Market Trends of United States Commercial Real Estate Industry

This section covers the major market trends shaping the US Commercial Real Estate Market according to our research experts:

Industrial Sector Expected to Record High Demand

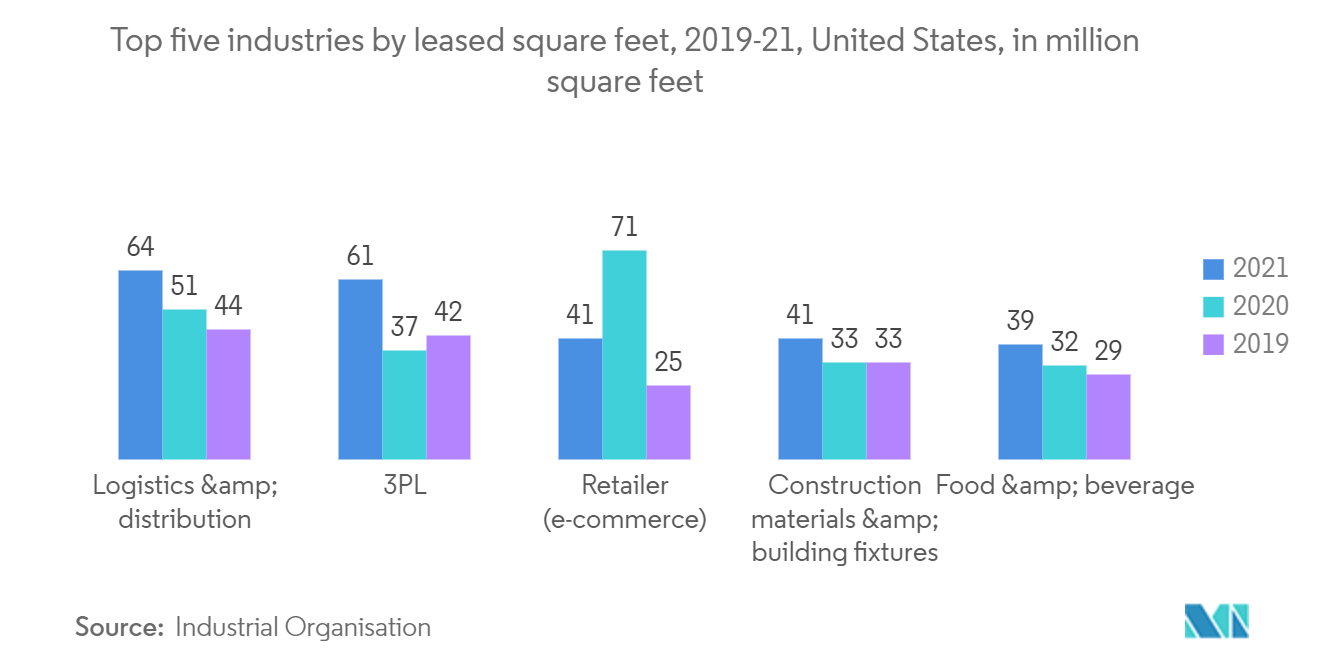

The US commercial real estate market ended 2021 with unprecedented demand, exceptionally low vacancy rates, and record-setting rental growth. Though the supply chain crisis added pressure to many economic factors, the industrial sector benefited from supply chain reconfigurations. While industry demand shifted away from e-commerce in 2021, the existing online shopping practices drove up the demand for 3PL and logistics and distribution.

Since the onset of the pandemic, industrial leasing has increased by more than 24%. The scarce availability of properties in the market continued to push vacancy down in 2021. For the first time in history, vacancy dropped below the 4% threshold, with a vacancy rate of 3.8% reported in 2021. With the strong leasing from prior quarters and tenants shifting properties throughout 2021, the net absorption increased by more than 81% year-over-year. The net absorption significantly exceeded expectations that year, recording over 496.3 million sq. ft. Rents also continued to trend upward as the market grew even more competitive, with the average asking rate at USD 7.11 per sq. ft. Also, the year-over-year rent was up by 11.3%.

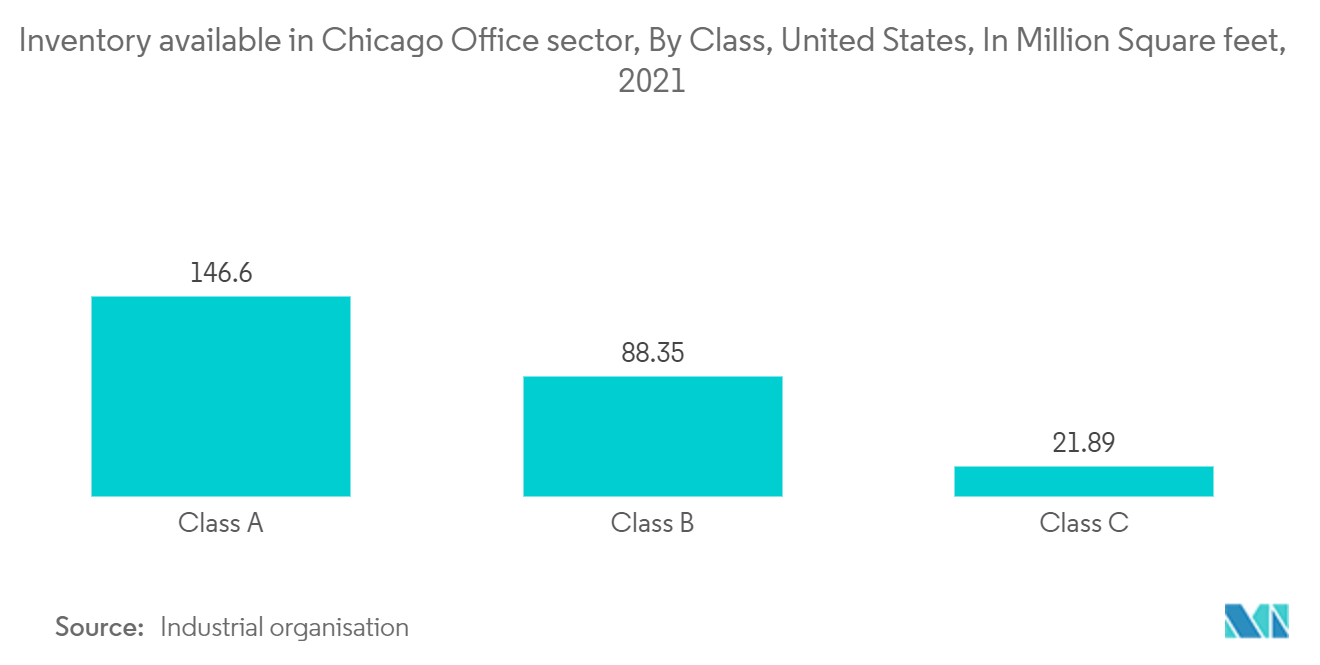

Chicago's Office Sector Closed 2021 on a High

After much turbulence, the Chicago suburban office market closed 2021 on a high after realizing year-over-year growth in new lease transactions and improved levels of capital market activity. Overall, leasing realized a slight uptick quarter-over-quarter, but the total activity realized throughout the year grew 14% compared to 2020. The average term increased consecutively over the last three quarters, as tenants became more comfortable signing longer-term deals in the second half of the year. The current average is 66 months, which remains 13% below pre-pandemic standards. While new leasing grew over the course of the year, tenants are disproportionately favoring Class A offices, which accounted for nearly 70% of the new leases executed in 2021.

The overall absorption levels began to plateau as Q4 realized -50,807 sq. ft of absorption. The largest move-outs came from AT&T at 903 National Pkwy and Lake Forest Graduate School at 1300 E Woodfield for 106,380 sq.ft and 56,000 sq.ft, respectively. Much the like the rest of the nation, the Class B office inventory continued to underperform. This was due to large tenant downsizes and a shift in preference to high-quality Class A buildings in order to motivate employees to return to physical workplaces.

Property sales grew substantially in the second half of the year after nine buildings traded hands from Q3 to Q4. A total of 14 buildings were sold in 2021 for just over USD 0.5 billion in transactional volume, which is slightly lower than the usual levels. The largest transaction closed in Deerfield after the four-building 700,000 sq. ft campus, Corporate 500, closed for USD 178 million or USD 256 per square feet. The transaction marked the highest sale price recorded over the last three years.