe maintains balanced momentum on the back of harmonized EMA regulations and strong welfare commitments. German, French, and UK households accept preventive health plans bundled with insurance, though price sensitivity tempers biologic adoption compared with North America. Strategic acquisitions by European firms such as Virbac expand geographic footprints, while private equity buys into veterinary service groups, anticipating continued consolidation.

South America, the Middle East, and Africa contribute a smaller revenue share yet present long-term upside as companion animal ownership rises alongside urbanization. Multinationals pilot vaccine and parasiticide programs through distribution partnerships that navigate heterogeneous regulatory standards and variable cold-chain infrastructure.

Competitive Landscape

The companion animal pharmaceuticals market is moderately concentrated, with the five largest firms holding more than 60% of global revenue. Zoetis leads with USD 9.3 billion in 2024 sales, deriving roughly two-thirds from companion animals and posting an 8% revenue CAGR since its 2013 spin-off. Boehringer Ingelheim follows at EUR 4.7 billion, buoyed by NEXGARD’s double-digit growth and recent acquisitions that add therapeutic vaccines. Elanco places third with USD 4.4 billion and an innovation pipeline targeting dermatology, pain, and parasiticide adjacencies.

Diagnostic integration distinguishes IDEXX, whose 91% companion animal revenue focus supports pharmaceutical partners through precise disease detection and monitoring. Dechra strengthens niche leadership with single-dose otic solutions amid its transition to private equity ownership. Private investors increase their footprint, evidenced by EQT’s takeover of Dechra and its pending VetPartners acquisition that bundles distribution, services, and practice management into a cohesive platform. Competitive positioning revolves around lifecycle management, rapid geographic rollouts, and the blending of therapeutic, diagnostic, and digital assets to deepen customer lock-in.

Companion Animal Pharmaceuticals Industry Leaders

-

Zoetis Inc.

-

Boehringer Ingelheim Animal Health

-

Elanco Animal Health

-

Merck Animal Health (MSD)

-

Virbac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zoetis posted USD 2.2 billion Q1 revenue with 8% companion animal product growth and raised full-year guidance to as much as USD 9.575 billion.

- May 2025: Merck Animal Health acquired US rights to the SENTINEL parasiticide range and announced a USD 895 million Kansas manufacturing and R&D expansion.

- May 2025: Zoetis opened a 32,000-square-foot reference laboratory in Louisville, KY, to enhance diagnostic turnaround times.

- May 2025: Dechra gained FDA approval for Otiserene, a single-dose canine otitis externa therapy that delivered 71.3% clinical improvement in trials.

- April 2025: The FDA cleared an expanded indication for Simparica Trio, making it the first canine parasiticide to prevent flea tapeworm infection by eliminating vector fleas.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the companion animal pharmaceutical market as the annual revenues generated worldwide from prescription and approved over-the-counter drugs, biologicals, and vaccines that prevent, diagnose, or treat diseases in household pets, principally dogs and cats, with rabbits and small mammals captured in "other companion animals." According to Mordor Intelligence, only finished, regulated therapeutics are counted; bulk actives, nutritional supplements, medicated feeds, and livestock medicines sit outside this boundary.

Scope Exclusion: items such as functional treats, probiotics, feed additives, and production-animal drugs are not included.

Segmentation Overview

- By Indication

- Infectious Diseases

- Dermatologic Diseases

- Orthopedic Diseases

- Ophthalmic Diseases

- Neurologic Disorders (Epilepsy, Anxiety)

- Other Indications

- By Product Type

- Vaccines

- Parasiticides & Ectoparasiticides

- Anti-infectives (Antibiotics, Antivirals, Antifungals)

- Anti-inflammatory & Analgesics (NSAIDs, Steroids)

- Other Product Types

- By Animal Type

- Dogs

- Cats

- Other Animal Types

- By Distribution Channel

- Veterinary Hospitals & Clinics

- Retail Pharmacies

- Online / E-commerce Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews were held with practicing veterinarians, purchasing managers at veterinary hospital chains, regional distributors, and e-commerce pharmacy executives across North America, Europe, and fast-growing Asian markets. Surveys of pet owners supplemented demand-side elasticity assumptions, while follow-up calls with regulatory experts clarified launch timelines for monoclonal antibodies and long-acting parasiticides.

