| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 43.50 Billion |

| Market Size (2030) | USD 54.62 Billion |

| CAGR (2025 - 2030) | 4.66 % |

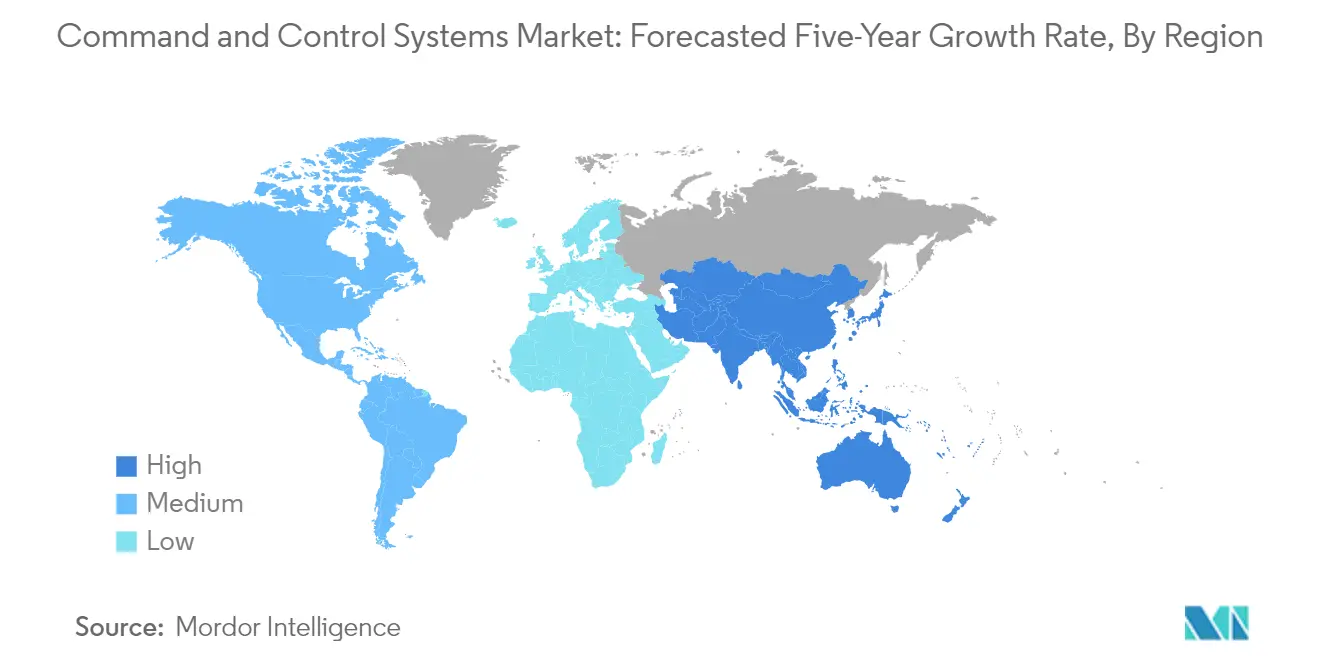

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Command and Control Systems Market Analysis

The Command And Control Systems Market size is estimated at USD 43.50 billion in 2025, and is expected to reach USD 54.62 billion by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).

The command and control systems industry continues to evolve amid increasing global security challenges and technological advancements. According to the International Institute for Strategic Studies (IISS), global defense expenditure reached USD 1.92 trillion in 2021, representing a 3.4% increase over previous levels, indicating strong investment in military capabilities, including command and control systems. The industry is witnessing a significant shift toward integrated solutions that can handle complex battlefield scenarios while providing enhanced situational awareness and decision-making capabilities. This transformation is particularly evident in the increasing adoption of network-centric warfare concepts, where interconnected systems enable real-time information sharing and coordinated responses across multiple platforms.

