Cloud Gaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

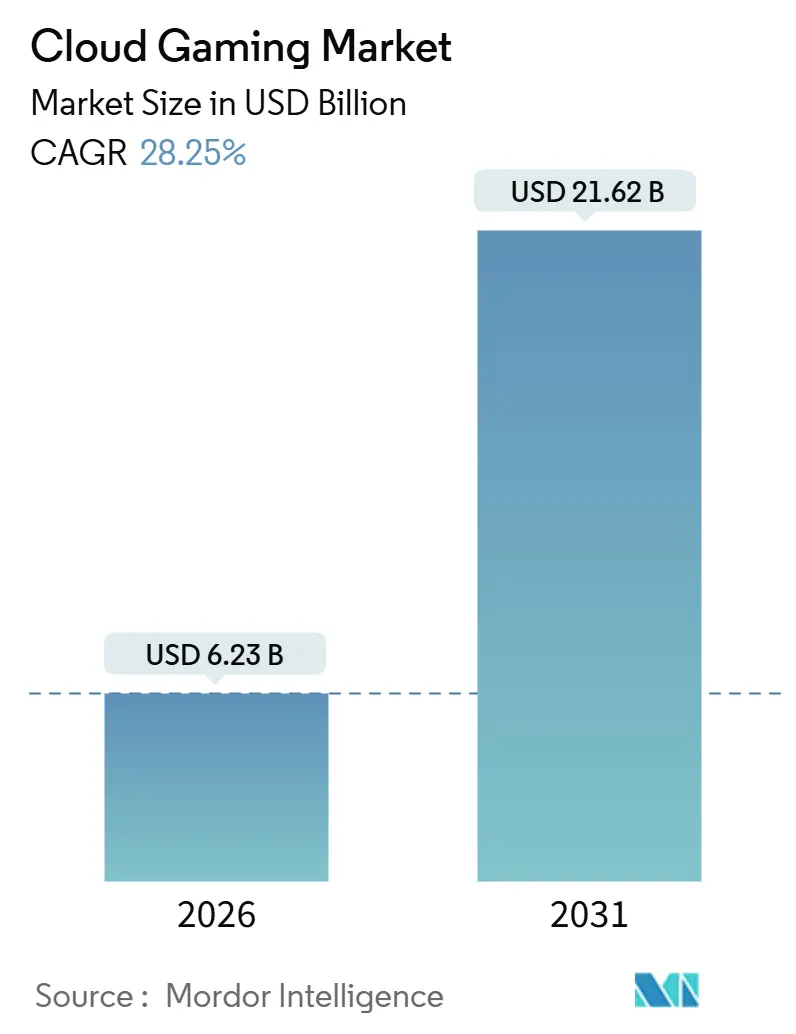

| Market Size (2026) | USD 6.23 Billion |

| Market Size (2031) | USD 21.62 Billion |

| Growth Rate (2026 - 2031) | 28.25% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

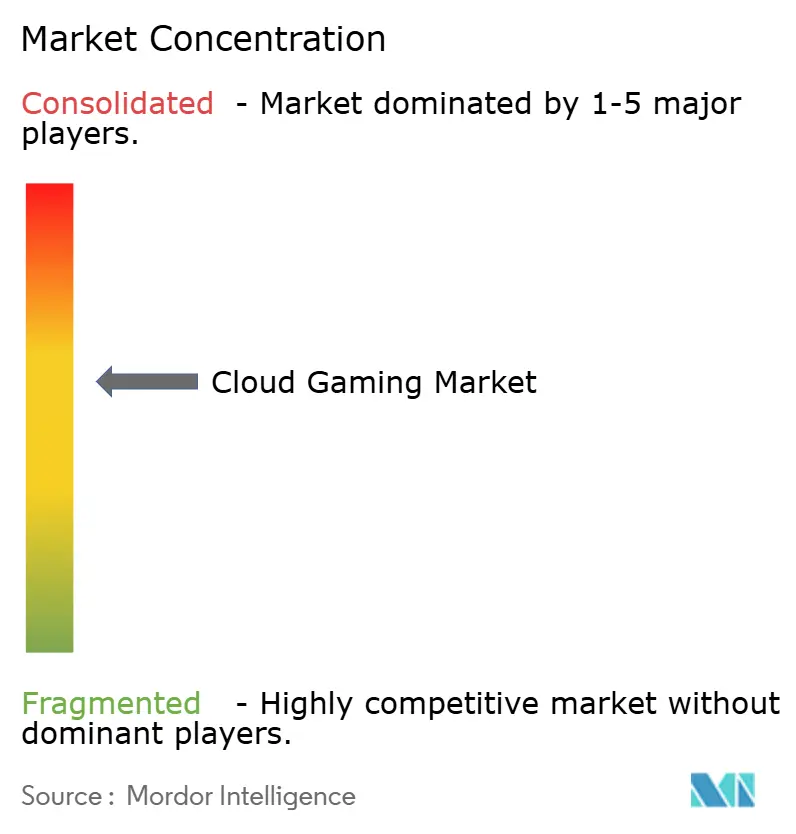

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Gaming Market Analysis by Mordor Intelligence

The cloud gaming market size stood at USD 6.23 billion in 2026 and is projected to reach USD 21.62 billion by 2031, reflecting a robust 28.25% CAGR. Rapid 5G and edge rollouts, publisher adoption of cloud-first releases, and generative AI compression have combined to push average round-trip latency below the 20-millisecond threshold in many metro areas, enabling premium gameplay on low-power devices. Platform holders are expanding regionally. Microsoft launched Xbox Cloud Gaming in India, Brazil, and Argentina in late 2025, while Sony launched PlayStation Portal streaming across 30 countries, illustrating a strategic shift toward geographic diversification. Telcos are bundling services to lift average revenue per user, and Asia Pacific remains the largest regional contributor, buoyed by Reliance Jio and Tencent initiatives.

Key Report Takeaways

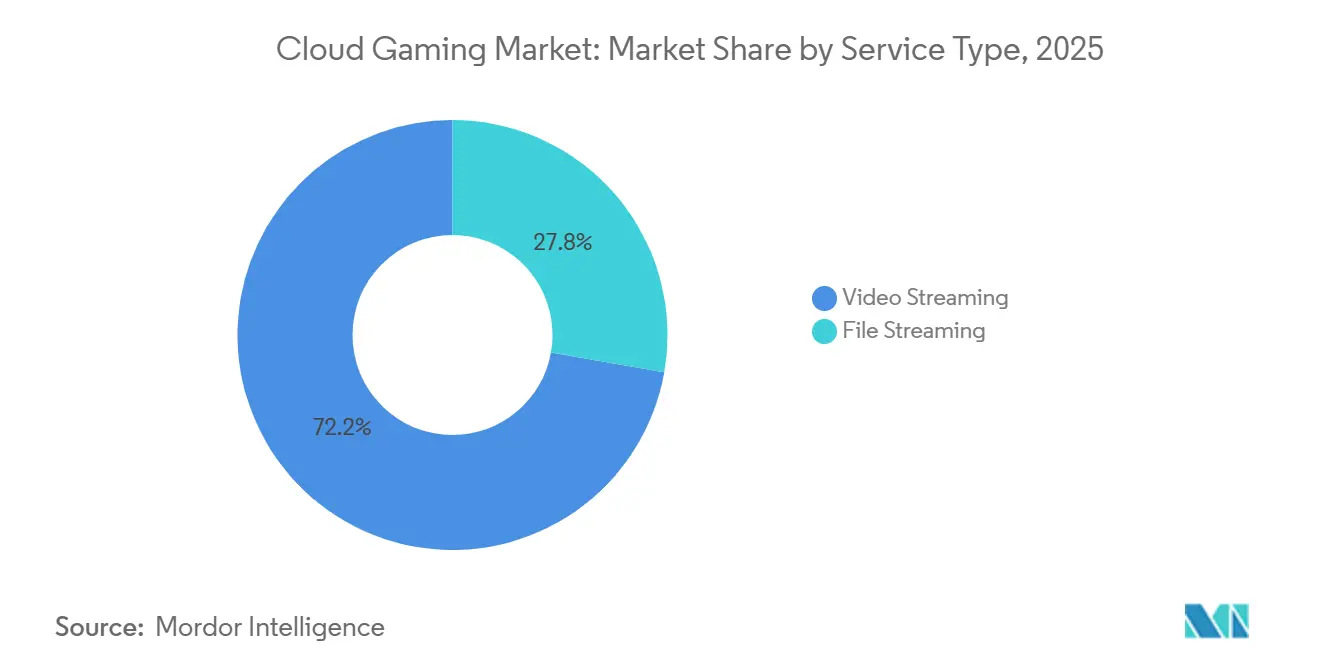

- By service type, video streaming led with 72.22% revenue share in 2025, while file streaming is advancing at a 28.71% CAGR through 2031.

- By device, smartphones held 46.12% of the cloud gaming market share in 2025, whereas tablets are forecast to expand at a 28.61% CAGR to 2031.

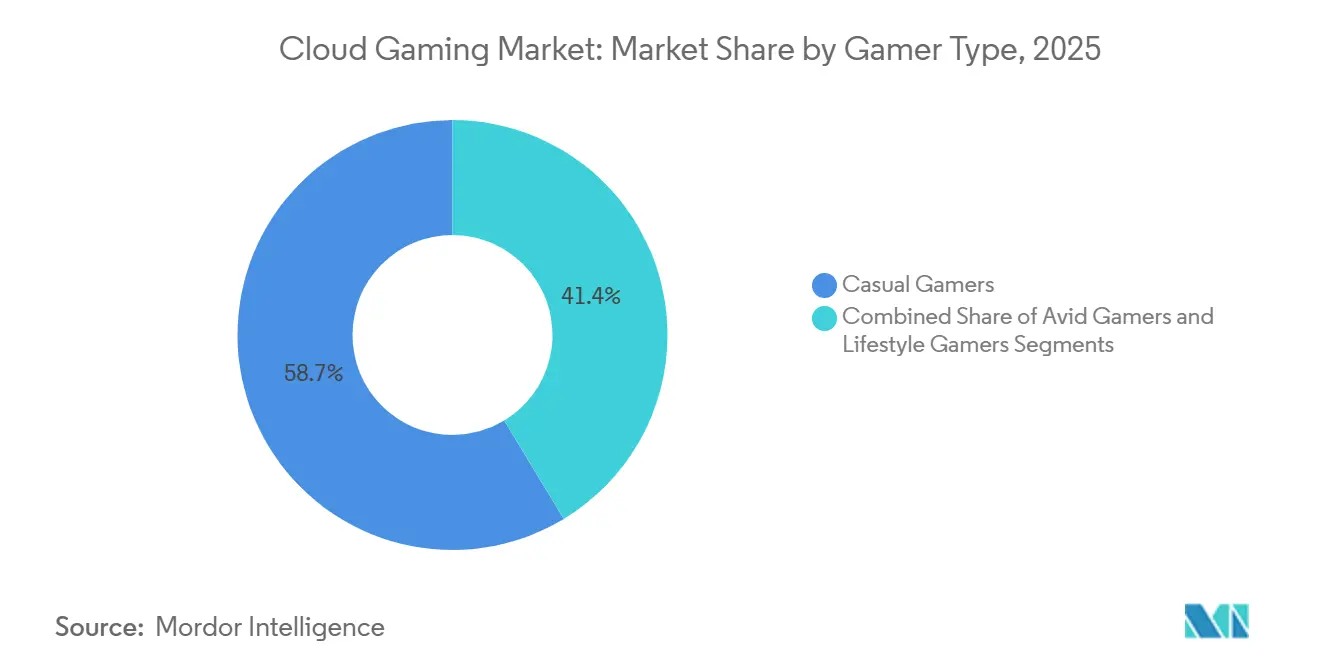

- By gamer type, casual gamers accounted for 58.65% of the cloud gaming market size in 2025, and lifestyle gamers are tracking a 29.01% CAGR into 2031.

- By business model, subscription plans captured 64.83% of revenue in 2025; free-to-play and ad-supported tiers are set to grow at a 29.15% CAGR through 2031.

- By geography, Asia Pacific commanded 38.45% of the cloud gaming market share in 2025, while the Middle East and Africa represent the fastest-growing region at a 29.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Cloud Gaming Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G and edge roll-outs unlocking low-latency gameplay | +6.2% | Asia Pacific, North America | Medium term (2-4 years) |

| AAA publishers adopting cloud-first distribution | +5.8% | Global | Medium term (2-4 years) |

| Telco gaming bundles monetizing mobile data plans | +4.5% | Asia Pacific, the Middle East and Africa, and South America | Short term (≤ 2 years) |

| Generative-AI compression cuts bandwidth costs | +3.9% | Global | Long term (≥ 4 years) |

| Growth of cross-platform and device-agnostic gaming | +3.2% | Global | Medium term (2-4 years) |

| Increasing penetration of smart TVs and connected devices | +2.7% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G and Edge Roll-outs Unlocking Low-Latency Gameplay

Multi-access edge computing nodes now place rendering servers within city limits, letting carriers deliver sub-15-millisecond round-trip times for titles such as Forza Horizon 5. Verizon’s partnership with AWS Wavelength in the United States and Bridge Alliance’s unified edge platform across Southeast Asia have proved that reducing backhaul hops immediately boosts session quality.[1]Verizon Editorial Staff, “5G Edge Computing Solutions,” Verizon, verizon.com GSMA Intelligence counted more than 1.2 billion 5G connections in the Asia Pacific in 2025, while Ericsson ConsumerLab reported that 68% of cloud gamers rank latency as the single most important satisfaction driver. Together, these factors convert casual mobile users into paying subscribers, particularly in bandwidth-intensive genres such as battle royales and racing simulators.

AAA Publishers Adopting Cloud-First Distribution

Publishers are launching marquee franchises simultaneously on cloud and traditional consoles to reach non-console owners. At GDC 2025, Microsoft revealed 140 million cumulative streaming hours, with over one-third of those coming from devices unable to run the content locally. Ubisoft and Tencent created a EUR 4 billion (USD 4.28 billion) subsidiary to push Assassin’s Creed and Rainbow Six directly to cloud players in Asia, bypassing physical disc sales. Amazon Luna’s multiyear pact with Electronic Arts places Star Wars Jedi: Survivor day-and-date inside the Prime bundle, cementing the expectation of instant access. Boston Consulting Group estimates that cloud-first launches widen the potential paying audience by 40%.

Telco Gaming Bundles Monetizing Mobile Data Plans

Connectivity providers are differentiating commoditized data plans by embedding premium titles. Reliance Jio offers unlimited Xbox Cloud Gaming traffic for subscribers paying INR 1,499 (USD 18) or more per month, while Zain KSA waived six months of GeForce NOW fees and increased postpaid conversions by 22%. It notes incremental monthly ARPU gains of USD 3 to USD 5, while Kearney reports an 18% reduction in subscriber churn among 18- to 34-year-olds. The model works because telcos already own last-mile infrastructure, making content bundling a low-marginal-cost upsell.

Generative-AI Compression Cutting Bandwidth Costs

SimaBit’s neural codec demonstrated 40% lower bitrates at comparable visual fidelity, reducing 1080p requirements from 15 Mbps to 9 Mbps and slashing one of the largest operating costs for smaller services. Nvidia’s RTX Video Super Resolution shifts upscaling to client devices, reducing data-center egress by 35% while still producing 1440p images. Peer-reviewed IEEE studies show transformer-based techniques surpassing the H.265 standard for motion-heavy gameplay. Over a five-year horizon, AI codecs could extend service reach into bandwidth-constrained emerging markets.

Restraints Impact Analysis of Cloud Gaming Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural latency bottlenecks in South America and Africa | -3.8% | South America, Sub-Saharan Africa | Long term (≥ 4 years) |

| High cloud-GPU rental costs are limiting indie platforms | -2.9% | Global | Medium term (2-4 years) |

| Content-licensing barriers to cross-border expansion | -1.7% | Europe | Medium term (2-4 years) |

| Data-usage caps and bandwidth restrictions | -1.4% | North America, select Asia Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rural Latency Bottlenecks in South America and Africa

The World Bank found that only 35% of Sub-Saharan Africa had 4G access in 2024, and that median latency exceeded 80 milliseconds, making competitive titles unplayable. GSMA data shows that 5G coverage reached just 12% of South America’s population in 2025, largely confined to São Paulo, Buenos Aires, and Santiago. Brazil’s telecom regulator recorded rural fixed-broadband speeds below 10 Mbps, further limiting service quality. Infrastructure shortfalls effectively cap the cloud gaming market in vast interior regions, delaying uptake by several years.

High Cloud-GPU Rental Costs Limiting Indie Platforms

Spot pricing for Nvidia H100 GPUs on AWS and Azure averaged USD 2.50 to USD 3.00 per hour in 2025, translating to USD 1,800 per month at full utilization. CoreWeave reported gross margins of just 22% on gaming workloads, versus 35% on AI inference, steering scarce GPU capacity toward higher-margin customers. Smaller services like Shadow and Blacknut therefore impose waitlists during peak hours, eroding user satisfaction. Unless wholesale GPU prices ease or demand elasticity allows higher pay-as-you-play fees, indie platforms will struggle to scale globally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cloud Gaming Market Segment Analysis

By Service Type:

File Streaming Gains on Install-to-Play FeaturesFile streaming captured momentum after Nvidia introduced install-to-play in September 2025, blending local asset storage with remote rendering and cutting perceived input lag to under 10 milliseconds for esports titles. Although video streaming still dominated with 72.22% of revenue in 2025, performance-sensitive gamers now gravitate toward hybrid delivery, driving a 28.71% CAGR for file streaming through 2031.

Academic work in the ACM Transactions on Graphics found 60% lower bandwidth use in static environments, validating the cost-benefit. The cloud gaming market, therefore, splits between casual players who value device agnosticism and enthusiasts who prioritize responsiveness. Install-to-play also lays the groundwork for emerging mixed-reality titles that require rapid asset swapping, expanding the overall cloud gaming market size by unlocking new content formats.

By Device:

Tablets Surge on Virtualization and PortabilityTablets are poised for a 28.61% CAGR, as Xiaomi’s WinPlay engine enables ARM-based devices to run Windows and Steam apps via virtualization, closing the content gap with PCs.[2]Xiaomi Global Communications, “WinPlay Engine Launch,” Xiaomi, mi.com Logitech sold 500,000 G Cloud handhelds in 2025, signalling pent-up demand for all-day battery life and physical controls. Smartphones will continue to contribute nearly half of 2026 revenue thanks to telco bundles, but tablets combine portability with larger screens, improving immersion for live-service games.

As vendors add detachable controllers and 144 Hz displays, the cloud gaming market share held by tablets is expected to close the gap with phones. Manufacturers are segmenting aggressively from high-refresh-rate OLED handhelds to entry-level Android slates, diversifying hardware options without fragmenting cloud infrastructure.

By Gamer Type:

Lifestyle Gamers Drive Cross-Platform AdoptionCasual users held 58.65% of 2025’s base, yet lifestyle gamers, Gen Z players who emphasize social connectivity, are expanding at 29.01% CAGR. Super Gamers in the United States spend USD 38 per month and view cloud streaming as a frictionless way to access day-one releases.

As engagement shifts from hardware ownership to continuous service access, lifestyle gamers expand the cloud gaming market by persuading publishers to maintain live-service roadmaps, thereby ensuring fresh content and ongoing microtransactions. Casual players, meanwhile, benefit from periodic free-to-play promotions, keeping funnel conversion high during seasonal events.

By Business Model:

Ad-Supported Tiers Broaden the FunnelSubscription tiers accounted for 64.83% of 2025 revenue, but Amazon Luna’s inclusion within Prime and Microsoft’s ad-supported pilot signal a pivot toward lower entry prices. Free-to-play and ad-funded offerings are projected to grow at a 29.15% CAGR, adding millions of price-sensitive users in developing markets.

This diversification stabilizes revenue by balancing predictable subscription income with the upside from advertising and microtransactions. In parallel, pay-as-you-play options such as NetEase’s RMB 1.8 (USD 0.25) per-hour service target infrequent players who balk at recurring fees. All told, a multilayered pricing ladder encourages trial, upgrades, and retention, distributing risk across different spending cohorts.

Geography Analysis

APAC Cloud Gaming Market

Asia Pacific captured 38.45% of 2025 revenue, anchored by Reliance Jio’s Xbox integration and Tencent’s EUR 1.16 billion (USD 1.24 billion) Ubisoft investment, which cements the region as a cloud-first hub. India alone added more than 800 million smartphones and is on track to become the largest gaming territory by 2033. China’s local platforms, despite foreign licensing hurdles, generated USD 1.87 billion in revenue in 2024, illustrating domestic resilience.

MEA Cloud Gaming Market

The Middle East and Africa have the fastest trajectory, with a 29.35% CAGR through 2031. Saudi Arabia’s USD 38 billion Savvy Games Group investment and the United Arab Emirates’ push to host regional studios reduced regional dependence on imported content. MTN’s Cloudplay launch and Zain KSA’s bundling of GeForce NOW show that carrier-led approaches can leapfrog console scarcity. Increased data-center capacity across Gulf states has lowered latency below 30 milliseconds, a critical threshold for multiplayer shooters.

North America and Europe Cloud Gaming Market

North America and Europe retain high revenue per user, with the United States and Germany acting as early adopters of premium subscriptions. Microsoft’s partnership with Telcel in Mexico broadens Spanish-language catalogs, while European operators must navigate content-licensing mandates arising from the Activision Blizzard decision, which fragments libraries across borders.

Mordor Intelligence provides coverage of the cloud gaming market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Regulatory Landscape

Cloud gaming regulation is tightening around technical performance, consumer protection, and platform competition, with new standards increasingly used as compliance baselines for service quality and device capability. ITU-T approved Recommendation J.1311 in June 2024 (technical requirements for cloud gaming service platforms) and Recommendation J.1613 in December 2025 (capability framework for cloud gaming smart terminals), giving operators and OEMs shared reference points for platform and terminal design.

In 2026, country-level rulemaking and standards advanced further. India brought the Promotion and Regulation of Online Gaming Rules, 2026 into force on May 1, 2026, adding formal oversight expectations for online gaming services. In China, MIIT issued YD/T 6747-2026 in February 2026 (network quality evaluation metrics for cloud gaming, effective September 1, 2026) and MOPS issued GA 1277.17-2026 in February 2026 (security management requirements for online game services, effective July 1, 2026). Alongside NRTA technical requirement drafts that reference platform performance targets and minors-protection controls such as real-name authentication and time limits, these measures raise the bar for cross-border expansion and local operations. UK competition scrutiny also continues to shape distribution rules, with the Competition and Markets Authority publishing work on cloud gaming competition and app store requirements and maintaining remedies-centric approaches such as licensing commitments in high-profile gaming transactions.

Value Chain Analysis

The cloud gaming value chain begins with game developers and publishers providing content and rights, then cloud and edge infrastructure providers (AWS, Microsoft Azure, Google Cloud, Tencent Cloud) supplying compute, storage, and networking. Cloud gaming platforms (Microsoft, Sony, Nvidia, Blacknut, Ubitus) integrate streaming stacks, client apps, identity, billing, and content curation. Distribution commonly runs through telecom operators and device ecosystems, where carriers such as Reliance Jio, Zain KSA, and Sonatel bundle access and reduce customer-acquisition costs. End-user endpoints span smartphones, tablets, PCs, smart TVs, and dedicated handhelds.

Key cost and performance drivers sit in the middle of the chain: GPU availability and pricing, data-center egress, and last-mile latency. In 2025, spot pricing for Nvidia H100 GPUs on hyperscalers averaged about USD 2.50 to USD 3.00 per hour, and gaming workloads competed directly with higher-margin AI demand, pressuring smaller platforms with waitlists and constrained peak-hour capacity. Partnerships and licensing deals increasingly connect publishers and platforms to secure day-and-date cloud access (for example, Amazon Luna content bundling, Ubisoft and Tencent cloud-focused initiatives). Region-specific launches, such as Sonatel and Netgem launching Wido Games in February 2025, also show how telcos and local network reach function as gatekeeping assets for scaling in under-served geographies.

Competitive Landscape

The sector is moderately fragmented, with Microsoft, Sony, and Nvidia anchoring platform strategies. Microsoft expanded Xbox Cloud Gaming into populous emerging markets and began testing ad-funded tiers, diversifying both geography and price points. Sony leverages exclusive first-party franchises to entrench subscribers, launching PlayStation Portal streaming across 30 countries in November 2025. Nvidia’s GeForce NOW differentiates on hardware independence and frequent GPU upgrades, introducing RTX 5080 nodes for 1440p at 120 fps.

Telcos such as Reliance Jio and Zain KSA serve as distribution gatekeepers, bundling gaming traffic with higher-tier data plans while avoiding direct content acquisition costs. Independent aggregators Shadow, Blacknut, and Boosteroid address niches like bring-your-own-storefront libraries but face margin pressure because GPU rentals absorb up to 50% of operating budgets.

Intellectual-property access remains a strategic battleground. The European Commission imposed 10-year licensing guarantees on Microsoft’s Activision assets, raising compliance complexity but improving third-party content parity.[3] Vision 2030 Secretariat, “Savvy Games Investment Overview,” Vision 2030, vision2030.gov.sa Technology differentiation focuses on proprietary codecs, AI upscaling patents, and cross-platform save states. First movers in edge nodes and generative compression gain defensible user-experience advantages that lower churn and raise switching costs.

