Clinical Communication And Collaboration Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

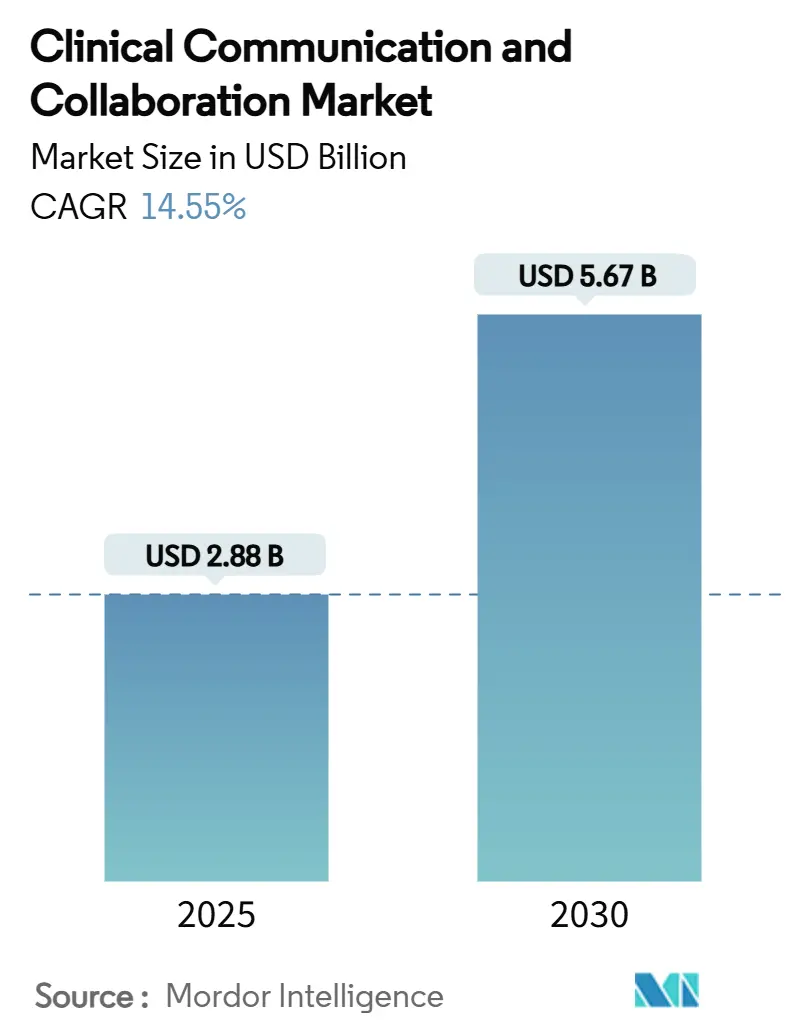

| Market Size (2025) | USD 2.88 Billion |

| Market Size (2030) | USD 5.67 Billion |

| Growth Rate (2025 - 2030) | 14.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Clinical Communication And Collaboration Market Analysis by Mordor Intelligence

The Clinical Communication And Collaboration Market size is estimated at USD 2.88 billion in 2025, and is expected to reach USD 5.67 billion by 2030, at a CAGR of 14.55% during the forecast period (2025-2030).

Accelerated investments in unified digital ecosystems, mandates for patient-safety reporting, and the drive to replace pagers with cloud-native platforms are the principal forces powering this expansion. Hospitals that adopt enterprise-wide suites report double-digit drops in sentinel events, measurable gains in clinician productivity, and faster stroke-code activation times, underscoring the link between modern communication and patient outcomes. Cloud deployment dominates because it delivers automatic updates, elastic scaling, and streamlined HIPAA compliance, while integration with Epic and Cerner ensures data liquidity across care pathways. Intensifying competition from TigerConnect, Microsoft, and Cisco keeps pricing disciplined and spurs rapid feature rollouts, especially in ambient AI, virtual nursing, and real-time analytics.

Key Report Takeaways

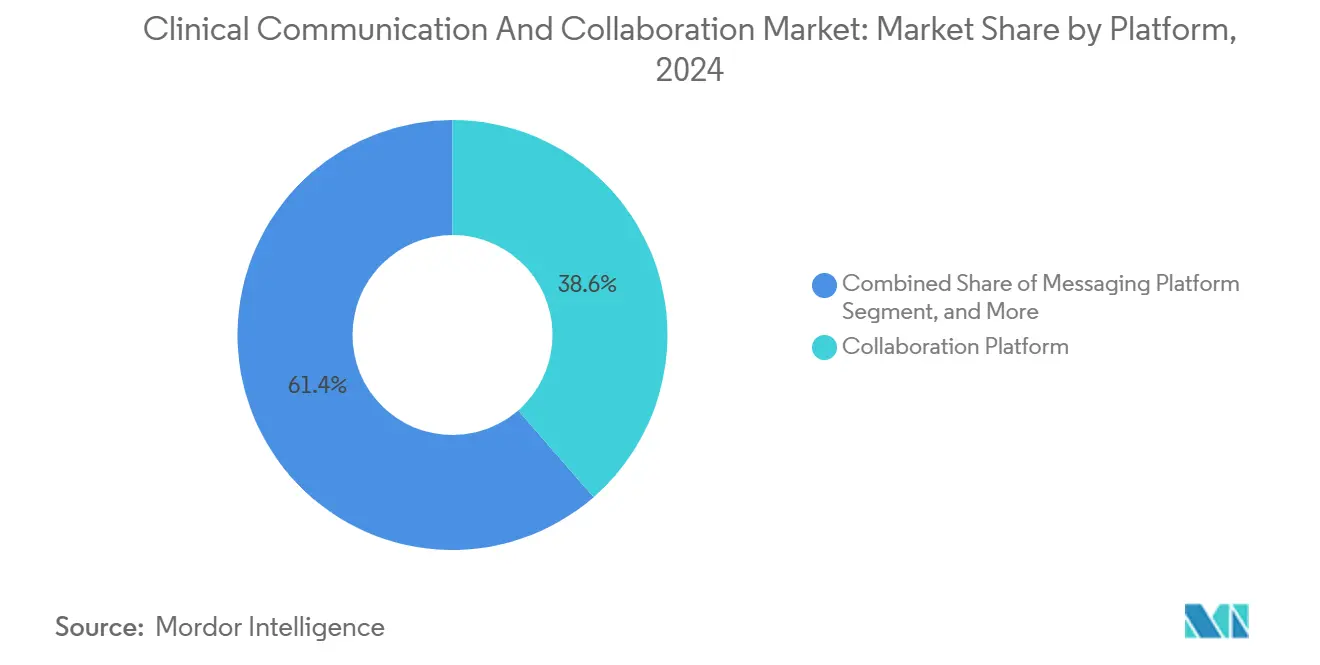

- By platform, collaboration platforms led with 38.61% revenue share in 2024, while virtual chatting platforms are projected to expand at an 18.09% CAGR through 2030.

- By component, software accounted for 66.26% of the clinical communication and collaboration market share in 2024, whereas services posted the fastest CAGR at 19.56% over 2025-2030.

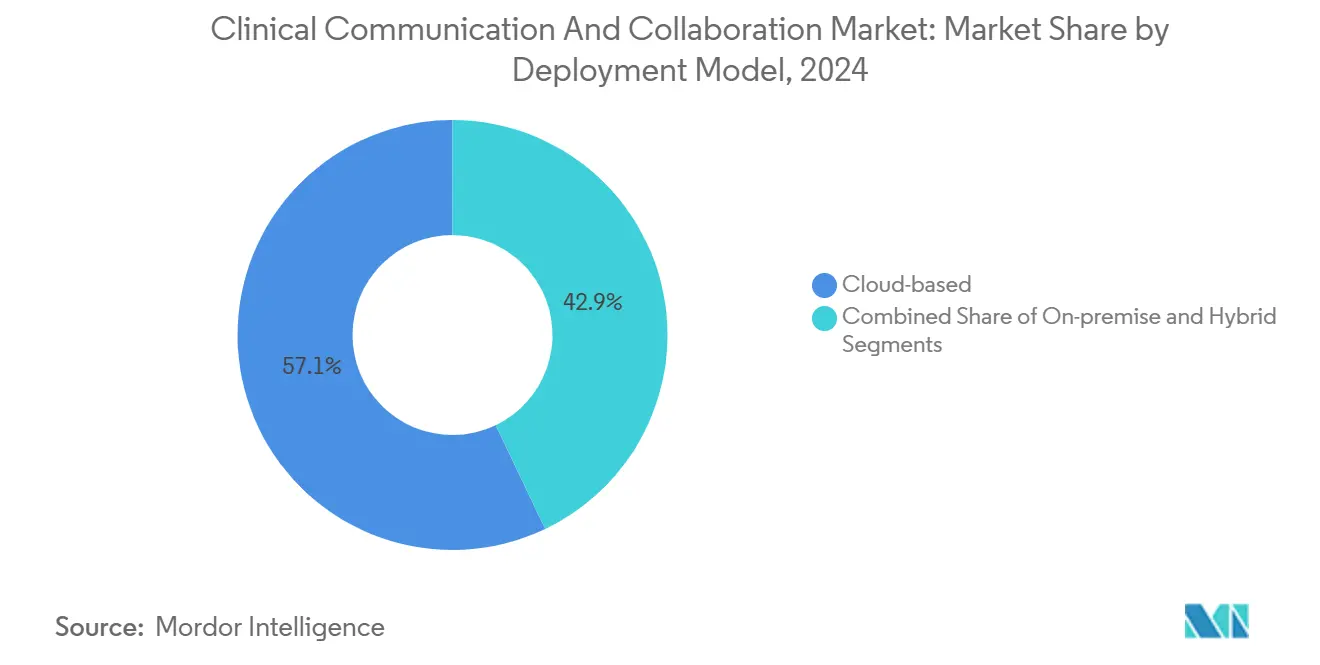

- By deployment model, cloud models held 57.14% of the clinical communication and collaboration market share in 2024 and are expected to continue rising at a 16.74% CAGR.

- By application, nurse communication contributed 28.94% of revenue in 2024; physician communication is forecasted to grow at a 18.47% CAGR to 2030.

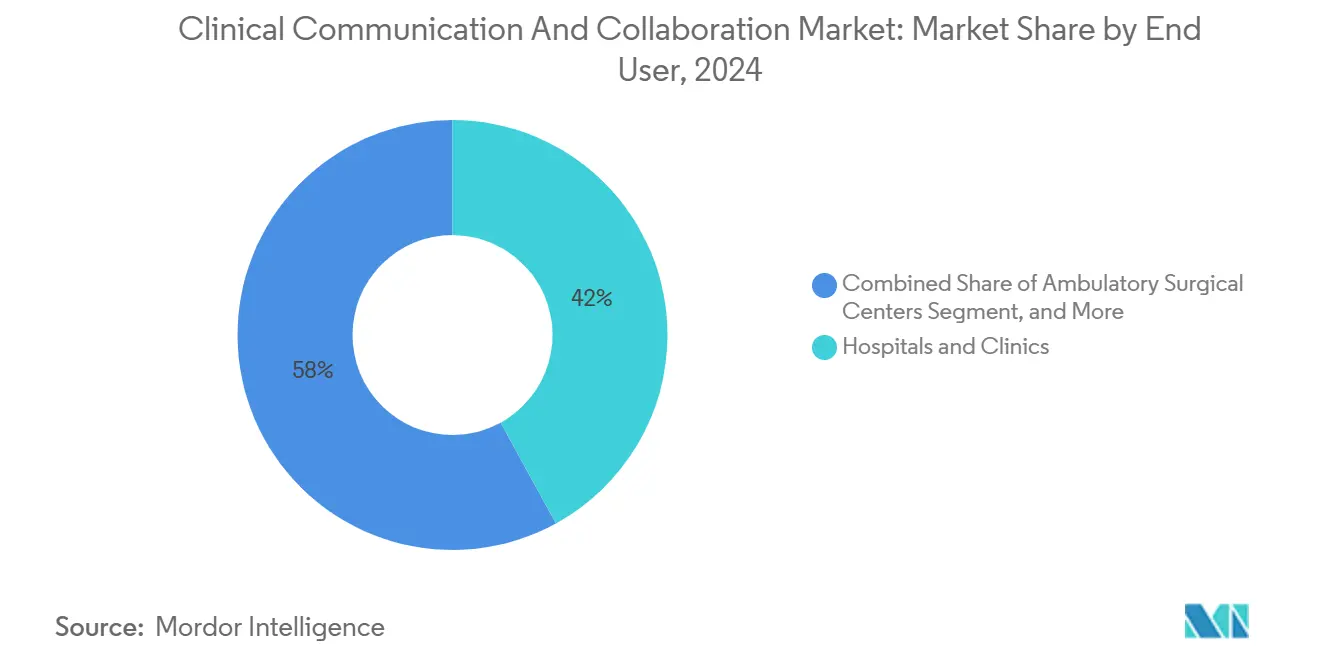

- By end user, hospitals and clinics captured a 41.97% share in 2024; however, home healthcare providers are set to rise at a 17.80% CAGR through the forecast period.

- By geography, North America commanded 40.06% of the clinical communication and collaboration market in 2024, and Asia-Pacific is projected as the fastest region with an 20.46% CAGR.

Global Clinical Communication And Collaboration Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation of healthcare ops | +3.2% | Global | Medium term (2-4 years) |

| Cloud-native suites replacing pagers | +2.8% | North America & EU; spill-over to APAC | Short term (≤ 2 years) |

| Integration with leading EHR platforms | +2.5% | Global; Epic/Cerner markets | Medium term (2-4 years) |

| Mandated patient-safety & quality reporting | +2.1% | North America; EU regulatory markets | Short term (≤ 2 years) |

| Ambient voice AI in documentation | +1.9% | North America; early APAC adoption | Long term (≥ 4 years) |

| Virtual nursing & RPM workflows | +1.8% | Global; developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation of Healthcare Operations

Digital overhauls are removing silos that once caused more than 60% of sentinel events, leading organizations to embed predictive analytics and real-time messaging into everyday workflows.[1]Baxter International, “Sentinel Event Root Cause Analysis Report,” baxter.com COVID-19 reinforced the cost of fragmentation: health systems equipped with unified suites recovered more quickly, maintained elective services, and protected staff by reducing unnecessary exposure. Executive boards now view communication modernization as a resilience mandate, anchoring capital budgets around platforms that integrate analytics, scheduling, and audit trails into a single interface. The clinical communication and collaboration market benefits directly because every rollout displaces legacy tools, secures data paths, and elevates user satisfaction benchmarks.

Cloud-Native Clinical Communication Suites Replacing Legacy Pagers

Hospitals switching from pagers to cloud messaging record 85% reductions in pager traffic and 35% fewer overhead alerts, while stroke-code activations drop from nine to four steps.[2]Symplr, “Stroke Code Activation Case Study,” symplr.com Such results illustrate how pagers bottleneck workflows and expose gaps in end-to-end encryption. Cloud models overcome those gaps through HIPAA-compliant storage, robust API integration, and systemwide downtime resilience. With major vendors bundling single sign-on, mobile device management, and analytics dashboards, the clinical communication and collaboration market now positions the cloud not as an alternative but as the enterprise default.

Integration of Clinical Communication with Leading EHR Platforms

Epic’s 2025 roadmap promotes ambient listening and automation that hinge on tight communication links, while Cerner’s extensions focus on closed-loop ordering and alert routing. Yet only 44% of clinicians currently rate EHR connectivity as satisfactory. Bridging that gap requires HL7-FHIR adapters, identity synchronization, and re-engineered task flows that preserve familiar decision trees. Vendors able to furnish turnkey connectors and pre-configured role-based routing accelerate adoption and widen their footprint inside the clinical communication and collaboration market.

Mandated Patient-Safety & Quality Reporting

The CMS Patient Safety Structural Measure, effective fiscal 2025, obliges hospitals to document safety culture and leadership engagement with digital evidence.[3]Press Ganey, “CMS Patient Safety Measure Guidance 2025,” pressganey.com Concurrent HIPAA updates require multi-factor authentication and data-at-rest encryption, eliminating discretionary controls. Platforms that embed automated event logging and analytics, therefore, win preference because they reduce audit workload and avert non-compliance penalties, amplifying demand across the clinical communication and collaboration market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & HIPAA/GDPR compliance | -1.8% | Global; regulated markets | Short term (≤ 2 years) |

| High upfront integration costs | -1.5% | Global; resource-constrained markets | Medium term (2-4 years) |

| Alarm fatigue & clinician alert-overload | -1.2% | Global; especially ICU | Long term (≥ 4 years) |

| Limited cellular/Wi-Fi in rural hospitals | -0.9% | Rural markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & HIPAA/GDPR Compliance Concerns

The 2025 HIPAA overhaul requires multi-factor logins, annual penetration tests, and complete system inventories, transforming optional safeguards into mandatory requirements. European regulators enforce similar rigor under the GDPR, levying fines that can reach up to 4% of a company's global annual revenue. Providers delay procurement until platforms demonstrate encrypt-in-use capabilities, exhaustive audit logs, and cyber-insurance attestations, thereby moderating short-term velocity in the clinical communication and collaboration market.

High Upfront Integration Costs

Enterprise installations often exceed USD 1 million once middleware, training, and workflow redesign are included, plus 15-20% annual maintenance costs. Smaller facilities hesitate despite evidence of 15-30% operational savings post-deployment. Vendors counter with modular licensing, managed-services pricing, and ROI modeling to widen adoption, yet capital scarcity remains a systemic drag across portions of the clinical communication and collaboration market.

Segment Analysis

By Platform: Collaboration Platforms Drive Unified Workflows

Collaboration platforms contributed 38.61% revenue in 2024, confirming their status as the operational backbone of the clinical communication and collaboration market. Hospitals favor these hubs because they consolidate secure texting, file sharing, and directory services, lowering handoff errors and shortening average length of stay. Virtual chatting platforms, posting an 18.09% CAGR, meet demand for immediate, context-aware exchanges in emergency and ICU units where seconds matter. The proliferation of AI chat assistants, real-time language translation, and patient-facing chatbots further accelerates this sub-segment’s pull on the clinical communication and collaboration market.

Messaging platforms remain foundational, particularly for small hospitals upgrading from pagers yet unready for full collaboration suites. Voice communication platforms gain traction where audible confirmation trumps typing, such as anesthesiology or trauma teams. Scheduling platforms occupy a precision niche, automating call-coverage rules and facilitating just-in-time staffing; they increasingly integrate with broader suites to eliminate duplicate data entry, widening the total clinical communication and collaboration market size attributed to interoperable ecosystems.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Dominance Reflects Platform-Centric Approach

Software captured a 66.26% share in 2024, underscoring a preference for device-agnostic, quickly deployable solutions that leverage existing smartphones and PCs. This orientation enlarges the clinical communication and collaboration market because capital constraints shift from hardware to subscription OPEX. Service revenues, with a 19.56% CAGR, mirror the complexity of enterprise migrations: consultative design, workflow mapping, and change-management support become non-negotiable to realize ROI. As a result, service providers forge multi-year partnerships that stabilize revenue visibility inside the clinical communication and collaboration market.

Hardware ranks lower yet remains indispensable for sterile or high-noise zones that require shielded intercoms or wearable badges. Nonetheless, as camera-equipped tablets and ruggedized phones clear infection-control tests, the discrete hardware slice of the clinical communication and collaboration market contracts proportionally, redirecting budgets toward advanced analytics modules and AI extensions.

By Deployment Model: Cloud-Based Solutions Accelerate Market Growth

Cloud deployments accounted for 57.14% of the clinical communication and collaboration market share in 2024 and exhibited the strongest 16.74% CAGR trajectory. CIOs prefer built-in redundancy, auto-patching, and elastic user provisioning over the maintenance burden of on-premise clusters. The subscription model aligns cash flows with usage, easing board approval and encouraging more health systems to adopt multi-tenant architectures. Hybrid installations persist where data-sovereignty laws or legacy voice gateways compel local nodes. Yet, even these environments increasingly rely on cloud analytics overlays, expanding overall clinical communication and collaboration market penetration.

On-premise systems appeal to military or behavioral-health facilities bound by stringent segregation rules. Their share is forecast to taper but not vanish, as specific scenarios still demand air-gapped voice networks. Vendors offer migration roadmaps that convert perpetual licenses into cloud credits, further smoothing adoption curves within the clinical communication and collaboration market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Nurse Communication Leads Patient Care Coordination

Nurse communication accounted for 28.94% of revenue in 2024, as nurses orchestrate medication rounds, multidisciplinary consultations, and family updates. Purpose-built modules streamline bedside task lists, integrate barcode med administration, and surface predictive deterioration alerts, directly influencing patient throughput and HCAHPS scores. Physician communication grows at the fastest rate, with a 18.47% CAGR; clinicians increasingly dictate notes, approve orders, and receive sepsis alerts on the same secure channel, consolidating previously fragmented mobile tools into the broader clinical communication and collaboration market.

Lab and radiology communication benefits as imaging turnarounds tighten under value-based care metrics. Patient communication and emergency alerts integrate portal messages, interpreter services, and mass-notification features for lockdown drills. Care-coordination modules automate discharge summaries and referral packets, which are critical to bundled-payment compliance, thereby cementing multi-department reliance on the clinical communication and collaboration market.

By End User: Hospitals & Clinics Anchor Market Demand

Hospitals and clinics commanded 41.97% share in 2024, reflecting their scale, regulatory exposure, and multifunctional demand. Large IDNs pursue single-vendor strategies to align formulary, imaging, and perioperative teams under uniform alerting rules, thereby driving enterprise deals that lift the clinical communication and collaboration market size. Home healthcare providers are posting a 17.80% CAGR on the back of hospital-at-home programs that require HIPAA-compliant video, vital feeds, and physician oversight within a single interface, extending the clinical communication and collaboration market beyond brick-and-mortar walls.

Ambulatory surgery centers and diagnostic labs adopt slimmer bundles to expedite turnover times and minimize cancellations. Long-term care facilities prioritize family messaging, wound care photo capture, and chronic disease teleconsults, carving a specialist niche with tailored workflows. Collectively, these segments diversify revenue streams across the clinical communication and collaboration market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 40.06% revenue in 2024, reflecting HIPAA-driven security mandates, mature EHR penetration, and widespread 5G coverage that supports video-rich handoffs. Large health systems routinely standardize across 30-plus hospitals, generating deal sizes that can exceed USD 20 million and fortifying the regional clinical communication and collaboration market. The government stimulus aimed at cybersecurity modernization further incentivizes upgrades, as grant recipients must demonstrate the use of encrypted communication.

The Asia Pacific is the growth pacesetter, with a 20.46% CAGR, driven by national digital health blueprints, AI pilot funding, and domestic cloud availability zones that meet data localization requirements. Singapore mandates secure messaging for all public hospitals, while China’s tertiary centers embed AI triage tools into their native super-apps, lifting the regional trajectory of the clinical communication and collaboration market. Emerging economies are leveraging low-cost Android devices and open-source FHIR connectors to leapfrog the constraints of the pager era.

Europe maintains steady adoption, although the GDPR necessitates in-region hosting and audit-file retention, which slows down procurement. The Middle East and Africa experience project-based spikes tied to smart hospital builds in Saudi Arabia and the UAE. South America’s momentum centers on Brazil and Colombia, where public-private partnerships are providing cloud credits to rural clinics, gradually increasing the continent’s share of the global clinical communication and collaboration market.

Competitive Landscape

Competitive intensity is moderate, positioning the clinical communication and collaboration market as attractive yet contested. TigerConnect and PerfectServe top the specialized segment, each offering deep care-team routing, EHR plug-ins, and robust compliance dashboards. Microsoft and Cisco leverage Teams and Webex integrations, bundling clinical connectors and device-management policies into enterprise agreements already spanning most hospitals in the United States. Oracle Health (Cerner) embeds voice commands and secure messaging within Millennium, challenging best-of-breed solutions.

M&A activity underscores a consolidation push: TigerConnect acquired Twiage to fortify EMS-to-ED continuity, while Commure and Athelas joined forces to absorb Augmedix, crafting the most extensive AI software portfolio in healthcare. Start-ups emphasize ambient voice, context-aware alerting, and predictive staffing; those with validated ROI quickly become targets for platform vendors looking to augment capabilities. As buyers gravitate toward vendors that deliver measurable gains in length of stay, readmissions, and staff turnover, product roadmaps converge on analytics, AI transcription, and patient engagement, shaping the next phase of the clinical communication and collaboration market.

Clinical Communication And Collaboration Industry Leaders

-

NEC Corporation

-

Microsoft Corporation

-

TigerConnect

-

Cisco Systems

-

Epic Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Emory Healthcare launched a virtual nursing initiative at Emory University Hospital Midtown, utilizing AI-driven technology and LIDAR for fall prevention, with plans to expand to eight inpatient units across multiple hospitals in 2025. The initiative aims to improve patient safety and reduce documentation burdens for nursing staff.

- February 2025: Cleveland Clinic announced the deployment of Ambience's AI-powered Clinical Documentation Improvement platform across its ambulatory practices, leveraging AI technology to enhance clinical communication and streamline documentation processes with potential for an 80% reduction in documentation time.

- December 2024: SpinSci Technologies has completed a Series C funding round, raising USD 53 million to advance its AI-enhanced patient engagement software, which aims to improve digital engagement and workflow efficiencies in healthcare communication.

- June 2024: Mitel, a Canadian telecommunications company, reported the launch of PlatfoMitel, a virtual care collaboration service (VCCS) made available in seven European countries, including Belgium, France, Italy, the Netherlands, Switzerland, and the United Kingdom.

Global Clinical Communication And Collaboration Market Report Scope

As per the scope of the report, clinical communication and collaboration systems are mobile platforms that clinicians, care teams, patients, and caregivers use to collaborate on treatment and care activities within ambulatory, acute, post-acute, and virtual care settings.

The clinical communication and collaboration market is segmented by platform, component, deployment, application, end user, and geography. By platform, the market is segmented into collaboration platform, messaging platform, voice communication platform, and other platforms (virtual chatting platform, scheduling platform, and others). By component, the market is segmented into hardware, software, and service. By deployment, the market is segmented into on-premise model and cloud-based model. By application, the market is segmented into lab and radiology communication, nurse communication, patient communication and emergency alerts, and physician communication. By end user, the market is segmented into hospitals and clinics, ambulatory surgical centers, long-term care facilities, and other end users (diagnostic centers, nursing centers, and others). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in value (USD) for the above segments.

| Collaboration Platform |

| Messaging Platform |

| Voice Communication Platform |

| Virtual Chatting Platform |

| Scheduling Platform |

| Other Platforms |

| Hardware |

| Software |

| Service |

| On-premise |

| Cloud-based |

| Hybrid |

| Lab & Radiology Communication |

| Nurse Communication |

| Patient Communication & Emergency Alerts |

| Physician Communication |

| Care Coordination & Handoffs |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Long-term Care Facilities |

| Diagnostic Centers |

| Nursing Centers |

| Home Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Platform | Collaboration Platform | |

| Messaging Platform | ||

| Voice Communication Platform | ||

| Virtual Chatting Platform | ||

| Scheduling Platform | ||

| Other Platforms | ||

| By Component | Hardware | |

| Software | ||

| Service | ||

| By Deployment Model | On-premise | |

| Cloud-based | ||

| Hybrid | ||

| By Application | Lab & Radiology Communication | |

| Nurse Communication | ||

| Patient Communication & Emergency Alerts | ||

| Physician Communication | ||

| Care Coordination & Handoffs | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Long-term Care Facilities | ||

| Diagnostic Centers | ||

| Nursing Centers | ||

| Home Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the clinical communication and collaboration market?

The clinical communication and collaboration market size is USD 2.88 billion in 2025 and is forecast to reach USD 5.67 billion by 2030 at a 14.55% CAGR.

Which deployment model is growing fastest?

Cloud-based platforms lead with 57.14% share in 2024 and a 16.74% CAGR through 2030, thanks to lower IT overhead and easier compliance.

Why are collaboration platforms favored over pagers?

Collaboration platforms cut pager usage by 85%, reduce stroke-code steps, and supply encrypted audit trails that simple pagers cannot offer, improving safety and efficiency.

Which region offers the highest growth potential?

Asia Pacific delivers the fastest expansion, advancing at 20.46% CAGR due to government funding, digital-health policy support, and rapid broadband rollout.

How does ambient voice AI support clinicians?

Ambient AI transforms spoken encounters into structured notes, with pilots at Stanford and Cleveland Clinic demonstrating 78-96% physician satisfaction and up to 80% time savings.

What factors restrain broader adoption?

Complex compliance requirements, high integration costs, alarm fatigue, and rural connectivity gaps collectively temper growth, though ROI evidence continues to overcome many barriers.

Page last updated on: