| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 11.83 Billion |

| Market Size (2030) | USD 14.64 Billion |

| CAGR (2025 - 2030) | 4.35 % |

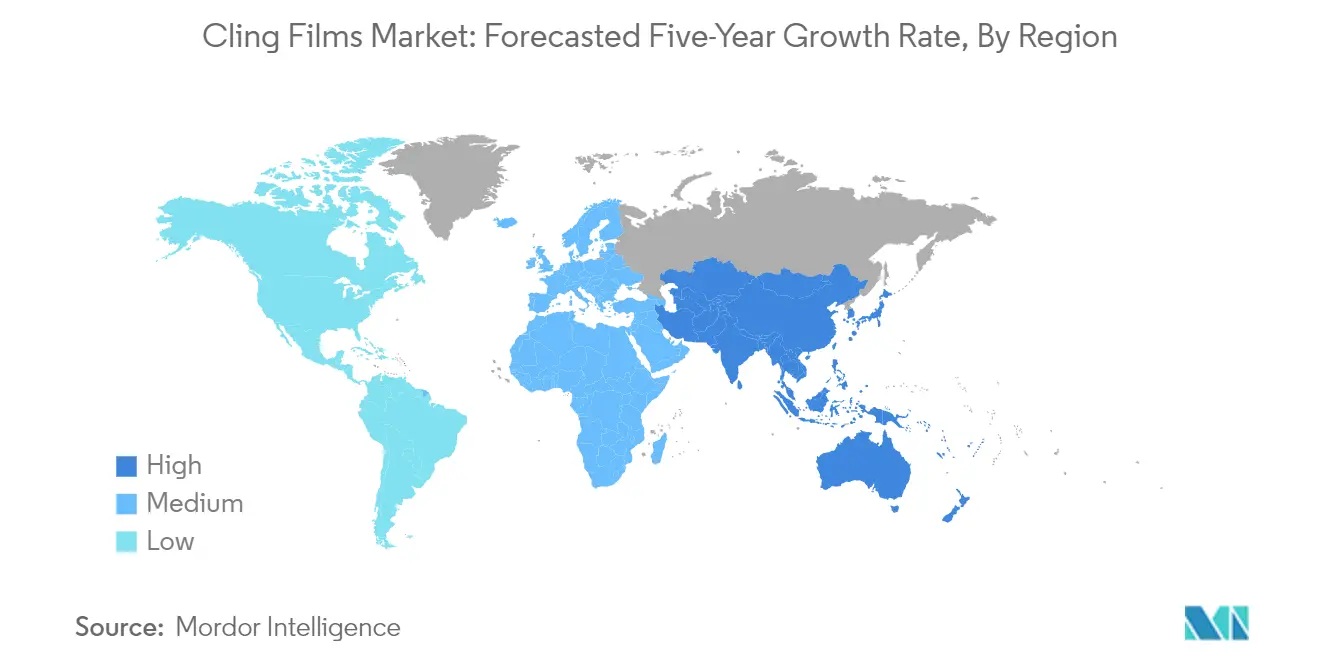

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

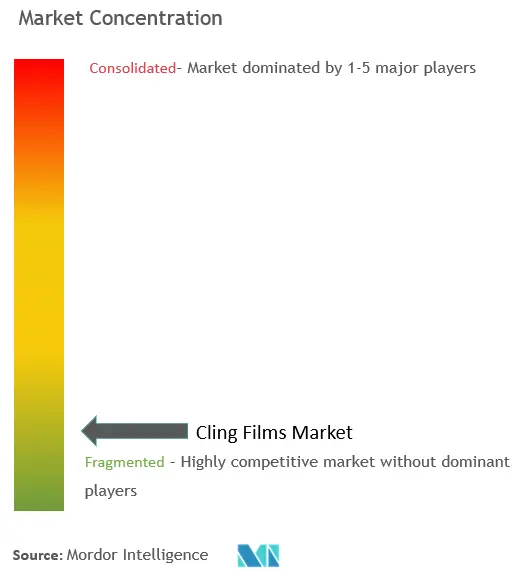

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Cling Films Market Analysis

The Cling Films Market size is estimated at USD 11.83 billion in 2025, and is expected to reach USD 14.64 billion by 2030, at a CAGR of 4.35% during the forecast period (2025-2030).

The global packaging industry has witnessed significant transformation driven by changing consumer preferences and sustainability initiatives. According to the World Packaging Organization (WPO), the global packaging industry's turnover exceeds USD 500 billion, highlighting the substantial scale of operations and opportunities in the sector. The emergence of bio-based alternatives and eco-friendly packaging solutions has become increasingly prominent, with manufacturers investing in research and development of sustainable materials. The industry has also experienced considerable consolidation through mergers and acquisitions, as companies seek to strengthen their market position and expand their technological capabilities. Recent innovations in packaging technologies have focused on improving product preservation while reducing environmental impact.

The food and beverage sector continues to be a major growth driver for the cling films market, with the global food processing sector generating approximately USD 7 trillion annually, according to the USDA. The industry has witnessed a significant shift towards sustainable packaging solutions, with several manufacturers developing bio-based and recyclable alternatives. In September 2022, KM Packaging introduced C-Cling, a home-compostable adhesive film for catering and retail applications, demonstrating the industry's commitment to environmental sustainability. The sector has also seen increased adoption of modified atmospheric packaging technologies and smart packaging solutions that enhance product shelf life and maintain freshness.

Regulatory changes across various regions have significantly impacted the industry landscape. The United Arab Emirates has announced a comprehensive ban on single-use plastic bags starting from 2024, with additional restrictions on plastic packaging materials, including cling films, scheduled for implementation from 2026. This regulatory shift has accelerated innovation in sustainable packaging solutions and prompted manufacturers to develop compliant alternatives. Industry players are increasingly focusing on developing products that meet both regulatory requirements and consumer demands for environmentally responsible packaging solutions.

The pharmaceutical packaging segment has emerged as a significant growth avenue for the cling films market, with the North American region accounting for 49.1% of total pharmaceutical sales globally, according to the European Federation of Pharmaceutical Industries and Associations (EFPIA). The industry has witnessed increased demand for specialized packaging solutions that ensure product integrity and safety while meeting stringent regulatory requirements. Manufacturers are developing advanced barrier films with enhanced protection capabilities and improved sustainability profiles. The sector has also seen growing adoption of smart packaging solutions that incorporate tracking and authentication features to ensure product security throughout the supply chain.

Cling Films Market Trends

Growing Food Industry and Increasing Demand for Food Packaging

The global food processing sector has emerged as one of the largest industries worldwide, generating approximately USD 7 trillion annually. This growth drives substantial demand for food packaging films in flexible food packaging applications. The increasing globalization of food distribution has enabled previously local foods to become accessible worldwide, creating new opportunities for protective packaging solutions such as food packaging wrap. This trend is further amplified by rising consumer awareness of diverse food options and the growing preference for packaged and ready-to-eat foods, particularly among urban consumers. The fast-paced lifestyle in metropolitan areas has led to increased adoption of convenient meal solutions, with rapidly rising incomes and improving living standards contributing to the expanded use of packaged foods in urban regions.

The food and beverage industry's robust growth is exemplified by the European Union's manufacturing sector, which stands as the region's largest in terms of employment and value addition. According to the FoodDrink Europe report published in December 2022, the industry employs 4.6 million people and generates a turnover of EUR 1.1 trillion, with a value addition of EUR 230 billion. The sector's strength is further demonstrated by its significant export performance, with EU food and beverage exports doubling over the past decade to exceed EUR 90 billion. This expansion in food processing and distribution activities has created sustained demand for effective packaging solutions, including cling films, which play a crucial role in maintaining food freshness and preventing contamination.

Understand The Key Trends Shaping This Market

Download PDF

Growing Usage in Other End-User Industries

The pharmaceutical sector has emerged as a significant driver for cling films demand, particularly in emerging economies like India, which has established itself as a prominent player in the global pharmaceutical market. With approximately 10,500 domestic drug manufacturers, India accounts for 20% of the global generic medicine supply by volume, serving more than 200 countries worldwide. The country's pharmaceutical prowess is particularly evident in its ability to satisfy 40% of the United States' generic drug demand and 30% of the United Kingdom's requirements, creating substantial demand for pharmaceutical packaging solutions including cling films.

The consumer goods industry has also demonstrated strong potential for food packaging films market applications, as evidenced by China's robust retail sector, which recorded total retail sales of approximately CNY 44 trillion in 2022. The expansion of healthcare infrastructure and services has further boosted demand, with China's public expenditure on healthcare and hygiene increasing by 17% in 2022 compared to the previous year, reaching approximately CNY 2.25 trillion. This growth in healthcare spending, combined with the increasing sophistication of medical packaging requirements and the expansion of consumer goods distribution networks, has created multiple avenues for food packaging wrap applications across various end-user industries.

Segment Analysis: Material Type

Polyethylene Segment in Cling Films Market

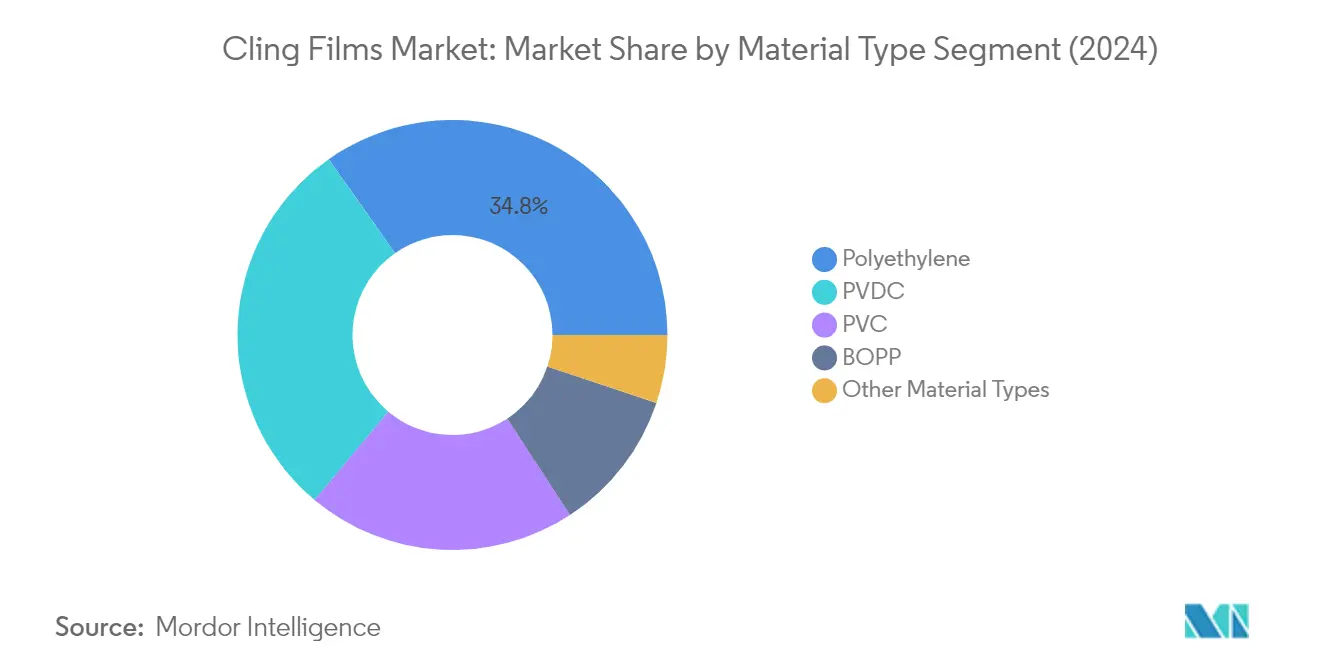

The polyethylene segment dominates the global cling films market, holding approximately 35% of the market share in 2024. This significant market position is attributed to polyethylene's superior barrier properties, excellent tear resistance, and strong tack strength. The segment's dominance is further reinforced by its widespread use in food packaging films applications, as polyethylene-based cling films are completely recyclable and highly effective in maintaining food freshness for extended periods. These films are particularly suitable for packaging various food items, including vegetables, meat, fruits, and seafood. The segment's growth is driven by increasing demand from supermarkets and cold storage facilities, where polyethylene cling films' fog resistance properties help enable water droplets inside packaging to wander and scatter automatically, reducing fogging chances while maintaining food freshness and packaging transparency.

BOPP Segment in Cling Films Market

The Biaxially Oriented Polypropylene (BOPP) segment demonstrates strong growth potential in the cling films market for the period 2024-2029. The segment's growth is driven by its superior characteristics, including better processability, a higher degree of cleanliness, and resistance to soft-flock formation during the die-cutting process. BOPP films offer enhanced clarity, improved stiffness, and higher resistance to oil and water while also enhancing barrier properties to oxygen and water vapor. These films are increasingly adopted in various end-user industries, including food manufacturing and distribution, consumer goods manufacturing, tobacco companies, and supermarkets. The segment's growth is further supported by BOPP films' better chemical resistance, weldability/sealing properties, and cost-effectiveness compared to traditional alternatives.

Remaining Segments in Material Type

The remaining segments in the cling films market include Polyvinyl Chloride (PVC), Polyvinylidene Chloride (PVDC), and other material types. PVC cling films are valued for their excellent tear resistance, strong fastening properties, and good tensile properties, making them ideal for food and pharmaceutical packaging. PVDC films offer exceptional barrier properties to water vapor, oxygen, and other odors and flavors, finding extensive use in modified atmospheric packaging of different food products. Other material types, including polyamide films, bio-PLA, cellulose derivatives, and biodegradable starch blends, are gaining traction due to increasing environmental concerns and regulatory pressures on conventional plastics.

Segment Analysis: Form

Cast Cling Film Segment in Global Cling Films Market

Cast cling films dominate the global cling films market, commanding approximately 76% of the total market share in 2024. This segment's dominance can be attributed to its superior properties, including excellent clarity, transparency, and glossy finish, which make it ideal for scanning technologies like RFID in packaging applications. Cast cling films demonstrate exceptional performance with natural clingy properties on both sides, enabling pallets to stick together effectively. The segment's growth is primarily driven by its superior advantages, such as excellent load-retaining capability, high film puncture resistance, and tear resistance. These films offer significant cost savings while maintaining high performance, making them particularly suitable for various applications, including food packaging films, healthcare packaging, and consumer goods packaging. The manufacturing process of cast cling films, which involves continuous feeding through a narrow slot-die followed by controlled cooling, ensures uniform thickness throughout the final product with virtually no limitations on achieving desired specifications.

Blow Cling Film Segment in Global Cling Films Market

The blow cling film segment represents a significant portion of the global cling films market, offering unique advantages in specific applications. These films are manufactured through a blown film extrusion process, where the resin is subjected to a circular die before being vertically blown upward and outward to form bubble-like structures. The segment's key strengths lie in its superior resistance to punctures, higher toughness, durability, and high level of cling properties. The production process of blow cling films results in lesser manufacturing scrap compared to cast cling films, making it an environmentally conscious choice. While these films can stretch further compared to cast cling films, they require additional force for stretching. The mechanical properties of blow cling films allow down-gauge to a thinner cling film while maintaining load stability on pallets, which helps reduce consumption and operational costs. The segment finds extensive applications in industrial packaging and consumer packaging for medical products and agricultural films.

Segment Analysis: End-User Industry

Food Segment in Cling Films Market

The food segment continues to dominate the global cling films market, commanding approximately 45% of the total market share in 2024. This segment's prominence is driven by the increasing demand for processed foods and the growing importance of food wrap and packaging solutions worldwide. The food industry's extensive use of cling films spans across various applications, from packaging fresh produce and meat products to preserving prepared meals and dairy items. Major food processing companies and retail chains are increasingly adopting cling films due to their superior properties in maintaining food freshness, preventing contamination, and extending shelf life. The segment's growth is further bolstered by the expanding food retail sector, particularly in emerging economies, and the rising consumer preference for conveniently packaged food products. Additionally, the increasing focus on reducing food waste through effective packaging solutions has significantly contributed to the segment's market leadership.

Healthcare Segment in Cling Films Market

The healthcare segment emerges as a significant growth opportunity in the cling films market, with robust expansion projected for the period 2024-2029. This segment's growth is primarily driven by the increasing adoption of cling films in pharmaceutical packaging, medical device protection, and various healthcare applications. The stringent requirements for maintaining sterility and safety in healthcare packaging have led to increased demand for high-quality cling films that can withstand temperature extremes, humidity, and exposure to contaminants. The segment's expansion is further supported by the growing pharmaceutical industry, particularly in emerging markets, and the increasing focus on maintaining product integrity throughout the supply chain. The healthcare segment also benefits from ongoing innovations in cling film technology, particularly in terms of enhanced barrier properties and compatibility with medical-grade applications. The rising demand for tamper-evident and secure packaging solutions in the healthcare sector continues to drive the adoption of specialized cling films.

Remaining Segments in End-User Industry

The consumer goods, industrial, and other end-user segments collectively represent significant portions of the cling films market, each serving distinct applications and requirements. The industrial segment maintains a strong presence due to its widespread use in packaging and protecting manufactured goods during storage and transportation. The consumer goods segment continues to evolve with changing consumer preferences and retail trends, particularly in the electronics and personal care sectors. Other end-user industries, including agriculture and textile packaging, contribute to market diversity through specialized applications. These segments benefit from ongoing technological advancements in cling film manufacturing, leading to improved product performance and sustainability features. The varying requirements across these segments drive continuous innovation in terms of film thickness, barrier properties, and application-specific characteristics, ensuring sustained market growth across multiple end-use sectors.

Cling Films Market Geography Segment Analysis

Cling Films Market in Asia-Pacific

The Asia-Pacific region represents a significant cling films market, driven by rapid industrialization, an expanding food processing sector, and growing retail infrastructure. China leads the regional cling films market, followed by India and Japan, while South Korea and ASEAN countries contribute substantially to the regional demand. The region's growth is primarily fueled by increasing urbanization, changing consumer lifestyles, and the rising adoption of convenient food packaging films solutions across various end-use industries, including food, healthcare, and consumer goods.

Cling Films Market in China

China dominates the Asia-Pacific cling films market, holding approximately 62% market share in 2024. The country's massive food and beverage industry, coupled with its robust pharmaceutical sector, drives substantial demand for cling films. The presence of numerous manufacturing facilities, along with government initiatives promoting the packaging industry, has strengthened China's position in the cling films market. The country's electronics industry, being one of the largest globally, further contributes to the demand for specialized packaging solutions, including cling films.

Cling Films Market in India

India emerges as one of the fastest-growing markets in the Asia-Pacific region, with a projected growth rate of approximately 5% during 2024-2029. The country's rapidly expanding food processing industry, coupled with increasing foreign direct investments in the packaging sector, drives market growth. The government's focus on improving healthcare infrastructure and the pharmaceutical industry's expansion creates additional demand for high-quality cling films. India's growing retail sector and changing consumer preferences towards convenient food packaging films solutions further accelerate market development.

Cling Films Market in North America

North America represents a mature cling films market, characterized by advanced packaging technologies and stringent quality standards. The United States leads the regional market, followed by Canada and Mexico. The region's market is driven by robust demand from the food service industry, healthcare sector, and industrial applications. The presence of major manufacturers and continuous technological innovations in stretch wrap film solutions further strengthens the market position.

Cling Films Market in United States

The United States maintains its leadership position in North America, commanding approximately 70% of the regional cling films market share in 2024. The country's extensive food and beverage industry, coupled with its significant pharmaceutical sector, drives substantial demand for cling films. The presence of leading manufacturers, advanced distribution networks, and strong research and development capabilities further reinforces the country's dominant position in the cling films market.

Cling Films Market in Canada

Canada demonstrates the highest growth potential in North America, with an expected growth rate of approximately 4% during 2024-2029. The country's expanding food processing industry and growing pharmaceutical sector contribute significantly to market growth. The increasing adoption of advanced flexible food packaging solutions across various industries, coupled with rising environmental awareness leading to demand for sustainable packaging options, drives market development.

Cling Films Market in Europe

Europe represents a sophisticated cling films market, characterized by high-quality standards and innovative packaging solutions. Germany leads the regional market, followed by the United Kingdom, Italy, and France. The region's strong focus on sustainable packaging solutions and circular economy principles shapes market development. The presence of established manufacturers and continuous technological advancements in stretch wrap film materials contributes to market growth.

Cling Films Market in Germany

Germany maintains its position as the largest market for cling films in Europe. The country's robust food and beverage industry, coupled with its significant pharmaceutical sector, drives substantial demand. Germany's central position in the EU makes it an ideal location for logistics hubs and distribution centers, further boosting the demand for industrial packaging solutions, including cling films.

Cling Films Market in France

France emerges as the fastest-growing market in Europe. The country's expanding food processing industry and growing healthcare sector drive market growth. The increasing adoption of advanced flexible food packaging solutions across various industries, coupled with rising environmental awareness leading to demand for sustainable packaging options, supports market development.

Cling Films Market in South America

The South American cling films market shows promising growth potential, with Brazil and Argentina being the key markets in the region. Brazil emerges as both the largest and fastest-growing market, driven by its extensive food processing industry and growing pharmaceutical sector. The region's market development is supported by increasing industrialization, growing retail infrastructure, and rising demand for convenient packaging solutions across various end-use industries.

Cling Films Market in Middle East & Africa

The Middle East & Africa region demonstrates growing demand for cling films, with Saudi Arabia and South Africa being the key markets. Saudi Arabia represents the largest market in the region, while South Africa shows the fastest growth potential. The region's market is driven by expanding food processing industries, a growing healthcare sector, and increasing adoption of modern packaging solutions across various industries.

Get Analysis on Important Geographic Markets

Download PDF

Cling Films Industry Overview

Top Companies in Cling Films Market

The global cling films market is characterized by continuous product innovation and strategic expansion initiatives by leading players. Companies are increasingly focusing on developing sustainable and eco-friendly film solutions while enhancing their manufacturing capabilities through technological advancements. Operational agility is demonstrated through flexible production systems that can quickly adapt to changing customer demands and market conditions. Strategic moves in the industry include vertical integration to control raw material supplies and strengthen distribution networks. Market leaders are expanding their geographical presence through both organic growth and acquisitions, particularly in emerging markets. Research and development investments are primarily directed towards improving film properties like strength, clarity, and environmental sustainability. Companies are also forming strategic partnerships to leverage complementary capabilities in technology and market access.

Fragmented Market with Strong Regional Players

The global cling films market exhibits a fragmented structure with a mix of large multinational corporations and regional specialists. The top four global players command approximately one-quarter to one-third of the market share, while numerous regional and local manufacturers serve specific geographical markets or specialized applications. Large conglomerates leverage their extensive resources, established distribution networks, and diverse product portfolios to maintain market positions. Regional players compete effectively by offering customized solutions and maintaining strong relationships with local customers. The market has witnessed significant merger and acquisition activity as larger companies seek to expand their product offerings and geographical reach.

The competitive dynamics vary significantly across regions, with developed markets showing higher consolidation compared to emerging markets. Major players are increasingly pursuing strategic acquisitions to strengthen their market position and expand their technological capabilities. Local manufacturers, particularly in Asia-Pacific and Latin America, maintain competitive advantages through their understanding of regional requirements and established customer relationships. The industry is characterized by significant barriers to entry, including high capital requirements, technical expertise, and established distribution networks, which favor incumbent players while limiting new entrants.

Innovation and Sustainability Drive Future Success

Success in the cling films market increasingly depends on companies' ability to address growing environmental concerns while maintaining product performance. Incumbent players must focus on developing sustainable alternatives to traditional materials, investing in recycling technologies, and optimizing their manufacturing processes to reduce environmental impact. Market leaders are strengthening their positions through vertical integration, enhanced distribution capabilities, and strategic partnerships with key end-users. Companies are also investing in digital technologies to improve operational efficiency and customer service while expanding their presence in high-growth markets through targeted acquisitions and greenfield investments.

For contenders seeking to gain market share, specialization in specific applications or regions offers a viable path forward. Success factors include developing innovative solutions for niche markets, building strong relationships with key customers, and maintaining operational flexibility to respond quickly to market changes. The industry faces increasing regulatory pressure regarding plastic usage and recycling, making sustainability initiatives crucial for long-term success. End-user concentration varies by segment, with food and healthcare industries representing significant buying power. The threat of substitution from alternative packaging solutions necessitates continuous innovation and value proposition enhancement by market players. The flexible food packaging market is also influencing trends in the cling films market, as innovations in food packaging films drive demand for more sustainable and efficient solutions.

Cling Films Market Leaders

-

Berry Global Inc.

-

Amcor plc

-

Sigma Plastics Group

-

Jindal Poly Films Limited

-

Reynolds Consumer Products

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Cling Films Market News

- February 2023: Berry Global Group Inc. launched a next-generation version of its proven stretch hood film with a minimum of 30% recycled plastic content. This will help the company to support businesses in achieving sustainability objectives as well as meeting the requirements of current and forthcoming United Kingdom and European plastics packaging legislation.

- January 2023: Amcor plc announced the introduction of its new PrimeSeal and DairySeal Recycle-Ready Thermoforming Films for meat and dairy, which provide outstanding packaging performance and enhanced packaging circularity. The novel packaging is heat resistant up to 90 °C and is made with low Ethylene-Vinyl Alcohol Copolymer (EVOH) content without reducing the shelf-life of perishable items. It is appropriate for fresh and processed meat and fish, as well as hard cheese.

Cling Films Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Food Industry and Increasing Demand For Food Packaging

- 4.1.2 Increase in Demand from the Healthcare Sector

-

4.2 Restraints

- 4.2.1 Low Resistance to Extreme Weather Conditions

- 4.2.2 Rising Global Regulations on its Usage

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Material Type

- 5.1.1 Polyethylene

- 5.1.2 Biaxially Oriented Polypropylene

- 5.1.3 Polyvinyl Chloride

- 5.1.4 Polyvinylidene Chloride

- 5.1.5 Other Material Types

-

5.2 Form

- 5.2.1 Cast Cling Film

- 5.2.2 Blow Cling Film

-

5.3 End-user Industry

- 5.3.1 Food

- 5.3.2 Healthcare

- 5.3.3 Consumer Goods

- 5.3.4 Industrial

- 5.3.5 Other End-user Industries

-

5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 ADEX SRL

- 6.4.3 Alliance Plastics

- 6.4.4 All American Poly

- 6.4.5 Amcor plc

- 6.4.6 Anchor Packaging LLC

- 6.4.7 Berry Global Inc.

- 6.4.8 Deriblok SpA

- 6.4.9 Hipac SPA

- 6.4.10 Inteplast Group

- 6.4.11 Intertape Polymer Group

- 6.4.12 Jindal Poly Films Limited

- 6.4.13 Malpack

- 6.4.14 Mitsubishi Chemical Corporation

- 6.4.15 Nan Ya Plastics Corporation

- 6.4.16 Novamont SPA

- 6.4.17 Paragon Films

- 6.4.18 Reynolds Consumer Products

- 6.4.19 Sigma Plastics Group

- 6.4.20 Technovaa Plastic Industries Pvt. Ltd.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications Of Bio-based Cling Films

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Cling Films Industry Segmentation

Cling film (plastic wrap, food wrap, or saran wrap) is a thin, transparent plastic film that adheres to surfaces and to itself and is used for packaging food items. They protect food from insects and microbial contamination, keep it fresh, and minimize the risk of food wastage by increasing its shelf life. Besides food applications, it is used for packaging in healthcare, consumer goods, industrial, and other applications.

The cling films market is segmented by material type (Polyethylene, Biaxially Oriented Polypropylene, Polyvinyl Chloride (PVC), Polyvinylidene Chloride (PVDC), and Other Material Types), form (Cast Cling Film and Blow Cling Film), end-user industry (Food, Healthcare, Consumer Goods, Industrial, and Other End-user Industries), and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of revenue (USD) for all the above segments.

| Material Type | Polyethylene | ||

| Biaxially Oriented Polypropylene | |||

| Polyvinyl Chloride | |||

| Polyvinylidene Chloride | |||

| Other Material Types | |||

| Form | Cast Cling Film | ||

| Blow Cling Film | |||

| End-user Industry | Food | ||

| Healthcare | |||

| Consumer Goods | |||

| Industrial | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Cling Films Market Research FAQs

How big is the Cling Films Market?

The Cling Films Market size is expected to reach USD 11.83 billion in 2025 and grow at a CAGR of 4.35% to reach USD 14.64 billion by 2030.

What is the current Cling Films Market size?

In 2025, the Cling Films Market size is expected to reach USD 11.83 billion.

Who are the key players in Cling Films Market?

Berry Global Inc., Amcor plc, Sigma Plastics Group, Jindal Poly Films Limited and Reynolds Consumer Products are the major companies operating in the Cling Films Market.

Which is the fastest growing region in Cling Films Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Cling Films Market?

In 2025, the Europe accounts for the largest market share in Cling Films Market.

What years does this Cling Films Market cover, and what was the market size in 2024?

In 2024, the Cling Films Market size was estimated at USD 11.32 billion. The report covers the Cling Films Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Cling Films Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Cling Films Market Research

Mordor Intelligence provides a comprehensive analysis of the cling films industry. We leverage our extensive expertise in food packaging films research. Our detailed report examines the entire ecosystem of plastic wrap and saran wrap products. It includes applications of PVC food film and technologies related to stretch wrap film. The analysis covers various segments, such as flexible food packaging solutions and commercial food wrap innovations. This offers stakeholders actionable insights, all available in an easy-to-read report PDF format for download.

Our research benefits industry participants by offering detailed insights into food wrap and kitchen wrap trends. It examines the evolving landscape of plastic food wrap applications. The report investigates emerging technologies in food preservation film and fresh keeping film solutions. It also explores developments in disposable food wrap products. Stakeholders gain a valuable understanding of food packaging wrap dynamics and flexible food packaging market opportunities. This is supported by our analysis of food packaging films market trends and comprehensive coverage of cling films market developments.