| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 35.87 Billion |

| Market Size (2030) | USD 43.99 Billion |

| CAGR (2025 - 2030) | 4.17 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Commercial Aircraft Avionics Systems Market Analysis

The Commercial Aircraft Avionics Market size is estimated at USD 35.87 billion in 2025, and is expected to reach USD 43.99 billion by 2030, at a CAGR of 4.17% during the forecast period (2025-2030).

The commercial aircraft avionics industry is experiencing rapid technological evolution, with a growing emphasis on sophisticated electronic systems and digital integration. Advanced software integration, enhanced autonomy capabilities, and the incorporation of artificial intelligence for improved aircraft management and fault prediction are becoming standard features in next-generation avionics systems. This technological advancement is evident in recent developments such as Garmin's September 2023 expansion of its G5000 integrated flight deck retrofit program for Citation XLS+ and XLS Gen2 aircraft, which introduces advanced visualization features and split-screen capability for simultaneous viewing of maps, charts, and weather data.

Global air travel has shown remarkable resilience, with IATA reporting a 28.4% increase in total aviation traffic in August 2023 compared to the previous year. This recovery has catalyzed significant fleet modernization initiatives across major airlines. In November 2023, Air India announced plans to add 30 aircraft to its fleet, while United Airlines placed a substantial order for 50 Boeing 787 Dreamliners in September 2023, demonstrating the industry's commitment to fleet renewal and expansion.

The avionics industry is witnessing a significant shift toward advanced avionics integration and connectivity solutions. In June 2023, Panasonic Avionics Corporation secured a landmark agreement with United Airlines to implement its new Astrova in-flight engagement solution, marking a significant advancement in passenger experience technology. This trend is further exemplified by the increasing adoption of cloud-connected cockpit systems, which enable seamless data transfer between aircraft and ground-based servers without physical connections.

Strategic partnerships and collaborations are reshaping the avionics landscape, with manufacturers focusing on developing integrated solutions for enhanced operational efficiency. Airlines are increasingly partnering with avionics providers to upgrade their existing fleets with advanced systems. For instance, in October 2023, EasyJet finalized a deal with Airbus for 157 new short-haul aircraft, incorporating state-of-the-art avionics systems. These partnerships are driving innovation in areas such as enhanced flight vision systems, advanced weather radar capabilities, and sophisticated flight management systems, contributing to improved safety and operational efficiency across the commercial aviation sector.

Commercial Aircraft Avionics Systems Market Trends

Airline Fleet Expansion Plans Driving Market Growth

The global commercial aviation industry is witnessing significant fleet expansion activities driven by increasing air passenger traffic and the need for more fuel-efficient aircraft. Major airlines worldwide are placing substantial orders for new aircraft, creating robust demand for advanced aircraft avionics systems. For instance, in September 2023, Air India announced plans to add 30 aircraft to its fleet, including six Airbus A350s, four Boeing B777s, and 20 narrow-body Airbus A320neo aircraft. Similarly, in October 2023, United Airlines revealed its expansion strategy to acquire 50 Boeing 787 Dreamliner aircraft and 60 single-aisle Airbus A321neo aircraft, with deliveries expected to begin in the next five years.

The growing backlog of aircraft orders from major manufacturers further demonstrates the strong momentum in fleet expansion plans. In 2022, Airbus delivered 661 commercial aircraft, an increase from 609 deliveries in 2021, while Boeing completed 480 commercial aircraft deliveries. The substantial order book is reflected in Airbus's backlog of 7,239 aircraft in 2022, while Boeing maintained a backlog of 5,430 aircraft. These expansion plans are complemented by the entry of new carriers and the growth of existing airlines in emerging markets. For instance, in August 2023, Qantas Airways placed a multi-million-dollar order for 24 new aircraft as part of their approach toward fleet expansion and modernization, while Lynx Air, Canada's new ultra-affordable airline, received its seventh Boeing B737 MAX-8 aircraft in May 2023 to support its North American market expansion.

Understand The Key Trends Shaping This Market

Download PDF

Retrofitting of Existing Aircraft with Advanced Avionics Systems

The aviation industry is experiencing a significant surge in retrofit activities as airlines worldwide upgrade their existing aircraft with advanced commercial aircraft avionics systems to enhance operational efficiency and comply with evolving aviation regulations. In September 2023, Garmin announced the expansion of its G5000 integrated flight deck retrofit upgrades to include the popular Cessna Citation XLS+ and XLS Gen2 aircraft. This upgrade provides modernized cockpit capabilities with additional features, reducing operational costs and increasing situational awareness while addressing concerns related to legacy avionics parts obsolescence. The G5000 system includes three landscape-oriented flight displays with split-screen capability, allowing pilots to simultaneously view maps, charts, checklists, TAWS, TCAS, flight plan information, and weather data.

The trend toward retrofitting is further evidenced by major developments in avionics upgrades across the industry. In August 2023, Bombardier introduced a new Advanced Avionics Upgrade (AAU) for the Bombardier Vision flight deck, featuring enhanced visualization capabilities and advanced software improvements. Additionally, in July 2023, Honeywell Aerospace announced the availability of their Primus Epic avionics upgrade for the Gulfstream G650/650ER, which includes new graphics modules providing higher terrain resolution and improved synthetic vision display options. The Block 3 avionics update introduces enhanced graphics, improvements to communications and alerting systems, and new software for the next-generation flight management system. These retrofitting initiatives are driven by the need to extend aircraft lifecycle, improve safety features, and maintain compliance with emerging aviation standards. The involvement of leading avionics systems manufacturers in these upgrades highlights the dynamic nature of the avionics market.

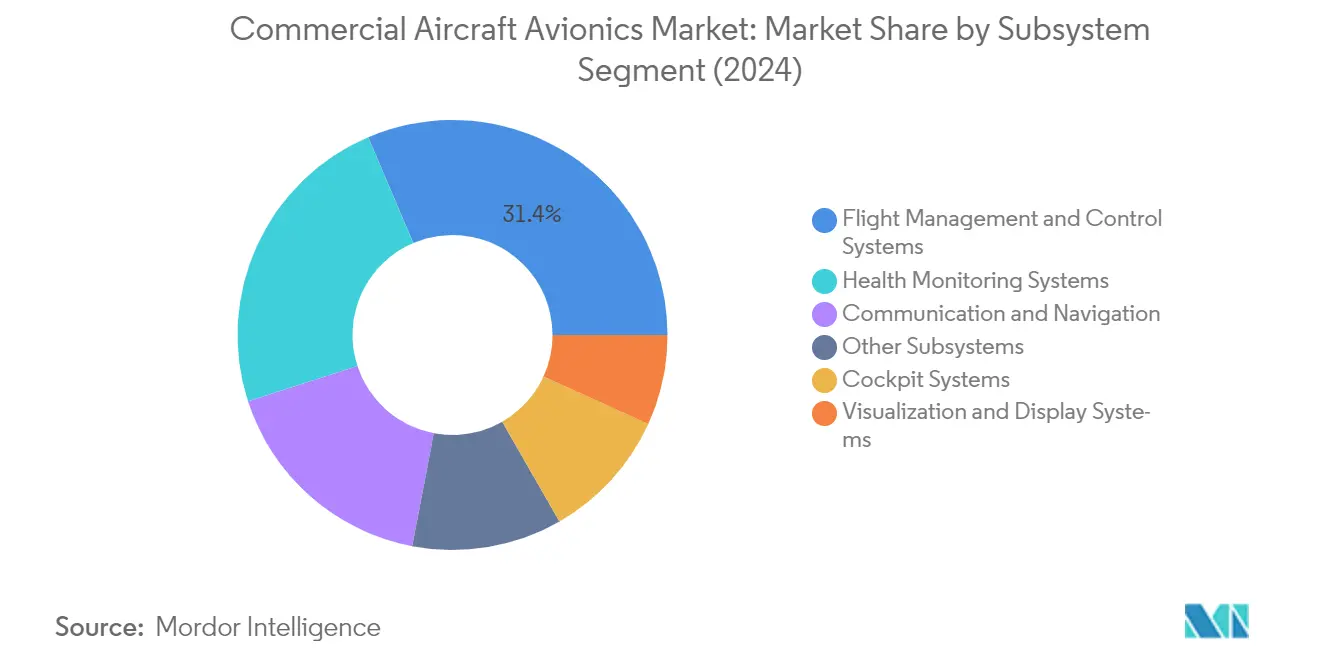

Segment Analysis: By Subsystem

Flight Management and Control Systems Segment in Commercial Aircraft Avionics Market

Flight Management and Control Systems (FMCS) continue to dominate the commercial aircraft avionics market, commanding approximately 31% market share in 2024. This segment encompasses sophisticated computer systems that automate various in-flight tasks, significantly reducing flight crew workload and eliminating the need for flight engineers or navigators. The segment's prominence is driven by increasing airline requirements for operational efficiency, safety, and sustainability of aircraft operations. Major aircraft manufacturers are actively partnering with leading avionics OEMs to equip their aircraft with advanced flight management and control systems, particularly focusing on features that enhance operational efficiency and fuel consumption optimization through up-to-the-minute data utilization. The aircraft flight control systems market is expected to continue its growth trajectory as airlines seek to enhance their operational capabilities.

Visualization and Display Systems Segment in Commercial Aircraft Avionics Market

The Visualization and Display Systems segment is experiencing remarkable growth, projected to expand at approximately 11% CAGR from 2024 to 2029. This accelerated growth is driven by increasing demand for advanced heads-up display technology and enhanced vision systems that improve pilot situational awareness and safety during extreme weather conditions and low visibility situations. Airlines are increasingly equipping their fleets with advanced enhanced vision system cameras and wearable heads-up displays to overcome challenging weather conditions during critical flight phases. The integration of sophisticated display technologies, including touch screens, enhanced vision systems, and advanced communication displays, is becoming increasingly crucial for modern commercial aircraft operations. This growth is reflective of the expanding display market for avionics applications.

Remaining Segments in Commercial Aircraft Avionics Market

The commercial aircraft avionics market encompasses several other crucial segments including Health Monitoring Systems, Communication and Navigation Systems, Cockpit Systems, and Other Subsystems. Health Monitoring Systems play a vital role in gathering real-time fleet data and enabling preventive maintenance measures. Communication and Navigation Systems ensure reliable connectivity and precise positioning during flights. Cockpit Systems provide essential flight instruments and controls for pilot operations. These segments collectively contribute to the overall advancement of aircraft safety, efficiency, and operational capabilities, with each segment addressing specific aspects of modern aviation requirements and regulatory compliance. The role of avionics subsystems is critical in ensuring the seamless integration of these technologies.

Segment Analysis: By Aircraft

Narrow-body Segment in Commercial Aircraft Avionics Market

The narrow-body segment dominates the commercial aircraft avionics market, commanding approximately 66% market share in 2024. This dominance is primarily driven by the increasing utilization of low-cost carriers and the segment's advantages such as low operation costs and fuel efficiency in short-haul routes. The narrow-body aircraft segment currently represents about 80% of the global passenger aircraft category, with airlines increasingly deploying these aircraft on long-haul routes of over 6-7 hours. Major manufacturers are focusing on improving passenger comfort through sophisticated cabin interior products, while airlines are expanding their fleets with new generation narrow-body aircraft to exploit new market opportunities and match the competencies of successive aircraft versions. The growth in this segment also impacts the aircraft computers market, as advanced computing systems are integral to modern avionics.

Wide-body Segment in Commercial Aircraft Avionics Market

The wide-body aircraft segment is projected to demonstrate the strongest growth trajectory in the commercial aircraft avionics market, with an expected growth rate of approximately 11% during 2024-2029. This remarkable growth is primarily driven by increasing demand within the Asia-Pacific region, which holds 41% of the delivery share, followed by significant contributions from the Middle East and Africa, Europe, and North America. Airlines are increasingly investing in wide-body aircraft to enhance their long-haul capabilities and meet growing passenger demands. The surge in international travel and the need for larger capacity aircraft on popular routes are further accelerating the adoption of wide-body aircraft, consequently driving the demand for sophisticated avionics systems.

Regional Jets in Commercial Aircraft Avionics Market

Regional jets play a crucial role in the commercial aircraft avionics market by serving short to medium-haul routes with capacity typically less than 100 passengers. These aircraft enable airlines to serve smaller and less congested airports while increasing flight frequency and connectivity. Manufacturers like Embraer, Bombardier, Airbus, Sukhoi, and COMAC are actively developing regional jets with advanced avionics systems to enhance operational efficiency and safety. The segment's impact on the market is particularly significant in developing regions where regional connectivity is expanding, and airlines are looking for cost-effective solutions to serve emerging routes.

Segment Analysis: By Fit

Line-Fit Segment in Commercial Aircraft Avionics Market

The line-fit segment dominates the commercial aircraft avionics market, commanding approximately 90% market share in 2024, while also maintaining the highest growth trajectory in the industry. This segment's prominence is primarily driven by the increasing global demand for new commercial aircraft, as airlines worldwide continue to expand their fleets to accommodate growing passenger traffic. Major aircraft manufacturers like Airbus and Boeing are ramping up their production rates to fulfill substantial order backlogs, directly benefiting the line-fit avionics segment. The integration of sophisticated avionics systems during initial aircraft assembly ensures optimal performance and compatibility while reducing installation complexities. Airlines' preference for new aircraft equipped with advanced avionics systems, offering enhanced safety features, improved fuel efficiency, and better operational performance, further strengthens this segment's market position. Recent developments include significant contracts between avionics manufacturers and major airlines for new aircraft deliveries, particularly in regions experiencing rapid aviation sector growth such as Asia-Pacific and the Middle East. The commercial aircraft electronic flight bag systems market is also benefiting from this trend, as these systems are increasingly integrated into new aircraft.

Retro-Fit Segment in Commercial Aircraft Avionics Market

The retrofit segment plays a crucial role in the commercial aircraft avionics market by addressing the modernization needs of existing aircraft fleets. This segment focuses on replacing or upgrading avionics systems in older aircraft to comply with new aviation regulations, enhance operational efficiency, and extend aircraft service life. Airlines are increasingly investing in retrofitting their existing fleets with advanced avionics systems to maintain competitiveness and meet evolving safety standards. The retrofit market is particularly active in regions with aging aircraft fleets, where complete fleet replacement may not be economically viable. Major avionics manufacturers are developing specialized retrofit solutions that offer modern capabilities while ensuring compatibility with existing aircraft systems. The segment is seeing increased activity in areas such as cockpit displays, navigation systems, and communication equipment upgrades, driven by regulatory requirements and the need for enhanced operational capabilities. The role of avionics subsystems is pivotal in these upgrades, ensuring seamless integration with existing aircraft technology.

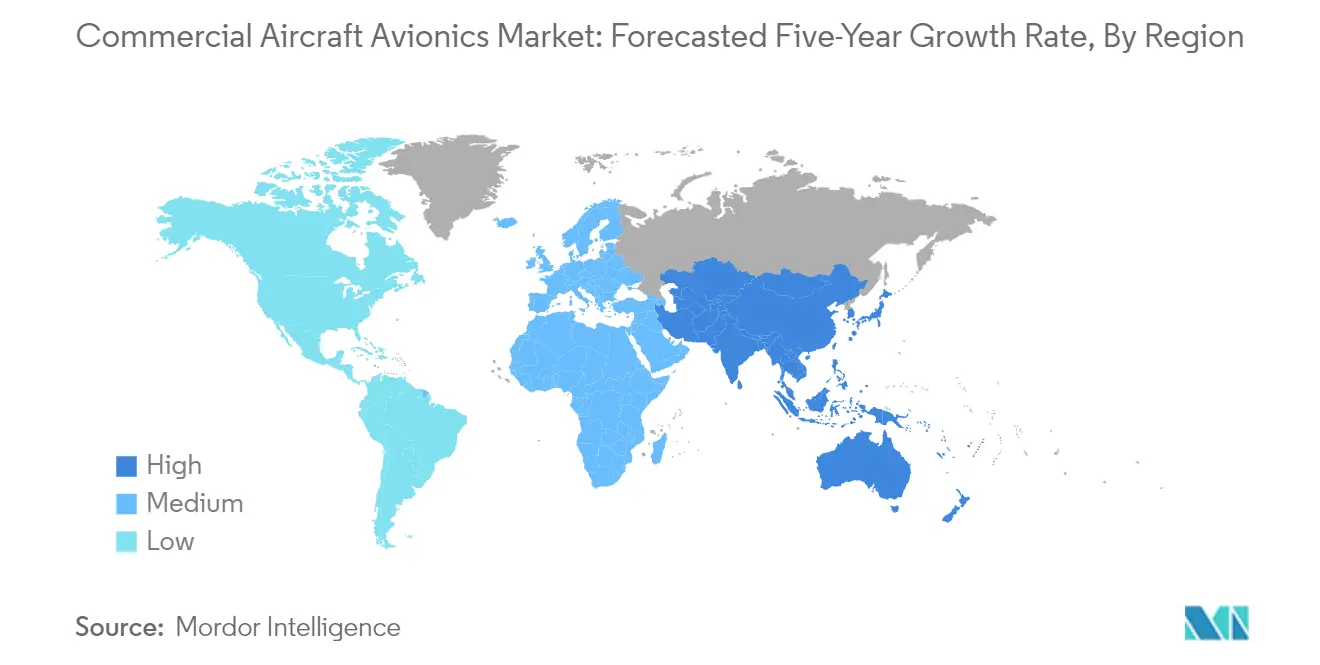

Commercial Aircraft Avionics Market Geography Segment Analysis

Commercial Aircraft Avionics Market in North America

North America represents a significant market for the global commercial aviation avionics market systems, driven by the presence of major aircraft manufacturers and airlines. The region's aviation sector demonstrates robust growth through fleet modernization programs and the increasing adoption of advanced avionics technologies. Both the United States and Canada have established strong aerospace manufacturing capabilities and research facilities, contributing to technological advancements in avionics market size systems.

Commercial Aircraft Avionics Market in United States

The United States dominates the North American commercial aircraft market share, supported by the presence of major aerospace manufacturers and a strong aviation infrastructure. The country's market leadership is driven by rising passenger traffic, rapid expansion of the aviation sector, and growing urbanization. Airlines based in the country are actively focusing on fleet expansion and adding new routes, with carriers like American Airlines and United Airlines making significant investments in new aircraft acquisitions. The US holds approximately 87% share of the North American market in 2024, reflecting its dominant position in the region's commercial aviation sector.

Commercial Aircraft Avionics Market Growth Trends in United States

The United States is experiencing the fastest growth in the North American region, with a projected growth rate of approximately 4% from 2024-2029. This growth is driven by the increasing adoption of advanced avionics suites and the rising procurement of next-generation in-flight entertainment systems. The US Federal Aviation Administration's ongoing modernization project of the National Airspace System (NextGen) is also contributing to market expansion. Airlines are increasingly investing in sophisticated avionics technologies to enhance operational efficiency and passenger experience while maintaining compliance with evolving aviation regulations.

Commercial Aircraft Avionics Market in Europe

Europe maintains a strong position in the global commercial aviation avionics market, characterized by the presence of major aerospace manufacturers and technological innovation centers. The region's market is driven by significant investments in research and development, particularly in countries like the United Kingdom, France, Germany, and Spain. The European aviation sector's focus on sustainable technologies and digitalization initiatives continues to shape the development of advanced avionics systems.

Commercial Aircraft Avionics Market in United Kingdom

The United Kingdom leads the European commercial avionics systems market, supported by its robust aerospace manufacturing capabilities and strong aviation infrastructure. The country's market position is strengthened by the presence of major airlines and their fleet modernization initiatives. Airlines like EasyJet and British Airways are actively expanding their fleets with next-generation aircraft equipped with advanced avionics systems. The UK accounts for approximately 25% of the European market in 2024, establishing its position as the largest market in the region.

Commercial Aircraft Avionics Market Growth Trends in France

France demonstrates the highest growth potential in the European region, with a projected growth rate of approximately 6% from 2024-2029. The country's growth is driven by the presence of major aerospace manufacturers and ongoing fleet modernization programs by airlines like Air France-KLM. The French aviation sector's commitment to technological innovation and sustainable aviation solutions is creating new opportunities for avionics system developments. The country's strong aerospace research and development capabilities, coupled with government support for aviation sector advancement, continue to drive market expansion.

Commercial Aircraft Avionics Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for the global aerospace defense avionics market size, characterized by rapid aviation sector growth and increasing investments in aerospace infrastructure. Countries like China, India, Japan, and South Korea are driving significant developments in the commercial aviation sector. The region's expanding middle class, growing air travel demand, and ambitious fleet expansion plans by major airlines are creating substantial opportunities for avionics system manufacturers. China emerges as the largest market in the region, while India shows the fastest growth potential, supported by their respective government initiatives and aviation sector developments.

Commercial Aircraft Avionics Market in Latin America

The Latin American commercial aircraft avionics market is experiencing steady growth, driven by increasing air passenger traffic and fleet modernization initiatives. Mexico and Brazil are the key markets in the region, with Brazil emerging as the largest market while Mexico demonstrates the strongest growth potential. Airlines across the region are focusing on upgrading their existing fleets with advanced avionics systems to enhance operational efficiency and comply with international aviation standards.

Commercial Aircraft Avionics Market in Middle East & Africa

The Middle East & Africa region shows significant potential in the commercial aircraft avionics market, driven by ambitious aviation sector expansion plans and increasing investments in aerospace infrastructure. The United Arab Emirates, Saudi Arabia, and Qatar are key markets in the region, with the UAE emerging as the largest market while Saudi Arabia shows the strongest growth potential. The region's position as a global aviation hub and the presence of major international carriers continue to drive demand for advanced avionics systems.

Get Analysis on Important Geographic Markets

Download PDF

Commercial Aircraft Avionics Systems Industry Overview

Top Companies in Commercial Aircraft Avionics Market

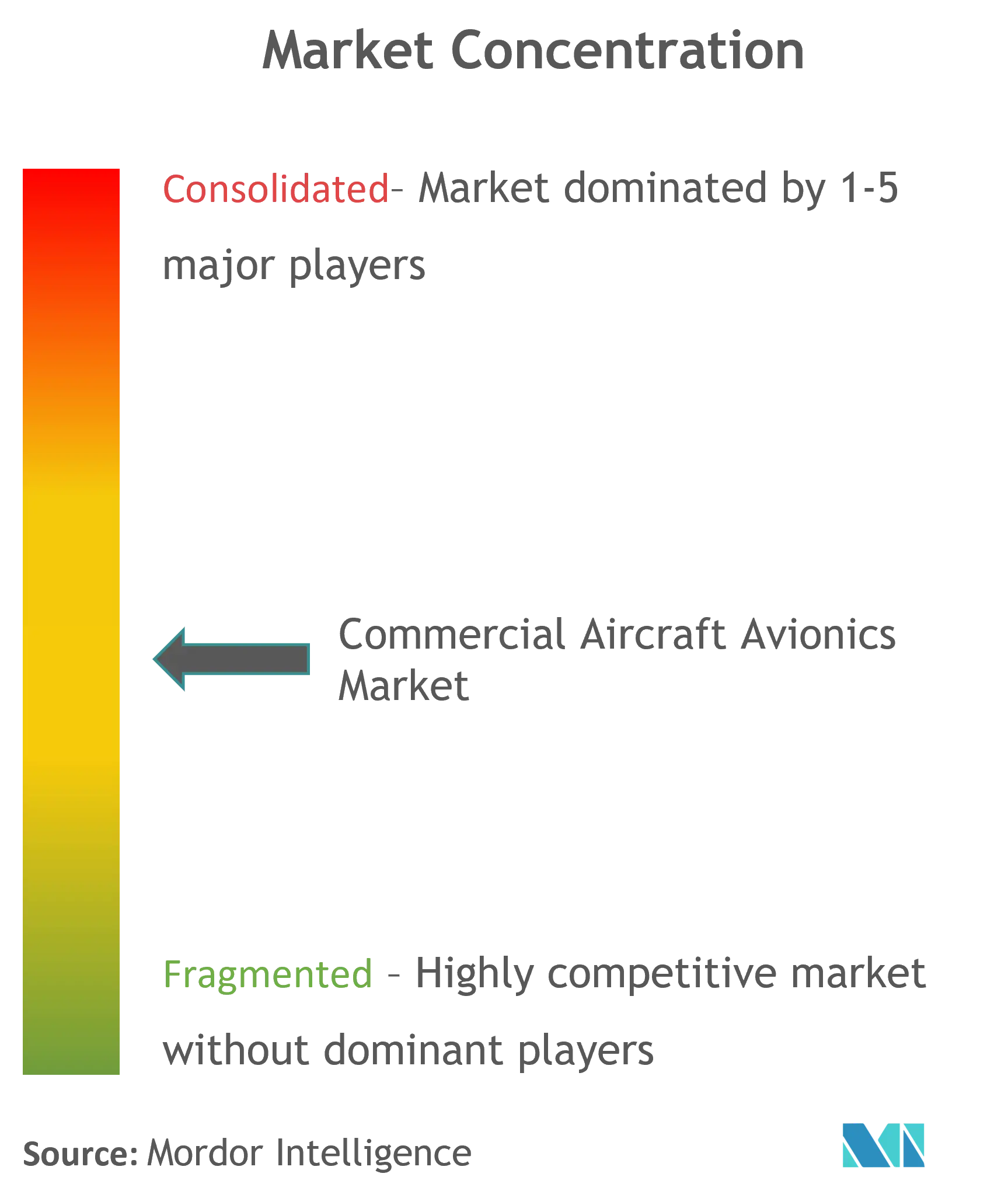

The commercial avionics market is led by established players like RTX Corporation, General Electric Company, Honeywell International, BAE Systems, and Thales Group, who collectively dominate the industry through their comprehensive product portfolios and global presence. These companies are heavily investing in research and development to develop next-generation avionics systems incorporating advanced technologies like artificial intelligence, enhanced flight management capabilities, and improved visualization systems. The industry witnesses continuous product innovation focused on improving operational efficiency, safety features, and sustainability aspects of aircraft operations. Companies are expanding their market presence through strategic partnerships with aerospace manufacturers, airlines, and maintenance providers while also pursuing regional expansion opportunities in emerging aviation markets. Operational agility is demonstrated through the development of integrated avionics solutions that can be both line-fitted in new aircraft and retrofitted in existing fleets, allowing companies to serve both market segments effectively.

Consolidated Market with High Entry Barriers

The commercial aircraft avionics market exhibits a highly consolidated structure dominated by large multinational conglomerates with diverse aerospace and defense portfolios. These established players leverage their extensive research capabilities, manufacturing infrastructure, and long-standing relationships with aircraft manufacturers to maintain their market positions. The market's high entry barriers stem from substantial capital requirements, complex certification processes, and the need for specialized technological expertise, which makes it challenging for new entrants to establish themselves without significant backing or strategic partnerships.

The industry landscape is characterized by strategic mergers and acquisitions aimed at expanding technological capabilities and market reach. Companies are increasingly focusing on vertical integration to strengthen their supply chain control and enhance their ability to deliver integrated avionics solutions. Regional players typically operate in specific market niches or serve as specialized suppliers to larger conglomerates, while local companies often focus on maintenance, repair, and overhaul services for existing systems rather than competing in primary equipment manufacturing.

Innovation and Integration Drive Future Success

For incumbent players to maintain and expand their market share, continuous investment in technological innovation and system integration capabilities is crucial. Companies must focus on developing more efficient, lighter, and more reliable avionics systems while ensuring seamless integration with existing aircraft platforms. Success in the market increasingly depends on the ability to offer comprehensive solutions that address emerging requirements for enhanced connectivity, improved safety features, and reduced environmental impact while maintaining competitive pricing structures.

Contenders looking to gain ground in the avionics industry need to identify and exploit specific market niches where they can establish technological leadership or cost advantages. This could involve focusing on particular aircraft segments, developing specialized subsystems, or innovating in emerging areas like electric aircraft avionics. The regulatory environment plays a crucial role in shaping market opportunities, with companies needing to maintain close alignment with evolving aviation safety standards and certification requirements. End-user concentration in the form of major airlines and aircraft manufacturers significantly influences market dynamics, making strong customer relationships and reliable after-sales support essential for long-term success.

Commercial Aircraft Avionics Systems Market Leaders

-

Honeywell International Inc.

-

General Electric Company

-

Raytheon Technologies Corporation

-

THALES

-

Safran

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Commercial Aircraft Avionics Systems Market News

- June 2023: United Airlines and Panasonic Avionics Corporation signed an agreement for Panasonic's new Astrova in-flight engagement (IFE) solution, making United Airlines the first customer for this IFE in the United States. The airlines plan to install this IFE solution on new Boeing 787 and Airbus A321XLR starting in 2025. With this agreement, the United Airlines program represents the largest-ever investment in Panasonic Avionics' IFE by any airline.

- July 2022: Universal Avionics Systems Corporation, a subsidiary of Elbit Systems Ltd., received a contract worth USD 33 million from AerSale Corporation to supply Enhanced Flight Vision Systems (EFVS) for Boeing 737NG aircraft. The contract will be executed through 2023.

Commercial Aircraft Avionics Systems Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Subsystem

- 5.1.1 Health Monitoring Systems

- 5.1.2 Flight Management and Control Systems

- 5.1.3 Communication and Navigation

- 5.1.4 Cockpit Systems

- 5.1.5 Visualizations and Display Systems

- 5.1.6 Other Subsystems

-

5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.2.3 Regional Aircraft

-

5.3 Fit

- 5.3.1 Linefit

- 5.3.2 Retrofit

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 United Arab Emirates

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 Qatar

- 5.4.4.4 Rest of Middle-East and Africa

- 5.4.5 Latin America

- 5.4.5.1 Brazil

- 5.4.5.2 Mexico

- 5.4.5.3 Rest of Latin America

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Share Analysis

-

6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 General Electric Company

- 6.2.3 THALES

- 6.2.4 BAE Systems plc

- 6.2.5 Cobham Limited

- 6.2.6 Esterline Technologies Corporation (TransDigm Group)

- 6.2.7 Diehl Stiftung & Co. KG

- 6.2.8 L3Harris Technologies Inc.

- 6.2.9 Raytheon Technologies Corporation

- 6.2.10 Meggitt PLC

- 6.2.11 Teledyne Technologies Incorporated

- 6.2.12 Safran

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Commercial Aircraft Avionics Systems Industry Segmentation

Avionics is an assembly of electronics subsystems integrated onboard an aircraft to carry out several mission and flight management tasks. These systems include engine controls, flight control systems, navigation, communications, flight recorders, lighting systems, fuel systems, electro-optic (EO/IR) systems, weather radar, and performance monitoring systems. The scope of the study is exclusive of freighter aircraft, military aircraft, business jets, and other private-owned, chartered, and unscheduled aircraft.

The commercial aircraft avionics market is segmented by subsystem, aircraft type, fit, and geography. By subsystem, the market is segmented into health monitoring systems, flight management and control systems, communication and navigation, cockpit systems, visualizations and display systems, and other subsystems. The other subsystems include emergency systems, fire safety systems, electronic flight bags (EFBs), and weather systems. By aircraft type, the market is segmented into narrowbody, widebody, and regional jet. By fit, the market is segmented into line fit and retrofit. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa.

The market sizing and forecasts have been provided in value (USD).

| Subsystem | Health Monitoring Systems | ||

| Flight Management and Control Systems | |||

| Communication and Navigation | |||

| Cockpit Systems | |||

| Visualizations and Display Systems | |||

| Other Subsystems | |||

| Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Aircraft | |||

| Fit | Linefit | ||

| Retrofit | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle-East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle-East and Africa | |||

| Latin America | Brazil | ||

| Mexico | |||

| Rest of Latin America | |||

Need A Different Region or Segment?

Customize Now

Commercial Aircraft Avionics Systems Market Research FAQs

How big is the Commercial Aircraft Avionics Market?

The Commercial Aircraft Avionics Market size is expected to reach USD 35.87 billion in 2025 and grow at a CAGR of 4.17% to reach USD 43.99 billion by 2030.

What is the current Commercial Aircraft Avionics Market size?

In 2025, the Commercial Aircraft Avionics Market size is expected to reach USD 35.87 billion.

Who are the key players in Commercial Aircraft Avionics Market?

Honeywell International Inc., General Electric Company, Raytheon Technologies Corporation, THALES and Safran are the major companies operating in the Commercial Aircraft Avionics Market.

Which is the fastest growing region in Commercial Aircraft Avionics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Commercial Aircraft Avionics Market?

In 2025, the North America accounts for the largest market share in Commercial Aircraft Avionics Market.

What years does this Commercial Aircraft Avionics Market cover, and what was the market size in 2024?

In 2024, the Commercial Aircraft Avionics Market size was estimated at USD 34.37 billion. The report covers the Commercial Aircraft Avionics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Commercial Aircraft Avionics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Commercial Aircraft Avionics Market Research

Mordor Intelligence provides a comprehensive analysis of the commercial aviation avionics market. With decades of expertise in researching and consulting for aerospace manufacturers, our detailed report examines avionics systems across various commercial aircraft platforms. This includes aircraft flight management systems, aircraft air management systems, and aircraft emergency systems. The analysis covers developments in global aerospace defense avionics, focusing particularly on commercial aircraft avionics systems and emerging avionics subsystems.

Stakeholders receive valuable insights through our global commercial aviation avionics market forecast and detailed industry analysis. This information is available in an easy-to-read report PDF format for download. The report offers comprehensive coverage of trends in aircraft software testing and development, commercial aircraft electronic flight bag systems, and innovations in aircraft health monitoring system. Our analysis provides avionics systems manufacturers with actionable intelligence on global defense avionics opportunities. It also tracks developments in the helicopter avionics and rotorcraft avionics segments. The report's projections on avionics market size and detailed examination of avionics industry dynamics enable informed decision-making for industry participants.