The integration of advanced technologies is reshaping the command and control systems landscape, with artificial intelligence, quantum communications, and big data analytics emerging as key enablers of next-generation capabilities. Military organizations are increasingly focusing on developing open architecture command and control systems that enable easy introduction of new interfaces and modes of interaction. This approach facilitates the seamless integration of emerging technologies while ensuring interoperability between different platforms and systems. The industry has witnessed significant developments in automation capabilities, with reports indicating that automation has helped reduce radar operator workload by as much as 50%, enabling operators to focus more on critical surveillance missions.

A notable trend in the market is the growing emphasis on multi-domain command and control operations, which enable military forces to conduct operations across multiple domains and contested spaces simultaneously. The industry is witnessing increased investment in systems that can integrate vast, diverse, and distributed forces of platforms, sensors, personnel, and networks. This evolution is particularly evident in the development of sophisticated battle management systems that can coordinate actions across land, air, sea, space, and cyber domains. Companies are focusing on developing solutions that enable forces to overcome adversary strengths through the combined employment of multi-domain formations and convergence of capabilities across domains.

The industry is experiencing a surge in collaborative development efforts and strategic partnerships aimed at enhancing command and control capabilities. In February 2022, Systematic released version 3.2 of its SitaWare Edge and SitaWare Frontline software, introducing enhanced mobile battle management capabilities for dismounted and mounted commanders. The market is also witnessing increased focus on developing protected technologies such as quantum cryptography protected communications, reflecting the growing importance of secure command and control systems in modern military operations. These developments are accompanied by efforts to standardize interfaces and protocols, ensuring seamless integration of new capabilities while maintaining backward compatibility with existing systems.

Command and Control Systems Market Trends

Growth in Defense Spending

The global defense expenditure has witnessed substantial growth in recent years, reaching USD 2.1 trillion in 2021, representing a significant increase from previous years. This surge in military spending is primarily attributed to profound changes in the international strategic landscape, where the configuration of international security systems has been undermined by growing hegemonism, unilateralism, and power politics. The increasing uncertainties in territorial rights, political tensions, and the quest for universal dominance among military powerhouses have emerged as major factors disturbing the geopolitical scenario, compelling nations to allocate substantial budgets toward military modernization and capability enhancement.

The robust defense spending has particularly manifested in the procurement of sophisticated command and control systems, as evidenced by recent major contracts and partnerships. For instance, in October 2023, Elbit Systems secured a significant contract worth USD 170 million to participate as an integration partner in the Swedish Army digitalization program LSS Mark, focusing on the integration and maintenance of advanced command and control systems across various platforms. Similarly, in January 2024, Northrop Grumman Corporation and Mitsubishi Electric Corporation established a strategic partnership to develop integrated air and missile defense capabilities for Japan's ground-based systems, demonstrating the continued investment in enhancing military command and control systems capabilities through international collaboration.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Focus on Modernization of Warfighting Capabilities

The modernization of warfighting capabilities has become imperative for militaries worldwide as they adapt to evolving threats and technological advancements. Military forces are increasingly focusing on conducting operations across multiple domains and contested spaces to overcome adversary strengths through the combined employment of multi-domain formations. This has led to significant investments in integrating vast, diverse, and distributed forces of platforms, sensors, personnel, and networks to meet the growing requirements of modern warfare. The emphasis on modernization is particularly evident in the integration of artificial intelligence and machine-to-machine communication, although managing information flows to ensure that information inputs do not slow down decision-making capabilities remains a crucial consideration.

Recent developments highlight the accelerating pace of military modernization efforts globally. For instance, Lockheed Martin Australia's partnership with the Royal Australian Air Force (RAAF) and Defence Science and Technology Group (DSTG) in August 2022 exemplifies the growing focus on leveraging artificial intelligence to support rapid decision-making at tactical levels of the command and control systems market across various domains. The modernization initiatives extend beyond traditional warfare domains, encompassing cyber capabilities and electronic warfare systems. Military organizations are increasingly investing in protective technologies such as quantum cryptography-protected communications and developing sophisticated command and control systems market that can effectively coordinate air defense activities while maintaining interoperability with various platforms and systems.

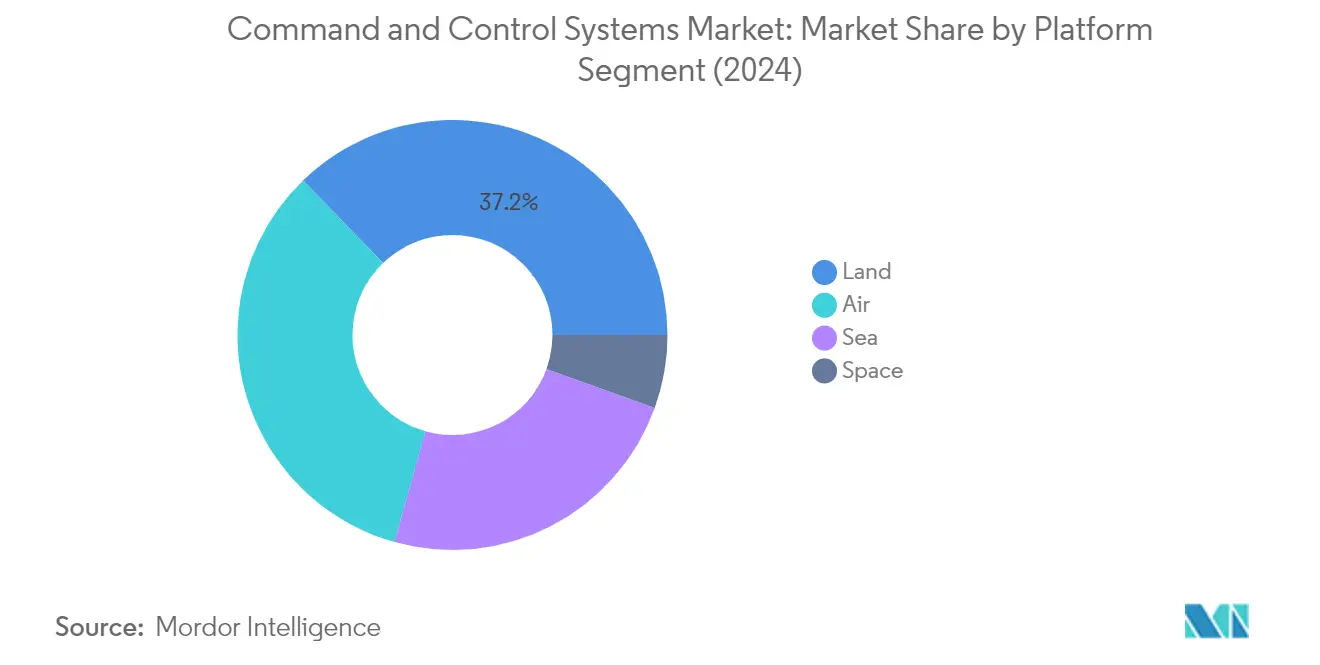

Segment Analysis: Platform

Land Segment in Command and Control Systems Market

The Land segment dominates the Command and Control Systems Market, holding approximately 37% market share in 2024. This significant market position is driven by the increasing focus on modernizing ground-based command and control systems capabilities across various military forces globally. The segment's prominence is reinforced by substantial investments in battlefield management systems, tactical communications infrastructure, and the integration of advanced technologies for ground forces. Military organizations worldwide are implementing sophisticated land-based C2 systems to enhance situational awareness, improve coordination between ground units, and enable faster decision-making in complex battlefield scenarios. The integration of artificial intelligence and machine learning capabilities in land-based C2 systems has further strengthened this segment's market position, allowing for more efficient processing of battlefield data and enhanced tactical response capabilities.

Space Segment in Command and Control Systems Market

The Space segment is emerging as the fastest-growing sector in the Command and Control Systems Market, with an expected growth rate of approximately 7% during the forecast period 2024-2029. This remarkable growth is primarily driven by increasing investments in space-based defense capabilities and satellite communications systems. The segment is witnessing rapid technological advancements in satellite-based command and control systems, particularly in areas such as space situational awareness and orbital warfare capabilities. Military organizations are increasingly recognizing the strategic importance of space-based C2 systems in modern warfare, leading to enhanced investments in satellite communication networks, space surveillance systems, and integrated space-ground command architectures. The growing emphasis on developing resilient space-based C2 capabilities to counter emerging threats in the space domain is further accelerating the segment's growth.

Remaining Segments in Platform Segmentation

The Air and Sea segments continue to play crucial roles in the command and control systems market, each bringing unique capabilities and requirements to military operations. The Air segment focuses on advanced airborne early warning systems, tactical air control, and integrated air defense networks, while maintaining crucial links between aerial assets and ground control stations. The Sea segment emphasizes maritime domain awareness, naval combat management systems, and integrated fleet command capabilities, which are particularly important in maintaining maritime security and conducting naval operations. Both segments are experiencing continuous technological upgrades with the integration of advanced sensors, communication systems, and automated decision support tools, reflecting the evolving nature of modern military operations and the increasing need for interoperability across different platforms.

Command And Control Systems Market Geography Segment Analysis

Command and Control Systems Market in Asia-Pacific

The Asia-Pacific region represents a dynamic marketplace for the command and control systems market, characterized by diverse military modernization initiatives and growing security concerns. Countries like China, India, Japan, and South Korea are making significant investments in upgrading their military capabilities with advanced C2 systems. The region faces various security challenges, including territorial disputes, maritime security concerns, and evolving threat landscapes, driving the demand for sophisticated command and control systems. Many countries in the region are focusing on developing indigenous capabilities while maintaining strategic partnerships with global defense contractors.

Command and Control Systems Market in China

China maintains its position as the dominant force in the Asia-Pacific command and control systems market, driven by its comprehensive military modernization program and increasing focus on network-centric warfare capabilities. The country has made substantial investments in developing indigenous C2 systems capabilities, particularly in areas such as artificial intelligence integration and multi-domain operations. With approximately 35% market share in 2024, China's command and control systems market is supported by a robust domestic defense industrial base and significant research and development initiatives. The country's focus on military modernization encompasses various domains, including land, air, sea, and space, with particular emphasis on integrated command and control networks.

Command and Control Systems Market in Australia

Australia emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's robust growth is driven by its comprehensive defense modernization initiatives and increasing focus on enhancing its military capabilities in response to regional security dynamics. Australia's strategic partnerships with key defense contractors and its commitment to developing advanced military capabilities have positioned it as a significant player in the regional command and control systems market. The country's investment in next-generation command and control systems spans across its army, navy, and air force, with particular emphasis on integrated battle management systems and joint operations capabilities.

Command and Control Systems Market in Latin America

The Latin American command and control systems market is characterized by modernization efforts across several countries, with varying degrees of investment and technological advancement. The region's military forces are increasingly focusing on enhancing their command and control systems capabilities to address security challenges, including border control, counter-narcotics operations, and internal security. Countries such as Brazil, Mexico, and Chile are leading the regional modernization efforts, with significant investments in upgrading their military communication and control infrastructure.

Command and Control Systems Market in Brazil

Brazil stands as the largest market for command and control systems in Latin America, commanding approximately 28% of the regional market share in 2024. The country's dominant position is supported by its comprehensive military modernization programs and significant investments in indigenous defense capabilities. Brazil's focus on developing advanced command and control systems is evident through its various military programs, including the SISFRON border monitoring system and other strategic defense initiatives. The country's defense industry has established strong partnerships with international defense contractors while simultaneously developing local manufacturing capabilities.

Command and Control Systems Market in Brazil - Growth Trajectory

Brazil continues to demonstrate strong growth potential, with a projected growth rate of approximately 5% during 2024-2029. The country's robust growth trajectory is supported by ongoing military modernization programs and an increasing focus on enhancing its command and control systems capabilities across all military branches. Brazil's investment in advanced technologies and its commitment to developing indigenous defense capabilities continue to drive market expansion. The country's strategic focus on improving its military communication and control infrastructure, coupled with increasing defense budget allocations, positions it for sustained growth in the command and control systems market.

Command and Control Systems Market in Middle East

The Middle Eastern command and control systems market is characterized by significant investments in military modernization and the adoption of advanced defense technologies. The region's geopolitical dynamics and security challenges have led to an increased focus on enhancing military capabilities across all domains. Countries such as Saudi Arabia, Israel, and the UAE are making substantial investments in modernizing their command and control systems infrastructure, with particular emphasis on integrated air defense systems and network-centric warfare capabilities.

Command and Control Systems Market in Saudi Arabia

Saudi Arabia maintains its position as the largest market for command and control systems in the Middle East. The kingdom's dominant market position is driven by its comprehensive military modernization programs and significant investments in advanced defense technologies. Saudi Arabia's focus on developing robust command and control systems capabilities spans across its land, air, and naval forces, supported by strategic partnerships with international defense contractors and a growing emphasis on local manufacturing capabilities through its Vision 2030 initiative.

Command and Control Systems Market in Israel

Israel emerges as the fastest-growing market in the Middle East region. The country's growth is driven by its strong focus on technological innovation and indigenous development of advanced military systems. Israel's robust defense industrial base and expertise in developing sophisticated command and control systems continue to strengthen its market position. The country's emphasis on developing cutting-edge military technologies and its experience in operational requirements have established it as a significant player in the regional market.

Command and Control Systems Market in Africa

The African command and control systems market is characterized by varying levels of military modernization across different regions, with North African countries generally leading in terms of defense investments. The market is driven by requirements for border security, counter-terrorism operations, and maritime surveillance capabilities. Algeria emerges as the largest market in the region, supported by its significant defense budget and comprehensive military modernization programs. Tunisia represents the fastest-growing market, driven by its increasing focus on enhancing military capabilities and modernizing its command and control systems infrastructure. The region's market dynamics are influenced by both internal security challenges and the need to protect maritime interests, particularly in coastal nations.

Get Analysis on Important Geographic Markets

Download PDF

Command and Control Systems Industry Overview

Top Companies in Command and Control Systems Market

The command and control systems market features prominent players like IAI, L3Harris Technologies, Leonardo, Elbit Systems, and Kongsberg leading the industry through continuous innovation and strategic initiatives. Companies are heavily investing in artificial intelligence integration, multi-domain command capabilities, and network-centric warfare solutions to maintain a competitive advantage. The focus on developing sophisticated cyber warfare capabilities and quantum communications demonstrates the industry's commitment to technological advancement. Market leaders are expanding their geographical presence through strategic partnerships and collaborations, particularly in emerging defense markets across the Asia Pacific and Middle East regions. Companies are also emphasizing the development of modular and scalable C2 systems that can be integrated with existing military infrastructure while ensuring interoperability across different platforms and domains.

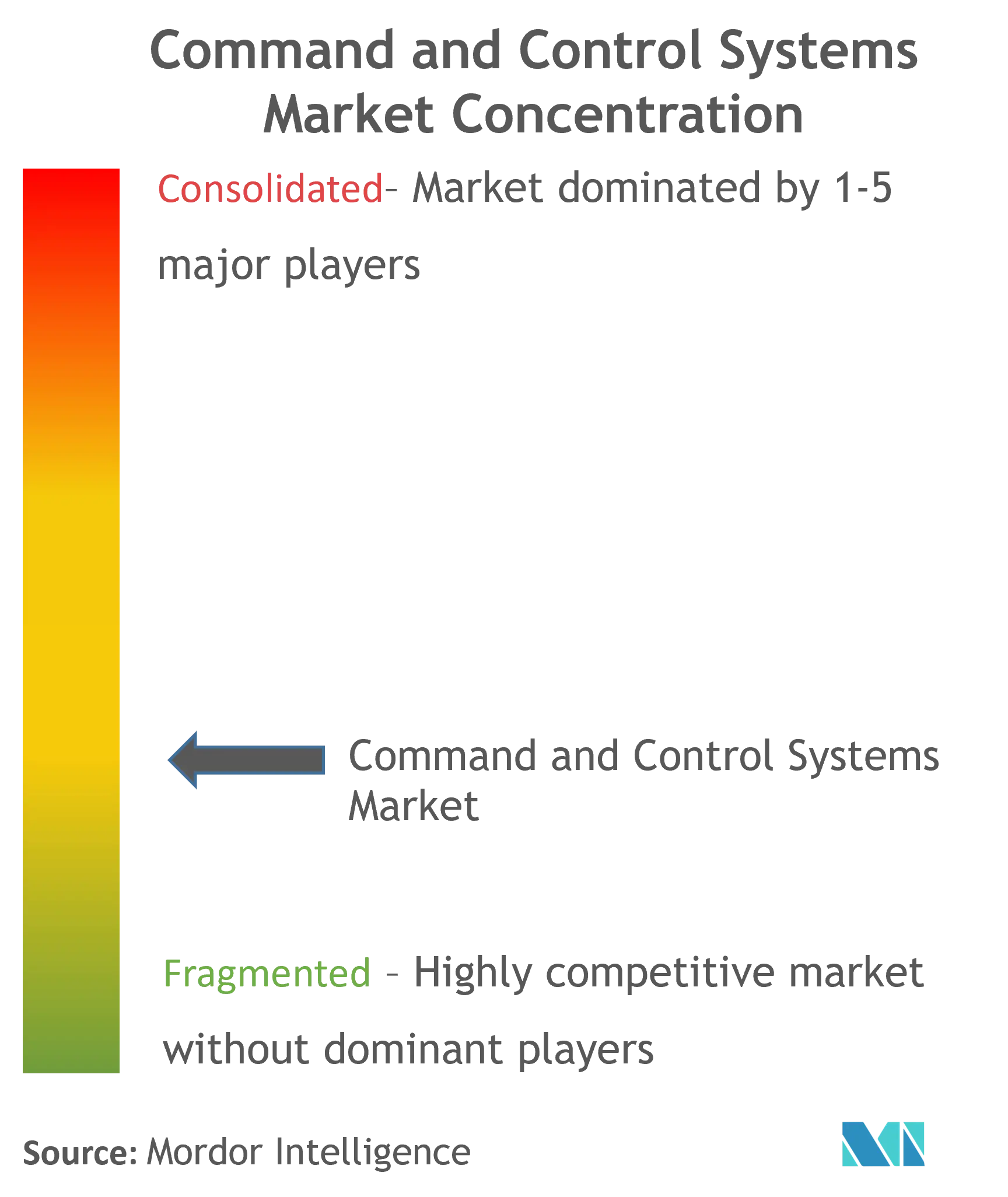

Fragmented Market with Strong Regional Players

The command and control systems market exhibits a fragmented structure with a mix of global defense conglomerates and specialized regional players competing for market share. Major defense contractors maintain their market positions through extensive R&D capabilities, established relationships with military organizations, and comprehensive product portfolios spanning multiple defense domains. Regional players, particularly in countries like Turkey, Israel, and South Korea, have carved out strong positions in their domestic markets through close alignment with national defense priorities and specialized technological expertise.

The industry is characterized by strategic partnerships and joint ventures rather than outright acquisitions, as companies seek to combine complementary capabilities and access new markets while managing technological sovereignty concerns. Defense contractors are increasingly focusing on developing indigenous capabilities through technology transfer agreements and local manufacturing partnerships, particularly in emerging markets with growing defense modernization programs. The market structure is further influenced by government policies promoting domestic defense industrial capabilities, leading to the emergence of new competitive dynamics and partnership models.

Innovation and Adaptability Drive Market Success

Success in the command and control systems market increasingly depends on companies' ability to deliver integrated solutions that address the evolving nature of modern warfare. Incumbent players must focus on developing flexible, scalable architectures that can accommodate rapid technological changes while maintaining robust cybersecurity features. Companies need to demonstrate expertise in emerging technologies like artificial intelligence, big data analytics, and quantum computing while maintaining strong relationships with military decision-makers and understanding evolving operational requirements.

Market contenders can gain ground by focusing on specialized capabilities in areas like cyber warfare, autonomous systems integration, or specific domain expertise while building strategic partnerships with established players. The highly regulated nature of the defense industry creates significant barriers to entry, making it essential for new entrants to develop unique technological capabilities or cost advantages. Success also depends on companies' ability to navigate complex procurement processes, maintain long-term customer relationships, and adapt to changing geopolitical dynamics that influence defense spending patterns and technological priorities.

Command and Control Systems Market Leaders

-

Lockheed Martin Corporation

-

L3Harris Technologies Inc.

-

BAE Systems plc

-

RTX Corporation

-

THALES

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Command and Control Systems Market News

- February 2024: The Defense Information Systems Agency awarded Data Computer Corporation of America a five-year contract with a maximum value of USD 37 million. It is to provide a variety of support services like systems and software engineering and cybersecurity for DISA’s command and control portfolio capabilities.

- January 2022: THALES was awarded a 10-year contract to provide logistics support to the French military's national air command and control system (SCCOA). Under the contract, the company will ensure that the main components of the air surveillance system are sustained to meet the needs of the French armed forces.

Command and Control Systems Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Platform

- 5.1.1 Land

- 5.1.2 Air

- 5.1.3 Sea

- 5.1.4 Space

-

5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 South Africa

- 5.2.5.3 Saudi Arabia

- 5.2.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 THALES

- 6.2.3 General Dynamics Corporation

- 6.2.4 L3Harris Technologies, Inc.

- 6.2.5 BAE Systems plc

- 6.2.6 Honeywell International Inc.

- 6.2.7 Saab AB

- 6.2.8 CACI International Inc

- 6.2.9 Kratos Defense & Security Solutions, Inc.

- 6.2.10 Leonardo S.p.A

- 6.2.11 Lockheed Martin Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Command and Control Systems Industry Segmentation

Command and control systems are operational architectures that include different computer systems, such as hardware, software, interfaces, and stored procedures. These systems help with situational awareness, intelligence support, and deployment readiness. They also provide accurate, real-time information that helps in combat operations.

The command-and-control systems market is segmented based on platform and geography. By platform, the market is segmented into land, air, naval, and space. The report also covers the market sizes and forecasts for the command and control systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Platform | Land | ||

| Air | |||

| Sea | |||

| Space | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Saudi Arabia | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Command and Control Systems Market Research FAQs

How big is the Command And Control Systems Market?

The Command And Control Systems Market size is expected to reach USD 43.50 billion in 2025 and grow at a CAGR of 4.66% to reach USD 54.62 billion by 2030.

What is the current Command And Control Systems Market size?

In 2025, the Command And Control Systems Market size is expected to reach USD 43.50 billion.

Who are the key players in Command And Control Systems Market?

Lockheed Martin Corporation, L3Harris Technologies Inc., BAE Systems plc, RTX Corporation and THALES are the major companies operating in the Command And Control Systems Market.

Which is the fastest growing region in Command And Control Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Command And Control Systems Market?

In 2025, the North America accounts for the largest market share in Command And Control Systems Market.

What years does this Command And Control Systems Market cover, and what was the market size in 2024?

In 2024, the Command And Control Systems Market size was estimated at USD 41.47 billion. The report covers the Command And Control Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Command And Control Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Command And Control Systems Market Research

Mordor Intelligence brings extensive expertise in analyzing the command and control systems industry. We offer comprehensive insights into this critical sector. Our detailed analysis covers the evolution of C2 systems and their growing importance in modern operations. The research encompasses various aspects of command & control systems. This includes technological advancements, operational implementations, and emerging trends in command centre software applications. Our expert analysts provide in-depth coverage of both military command and control systems and satellite command and control systems. This ensures a complete understanding of the entire ecosystem.

Stakeholders gain valuable insights through our meticulously researched report, available as an easy-to-download PDF. It examines the complex dynamics of the command and control systems market. The analysis provides a detailed evaluation of various command and control system implementations across different sectors, including defense, aerospace, and civilian applications. Our report offers actionable intelligence on market dynamics, technological innovations, and growth opportunities within the command and control systems industry. This enables decision-makers to make informed strategic choices based on robust data and expert analysis.