Coffee Roaster Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

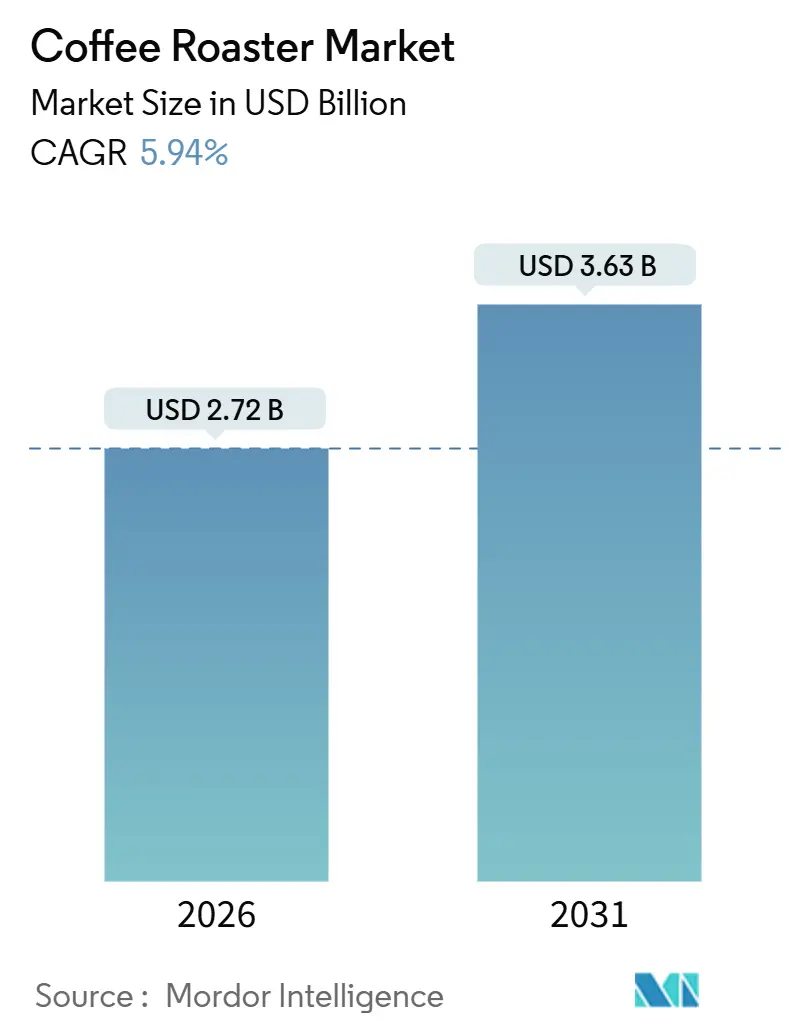

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Coffee Roaster Market Analysis by Mordor Intelligence

The coffee roaster market size stands at USD 2.72 billion in 2026 and is projected to reach USD 3.63 billion by 2031, reflecting a 5.94% CAGR during the forecast period. Operators are investing in equipment that captures real-time data, connects via IoT, and utilizes heat-recovery technology. These features not only comply with the European Union Deforestation Regulation traceability rules but also enhance energy economics. In August 2025, green-coffee prices surged to 328 cents per pound, heightening margin pressures and intensifying the quest for energy-efficient designs to counteract input-cost volatility. Europe, bolstered by its robust specialty-coffee infrastructure, commands the largest regional share. Meanwhile, the Asia-Pacific, driven by urbanization, witnesses rapid unit growth, especially with rising on-premise roasting demands in China and India. While drum roasters continue to dominate industrial facilities, there's a notable shift. Fluid-bed systems and electric heating are gaining traction, especially in areas with tightening emissions regulations and limited floor space, though product substitution remains constrained.

Key Report Takeaways

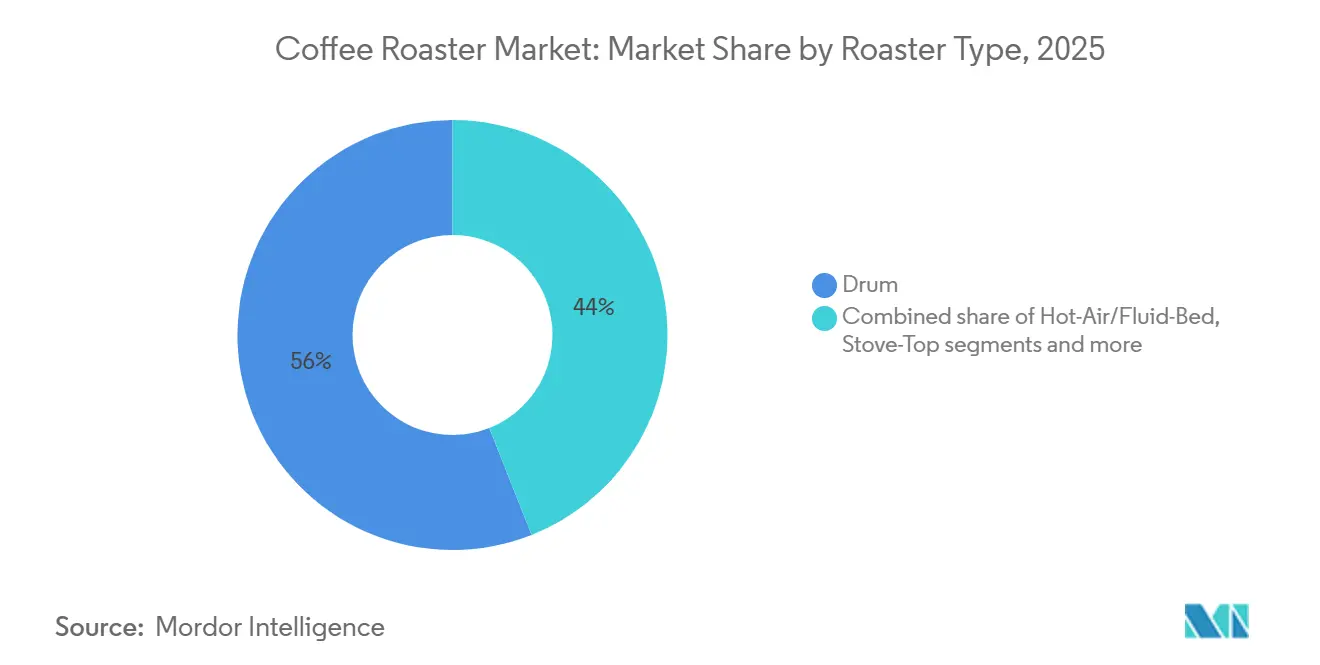

- By roaster type, drum units led with 56.01% coffee roaster market share in 2025; fluid-bed systems are forecast to expand at a 7.40% CAGR through 2031.

- By category, gas-powered equipment captured 61.52% of the coffee roaster market size in 2025; electric variants are advancing at a 6.90% CAGR to 2031.

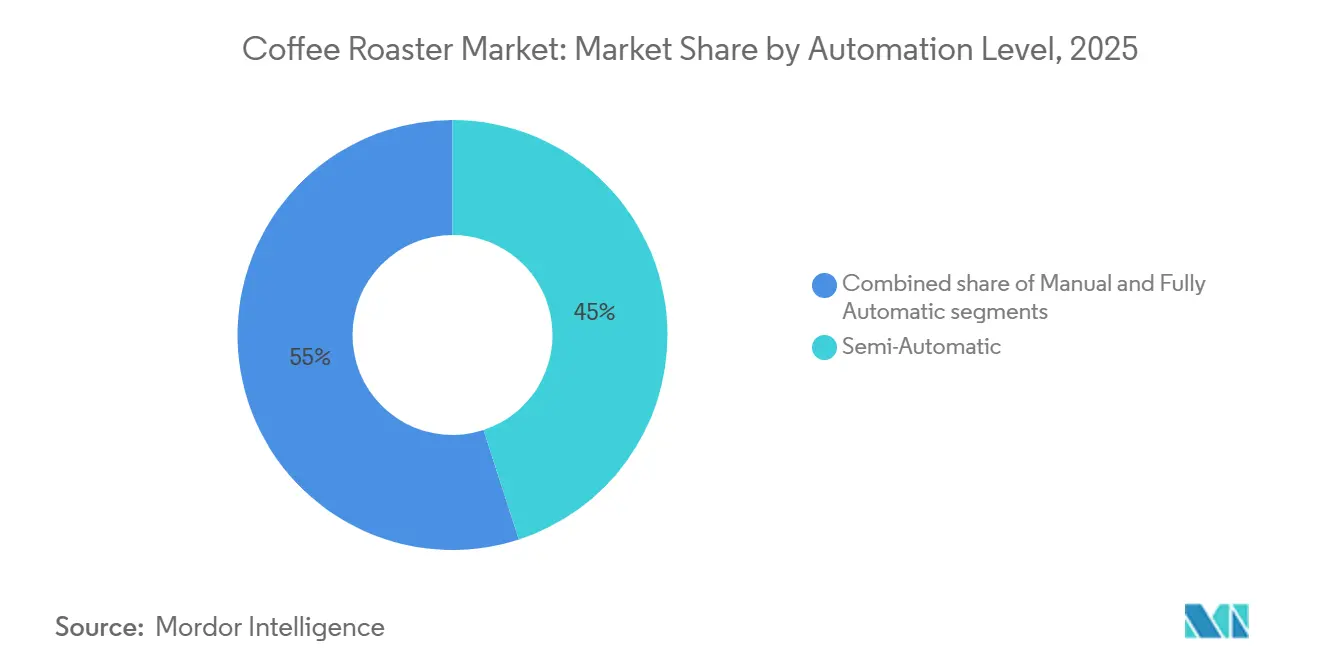

- By automation level, semi-automatic models held 45.02% revenue share in 2025; fully automatic systems are projected to post the highest 9.10% CAGR to 2031.

- By end user, industrial and commercial operators commanded 55.45% share of the coffee roaster market size in 2025; the HoReCa segment is growing at a 7.60% CAGR through 2031.

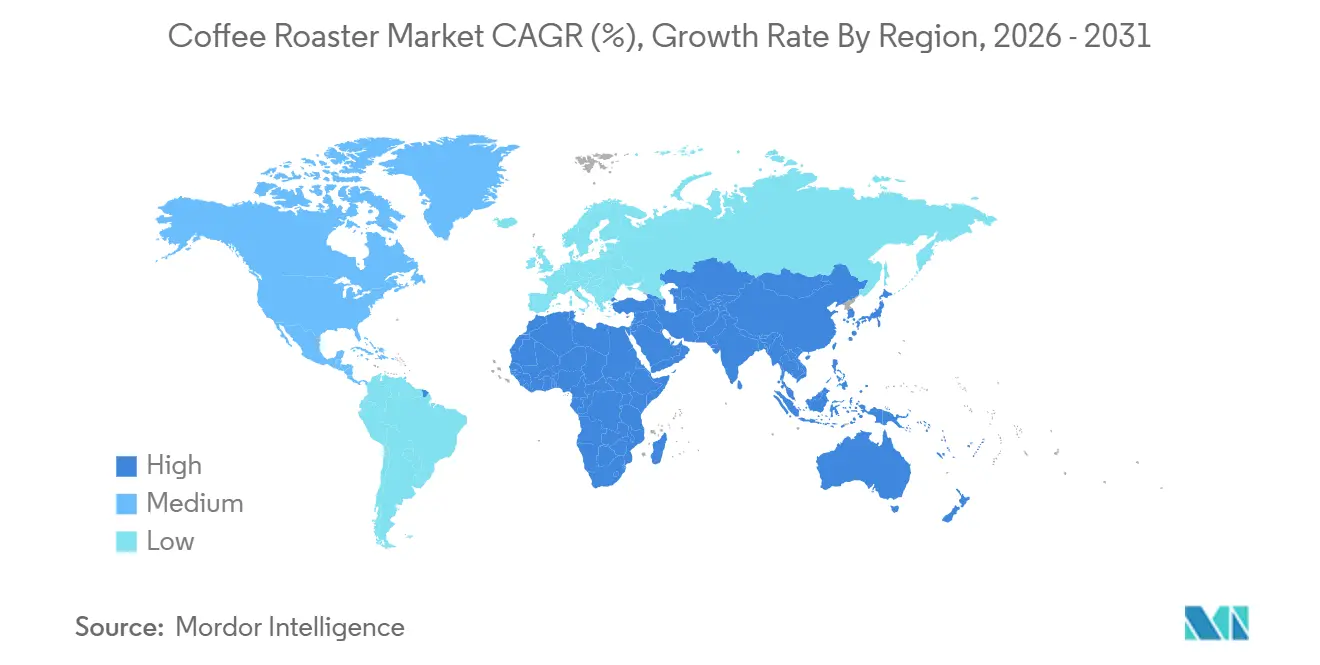

- By geography, Europe accounted for 32.45% of 2025 revenue; Asia-Pacific exhibits the fastest regional growth at a 7.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coffee Roaster Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in specialty-coffee cafés worldwide | +1.2% | Global, with concentration in Europe, North America, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing micro-roastery business models | +0.9% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Rising adoption of energy-efficient roasting technology | +1.1% | Europe, North America, early adoption in Asia-Pacific | Long term (≥4 years) |

| Increasing automation and Industry 4.0 integration | +1.3% | Global, led by Europe and North America | Long term (≥4 years) |

| Carbon-neutral roasting innovations | +0.7% | Europe, North America, selective Asia-Pacific markets | Long term (≥4 years) |

| Surge in demand for portable nano-roasters | +0.6% | North America, Europe, emerging in Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid rise in specialty-coffee cafés worldwide

Specialty cafés are increasingly opting for mid-capacity roasters, specifically in the 15–50 kg range. This trend is driven by the fact that in-store roasting not only signals provenance but also boosts selling prices by 20–40% compared to commodity blends. In 2024, Europe boasted 45,008 independent cafés, with projections pointing to a rise to 52,800 by 2029, indicating a consistent cycle of equipment refreshes[1]Source: World Coffee Portal, "Europe’s branded coffee chains achieve sustained growth amid challenging economy," worldcoffeeportal.com. Meanwhile, in the Asia-Pacific region, second-tier cities in China and metropolitan areas in India are rapidly opening cafés. However, these locations are lagging in installing roasting lines, leading to a burgeoning demand for compact, plug-and-play systems. While regulatory challenges remain minimal, there's a growing emphasis on the ISO 22000 food-safety certification. This is particularly evident as multi-unit operators strive for consistent quality across their locations. Manufacturers that prioritize user-friendly maintenance and eye-catching design elements are finding increased traction in this competitive channel.

Growing micro-roastery business models

In 2024, micro-roasteries in the U.S. that roast under 100 kg per day secured 68% of the nation's roasting licenses, a notable rise from 52% in 2020. Operators are increasingly favoring drum roasters in the 5–15 kg range, often opting for modular equipment packages priced under USD 30,000. While direct-to-consumer channels shield these micro-roasteries from fluctuations in commodity prices, they also lead to increased logistics expenses. In response, equipment vendors are offering subscription-based maintenance and remote diagnostics, a move aimed at minimizing downtime, especially in rural areas with a shortage of technicians. Additionally, demand for sample roasters surged by 12% in 2025, enabling micro-roasteries to expand their SKU portfolios and seasonally rotate their single-origin offerings.

Rising adoption of energy-efficient roasting technology

Energy expenses make up about 25% of total roasting costs. Heat-recovery systems, which can reduce natural gas consumption by 25-40%, result in annual savings ranging from USD 20,000 to USD 50,000 for plants processing 500 kg per hour. These systems not only lower operational costs but also contribute to sustainability goals by reducing greenhouse gas emissions. In Europe, the push to eliminate gas connections in new commercial buildings is speeding up the adoption of electric systems, particularly in Germany, the Netherlands, and Belgium, where governments are implementing stricter energy policies. Today's modern drum lines are equipped with variable-frequency drives and PLC controls to minimize idle losses, enhancing energy efficiency and operational precision. As utility rates climb and carbon credits become monetizable, payback periods shrink to nearly two years, aligning perfectly with the internal hurdle rates set by major contract roasters. This combination of cost savings and environmental benefits makes these advancements highly attractive for industry players.

Increasing automation and Industry 4.0 integration

Fully automatic roasters, equipped with PLC control, moisture sensors, and batch-level traceability, ensure compliance with EUDR and ISO 22000 standards, which are critical for maintaining food safety and sustainability in the supply chain. With skilled roast masters commanding salaries exceeding USD 70,000 annually, labor shortages in Europe and North America heighten the appeal of these automated systems, as they reduce dependency on manual expertise. Enterprise buyers are increasingly influenced by NIST guidelines on cybersecure sensor networks in their procurement decisions, ensuring robust data protection and operational integrity[2]Source: National Institute of Standards and Technology, "Security for IoT Sensor Networks," nccoe.nist.gov. Platforms like Cropster are streamlining operations by synchronizing recipes across various sites, thereby reducing quality discrepancies and enhancing consistency in production. Furthermore, predictive analytics are linking roast curves to green-bean moisture levels, empowering operators to preemptively adjust parameters, avert defects, and protect their long-term contracts with retail chains by ensuring consistent product quality and reliability.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure of industrial roasters | -0.8% | Global, acute in emerging markets | Short term (≤2 years) |

| Volatility in green-coffee prices impacting ROI | -0.9% | Global, severe in price-sensitive markets (Asia-Pacific, Middle East and Africa) | Short term (≤2 years) |

| Tightening EU emissions norms for gas roasters | -0.5% | Europe, spillover to North America | Medium term (2-4 years) |

| Supply-chain shortages of high-grade steels | -0.6% | Global, concentrated in Europe and North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High capital expenditure of industrial roasters

Large drum roasters equipped with afterburners, heat-recovery systems, and PLC controls come with a price tag of USD 300,000–750,000, posing a significant challenge for smaller operators. These high costs often deter small-scale businesses from investing in advanced equipment. When factoring in auxiliary expenses like ventilation, electrical upgrades, and training, costs can surge by an additional 30–50%, further increasing the financial burden. While vendors in North America and Europe provide leasing options to ease this burden, less than 15% of transactions take advantage of these terms, indicating limited adoption. Buyers from emerging markets tend to self-finance, often opting for older gas lines due to budget constraints, even if these units fail to meet new emissions standards, potentially exposing them to regulatory risks. In the 100–500 kg batch category, firms face a critical choice: modernize their operations to remain competitive or exit the market entirely. This dilemma has spurred consolidation among contract roasters, particularly in Germany and the Netherlands, where larger players are absorbing smaller ones to strengthen their market position.

Volatility in green-coffee prices impacting ROI

In August 2025, Arabica futures surged 100% year-on-year, driven by a 15% output reduction in Brazil due to frost and a 12% export cut in Vietnam from drought. This significant price increase has had a cascading effect on the coffee industry. A mere 50-cent uptick in raw-bean prices can wipe out as much as 80% of the gross margin on commodity blends, forcing companies to delay capital purchases and reevaluate their operational strategies. While flexible equipment that can process either Arabica or Robusta offers some protection against market fluctuations, it does not completely eliminate the risks. Buyers are still holding off on investments until prices stabilize, as uncertainty in raw material costs continues to impact decision-making. Price sensitivity is particularly pronounced in India, Indonesia, and Nigeria, where retail mark-ups exceeding 7% encounter pushback from consumers, making it challenging for businesses to pass on the increased costs without affecting demand.

Segment Analysis

By Roaster Type: Drum Dominance Meets Fluid-Bed Efficiency

In 2025, drum units captured a dominant 56.01% share of the global coffee roaster market. Their success stems from operator familiarity, consistent performance, and robust aftermarket support. These systems have become the benchmark for industrial operations, particularly for batch sizes over 500 kg. To solidify their lead, manufacturers are upgrading drum designs with infrared sensors and variable speed drives, trimming roast times by 10–15%. These advancements not only enhance efficiency but also ensure uniform roasting, which is critical for maintaining product quality at scale. While newer technologies are surfacing, the reliability and rich roast profiles of drum roasters keep them at the helm of large-scale production, making them indispensable for high-volume coffee producers.

Hot-air fluid-bed roasters are the market's fastest-growing segment, boasting a CAGR of 7.40% projected through 2031. Their advantages, such as reduced particulate emissions and quicker heat transfer, resonate with micro-roasters, research facilities, and small urban cafés prioritizing cleaner and faster roasting. This trend is especially pronounced in the Asia-Pacific region and in markets enforcing strict emission regulations, where environmental compliance is a key driver for adoption. Moreover, the rise of hybrid systems that merge fluid-bed efficiency with drum-style flavor is propelling this segment's growth. These hybrid systems not only offer operational flexibility but also cater to diverse consumer preferences, indicating a steady ascent in global market presence.

Note: Segment shares of all individual segments available upon report purchase

By Category: Electric Gains Ground as Gas Infrastructure Faces Headwinds

In 2025, gas lines dominated the coffee roaster market, accounting for 61.52% of the installed capacity. Operators capitalized on the existing gas infrastructure and its high thermal output to bolster commercial roasting lines. Yet, as Europe tightens building codes and regulatory pressures mount against fossil fuels, the once-expanding gas segment faces limitations. In countries like Germany and Japan, gas maintains a cost advantage per pound, especially when electricity costs exceed USD 0.15 per kWh. This advantage keeps gas-fired systems prevalent in numerous industrial plants. However, manufacturers are proactively adapting, developing hydrogen-ready burners. These innovations could facilitate a transition from fossil gas in regions rich in green hydrogen, thereby mitigating long-term asset risks. While gas roasters are expected to dominate the installed base until 2031, their potential for expansion in economies shifting towards decarbonization appears to be constrained.

Electric coffee roasters are on a growth trajectory, with projections indicating a CAGR of about 6.90% through 2031. This surge is largely driven by evolving sustainability regulations and corporate decarbonization objectives influencing equipment procurement. In markets like Norway and Iceland, where hydropower keeps industrial electricity tariffs at or below USD 0.05 per kWh, electric systems already boast lower per-pound roasting costs compared to gas. Recent innovations in induction coils and high-density resistance elements have bridged performance disparities. Electric units can now achieve peak temperatures within 10% of gas ramp rates, enhancing their appeal for high-throughput applications. With grid investments on the rise and carbon pricing becoming more pronounced, the momentum for electric adoption is set to quicken. This is especially true for new plants and retrofit projects under emissions scrutiny. As a result, while both gas and electric technologies are witnessing growing demand alongside the expanding coffee market, electric roasters are poised to incrementally siphon market share from their gas counterparts across various economic regions.

By Automation Level: Fully Automatic Systems Capture Labor-Scarce Markets

In 2025, semi-automatic coffee roasters commanded a dominant 45.02% share of the market. Operators gravitated towards these systems for their blend of programmable profiles and hands-on control. Specialty cafés and mid-sized roasteries, seeking consistency yet valuing real-time adjustments by baristas and roastmasters, found these systems particularly appealing. Enhancements like connected sensors and basic telemetry, often seen as IoT add-ons, are becoming standard on semi-automatic platforms. These features boost batch logging and equipment uptime, all while retaining essential human oversight. Meanwhile, manual models carve out a niche in training academies and micro-roasters. Here, the focus is on honing tactile roasting skills and sensory judgment, integral to their brand identity. Thus, while the market sees a push towards back-end digitalization, the "craft" essence remains firmly rooted in the semi-automatic and manual formats.

Fully automatic roasters are on a rapid ascent, with projections indicating a CAGR of 9.10% through 2031. This surge is largely driven by industrial plants and large chains emphasizing labor efficiency and consistency. With the integration of advanced PLC controls, IoT modules, and cloud connectivity, these roasters offer features like predictive maintenance, batch-level traceability, and centralized recipe management. Such capabilities are not just technological advancements; they align with stringent regulations like the EUDR, which mandates thorough documentation of origin and processes. This technological edge allows multinational coffee chains to deploy or adjust seasonal roast curves across multiple locations in unison, minimizing variability and expediting new product launches. Furthermore, vendors are shifting their business model. By bundling remote diagnostics, software subscriptions, and analytics dashboards with hardware, they're moving from traditional one-time equipment sales to a more lucrative recurring service revenue model. With skilled labor costs on the rise, the trend suggests a dominance of fully automated lines in large industrial facilities by decade's end. In contrast, semi-automatic units are likely to remain a staple in specialty cafés, where the emphasis is on craft and sensory nuances.

Note: Segment shares of all individual segments available upon report purchase

By End User: HoReCa Segment Accelerates as Experiential Retail Gains Traction

In 2025, industrial and commercial facilities dominated the coffee roaster market, capturing 55.45% of the total share. These operations cater to supermarkets, private-label brands, and large-scale processors, all of whom demand high throughput and stringent compliance documentation. Industrial setups, benefiting from scale efficiencies and established supply chains, prioritize bulk roasting where traceability and volume consistency are essential for retail distribution. These segments enjoy strong aftermarket support and customization options tailored to their high-capacity needs, reinforcing their lead in a market with steady demand for packaged coffee products. Despite added complexities from regulatory pressures like the EUDR, industrial players are channeling investments into integrated systems. This strategy not only helps them maintain certification but also offers efficiency advantages over smaller counterparts. With infrastructure investments that dwarf those of smaller operators, this end-use category is poised to anchor market stability through 2031.

Hotels, restaurants, and cafés (HoReCa) are emerging as the fastest-growing segment in the coffee roaster market, projected to grow at a 7.60% CAGR through 2031. This surge is largely driven by a push for premium experiences, leading to a rise in on-site roasting. As tourism rebounds to pre-2019 levels by 2024, five-star establishments in cities like Dubai, Singapore, and New York are showcasing tabletop roasters in their lobbies, leveraging them to justify a 30–50% price premium on single-origin brews. Vendors are stepping up, providing comprehensive solutions that encompass staff training and preventive maintenance, making it easier for outlets without in-house expertise to adopt. High-end venues are also capitalizing on experiential trends, such as the "roasting theatre," emphasizing guest engagement over mere cost considerations. Unless there's a significant dip in discretionary spending, HoReCa is well-positioned for substantial growth, outpacing industrial volumes.

Geography Analysis

In 2025, Europe commanded a 32.45% share of the coffee roaster market, bolstered by 45,008 independent cafés and a robust equipment supply network in Germany, Italy, and Switzerland. The EUDR's push for batch-level traceability and stricter NOx caps is accelerating a shift towards electric models and retrofit kits. With municipal gas-connection bans in place, electric installations are set to surpass 40% of new setups by 2028, and hydrogen pilots are paving the way for broader low-carbon options. These developments are expected to reshape the market dynamics, encouraging manufacturers to innovate and align with sustainability goals.

Asia-Pacific is on a rapid ascent, boasting the highest CAGR of 7.34% through 2031. China's specialty coffee market surged by 18% in 2024, with tier-2 cities contributing to 60% of the new cafés. This growth reflects increasing urbanization and a rising middle class with a preference for premium coffee experiences. Meanwhile, India's organized café sector is gearing up to double its outlets by 2028, driven by expanding disposable incomes and evolving consumer preferences. Many café operators begin with pre-roasted beans but transition to in-house roasting after a couple of years, driving a steady demand for 15–50 kg machines. In Southeast Asia, countries like Indonesia and Thailand are ramping up mid-capacity purchases, spurred by deepening domestic consumption and import tariffs on finished coffee that promote local roasting. These trends highlight the region's growing emphasis on self-reliance and value addition within the coffee supply chain.

North America, while mature, witnesses a surge in micro-roasteries and tech upgrades at larger contract plants, all aiming for energy efficiency and data integration.According to National Coffee Association it is revealed that about 81% of past-day coffee drinkers had coffee at-home as of 2024[3]Source: National Coffee Association, "The Fall 2024 National Coffee Data Trends," ncausa.org. The region's focus on sustainability and operational efficiency is driving investments in advanced roasting technologies. South America is shifting roasting closer to farms to capture added value; both Brazil and Colombia are opting for 100–300 kg energy-efficient drums tailored for export. This strategy not only enhances profitability but also strengthens the region's position in the global coffee market. The Middle East is channeling investments into upscale café concepts, favoring compact and visually striking roasters that align with the region's luxury-oriented consumer base. In Africa, demand is burgeoning in Ethiopia and Kenya, bolstered by development finance that champions local value addition. Despite infrastructure and financing hurdles, which temper wider adoption, successful pilot projects signal a promising growth trajectory. These initiatives are gradually building a foundation for long-term market expansion in the region.

Competitive Landscape

The coffee roaster market shows signs of moderate consolidation. Industrial lines exceeding 200 kg are dominated by German and Swiss manufacturers, who bundle installation and service packages to provide comprehensive solutions. Meanwhile, regional firms in Turkey, South Korea, and the U.S. are carving out a niche in the sub-50 kg batch class, offering modular chassis and subscription maintenance plans. These strategies significantly reduce upfront costs, making them attractive to micro-roasters and small-scale businesses.

Technology stands out as a key differentiator in this market. IoT data platforms are capitalizing on predictive maintenance, enabling manufacturers to offer proactive service solutions that minimize downtime. Additionally, patents in heat-recovery and induction heating are driving innovation, reducing energy payback periods to under two years and enhancing operational efficiency. Meeting ISO 9001 and ISO 14001 standards acts as a critical gatekeeper for suppliers targeting multinational beverage brands, thereby elevating entry barriers and ensuring quality and environmental compliance. There's untapped potential in portable nano-roasters and hydrogen-ready burners. These categories remain underdeveloped by established players, presenting start-ups with an opportunity to establish niche leadership and cater to emerging market demands. If stainless-steel shortages persist, the market may witness increased consolidation, as smaller fabricators struggle to secure raw materials at competitive contract prices, potentially leading to a reshaping of the competitive landscape.

Strategic maneuvers highlight market divergence and innovation. Bühler is collaborating on hydrogen burners, which are scheduled for a late 2026 debut, aiming to address the growing demand for sustainable energy solutions. Giesen has launched a 15 kg induction roaster specifically designed for EU gas-phase-out markets, aligning with regional regulatory shifts. PROBAT has invested USD 22 million to expand its electric-roaster production capacity, signaling a strong commitment to electrification. Loring's recent achievement of securing a 25-unit contract marks its largest single electric order to date, underscoring institutional acceptance of high-capacity electric systems and their growing role in the market. Italian firms are partnering with IoT providers to enhance software capabilities and improve traceability, ensuring compliance and transparency in supply chains. Meanwhile, U.S. companies are rolling out subscription maintenance plans to deepen recurring revenue streams, providing customers with cost-effective and reliable service options.

Coffee Roaster Industry Leaders

-

Bühler AG

-

Giesen Coffee Roasters

-

Loring Smart Roast Inc.

-

IMF S.r.l.

-

PROBAT-Werke von Gimborn Maschinenfabrik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stronghold, a South Korean roaster-maker, has unveiled its latest offering: the S8X, a commercial coffee roasting machine boasting a 4.5-kilo capacity. This new model joins the ranks of the company's existing lineup, which includes the 850-gram-capacity S7 and the production-focused 8-kilo-capacity S9. The S8X comes with a priced at USD 38,000.

- May 2025: Roest, a Nordic roaster maker, unveiled its flagship sample roaster, the L100 Ultra, at last month's SCA Expo in Houston. Building on the technology and design of its predecessors, the original Roest (formerly Røst) and the S100 and L100 lines, the new 200-gram-capacity L100 Ultra has a touchscreen interface. Additionally, the machine is equipped with a motor enabling reverse drum rotation and several enhancements for better airflow.

- April 2024: Bellwether Coffee unveiled an affordable electric shop roaster. This compact, ventless commercial roaster is specifically designed to seamlessly integrate into any retail space, making it an ideal solution for businesses with limited room. It offers the capability to roast hundreds of pounds of coffee weekly, catering to the needs of high-demand operations.

- February 2024: Sweet Coffee Italia, an Italian company specializing in roasting equipment, has unveiled its new line of electric-heat commercial machines, branded as Gemma Induction. The Gemma Induction lineup features five models, with capacities spanning from 2 to 120 kilograms. These machines utilize induction heating, where a traditional perforated stainless steel drum is housed within an extra cylindrical chamber, completely surrounded by electromagnetic induction coils.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the coffee roaster market as all new, factory-built roasting machines, drum, hot-air, fluid-bed, stove-top, and hybrid, sold to industrial plants, HoReCa chains, specialty cafes, and retail equipment dealers worldwide. Each unit is valued at the first sale price of the fully assembled roaster, irrespective of burner type or automation level.

Scope Exclusions: The numbers exclude refurbished or second-hand machines and ancillary post-roast equipment such as destoners, grinders, or afterburners.

Segmentation Overview

-

By Roaster Type

- Drum

- Hot-Air/Fluid-Bed

- Stove-Top

- Hybrid and Other Types

-

By Category

- Electric Roasters

- Gas Roasters

-

By Automation Level

- Manual

- Semi-Automatic

- Fully Automatic (PLC/IoT-enabled)

-

By End User

- HoReCa

- Retail

- Industrial/Commercial

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed roaster OEM engineers, plant managers at multinational coffee processors, procurement heads of café chains across Europe, North America, and Asia, and distributors serving micro-roaster start-ups. Conversations tested average selling prices, replacement cycles, and regional emission-control costs, then fine-tuned model assumptions.

Desk Research

We began with open datasets on global trade in machinery classified under HS 841981 and HS 851679, drawing shipment values and volumes from UN Comtrade, Eurostat PRODCOM, and USITC. Industry output tables from the International Coffee Organization, the National Coffee Association, and Brazil's CONAB guided green-bean availability and roast-capacity ratios. Technology adoption trends were sourced from patent filings (Questel) and sustainability regulations outlined by the EU BAT directives. Company financials collected via D&B Hoovers and news checks on Dow Jones Factiva clarified revenue splits by equipment line. These examples illustrate, rather than exhaust, the secondary material consulted.

Market-Sizing & Forecasting

A top-down demand pool was reconstructed from new-build production data, import-export balances, and roaster replacement rates. Results are cross-checked through selective bottom-up rolls of supplier shipments and sampled ASP × unit calculations, which adjust totals where under-reporting is detected. Key model inputs include green-bean consumption per capita, café outlet expansion counts, average drum capacity installed per facility, energy cost differentials between gas and electric systems, and specialty-coffee penetration levels. Multivariate regression with ARIMA overlays projects each variable, while scenario analysis captures regulatory or commodity-price shocks. Any data void in bottom-up checks is bridged with conservative interpolation from adjacent capacity bands before the final triangulation.

Data Validation & Update Cycle

Outputs pass a two-step analyst review: variance screens against historical ratios followed by peer sign-off. We refresh every twelve months and reopen the model mid-cycle if material events, trade tariffs, landmark technology launches, or force-majeure supply disruptions, shift the baseline.

Why Mordor's Coffee Roaster Baseline Earns Stakeholder Confidence

Published figures on this market often diverge because different firms count only certain roaster sizes, convert currencies at outdated averages, or apply blanket CAGRs to fill data gaps.

Key gap drivers stem from (a) narrower geographic cuts that ignore high-growth Southeast Asian demand, (b) omission of electric fluid-bed units now popular with carbon-neutral cafes, and (c) less frequent refresh cadences that miss post-pandemic café build-outs. Mordor Intelligence integrates all machine classes, reconciles values in constant 2025 USD, and applies annual source audits, so our totals sit higher yet remain fully traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.52 B (2025) | Mordor Intelligence | - |

| USD 1.35 B (2023) | Global Consultancy A | excludes household-scale fluid-bed units and converts at spot FX without inflation rebasing |

| USD 1.14 B (2025) | Trade Journal B | models only drum roasters sold into commercial channels, omits industrial replacements |

| USD 1.46 B (2024) | Research Publisher C | relies on import statistics, does not add domestic production from Europe and China |

In short, buyers gain a balanced, transparent baseline from Mordor Intelligence because our numbers emerge from clearly logged variables, multi-angle validation, and an annual refresh that keeps assumptions aligned with real-world factory orders and cafe expansion plans.

Key Questions Answered in the Report

What is the current value of the coffee roaster market?

The coffee roaster market size is USD 2.72 billion in 2026 and is forecast to reach USD 3.63 billion by 2031.

Which region leads coffee roaster sales today?

Europe holds 32.45% of 2025 revenue due to its dense specialty-coffee network and advanced roasting infrastructure.

Which roaster type is most popular among industrial operators?

Drum roasters dominate with 56.01% market share in 2025 because they scale efficiently above 500 kg batches.

How fast is the HoReCa segment growing?

Hotels, restaurants, and cafés are projected to expand at a 7.60% CAGR as experiential retail models install on-premise roasting.