Cloud Gaming Industry Leaders

Nvidia Corporation

Microsoft Corporation

Sony Group Corporation

Tencent Holdings Limited

Amazon.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Cloud Gaming Market Companies Covered in this Report

- Nvidia Corporation

- Microsoft Corporation

- Sony Group Corporation

- Tencent Holdings Limited

- Amazon.com, Inc.

- Alphabet Inc. (Google)

- Ubisoft Entertainment SA

- Electronic Arts Inc.

- Ubitus K.K.

- Shadow SAS

- Blacknut SAS

- Parsec Cloud Inc. (Unity Software Inc.)

- Utomik BV

- Numecent Holdings Ltd.

- Antstream Arcade Ltd.

- Vortex Cloud Gaming (RemoteMyApp Sp. z o.o.)

- Loudplay (Azerion)

- PlayGiga S.L. (Meta Platforms Inc.)

- Boosteroid Ltd.

- My.Games Cloud (VK Company Limited)

Market Opportunities and Future Outlook

Operator-led distribution and emerging-market onboarding remain key whitespace, particularly where hardware affordability and app-store friction limit premium gaming. India is a clear reference point: Vodafone Idea unveiled its Cloud Play platform in April 2024 in partnership with CareGame, and Microsoft expanded Xbox Cloud Gaming into India via carrier bundles in late 2025. Together, these steps reinforce the role of telcos as acquisition channels for low-power devices and prepaid-heavy user bases. Similar carrier-first models are active in MEA and West Africa, including Zain KSA bundles and Sonatel and Netgem's Wido Games, which supports demand for more localized catalogs, payment rails, and latency-optimized regional points of presence.

Infrastructure and performance engineering create a second opportunity layer as the industry formalizes latency and quality targets. Capacity additions in Europe, including Boosteroid expanding data center capacity in France, Poland, and the Czech Republic in July 2026, point to providers investing in regional footprints to tighten propagation delay and support more concurrent sessions. On the technology side, wider deployment of L4S (Low Latency, Low Loss, Scalable throughput) and the move toward tail-latency SLOs, alongside AI-assisted codecs and speculative rendering approaches documented in 2026 research, can support higher user density per GPU and reduce bandwidth costs. That is particularly relevant for ad-supported and pay-as-you-play tiers looking to expand beyond premium subscribers.

Recent Industry Developments in Cloud Gaming Market

- July 2026: NVIDIA launched GeForce NOW in India on July 15, 2026, moving the service beyond early access and anchoring delivery on GeForce RTX 5080 SuperPODs. The rollout broadens high-end PC cloud gaming access in a price-sensitive, mobile-first market and reinforces Nvidia's position as a performance-led alternative to console-centric ecosystems.

- July 2026: NVIDIA announced a new GeForce RTX 5080-powered GeForce NOW server location in Toronto, Canada. Adding a local node improves latency outcomes and highlights the competitive importance of regional points of presence as platforms pursue more consistent metro-area performance.

- November 2025: Sony activated full cloud streaming for PlayStation Portal across 30 countries, enabling 1080p visuals and 3D audio access to a large PlayStation 5 catalog. Expanding Portal functionality deepens Sony's device ecosystem strategy and reinforces cloud streaming as a feature layer tied to first-party content and subscription retention.

Cloud Gaming Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the cloud gaming market is defined as revenue earned when video games are run on remote servers and delivered to users over the internet, so gameplay is streamed to a device instead of being processed locally.

Scope exclusions: physical console or PC hardware sales, discretionary in-game micro-transactions, and generic cloud infrastructure leasing that is not tied to game delivery are excluded.

Segments Covered in This Report

- By Service Type

- Video Streaming

- File Streaming

- By Device

- Smartphones

- Tablets

- PCs and Laptops

- Other Devices

- By Gamer Type

- Casual Gamers

- Avid Gamers

- Lifestyle Gamers

- By Business Model

- Subscription-Based

- Pay-As-You-Play

- Free-to-Play and Ad-Supported

- Other Business Models

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of the addressable user base and the connectivity conditions that make cloud gaming practical. We use public sources such as ITU connectivity indicators, World Bank macro series, OECD digital economy releases, and national telecom regulator dashboards where available, then cross-check with platform policy pages and credible press coverage.

To convert adoption signals into a revenue model, we review company filings, earnings call transcripts, and investor presentations for cues on subscriptions, bundling, and user engagement. Patent databases are used selectively to understand where streaming, latency, and edge delivery capabilities are being developed. For baseline financial context, we reference paid subscriptions focused on company financials and news intelligence, and we treat them as supporting inputs rather than the only input. These desk sources are illustrative only, and many other public references were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test what users actually pay for, how often they play via cloud versus local installs, and how bundling changes the effective price. We speak with ecosystem participants across publishing, platform operations, telecom and broadband, and device channel roles. We then validate findings across APAC, EMEA, and the Americas so regional network readiness and pricing norms are reflected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 41% |

| Mid tier: 46% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 18% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool, where broadband and 5G readiness, addressable gamer population, and device access are used to reconstruct how many users can realistically stream gameplay, and then how many convert to paying usage. After that structure is set, we corroborate it with selective bottom-up checks such as sampled price points, subscription tiers, and observed bundling patterns, followed by sanity checks against service rollouts and country-level adoption signals.

Key inputs include active gamer base by region, average effective subscription price after bundles and promotions, cloud gaming usage frequency (hours and session patterns), the share of users on video streaming versus file streaming modes, and latency or data cap constraints that can limit sustained use. When a direct variable is missing for a smaller country, we handle the gap through proxy indicators like smartphone gaming penetration, fixed broadband speeds, and regional pricing bands, then adjust using interview feedback.

Forecasts are developed using scenario analysis supported by trend lines from connectivity upgrades, content catalog expansion, and expected pricing normalization, and they are reviewed against expert views from primary discussions so the final curve stays practical.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, and any large jumps are traced back to one clear driver before the model is accepted. We run variance checks across regions and compare implied revenue per user with observed subscription pricing and typical engagement ranges, then review exceptions in a second analyst pass.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major service launches, pricing resets, or large network coverage changes. Before delivery, a final review is completed so the view reflects the latest publicly available signals and the newest primary feedback.

Mordor Intelligence's Cloud Gaming Market Size Compared With Other Published Estimates

Published cloud gaming market values can look far apart because companies do not always count the same revenue streams, and they may use different base years and conversion assumptions. Differences also show up when one estimate leans on aggressive adoption curves, while another stays anchored to near-term network and pricing realities.

The main gap comes from whether adjacent digital gaming revenues get folded into the total. Mordor Intelligence counts only revenues directly tied to game streaming delivery, and leaves out physical hardware, discretionary in-game micro-transactions, and generic cloud infrastructure leasing. Timing choices also matter, because fast growth makes a 2024 base look very different from a 2026 base, and currency handling can shift totals when regional pricing is converted into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.23 B (2026) | |

| Global Consultancy A | USD 2.27 B (2024) | Uses a 2024 base year and a different ramp for conversion to paid usage, which can depress the starting value versus later-base models, and it may treat bundled subscriptions and promotional pricing with simpler averages. |

| Industry Publisher B | USD 3.30 B (2025) | Uses a 2025 starting point and a long-dated forecast horizon, and it can lift the near-term figure if broader definitions of cloud gaming revenue are applied across device and gamer-type segments without consistent exclusions. |

Looking at the table, the spread is explained mostly by what gets counted as cloud gaming revenue and the year chosen as the starting point in a fast-growing market. By keeping the revenue scope tight, then testing adoption and pricing assumptions against connectivity and rollout signals, we can provide a figure that is easier to trace and repeat.

Key Questions Answered in the Report

What is the current size of the cloud gaming market, and what is its forecast growth?

The market generated USD 6.23 billion in 2026 and is expected to reach USD 21.62 billion by 2031 at a 28.25% CAGR.

Which region leads revenue in cloud streaming services?

Asia Pacific commanded 38.45% of 2025 revenue, thanks to large-scale telco bundles and publisher partnerships.

Why are tablets expected to grow faster than smartphones?

ARM virtualization like Xiaomi’s WinPlay and dedicated handhelds such as Logitech G Cloud improve performance and portability, driving a 28.61% CAGR.

How are publishers monetizing cloud gaming audiences?

AAA franchises now launch cloud-first, expanding reach to non-console owners and boosting total addressable players by up to 40%.

What pricing models are most attractive to new users?

Ad-supported and free-to-play tiers, exemplified by Amazon Luna and Microsoft pilots, lower entry barriers while maintaining upgrade paths to premium subscriptions.

What limits cloud gaming adoption in rural markets?

High latency from limited 4G and 5G coverage, combined with low fixed-broadband speeds, hampers playability outside urban centers in South America and Africa.

Page last updated on: