Cocoa Beans Market Size and Share

Cocoa Beans Market Analysis by Mordor Intelligence

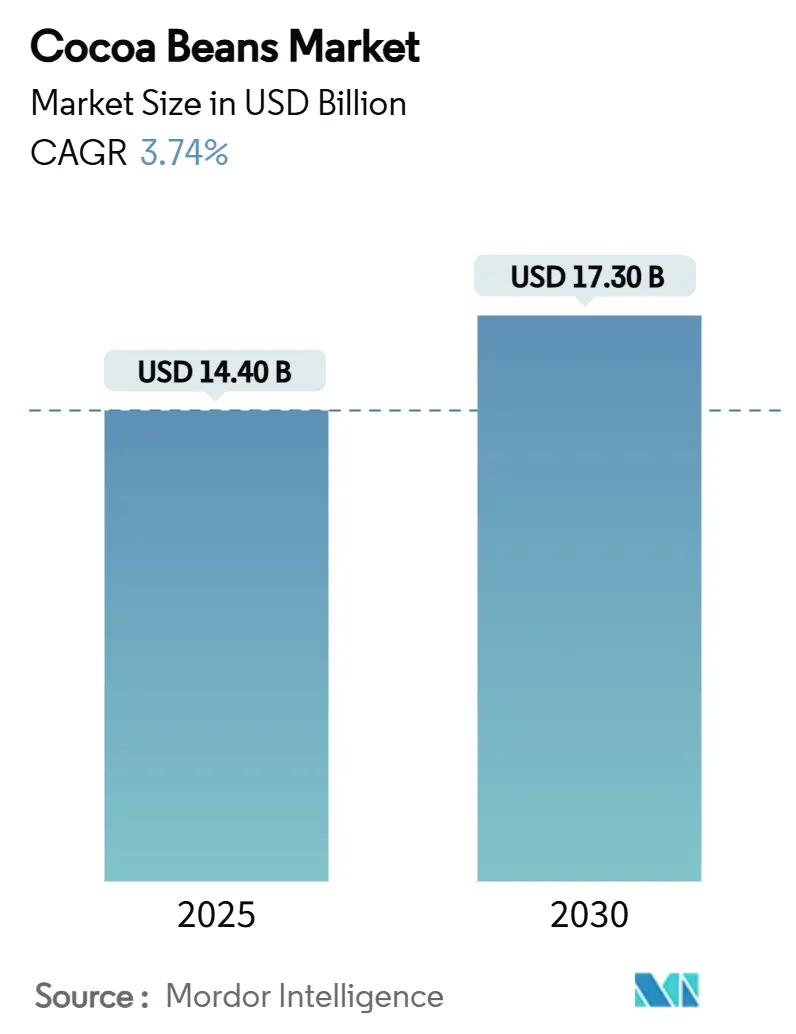

The Cocoa Beans Market size is estimated at USD 14.40 billion in 2025, and is expected to reach USD 17.30 billion by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

The market maintains stable growth, supported by Europe's processing capacity, production challenges in West Africa, and increasing premium consumption in North America. Processors are investing in traceability systems to meet deforestation regulations, while implementing AI-based agricultural solutions to enhance yields in climate-vulnerable regions. The growing ready-to-drink (RTD) beverage segment expands market opportunities beyond confectionery, particularly for processors supplying polyphenol-rich ingredients.

Key Report Takeaways

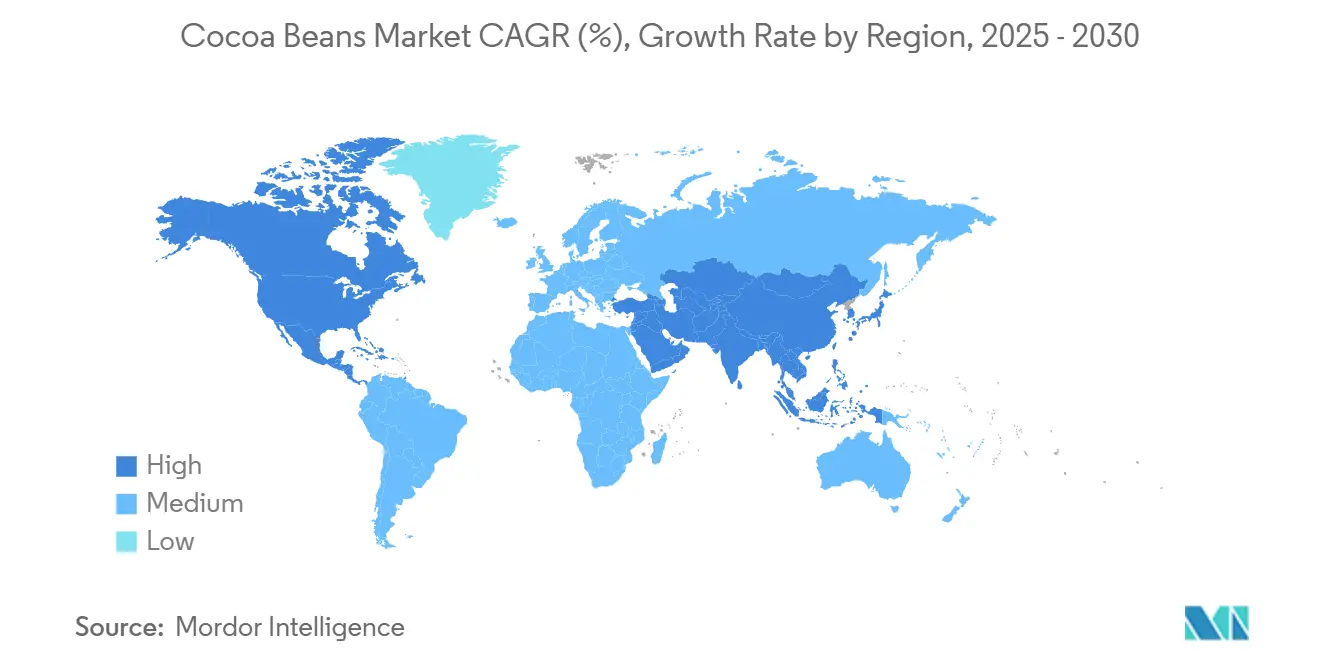

- By geography, Europe led with 45% of the cocoa bean market share value in 2024, while North America is projected to expand at a 7.2% CAGR through 2030.

Global Cocoa Beans Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Cocoa Beans in the Chocolate Industry | +1.5% | Global, with highest impact in Europe and North America | Long term (≥ 4 years) |

| Increasing Adoption of Advanced Farming Technologies | +0.8% | West Africa, South America, Asia-Pacific | Medium term (2-4 years) |

| Supportive Government Initiatives | +0.6% | Ghana, Côte d'Ivoire, Indonesia, Brazil | Medium term (2-4 years) |

| Functional RTD Cocoa Beverages Driving Polyphenol Ingredient Uptake | +0.4% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Cocoa Beans in the Chocolate Industry

The global premium chocolate market is growing due to product innovation and advanced manufacturing technologies. Affluent consumers seek products with clean-label ingredients, traceable sourcing, minimal toxicity, and specific sensory characteristics. Manufacturers are expanding their portfolios across dark, milk, and white chocolate categories with diverse flavors, fillings, and formats, including vegan and low-sugar variants. This diversification attracts more consumers and increases cocoa bean demand. Companies continue to develop new products to capitalize on the cocoa beans market potential. In 2024, the Hershey Company, North America's largest premium chocolate manufacturer, introduced Hershey's Choco Delights, a milk chocolate bar with melt-in-mouth crunchy pieces.

Increasing Adoption of Advanced Farming Technologies

Technological advancements are transforming cocoa bean farming through improved efficiency, sustainability, and productivity. Precision farming tools, including sensors, drones, and satellite imaging, enable farmers to monitor soil health, weather conditions, and crop status, supporting informed decisions for planting, irrigation, fertilization, and pest control. Kerala Agricultural University in India introduced a cocoa bean extractor in 2023 under the ICAR AICRP project. The machine features a hopper, metallic roller assembly, rotating cylindrical strainers, and a frame assembly to optimize cocoa pod processing. This development reduces manual labor requirements, decreases worker injuries, and increases productivity while maintaining bean quality. Lutheran World Relief launched Cacao Movil in 2024, a mobile application for South American cocoa farmers that provides interactive training modules and tutorials on improved farming methods. The application enables farmers in remote areas to access agricultural information without formal training.

Supportive Government Initiatives

Governments worldwide have implemented programs to enhance cocoa bean production, focusing on sustainability, farmer welfare, and environmental protection. The Cote d'Ivoire government allocated USD 16.75 million annually from 2024 for four years to support small exporters facing challenges in securing financing from local banks. This initiative enables them to compete with international entities and is anticipated to increase their annual cocoa bean purchasing capacity by more than double. The Malaysian government also allocated USD 2.13 million in 2024 to revitalize cocoa projects, aiming to increase local cocoa bean production and strengthen its position in the global cocoa market.

Functional RTD Cocoa Beverages Driving Polyphenol Ingredient Uptake

The functional beverage market drives demand for cocoa-derived ingredients, specifically polyphenols, which offer antioxidant and cardiovascular benefits. Ready-to-drink products containing cocoa-derived ingredients are growing in popularity, especially in North America, where manufacturers use cacao beans as natural caffeine sources instead of synthetic alternatives in energy and wellness drinks. This market shift enables ingredient suppliers to develop specialized cocoa extracts for functional applications, creating opportunities in premium market segments that demonstrate lower price sensitivity compared to traditional chocolate manufacturing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disease Outbreaks and Climate Challenges in Cocoa Bean Production | -1.2% | West Africa, particularly Côte d'Ivoire and Ghana | Medium term (2-4 years) |

| Emergence of Cocoa Bean Substitutes in the Market | -0.4% | Global, with initial impact in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Disease Outbreaks and Climate Challenges in Cocoa Bean Production

Disease outbreaks significantly affect global cocoa bean production and yield. In 2023, Ghana's Western North region faced a severe outbreak of swollen shoot disease that affected 330,456 hectares out of the total 410,229 hectares, representing 81% of the area.[1]CBI, Ministry of Foreign Affairs The virus, transmitted by mealybugs, reduces cocoa yields and ultimately kills the trees, requiring complete removal and soil treatment before replanting. Additionally, black pod disease, caused by Phytophthora species, impacts cocoa production across West Africa, particularly in Ivory Coast and Ghana. The prevalent wet and humid conditions have created favorable environments for this fungal disease, which causes pod rot and substantial crop losses.

Emergence of Cocoa Bean Substitutes in the Market

The development of substitute cocoa bean products has accelerated in recent years. Food manufacturers are exploring alternatives to cocoa beans in response to price volatility, supply chain disruptions, and changing consumer preferences. These substitutes aim to replicate cocoa's flavor, texture, and functionality across various applications, which may impact traditional cocoa product demand. In May 2024, Voyage Foods launched a cocoa-free chocolate alternative that uses grape seeds, a wine production byproduct, combined with vegetable oil, cane sugar, sunflower protein flour, natural flavors, sunflower lecithin, and salt. The growth of these substitutes may create competitive pressure, particularly in mass-market applications where flavor profiles can be more easily replicated.

Geography Analysis

Europe maintains a 45% share of the global cocoa bean processing market despite pressures from high bean prices and compliance costs. Major European processors are implementing blockchain-based traceability systems, with Barry Callebaut implementing end-to-end digital tracking from farm to factory.[2]International Cocoa Organization While ports in Amsterdam and Antwerp provide cost advantages, reduced stockpiles, and increased energy costs affect profit margins. The market benefits from high consumer awareness of sustainability, with retail assortments focusing on ethically certified products, maintaining premium segment strength despite mid-range segment contraction.

North America projects a 7.2% CAGR through 2030, reflecting market diversification. The market sees increased launches of functional beverages using cocoa extracts as natural stimulants across grocery and convenience stores. U.S. processing capacity has increased by 8% annually, driven by mid-sized grinders focusing on small-batch, flavor-specific liquors for craft chocolate production. Companies respond to high cocoa prices through different strategies, such as reducing product sizes and modifying formulations, or maintaining high cocoa content to protect brand value. These approaches balance volume reduction with value growth in the cocoa bean market.

Asia-Pacific and South America are expanding their presence in the cocoa supply chain. Brazil aims to double production by 2030 through large-scale estates with mechanized operations and disease-resistant varieties. Indonesia uses its geographical advantages and government incentives to attract processors seeking proximity to its origin. This regional expansion in production and processing reduces global dependence on West African supplies. New port facilities in Pará and Sulawesi reduce transportation times to Asian confectionery manufacturing centers, decreasing freight risks and ensuring better bean quality upon delivery.

Recent Industry Developments

- February 2025: Guan Chong Berhad (GCB), a Malaysian producer of cocoa-derived food ingredients agreed to acquire a 25% stake in Transcao Côte d'Ivoire, bolstering local processing capacity at the world’s largest origin.

- January 2025: Mars, Incorporated announced a commitment to support 14,000 cocoa farmers in Côte d'Ivoire and Indonesia towards achieving a sustainable living income by 2030 as part of their Cocoa for Generations strategy, which has already invested USD 1 billion in sustainable cocoa initiatives.

- January 2025: Olam Food Ingredients (ofi) set new targets to enhance regenerative agriculture in cocoa, aiming for over a million hectares under such practices by 2030, including planting 15 million trees and establishing seven landscape partnerships.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cocoa beans market as the value of whole, fermented and dried beans of Theobroma cacao that enter formal trade channels for onward processing into liquor, butter, or powder. Coverage spans production, trade, and apparent consumption in value (USD) and volume terms across five broad regions.

Explicitly excluded are downstream chocolate confectionery, intermediate derivatives sold separately, and any beans moving through purely informal barter chains.

Segmentation Overview

- By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- North America

- United States

- Canada

- Europe

- Germany

- Netherlands

- United Kingdom

- France

- Belgium

- Russia

- Asia-Pacific

- India

- Malaysia

- Indonesia

- Singapore

- Japan

- South America

- Brazil

- Ecuador

- Middle East

- United Arab Emirates

- Saudi Arabia

- Iran

- Africa

- Ghana

- Uganda

- Nigeria

- Cote D'lvoire

- Cameroon

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with farm-gate aggregators in Côte d'Ivoire and Ghana, mid-stream grinders in the Netherlands and Malaysia, and procurement managers at beverage innovators in the United States allow us to test secondary ratios, sense-check unit prices, and refine yield loss and contract premium assumptions that desktop work alone cannot surface.

Desk Research

During desk research, we draw first on high-credibility, open datasets such as FAOSTAT crop balances, UN Comtrade trade codes 1801 and 1803, International Cocoa Organization quarterly bulletins, and price series from the World Bank Commodities database. Alongside public statistics, our team screens scholarly journals on plant science and climate resilience, plus policy notes from ECOWAS and the European Parliament that frame sustainability and traceability rules affecting bean flows.

Company annual reports, IPO filings, and audited processor capacity disclosures supply conversion yields and utilization benchmarks, which are then contrasted with shipment-level insights gathered through D&B Hoovers and Volza. The sources named are illustrative; many further records inform data collection, validation, and clarification.

Market-Sizing & Forecasting

For quantification, we apply a top-down production and trade reconstruct: starting with harvested tonnage, subtracting farm losses, and valuing the clean bean pool at region-specific average selling prices. Results are corroborated through selective bottom-up roll-ups of grinder capacity and sampled average selling price multiplied by volume invoices, which help us adjust for unreported artisan flows. Key variables feeding the model include hectare yields, certified-bean penetration, terminal exchange prices, grind-to-press ratios, and regional dark-chocolate share of confectionery demand. Scenario analysis coupled with multivariate regression against GDP per capita and retail chocolate spend projects the market from 2025 to 2030. Where bottom-up evidence lags, interpolation is guided by three-year moving averages of ICCO stock-to-grind ratios.

Data Validation & Update Cycle

Before finalization, Mordor analysts run variance checks against ICCO supply balances and customs data outliers, escalate anomalies for peer review, and document every adjustment. Reports refresh annually, with interim updates triggered by material events such as extreme price shocks or regulatory changes; a fresh analyst pass occurs just prior to delivery so clients receive the latest view.

Why Mordor's Cocoa Beans Baseline Commands Reliability

Published estimates often diverge because firms choose different bean definitions, price assumptions, and refresh cadences. According to Mordor Intelligence, anchoring the baseline in physically traded beans and vetting price series directly with grinders keeps our figure grounded and repeatable.

The main spread in values arises when other publishers fold in derivatives, apply constant-currency conversions, or extrapolate aggressive premium penetration without validating certified-bean supply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.40 B (2025) | Mordor Intelligence | - |

| USD 13.54 B (2023) | Global Consultancy A | Includes cocoa butter and powder revenues; older base year; currency fixed at 2023 rates |

| USD 13.67 B (2024) | Regional Consultancy A | Assumes uniform farm-gate prices, limited grinder interviews, and no stock reconciliation |

| USD 14.60 B (2025) | Trade Journal B | Mixes organic and conventional beans yet applies a single price curve; excludes re-exports |

Taken together, the comparison shows that Mordor's disciplined scope selection, live price validation, and balanced triangulation provide a dependable decision-making baseline for stakeholders seeking clarity in a highly volatile commodity landscape.

Key Questions Answered in the Report

What is the current size of the cocoa bean market?

The cocoa bean market stands at USD 14.4 billion in 2025 and is on track to reach USD 17.3 billion by 2030.

Which region currently leads the cocoa bean production?

Africa, particularly West Africa, dominates global cocoa bean production, with Côte d'Ivoire and Ghana collectively accounting for approximately 60% of worldwide output.

What technologies are improving cocoa farming yields?

Satellite imagery, IoT sensors, and AI analytics enable precision nutrient management and early disease detection, boosting yields up to 20% in field trials.

Are cocoa bean substitutes a real threat to traditional producers?

Cocoa-free formulations and lab-grown cocoa are still costly but could become price-competitive within ten years, especially for mass-market chocolate.

Page last updated on: