Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

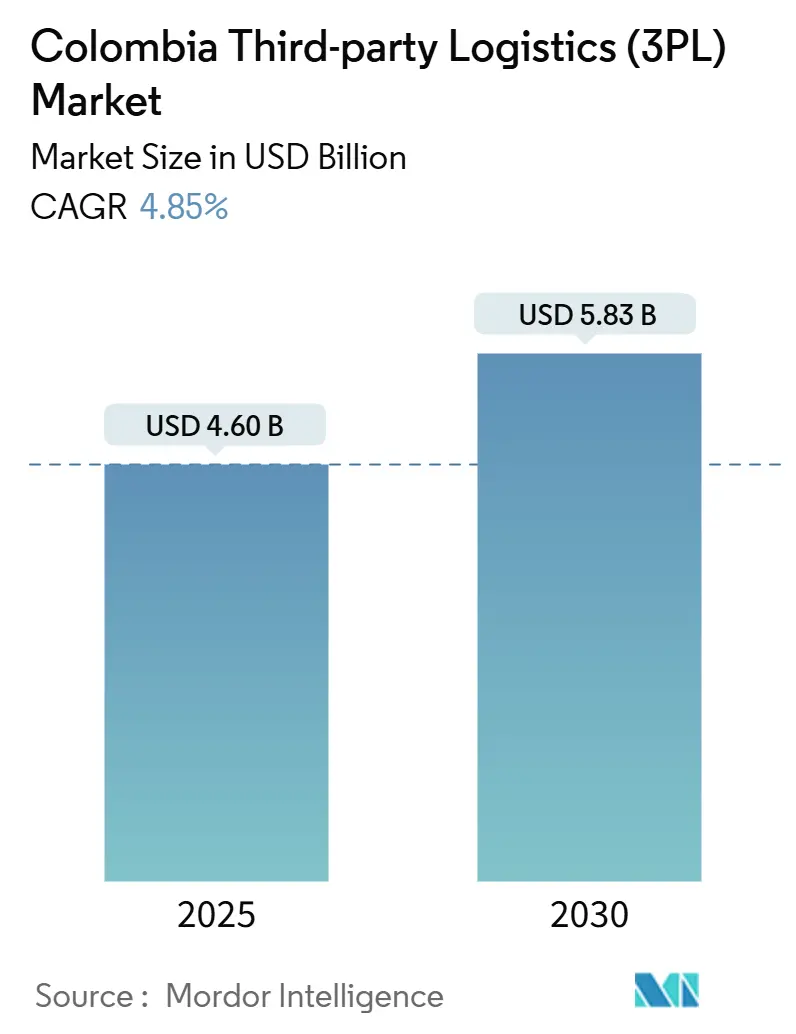

| Market Size (2025) | USD 4.60 Billion |

| Market Size (2030) | USD 5.83 Billion |

| Growth Rate (2025 - 2030) | 4.85% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Colombia Third-party Logistics (3PL) Market Analysis by Mordor Intelligence

The Colombia Third-party Logistics Market size is estimated at USD 4.60 billion in 2025, and is expected to reach USD 5.83 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030). Widening investment in port and rail corridors, faster e-commerce adoption in Bogotá and Medellín, and an accelerating pivot toward near-shoring all underpin this steady expansion. Large retailers are now demanding real-time inventory visibility, pushing 3PLs to upgrade warehouse management platforms and radio-frequency identification capability. At the same time, cold-chain operators are scaling up to move avocados and specialty pharmaceuticals, while hybrid logistics networks are emerging to balance cost efficiency with tighter service-level commitments. Infrastructure gaps and driver shortages continue to pose headwinds, yet high-impact projects such as the La Dorada–Chiriguaná rail upgrade and new Pacific port terminals are gradually easing structural constraints for the Colombia Third Party Logistics (3PL) market.

Key Report Takeaways

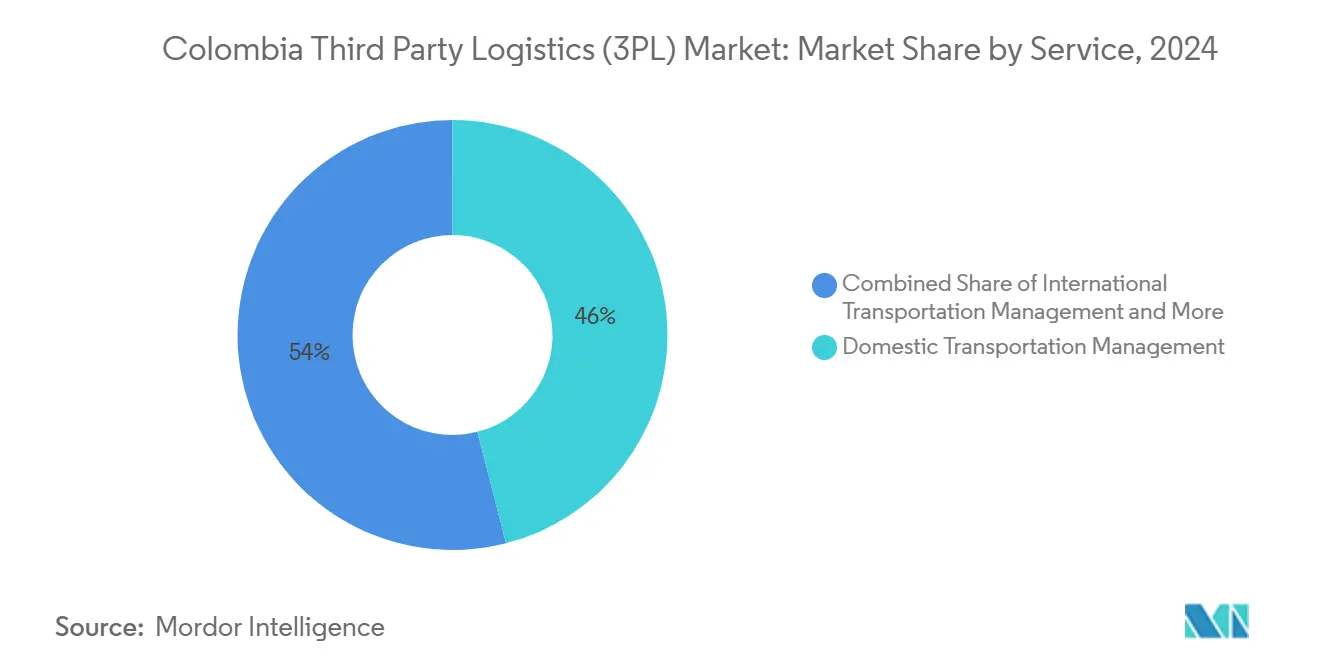

- By service, Domestic Transportation Management led with 46% of the Colombia Third Party Logistics (3PL) market share in 2024. The Colombia Third Party Logistics (3PL) market for Value-Added Warehousing and Distribution is projected to expand at a 6.05% CAGR between 2025-2030.

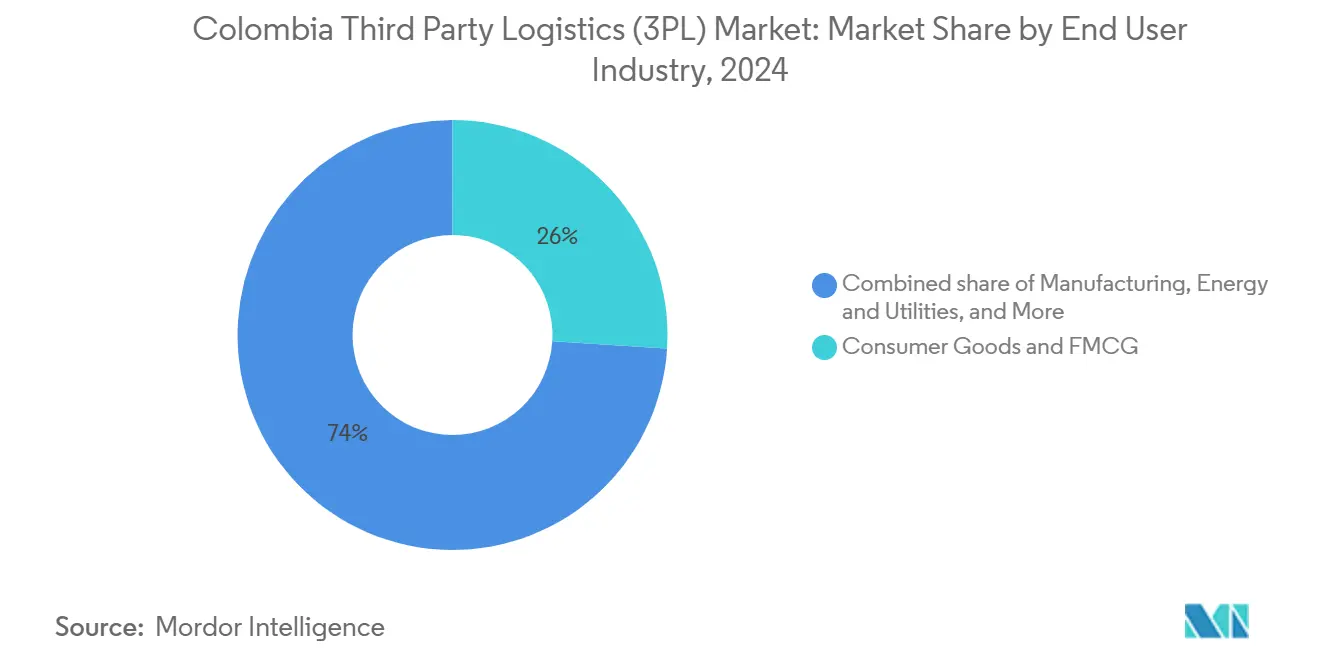

- By end-user industry, Consumer Goods and FMCG held 26% of the Colombia Third Party Logistics (3PL) market size in 2024. The Colombia Third Party Logistics (3PL) market for Retail and E-commerce is set to grow at a 7.15% CAGR between 2025-2030.

- By logistics model, the Asset-Light category accounted for 44% of the Colombia Third Party Logistics (3PL) market share in 2024. The Colombia Third Party Logistics (3PL) market for the Hybrid model is advancing at a 5.75% CAGR between 2025-2030.

- By geography, the Andean Region commanded 58% of the Colombia Third Party Logistics (3PL) market size in 2024. The Colombia Third Party Logistics (3PL) market for the Pacific Corridor is forecast to post a 6.30% CAGR between 2025-2030.

Colombia Third-party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic manufacturing rebound | +1.2% | Andean Region; Caribbean Coast | Short term (≤ 2 years) |

| Near-shoring of U.S. retail supply chains | +1.5% | Nationwide; Andean hub | Medium term (2-4 years) |

| E-commerce parcel surge | +0.8% | Bogotá; Medellín | Short term (≤ 2 years) |

| Port capacity expansions | +0.7% | Pacific Corridor; Caribbean Coast | Medium term (2-4 years) |

| Logistics 4.0 technology adoption | +0.6% | Bogotá; Medellín | Medium term (2-4 years) |

| Rapid cold-chain export growth | +0.5% | Pacific Corridor; Caribbean Coast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Strong Post-Pandemic Manufacturing Rebound

Colombian factories located in free-trade zones have regained momentum, benefiting from cumulative economic growth of 1.5% in 1H 2024 and 2.1% GDP growth in Q2. Entertainment and agriculture posted output jumps above 8%, creating incremental freight flows into port complexes on both coasts. 3PLs are responding by tailoring bonded warehousing and value-added kitting solutions around these export-oriented clusters. Higher throughput is already visible in the La Dorada–Chiriguaná corridor upgrade, which aims to compress inland logistics costs by 26% by 2030.

Near-Shoring of U.S. Retail Supply Chains

U.S. brands that once sourced heavily from East Asia are diversifying production footprints across Latin America, with Colombia positioned as a short-haul replenishment node. The Andean Region’s inland intermodal yards are consequently handling larger cross-dock volumes headed to Pacific ports for expedited sailings to the U.S. West Coast, a shift that amplifies warehousing demand for SKU segmentation and postponement services.

E-Commerce Parcel Volumes Surging

In Bogotá, growing e-commerce parcel volumes create an unprecedented demand for last-mile delivery solutions. The food and grocery segment has been particularly dynamic, with online food sales increasing by 35% in 2023 despite an overall 1.7% decrease in retail food industry sales due to economic slowdown. Micro-fulfilment centers installed inside secondary-tier malls now cut average last-mile distances, trimming delivery windows by 43%. Electric vans and cargo e-bikes deployed in Medellín expanded by 65% in 2024[1]International Transport Forum, “Urban Logistics and Sustainable Delivery Practices,” itf-oecd.org, indicating that sustainability has moved from pilot stage to mainstream criteria in 3PL contract awards.

Pacific and Caribbean Port Capacity Expansions

Grupo Puerto de Cartagena ranks third worldwide for berth productivity, serving 150 countries and 840 ports. New break-bulk and container berths at Puerto Antioquia, slated to open in 2025, will unlock 6 million tons of incremental capacity for coffee, banana, and manufactured exports. Coupled with the 499 km Pacific Railway Network that links Buenaventura to sugar and paper mills, these investments diversify modal options for 3PLs and anchor multimodal service bundles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Truck driver shortages | -0.9% | Nationwide | Medium term (2-4 years) |

| Security surcharges on key corridors | -0.6% | Ruta del Sol; Norte de Santander | Short term (≤ 2 years) |

| Persistent customs bottlenecks | -0.5% | Buenaventura; Cartagena | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Truck Driver Shortages and High Turnover

The IRU projects the gap in qualified Colombian truck drivers to double by 2028, pressuring fleet utilization and raising salary costs[2]International Road Transport Union, “Global Truck Driver Shortage Report 2024,” iru.org. Carriers are sharpening retention incentives, including AI-driven route optimization that cuts empty miles and dynamic fuel-surcharge mechanisms that stabilize pay. A new Ministry of Transport rule setting a minimum 8-hour trip standard will push tariffs on sub-50 km hauls up by 51%, altering network design and rate negotiations across the Colombia Third Party Logistics (3PL) market.

Security Surcharges on Cargo Corridors

Heightened theft risk on sections of Ruta del Sol and the Cúcuta–Bucaramanga corridor has forced forwarders to add armed escorts and night-curfew routing, inflating accessorial charges. Real-time GPS monitoring of loading and unloading will become mandatory from November 30, 2025, increasing compliance overheads yet improving shipment visibility. Cybersecurity protocols under review by the Transportation Security Administration echo these safeguards, signalling that digital as well as physical protection will shape future 3PL cost structures.

Segment Analysis

By Service: Value-Added Warehousing and Distribution Gains Momentum

Value-Added Warehousing and Distribution opened 2025 with a prominent 6.05% CAGR outlook, outpacing core Domestic Transportation Management despite the latter’s 46% revenue lead in 2024. The Colombia Third Party Logistics (3PL) market size for VAWD is poised to scale further as manufacturers outsource kitting, postponement, and returns processing to offset inventory risk and save floor space. Maersk’s 44,000 m² Tocancipá complex, launched in June 2024, exemplifies the new breed of tech-ready campuses, featuring 3,378 m² depot space and 651 m² of refrigerated storage for cross-temperature SKU mixes.

Domestic Transportation Management continues to shoulder long-haul volume but faces margin erosion from driver scarcity and mandatory tariff hikes. International Transportation Management offers a differentiated growth flank, especially in RoRo automotive flows, now supported by CEVA’s three new deep-sea vessels that have moved 225,000 vehicles since launch[3]CEVA Logistics, “Expansion of Finished Vehicle Logistics Services,” cevalogistics.com. Multimodal combinations leveraging upgraded rail spines and seaport connectivity are stimulating demand for bundled inland haulage and drayage under a single rate card, reinforcing the trend toward integrated service packages within the broader Colombia Third Party Logistics (3PL) market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: E-Commerce Upsets Legacy Hierarchies

Consumer Goods and FMCG retained 26% revenue share in 2024, yet Retail and E-commerce is accelerating at a 7.15% CAGR that could reorder the ranking by the end of the decade. Colombia Third Party Logistics (3PL) market size for e-commerce fulfilment has surged alongside grocery platforms that logged 35% online sales growth even as overall food retail contracted. Urban demand for two-hour delivery windows is fuelling micro-fulfilment rollouts and bike-courier networks in Bogotá’s Chapinero and Medellín’s El Poblado districts.

Life Sciences and Healthcare is another momentum pocket. DHL’s purchase of specialty courier CRYOPDP in March 2025 strengthens its ultra-cold chain reach[4]DHL Group, “Acquisition of CRYOPDP Strengthens Life-Sciences Network,” dhl.com, answering rising clinical-trial flows and vaccine rerouting needs. Food and Beverage shippers, meanwhile, leverage controlled-atmosphere reefers to extend produce shelf life, carving out a premium service tier. Automotive, Technology, Energy and Manufacturing consignments rely increasingly on JIT inventory models, prompting 3PLs to integrate higher-frequency cross-dock schedules into legacy hub-and-spoke frameworks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Logistics Model: Hybrid Configurations Scale Up

Asset-Light operators held 44% of 2024 revenue, but Hybrid networks are clocking the fastest 5.75% CAGR, reflecting client appetite for both variable-cost flexibility and guaranteed capacity on critical lanes. The Colombia Third Party Logistics (3PL) market share commanded by Hybrid players rises most quickly in e-commerce, where they blend leased fulfillment centers with contracted last-mile fleets to match cyclical demand spikes. Progressive hybrids are also acquiring minority stakes in reefer depots or yard tractors to de-risk the temperature-controlled and port drayage segments.

Asset-Light incumbents continue to attract capital thanks to low fixed-asset intensity, yet rising congestion fees and security surcharges can dilute thin margins. Asset-heavy specialists remain relevant in hazardous goods and pharma, where shippers stipulate end-to-end custody under one provider. The hybridization trend enables providers to cherry-pick asset ownership by corridor and commodity, sharpening margin control across the Colombian Third Party Logistics (3PL) market without overextending balance sheets.

Geography Analysis

The Andean Region anchored 58% of national 3PL billings in 2024, driven by Bogotá-Medellín’s twin-city corridor that funnels finished goods to 35 million consumers. Urban congestion, however, pushes logistics costs above 13% of sales for some retailers, leading to the rollout of micro-fulfilment nodes that cut last-mile costs by 47% and slash failed-delivery rates. Rail connectivity upgrades under the National Railway Master Plan promise to streamline container transfers from central depots to Caribbean and Pacific ports, reinforcing the Andean role as a domestic consolidation hub within the Colombia Third Party Logistics (3PL) market.

The Pacific Corridor is carving the fastest trajectory at a 6.30% CAGR, buoyed by Buenaventura’s deeper berths and the 499 km Pacific Railway Network that handles pulp, minerals, and containerized agrifood consignments. The planned Tren de Cercanías around Cali, a USD 4 billion suburban rail loop, will extend intermodal access for exporters in Valle del Cauca, supporting time-sensitive produce runs to U.S. retailers.

The Caribbean Coast leverages Cartagena’s world-class quay performance and the forthcoming Puerto Antioquia complex near Urabá to siphon volumes from overburdened Andean trucking corridors. Orinoquía and Llanos, rich in hydrocarbons and grains yet light on paved road density, represents a greenfield opportunity where niche 3PLs can monetize barge and short-haul airfreight concepts. Amazonia remains sparsely served, but government attention to river dredging and small-port modernization could unlock new lanes by the decade’s close, edging more remote regions into the Colombia Third Party Logistics (3PL) market ecology.

Competitive Landscape

Top Companies in Colombia Third Party Logistics (3PL) Market

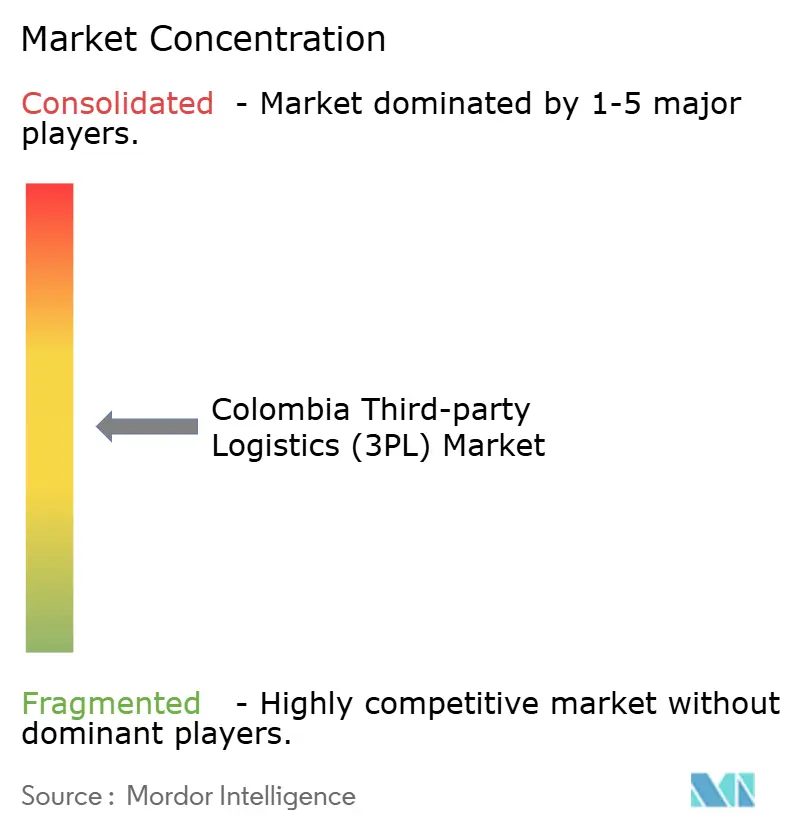

Colombia’s 3PL arena remains moderately fragmented, with the top five players collectively controlling a significant share of sector revenue. Global heavyweights such as DHL, Maersk, and DSV lean on multinational contracts and advanced tech stacks, while national champions operate granular last-mile fleets and maintain personal ties with local customs brokers. Hybrid specialists are acquiring predictive analytics platforms to upsell dynamic routing to mid-market shippers.

Technology has become the primary battleground. Maersk’s Tocancipá campus integrates automated gate entry, yard management sensors, and a control-tower dashboard that delivers SKU-level visibility in under 45 seconds per query. CEVA’s new RoRo vessels shorten transit times out of Asian manufacturing nodes, strengthening its value proposition for automotive OEMs exporting to Andean showrooms. DHL’s acquisition of CRYOPDP cements its hold on temperature-controlled clinical logistics, a segment commanding premium yields in the Colombian Third Party Logistics (3PL) market.

Local specialists are not standing still. Emergent Cold Latin America, now the region’s largest temperature-controlled platform at 157 million ft³, is adding Medellín capacity to service avocado packers and biopharma lines. Start-ups leveraging electric cargo bikes in Bogotá have formed partnerships with nationwide parcel networks, injecting sustainability credentials into traditionally diesel-heavy sectors. Across these tiers, competitive advantage increasingly stems from data-driven orchestration and sector-specific operating manuals rather than pure fleet size.

Colombia Third-party Logistics (3PL) Industry Leaders

-

Kuehne + Nagel

-

Servientrega S.A.

-

DHL Supply Chain & Global Forwarding

-

Blu Logistics Colombia SAS

-

Icoltrans

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: CEVA Logistics expanded its deep-sea car carrier network, adding Far-East links to Central and South America, including Colombia, and introduced three additional RoRo vessels.

- April 2025: DSV completed the purchase of Schenker, doubling its global scale and enhancing Colombian reach.

- March 2025: DHL Group acquired CRYOPDP to bolster pharma logistics reach.

- February 2025: Colombia’s Ministry of Transport set an 8-hour minimum freight trip, lifting tariffs on sub-50 km routes by 51%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Colombia third-party logistics market as all revenue earned by specialized providers that, on contract, manage domestic or international freight movement, customs brokerage, and value-added warehousing or distribution for shippers. Activities captured include road, air, sea, and multimodal transport management alongside outsourced storage and order-fulfillment services.

Scope Exclusion: Postal parcel networks and any in-house logistics operations run by manufacturers or retailers are not counted.

Segmentation Overview

- By Service

- Domestic Transportation Management

- Road

- Air

- Others

- International Transportation Management

- Road

- Air

- Sea

- Multimodal / Intermodal

- Value-Added Warehousing and Distribution (VAWD)

- Domestic Transportation Management

- By End-User Industry

- Automotive

- Energy and Utilities

- Manufacturing

- Life Sciences and Healthcare

- Technology and Electronics

- Retail and E-commerce

- Consumer Goods and FMCG

- Food and Beverages

- Others

- By Logistics Model

- Asset-Light (Management-Based)

- Asset-Heavy (Own Fleet and Warehouses)

- Hybrid

- By Geography

- Andean Region

- Caribbean Coast

- Pacific Corridor

- Orinoquía and Llanos

- Amazonia

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews and short surveys with freight forwarders, FMCG shippers, e-commerce sellers, fleet financiers, and regional warehouse developers helped us validate tariff assumptions, contract churn rates, and typical storage yields across Bogotá, Medellín, and the coastal corridors.

Desk Research

We extracted baseline indicators from open public sources such as the National Department of Statistics traffic surveys, DIAN customs dashboards, Ministry of Transport trucking bulletins, Civil Aviation freight ton-kilometer logs, Port of Cartagena throughput sheets, and releases from ANDI's logistics committee. Company filings, investor decks, and reputable press enriched operator benchmarks, while paid datasets like D&B Hoovers (financial splits) and Dow Jones Factiva (deal flow) sharpened the competitive map. These sources are illustrative; many additional references were screened to confirm consistency.

Market-Sizing & Forecasting

We began with a top-down reconstruction of Colombia's freight bill, applied a 54 percent outsourcing ratio, and then separated spend across domestic transport, international forwarding, and warehousing. Selective bottom-up checks sampled 3PL revenue disclosures, warehouse stock surveys, and channel checks tempered totals before finalization. Key model drivers include e-commerce parcel volumes, free-trade-zone export tonnage, diesel price index, warehouse vacancy, peso-USD exchange swings, and port dredging milestones. Multivariate regression coupled with ARIMA overlays produced forecasts, with expert panels adjusting scenario ranges wherever data gaps appeared.

Data Validation & Update Cycle

Mordor analysts run variance screens against historical series, peer benchmarks, and fresh trade data, then escalate anomalies for review before sign-off. The model updates annually, with interim refreshes if fuel tax shifts, port strikes, or currency shocks materially alter demand patterns.

Why Mordor's Colombia Third party Logistics Baseline Is Dependable

Published estimates often diverge because analysts apply dissimilar service scopes, outsourcing ratios, currency bases, or refresh cadences. Some studies fold courier volumes into 3PL totals, others track only asset-heavy warehousing, and several lock forecasts to a single-year exchange rate without later reconciliation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.60 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2023) | Regional Consultancy A | Includes freight forwarding and CEP, relies solely on macro spend shares |

| USD 0.48 B (2024) | Trade Journal B | Tracks contract warehousing only, omits transport management |

These contrasts show that our disciplined variable selection, rolling-currency normalization, and balanced top-down and bottom-up checks deliver a transparent baseline that decision-makers can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Colombia Third Party Logistics (3PL) market?

The Colombia Third Party Logistics (3PL) market stands at USD 4.60 billion in 2025 and is forecast to reach USD 5.83 billion by 2030.

Which service category is expanding the fastest?

Value-Added Warehousing & Distribution leads with a 6.05% CAGR thanks to rising demand for kitting, postponement and reverse-logistics services.

Why is the Pacific Corridor growing quicker than other regions?

New port terminals, a 499 km rail spine and multimodal links are driving a 6.30% CAGR by opening shorter export routes to U.S. and Asian markets.

How are driver shortages affecting logistics costs?

A doubling shortfall by 2028 is pushing carriers to raise wages and adopt AI route optimization, while new tariff floors lift haulage prices on short-distance lanes by up to 51%.

Which end-user industry now offers the strongest upside for 3PL providers?

Retail & E-commerce, powered by significant growth in online grocery sales and rapid last-mile innovations, is forecast to expand at a 7.15% CAGR through 2030.

What technologies are most in demand among Colombian shippers?

Warehouse Management Systems with RFID, electric last-mile vehicles and real-time control-tower platforms are becoming standard requirements in new 3PL contracts.

Page last updated on: