Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

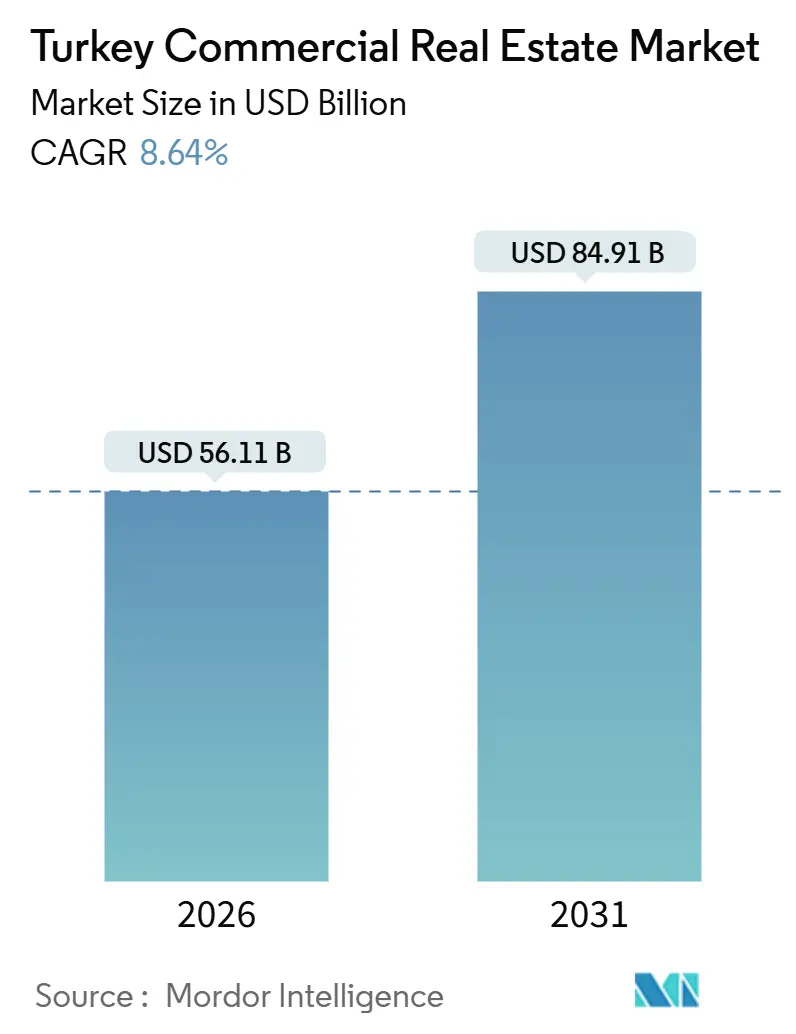

| Market Size (2026) | USD 56.11 Billion |

| Market Size (2031) | USD 84.91 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

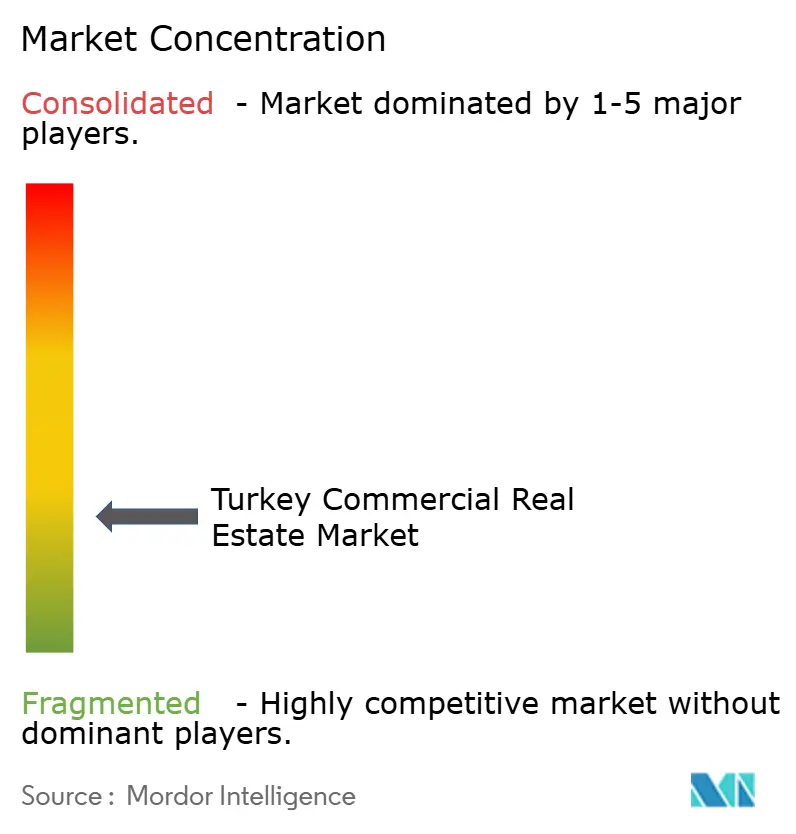

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Commercial Real Estate Market Analysis by Mordor Intelligence

The Turkey Commercial Real Estate Market size is estimated at USD 56.11 billion in 2026, and is expected to reach USD 84.91 billion by 2031, at a CAGR of 8.64% during the forecast period (2026-2031). This expansion is underpinned by nearshoring-led manufacturing, e-commerce-driven logistics absorption, and sustained tourism receipts that keep hospitality and retail occupancy elevated[1]OECD Economic Surveys: Türkiye 2024, OECD, oecd.org. Tight supply of Grade-A assets, currency-hedged lease structures, and seismic-code-compliant redevelopment further bolster rental yields despite a 50% policy-rate environment. Logistics leads all property types in growth as warehouse demand outpaces new completions, while data-center commitments from Google and other hyperscale operators signal rising appetite for digital infrastructure. Istanbul accounts for just over half of the overall value, yet Izmir is the fastest-growing city as port upgrades and lower land prices attract industrial tenants. Fragmented ownership among domestic GYOs, private developers, and global advisory firms keeps competition fluid and transaction pipelines diversified.

Key Report Takeaways

- By business model, rentals captured 73.7% of the Turkey commercial real estate market share in 2025; sales are expected to log the fastest 9.42% CAGR through 2031.

- By property type, retail led with 37.1% revenue share in 2025, while logistics is projected to advance at a 9.81% CAGR to 2031.

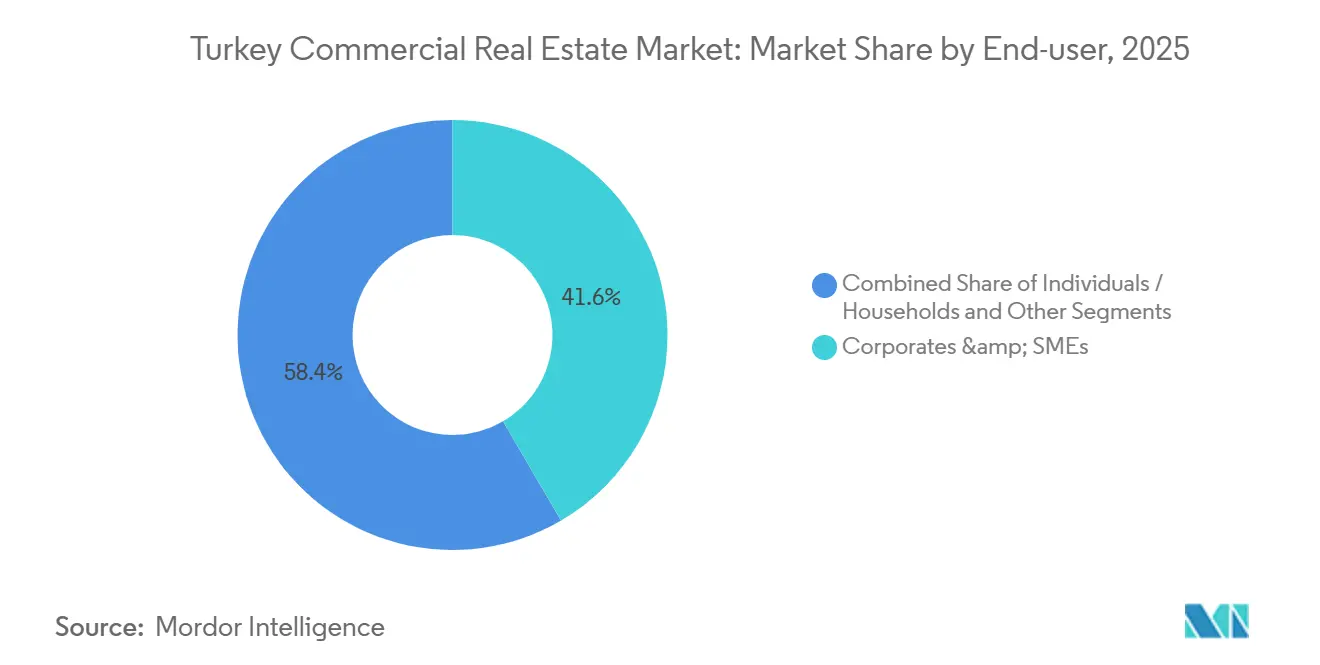

- By end-user, corporates and SMEs accounted for 44.9% of the Turkey commercial real estate market size in 2025; the same cohort is poised for the highest 10.03% CAGR to 2031.

- By city, Istanbul commanded 52.3% value in 2025, whereas Izmir is set to expand at a 10.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring and export-led manufacturing boost logistics/industrial demand | +2.1 | Marmara and Aegean corridors | Medium term (2–4 years) |

| Growing e-commerce accelerates modern warehousing and last-mile hubs | +1.9 | National with Istanbul focus | Medium term (2–4 years) |

| Tourism rebound supports hotels, retail, and mixed-use in coastal and heritage cities | +1.8 | Coastal regions and Cappadocia | Short term (≤ 2 years) |

| Urban renewal and seismic-resilient rebuilds create Grade-A development pipelines | +1.6 | Istanbul, Izmir, Bursa | Long term (≥ 4 years) |

| Data centers and business parks benefit from strategic location | +1.2 | Ankara and Istanbul | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring And Export-Led Manufacturing Boost Logistics/Industrial Demand

European automakers expanded capacity in Turkey during 2024, prompting a 100% rise in industrial rents as Organized Industrial Zones filled rapidly. Renault’s USD 220 million Bursa outlay lifted EV output and sparked ancillary warehouse leasing within a 100-kilometer radius. Manufacturing FDI climbed 32.5% year-on-year to USD 2.3 billion, diversified across Dutch, German, and U.S. investors. Government policy now targets USD 10 billion per year of fresh FDI, chiefly by enlarging OIZ capacity and streamlining permits. These measures shorten supply chains to Europe, trimming logistics costs up to 18% versus central Anatolia locations.

Tourism Rebound Supports Hotels, Retail, And Mixed-Use In Coastal And Heritage Cities

Tourism receipts hit USD 61.1 billion in 2024 as 52.6 million visitors flocked to coastal resorts and historic districts. Five-star occupancy in Antalya exceeded 85% between May and October, reviving stalled hotel pipelines. Istanbul’s Tersane waterfront melds shopping, dining, and museums across 140,000 square meters to capture visitor spending.[2]Turkey Real Estate Market Report H1 2024, Cushman & Wakefield, cushmanwakefield.com Luxury high-street rents on Bağdat Avenue reached USD 250 per square meter per month, a 40% premium over secondary sites. A VAT-exemption program for hotel renovations over 50 rooms accelerates cap-ex cycles and sustains tourism-led demand.

Urban Renewal And Seismic-Resilient Rebuilds Create Grade-A Development Pipelines

Law 6306 mandates demolition of non-compliant stock, generating a multi-decade Grade-A pipeline. ISMEP financing of USD 1.26 billion will retrofit 1,095 public buildings by end-2024. New code compliance adds 15%–25% to costs but secures rent premiums of up to 30% as tenants prioritize safety and insurers lower premiums[3]Turkey Economic Monitor, World Bank, worldbank.org. Emlak Konut’s USD 150 million Yeni Fikirtepe scheme outlines 11,000 seismically sound units plus retail amenities. Istanbul, Izmir, and Bursa host 70% of transformation sites, setting long-run demand for engineering and materials.

Growing E-Commerce Accelerates Modern Warehousing And Last-Mile Hubs

Online sales jumped to USD 66.6 billion equivalent in 2023, lifting warehouse take-up to 179,700 square meters in H1 2024—a 138% leap. FedEx opened a USD 130 million, 25,000-square-meter hub at Istanbul Airport in September 2025, slicing regional transit times by 30%. Amazon’s Tuzla fulfillment center employs 1,500 staff and handles same-day delivery across Marmara. SMARTIST’s 205,000-square-meter first phase underscores Istanbul’s air-cargo prominence. Government-designated logistics zones supply land 40% cheaper than private sites, catalyzing national distribution footprints.

Restraints Impact Analysis

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility, high inflation, and financing costs complicate underwriting | -1.5 | Nationwide | Short term (≤ 2 years) |

| Seismic code compliance and construction inflation elevate project budgets | -0.9 | Istanbul, Izmir, Bursa | Medium term (2–4 years) |

| Permitting variability and geopolitical/policy uncertainty extend timelines | -0.7 | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility, High Inflation, And Financing Costs Complicate Underwriting

The Turkish lira lost 30% against the dollar in 2024 while inflation reached 64.77%, squeezing unhedged returns. A 50% policy rate translates into 55%–65% commercial loan costs, rendering leverage unworkable unless rents reset 40% yearly. Dollar-pegged leases and swaps offset exposure but erode 3%–5% of gross yield spreads. İş GYO and Akfen postponed equity raises after the REIT index fell 18% in lira terms during the first nine months of 2024. Cash-rich conglomerates and sovereign funds thus dominate acquisitions, sidelining highly leveraged private equity.

Seismic Code Compliance and Construction Inflation Elevate Project Budgets

Mandatory seismic isolators and reinforced concrete add 15%–25% to baseline costs, while steel and cement outpaced CPI by up to 15 points in 2024. Retrofitting a 10-story block in Kadıköy can cost USD 800–1,200 per square meter versus USD 600–900 for new builds on vacant land. Permit approvals average 18–24 months in fragmented ownership scenarios, inflating carrying costs and deferring revenue. Insurers now refuse non-compliant buildings, pushing landlords toward upgrades or tenant churn. Smaller developers without deep balance sheets exit or merge, catalyzing consolidation.

Segment Analysis

By Business Model: Rental Dominance Reflects Yield-Seeking Capital

Rental assets accounted for 73.7% of the Turkey commercial real estate market share in 2025, driven by investors favoring dollar-indexed income streams that protect against lira depreciation. Pension funds and GYOs structure triple-net leases delivering 8%–10% annualized returns on Grade-A offices and malls. The build-to-rent wave is enlarging stock aimed at young professionals as home-ownership dips to 58%. Fractional ownership via the August 2025 tradable certificate launch on the USD 1.51 billion Damla Kent project could narrow the rental-sales gap by unlocking liquidity for retail investors. Sales transactions remain smaller but command premiums in luxury coastal enclaves, where Bodrum villas appreciated 12%–18% during 2024.

Rental growth is forecast at a robust 9.42% CAGR, supported by seismic-upgrade completions that achieve 20%–30% rent premiums. Conversely, sales activity faces headwinds from higher citizenship thresholds and mortgage costs exceeding 30%. Long-run upside exists for sales via digital platforms that shorten settlement cycles and through master-planned communities that offer integrated amenities. Still, rentals will remain the ballast of the Turkey commercial real estate market as institutions prioritize predictable cash flows and dividend visibility.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Property Type: Logistics Surge Contrasts With Retail Maturity

Retail led the 2025 revenue table at 37.1%, underpinned by 441 shopping centers totaling nearly 14 million square meters of GLA. Yet logistics assets are projected to post the fastest 9.81% CAGR as e-commerce and nearshoring tighten warehouse vacancies. Warehouse rents in Istanbul’s Tuzla corridor doubled year-on-year, while Izmir’s port expansion supports cost-effective distribution into Europe. FedEx’s USD 130 million airport hub and SMARTIST’s scalable air-cargo campus exemplify institutional bets on Turkey’s logistics spine.

Although brick-and-mortar retail faces online cannibalization, experiential formats—cinemas, indoor ski slopes, and food halls—keep occupancy above 95% at flagship centers like Mall of Istanbul. High-street strips in Nişantaşı achieve USD 250 per square meter rents, leveraging tourist luxury appetite. Office demand rebounded strongly, with Grade-A Istanbul occupancy touching a 12-year peak of 89.7% on the back of consolidations into seismic-compliant towers. Data-center and hospitality pipelines diversify the asset mix, ensuring that the traditional office-retail dyad no longer dominates the Turkey commercial real estate market.

By End-User: Corporations and SMEs Lead Occupier Mix

Corporates and SMEs held 44.9% revenue share in 2025, underlining their role as primary drivers of the Turkey commercial real estate market. The country’s 3.5 million registered enterprises, plus USD 1.2 billion in 2023 venture-capital inflows, feed a constant appetite for modern offices, light-manufacturing sheds, and data-center plots. Multinationals rented 60% of Istanbul’s new Grade-A supply in 2024, gravitating to seismic-proof towers with LEED certification that slash insurance costs. SMEs, especially e-commerce startups, favor co-working environments; flexible-space operators expanded footprints by 25% in 2024.

Individuals and households account for a smaller slice but sustain luxury coastal schemes. Bodrum villas appreciated 18% in 2024 after a wave of high-net-worth buyers from Gulf markets piled into branded residences with marina access. Government-subsidized rent support for tech startups under the KOSGEB program nudges SMEs into specialized tech parks in Ankara and Istanbul, reinforcing the forecast 10.03% CAGR for corporate-driven demand. The Turkey commercial real estate market share of corporates is expected to inch higher as crowd-funded certificates begin to finance tenant-specific shells.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Istanbul’s 52.3% grip on national value rests on unmatched infrastructure density and deep consumer spending. The city absorbed 138,597 square meters of Grade-A office stock in H1 2024, a 32.9% leap from the prior year, while the Istanbul Financial Center sealed full occupancy for anchor towers housing the central bank and capital-markets regulator. Prime logistics rents inside the airport corridor doubled as tenants fought for the last developable plots within the third-ring highway. Even so, seismic retrofitting curbs older stock; ISMEP demolished 592 sub-standard buildings by end-2024 and unlocked a USD 1.26 billion pipeline of code-compliant reconstruction.

Ankara, long a bureaucratic town, sharpened its tech profile after Google committed USD 1.2 billion to a data-center campus in Sincan. Office rents at USD 18 per square meter per month offer 60% savings versus Istanbul, prompting state agencies and foreign embassies to pre-lease Grade-A space in Çankaya. Government incentives reimburse up to 50% of rent for startups inside Bilkent and Hacettepe technoparks, feeding SME demand. Meanwhile, Izmir’s 10.23% CAGR outlook reflects the Aegean port expansion that will quadruple container throughput by 2030 and pull in nearshoring manufacturers seeking duty-free land.

Rest-of-Turkey markets exhibit pockets of resilience. Antalya’s 52.6 million national tourist arrivals in 2024 channeled USD 61.1 billion in visitor receipts that spill over into hotel and retail schemes. Bursa’s automotive corridor benefited from Renault’s EUR 200 million plant upgrade, sparking ancillary warehouse demand within a 100-kilometer radius. Municipal digitization of permit workflows cuts project timelines by 20-30% in the largest metros, but smaller municipalities still struggle with fragmented land titles, sustaining higher carrying costs for developers.

Competitive Landscape

Competition remains highly fragmented, with the leading GYOs controlling only a modest share of total gross asset value—leaving substantial headroom for industry consolidation. Emlak Konut deploys its tax-advantaged REIT structure to pre-sell residential units that fund mixed-use master plans, while Torunlar leans on mall management to recycle cash into logistics footprints. İş GYO and Akfen delayed 2024 secondary offerings after the REIT index lost 18% in lira terms, underlining the funding squeeze triggered by 50% policy rates. Cash-rich conglomerates such as Orjin Group exploit the gap: its USD 500 million acquisition of 42% of IstinyePark in April 2024 re-priced trophy retail assets north of USD 13,500 per square meter.

Foreign sovereign funds from Qatar, Abu Dhabi, and Kuwait concentrate on income-indexed office and hospitality plays, often teaming with local developers for permitting and construction expertise. Koc Holding’s USD 504 million marina buy in May 2025 diversifies into leisure while locking in dollar cash flows. Private developers Rönesans, NEF, and DAP Yapı increasingly use modular construction and off-site prefabrication to cut build cycles by up to 25%, a tactical hedge against volatile cement prices.

PropTech disruptors add another competitive vector. Tradable real-estate certificates, first issued for the USD 1.5 billion Damla Kent project, let individual investors buy blockchain-recorded slices of rental income, trimming transaction fees to 0.4%. Digital twin platforms that optimize energy use shave operating expenses 8-12%, a selling point for institutional buyers bound by ESG covenants. Consulting majors—Cushman & Wakefield, JLL, Colliers—package these technologies into asset-management mandates, chasing higher-margin advisory fees as pure brokerage spreads compress.

Turkey Commercial Real Estate Industry Leaders

Emlak Konut GYO

Torunlar GYO

Rönesans Gayrimenkul

NEF

Sinpaş GYO

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Emlak Konut signed a USD 400 million joint venture with Saudi Arabia’s National Housing Company to build 10,000 units in Mecca.

- September 2025: FedEx opened its USD 130 million, 25,000-square-meter Istanbul Airport hub, processing 7,000 packages per hour.

- May 2025: Koc Holding bought an Istanbul marina for USD 504 million, marking its entry into leisure real estate.

- October 2024: BLG Capital sold Galataport Istanbul to Dogus Group for USD 2.2 billion, Turkey’s largest property deal on record.

- September 2024: Google announced a EUR 1.1 billion (USD 1.2 billion) hyperscale data center in Ankara, operational by 2027.

Turkey Commercial Real Estate Market Report Scope

The commercial real estate market in Turkey report provides insights into the current economic scenario and consumer sentiment, commercial real estate buying trends - socioeconomic and demographic insights, government initiatives, regulatory aspects for the commercial real estate sector, insights into existing and upcoming projects, insights into interest rate regime for general economy and real estate lending, insights into rental yields in the commercial real estate segment, insights into capital market penetration and REIT presence in commercial real estate, insights into public-private partnerships in commercial real estate, insights into real estate tech and startups active in real estate segment (broking, social media, facility management, property management), and market dynamics, among others.

The report on the commercial real estate market in Turkey is segmented by type (office, retail, industrial, logistics, hospitality, and multi-family) and key cities (Istanbul, Bursa, and Antalya). The report offers market size and forecasts for the commercial real estate market in Turkey in value (USD billion) for all the above segments. The report also offers an in-depth analysis of the short-term and long-term impact of Covid-19 on the market. Additionally, the report provides company profiles to understand the competitive landscape of the market.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Turkey commercial real estate market in 2026?

It is estimated at USD 154 billion in 2026, tracking the 11.9% CAGR projected through 2031.

Which property type is growing fastest in Turkey?

Logistics facilities are pacing the quickest expansion, with a forecast 9.81% CAGR driven by e-commerce and nearshoring demand.

Why are rental models favored over sales transactions?

Dollar-indexed leases hedge against lira volatility, provide 8–10% nominal yields, and benefit from tax-exempt dividend rules for GYOs.

What city offers the highest growth rate?

Izmir leads with a 10.23% CAGR outlook thanks to port expansion and lower land costs.

How is seismic regulation influencing development costs?

The 2018 Earthquake Code adds 15–25% to construction budgets, pushing developers toward new builds or JV structures that can absorb the premium.

Who are the leading players in Turkey's commercial real estate?

Emlak Konut, Torunlar's GYO, Sinpa and Akfen—together holding 26% of gross asset value.