Desk Research

Mordor analysts began with authoritative, open datasets such as the FDA-CVM Green Book, USDA APHIS pet import tallies, European Medicines Agency product registries, Australia's APVMA approvals, and trade association yearbooks from APPA, FEDIAF, and NAPHIA. Company 10-Ks, patent filings accessed via Questel, and Dow Jones Factiva news archives anchored competitive and pricing insights. Academic journals provided incidence data on atopic dermatitis, osteoarthritis, and vector-borne diseases. This list is illustrative; many additional public and paid sources informed the evidence base.

Market-Sizing & Forecasting

A top-down and bottom-up blend was applied. We first reconstructed national demand pools from pet population, average veterinary-drug spend per animal, and compliance ratios. We then cross-checked totals with supplier shipment estimates and sampled ASP × volume data from distributor audits. Key model variables include: 1. Annual dog and cat population growth, 2. Vaccination coverage rates, 3. Chronic disease prevalence (e.g., osteoarthritis, epilepsy), 4. Average selling price drift after patent expiry, 5. New molecule approvals per year. Forecasts to 2030 rely on multivariate regression supported by ARIMA smoothing to capture cyclical heartworm and flea treatment seasons. Scenario analysis adjusts for macro shocks and currency shifts. Gaps in bottom-up inputs were bridged through ratio imputation from comparable economies before being re-triangulated.

Data Validation & Update Cycle

Outputs pass variance checks against historical customs data and insurer reimbursement trends, followed by peer review among senior analysts. Models refresh annually, with interim updates triggered by blockbuster drug launches, regulatory bans, or material M&A. A final sense-check is performed immediately prior to publishing so clients receive the latest perspective.

Why Mordor's Companion Animal Pharmaceuticals Baseline Is Dependable

Published figures often diverge because providers choose different product baskets, pet cohorts, and currency bases. We scrutinize each lever and publish a midpoint view that reflects realistic uptake and price erosion rather than aggressive best-case scenarios.

Key Gap Drivers include whether authors fold in medicated feeds, how they treat equine drugs, the cadence of refresh (Mordor is annual; some peers revisit every two to three years), and whether list or realized ASPs underpin calculations. Currency conversion dates and inflation deflators also widen spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.24 B (2025) | Mordor Intelligence | - |

| USD 25.60 B (2024) | Global Consultancy A | Includes feed additives, nutraceuticals, and equine drugs; uses manufacturer list prices |

| USD 16.63 B (2024) | Industry Association B | Excludes online pharmacy sales outside North America; two-year refresh cycle |

| USD 17.53 B (2024) | Trade Journal C | Utilizes survey-based pet counts without adjusting for multi-pet households |

In sum, while estimates vary, Mordor's disciplined scoping, frequent updates, and dual-path modeling give decision-makers a balanced, transparent baseline they can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the companion animal pharmaceuticals market?

The market is valued at USD 16.24 billion in 2025 and is projected to reach USD 21.98 billion by 2030 at a 6.24% CAGR.

Which therapeutic area holds the largest revenue share?

Dermatologic diseases lead with 31.34% of 2024 revenue, supported by brands such as Apoquel and Cytopoint.

Which region is expanding fastest?

Asia-Pacific is forecast to grow at a 7.43% CAGR, driven by rising pet ownership and healthcare spend in China and South Korea.

How are online channels affecting distribution?

E-commerce platforms are projected to grow at 9.34% CAGR, integrating telehealth consultations with pharmacy services to improve access and adherence.

What regulatory trends are shaping product development?

Accelerated approval pathways and conditional licenses in the US and EU shorten time-to-market, while antimicrobial stewardship rules tighten oversight of antibiotic use.

Page last updated on: