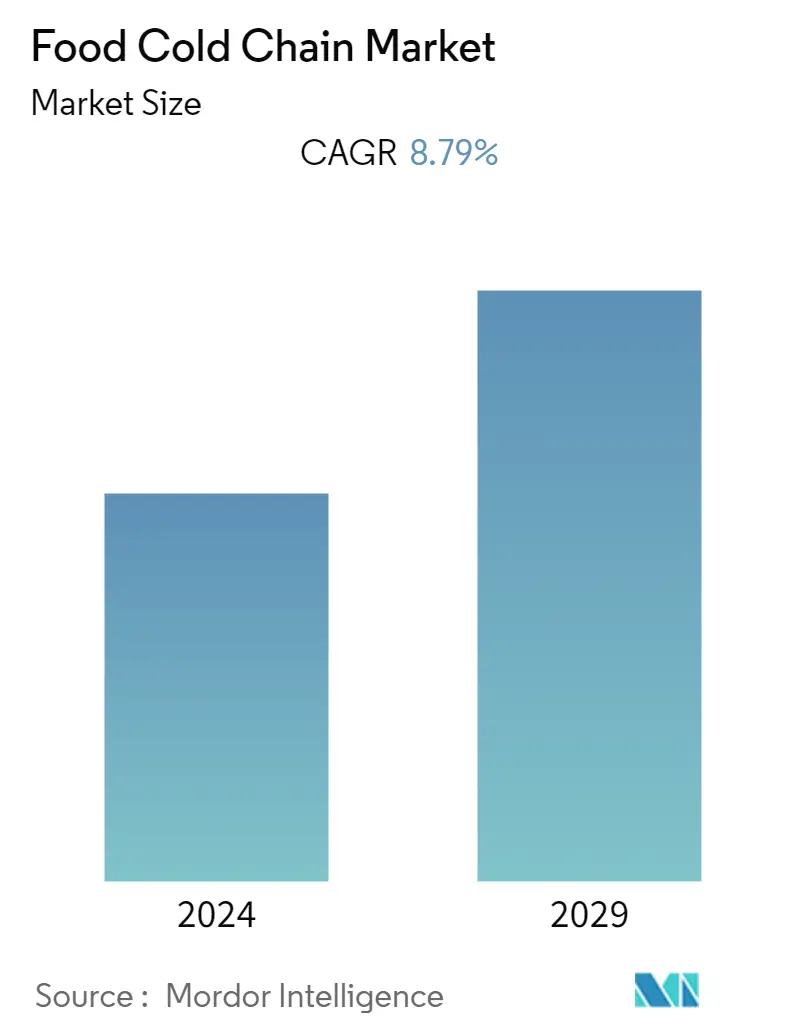

Food Cold Chain Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 8.79 % |

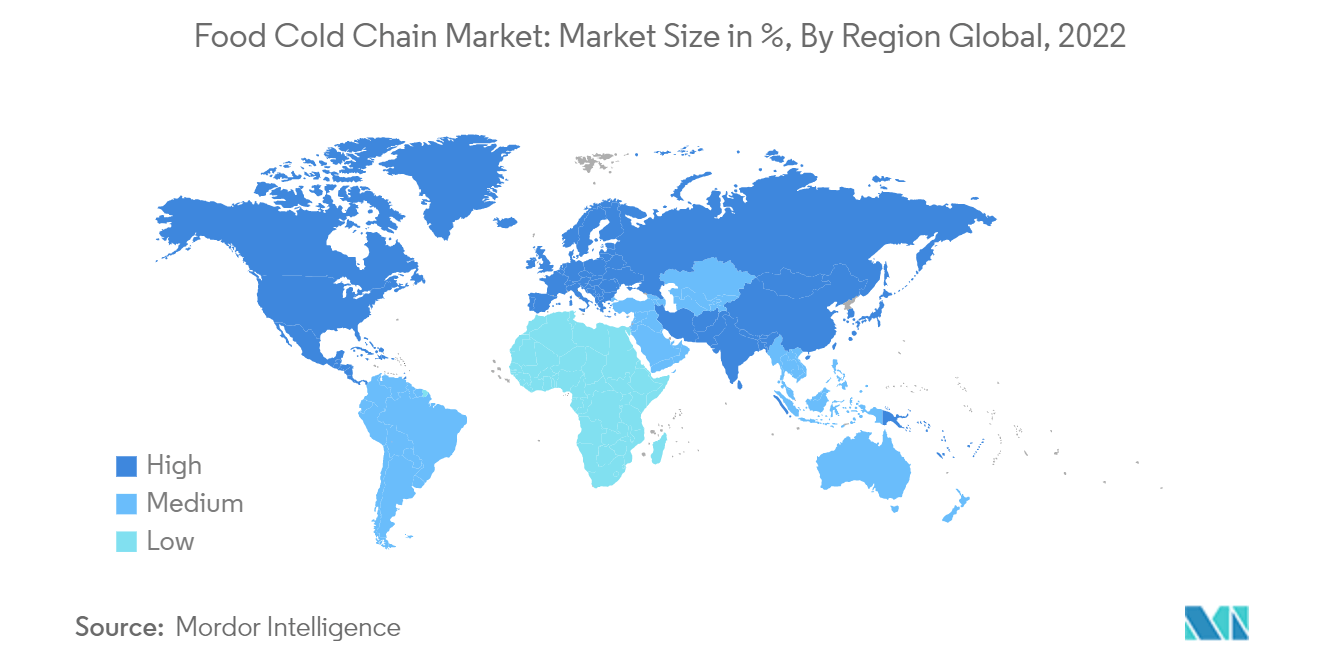

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

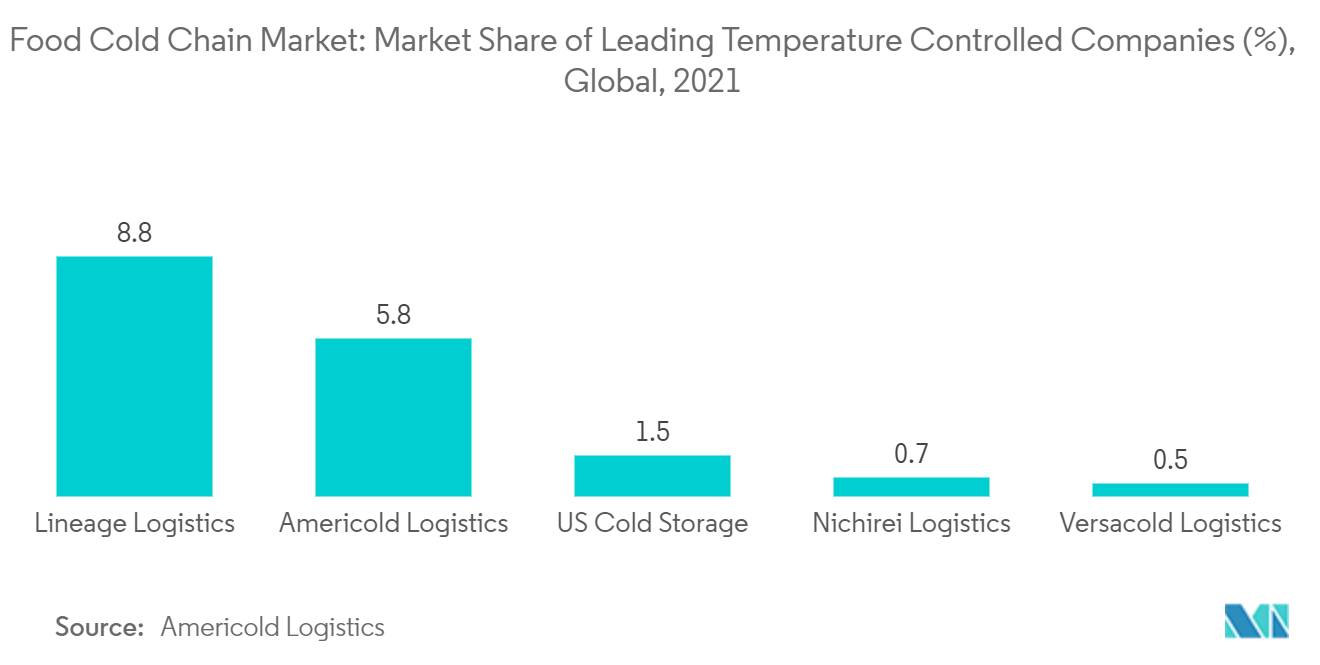

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Food Cold Chain Market Analysis

The food cold chain market is projected to register a CAGR of 8.79% over the next five years.

- The perishability of food is a mounting concern, from the procurement of raw materials to the showcasing of end products on retail shelves. With changes in ambient temperature resulting from climate change, cold chain infrastructure has become more vulnerable, and resilient cold chain solutions are increasingly necessary.

- The United Nations Environment Programme (UNEP) and WRAP released the Food Waste Index Report 2021 and highlighted that The household food waste estimate in the United States is 59 kg per capita per year, or 19,359,951 tonnes a year. This highlights the importance of finding ways to prevent food wastage. Cold chains can increase the shelf life of perishable products by providing controlled temperature, humidity, and atmospheric conditions. For instance, refrigeration can increase the shelf life of fresh fruits and vegetables by days or even months.

- In the current scenario, agencies linked with export promotion and trade policies are focusing on developing international cold chain processes through improved regulatory environments, increased workforce skills, and infrastructure investment. This promotes the benefits of a country or company's services and creates a favorable environment for the food cold chain market.

- Market players are inventing new technologies for transport and cold chain storage and forming mergers and acquisitions to create innovative approaches toward cold chain storage and transportation. For example, in August 2022, Lineage Logistics acquired VersaCold Logistics to expand its services in Canada and regulate the food supply chain across the country.

Food Cold Chain Market Trends

Growing Investments in Cold Chain Infrastructure

- The demand for frozen food and products is on the rise, thanks to their convenience and longer storage capacity. As a result, the need for cold storage and cold storage transport is increasing globally. Transportation of sensitive frozen food items, such as ice cream, frozen curries, and frozen canned products, requires proper temperature-controlled facilities to prevent physical or environmental damage.

- In addition, perishable products, such as meat, fish/seafood, fruits, vegetables, and dairy products, are traded in bulk compared to processed products. The shelf life of meat/fish is only a few hours, which has led to an increase in demand for proper temperature-controlled storage facilities. Market players are expanding their cold storage capacities to reduce food waste.

- For example, in May 2022, Lineage Logistics completed a new fully automated warehouse expansion with an additional 45,000 pallet positions for retail and food service customers. This expansion will not only help reduce food waste but also provide customers with more efficient and reliable cold storage solutions.

North America Holds the Largest Market Share

- Seasonality, time-temperature variation, and road accessibility throughout the year drive the demand for food cold chains in the North American market. In addition, consumers in the market are increasingly shifting away from highly processed and unhealthy foods with long shelf lives towards temperature-sensitive and perishable food products, creating momentum for a cold supply chain with advanced technology.

- Furthermore, food wastage has become a significant problem in the North American region. According to a report by the UN Environmental Programme, in 2021, Canadian household food wastage reached 79 kg per capita. With the increasing demand for cold chain storage and transport, market players are launching new transport facilities in the region.

- For example, in October 2022, A.P. Moller-Maersk ordered eight electric trucks from Volvo in Southern California to distribute food and other products. This move demonstrates the industry's efforts to adopt sustainable and environmentally friendly practices while meeting the growing demand for cold chain transport and storage.

Food Cold Chain Industry Overview

The global food cold chain market is highly fragmented, with a mix of global and regional players dominating the industry. Some of the key players in the market are Americold Logistics, Lineage Logistics (Preferred Freezer Services), Nichirei Corporation, Kloosterboer Group B.V., and VersaCold Logistics Services.

The cold chain market provides ample opportunities for both start-ups and established players to enter regions with high export potential, as well as those with rapidly growing demand for frozen foods in domestic markets. These companies are increasingly adopting expansion, mergers, and acquisitions as preferred strategies to establish a strong foothold in the global market.

Food Cold Chain Market Leaders

Americold Logistics

Lineage Logistics (Preferred Freezer Services)

Nichirei Corporation

Kloosterboer Group B.V.

VersaCold Logistics Services

*Disclaimer: Major Players sorted in no particular order

Food Cold Chain Market News

- September 2022: Celcius Logistics, India's fastest-growing cold-chain marketplace startup, launched its smart last-mile delivery platform that addresses and fixes the most pertinent pain points in India's fragile cold supply chains. The brand has also partnered with vehicle owners and automotive manufacturers to create a robust on-ground network of reefer vehicles that will be integrated with the smart platform created with a unique Inventory Management System (IMS).

- September 2022: Lineage Logistics LLC acquired Grupo Fuentes, a prominent operator of transport and cold storage facilities in Spain. Grupo Fuentes is a significant player in the market, with a fleet of 500 vehicles and trailers, six logistics centers, a cold storage warehouse, and value-added services supporting those facilities. This acquisition is expected to significantly expand Lineage Logistics' footprint in Europe and strengthen its position as a global leader in temperature-controlled logistics. With Grupo Fuentes' extensive network of facilities and expertise in the Spanish market, Lineage Logistics is now better equipped to serve customers across Europe and beyond.

- August 2021: GeoTab, a leading global company in IoT and connected vehicles, unveiled its latest offering - cold chain vans with advanced refrigeration capabilities. These vans have been specifically designed to transport temperature-sensitive goods, such as food and pharmaceuticals while maintaining the desired temperature range. The vans come equipped with cutting-edge refrigeration systems that can be easily controlled and monitored in real time. This allows for precise temperature management during transportation, ensuring that the goods remain fresh and safe to consume or use.

Food Cold Chain Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables and Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Restraints

4.3 Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Type

5.1.1 Cold Chain Storage

5.1.2 Cold Chain Transport

5.2 Application

5.2.1 Fruits and Vegetables

5.2.2 Meat and Seafood

5.2.3 Dairy and Frozen Dessert

5.2.4 Bakery and Confectionery

5.2.5 Ready-to-Eat Meal

5.2.6 Other Applications

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.1.4 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 Spain

5.3.2.4 France

5.3.2.5 Italy

5.3.2.6 Rest of Europe

5.3.3 Asia Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 South Africa

5.3.5.2 Saudi Arabia

5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 AmeriCold Logistics LLC

6.3.2 VersaCold Logistics Services

6.3.3 Lineage Logistics Holding LLC

6.3.4 Nichirei Corporation

6.3.5 AGRO Merchants Group

6.3.6 DSV A/S

6.3.7 Kloosterboer Group BV

6.3.8 Gruppo Marconi Logistica

6.3.9 Henningsen Cold Storage Co.

6.3.10 Celsius Logistics

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Food Cold Chain Industry Segmentation

The food cold chain is the facility provided for the storage and transportation of frozen food products.

The food cold chain market is segmented by type, application, and geography. By type, the market is segmented into cold chain storage and cold chain transport. By application, the market is segmented into fruits and vegetables, meat and seafood, dairy and frozen dessert, bakery and confectionery, ready-to-eat meals, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Type | |

| Cold Chain Storage | |

| Cold Chain Transport |

| Application | |

| Fruits and Vegetables | |

| Meat and Seafood | |

| Dairy and Frozen Dessert | |

| Bakery and Confectionery | |

| Ready-to-Eat Meal | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Food Cold Chain Market Research FAQs

What is the current Food Cold Chain Market size?

The Food Cold Chain Market is projected to register a CAGR of 8.79% during the forecast period (2024-2029)

Who are the key players in Food Cold Chain Market?

Americold Logistics, Lineage Logistics (Preferred Freezer Services), Nichirei Corporation, Kloosterboer Group B.V. and VersaCold Logistics Services are the major companies operating in the Food Cold Chain Market.

Which is the fastest growing region in Food Cold Chain Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Food Cold Chain Market?

In 2024, the North America accounts for the largest market share in Food Cold Chain Market.

What years does this Food Cold Chain Market cover?

The report covers the Food Cold Chain Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Food Cold Chain Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Food Cold Chain Industry Report

Statistics for the 2024 Food Cold Chain market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Food Cold Chain analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.