| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 6.13 Billion |

| Market Size (2030) | USD 10.23 Billion |

| CAGR (2025 - 2030) | 10.79 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Climate Change Consulting Market Analysis

The Climate Change Consulting Market size is estimated at USD 6.13 billion in 2025, and is expected to reach USD 10.23 billion by 2030, at a CAGR of 10.79% during the forecast period (2025-2030).

The climate change consulting industry is experiencing significant transformation driven by increasing corporate awareness and regulatory pressures. According to the International Energy Agency, global energy-related CO2 emissions reached a new record of 37.49 billion metric tons in 2022, highlighting the urgent need for strategic climate change consulting services. Major consulting firms are actively expanding their capabilities through strategic acquisitions, as evidenced by ERM's acquisition of Coho in February 2023, which added over 160 climate and sustainability specialists to their team. These consolidations are reshaping the competitive landscape and enabling firms to offer more comprehensive solutions for emissions reduction, renewable energy transition, and water resilience objectives.

The industry is witnessing a notable shift in corporate attitudes toward sustainability consulting services. According to the Business Insights and Conditions Survey (BICS), 39% of UK firms across various industries expressed significant concerns about climate change's impact on their operations in 2022, with the manufacturing sector showing the highest level of concern at 52%. This growing awareness has led to increased demand for specialized services such as carbon footprint assessment, climate risk consulting, and sustainable strategy development. In March 2023, Boston Consulting Group formed its Global Center for Climate & Sustainability Policy & Regulation, demonstrating the industry's response to growing corporate demands for climate expertise.

Technological innovation and digital transformation are revolutionizing the delivery of sustainability consulting services. Consulting firms are increasingly integrating advanced analytics, artificial intelligence, and digital platforms to provide more accurate climate risk assessments and carbon footprint measurements. This trend is exemplified by recent developments such as Sweco's launch of the Carbon Cost Compass climate footprint calculator and the formation of Twinfinity AB, a platform for digital twins. These technological advancements are enabling consultants to offer more sophisticated and data-driven solutions to their clients.

The renewable energy sector is emerging as a crucial driver for environmental consulting services. In March 2023, Actis launched a USD 500 million Japan-focused renewables platform targeting 1.1 GW of onshore wind and solar power generation by 2027, highlighting the growing investment in sustainable energy infrastructure. According to the International Energy Agency, emissions from Asia's emerging markets and developing economies grew by 4.2% in 2022, emphasizing the need for specialized consulting services in regions transitioning to renewable energy sources. Consulting firms are increasingly focusing on helping organizations navigate the complex landscape of renewable energy adoption, carbon market mechanisms, and sustainable infrastructure development.

Climate Change Consulting Market Trends

Increased Focus on the Reduction of Carbon Footprint and Fulfillment of Net Zero Targets

The increasing focus on reducing carbon footprint has emerged as a primary driver of the climate change consulting market, as governments and businesses worldwide recognize the urgent need to reduce greenhouse gas emissions. Global carbon dioxide emissions from industry and fossil fuels reached 37.12 billion metric tons in 2021, representing a concerning 60% increase since 1990. This dramatic rise in emissions has prompted organizations to seek professional guidance in developing and implementing comprehensive strategies for carbon footprint reduction. The launch of initiatives like the UN Climate Change Conference of the Parties (COP27) Net-Zero Government Initiative in 2022, which has attracted 18 countries to commit to achieving net-zero emissions from national government operations by 2050, demonstrates the growing momentum toward carbon neutrality.

The private sector is increasingly demonstrating its commitment to carbon reduction through strategic partnerships and initiatives. In January 2023, Danone launched a strategic partnership with the Environmental Defense Fund to support its methane reduction ambitions, targeting a 30% reduction in methane emissions from their fresh milk supply chain by 2030. This partnership encompasses improved science, data, reporting standards, and innovative financing models. Similarly, in April 2023, global professional services company GHD expanded its sustainability agenda by announcing a commitment to set net-zero greenhouse gas emissions targets through the Science Based Targets initiative (SBTi), highlighting the growing trend of firms actively pursuing consulting for carbon footprint reduction goals.

Understand The Key Trends Shaping This Market

Download PDF

National Goals Across the Globe to Combat Climate Change

Nations worldwide are implementing ambitious climate action plans and policies to address the escalating challenges posed by climate change. The severity of the situation is exemplified by extreme weather events, including heat waves, droughts, floods, and tropical cyclones, which are becoming more frequent and intense. These events are having far-reaching consequences, from disrupting water management and agricultural output to threatening food security, raising health risks, and damaging critical infrastructure. In response, governments are establishing comprehensive frameworks and making substantial investments in climate action, such as the United States Environmental Protection Agency's allocation of USD 250 million in March 2023 for developing cutting-edge plans to reduce climate pollution and create clean energy businesses.

International collaboration has become a cornerstone of climate action, as evidenced by significant cross-border initiatives and partnerships. For instance, in March 2023, the United States and Spain announced their collaboration to host an international climate and energy summit focused on accelerating the global clean energy transition. The International Energy Agency reports that emissions from Asia's emerging markets and developing economies grew significantly in 2022, increasing by 4.2% and highlighting the urgent need for coordinated international action. This has led to the establishment of programs like the Global Shield Against Climate Risks, a joint effort of the G7 and V20 Group of vulnerable nations, which received commitments of EUR 210 million from countries including Canada, Germany, the United States, France, Denmark, and Ireland to address climate-related damage and loss in vulnerable nations. This underscores the importance of consulting on climate risk and consulting on climate resilience to mitigate such impacts.

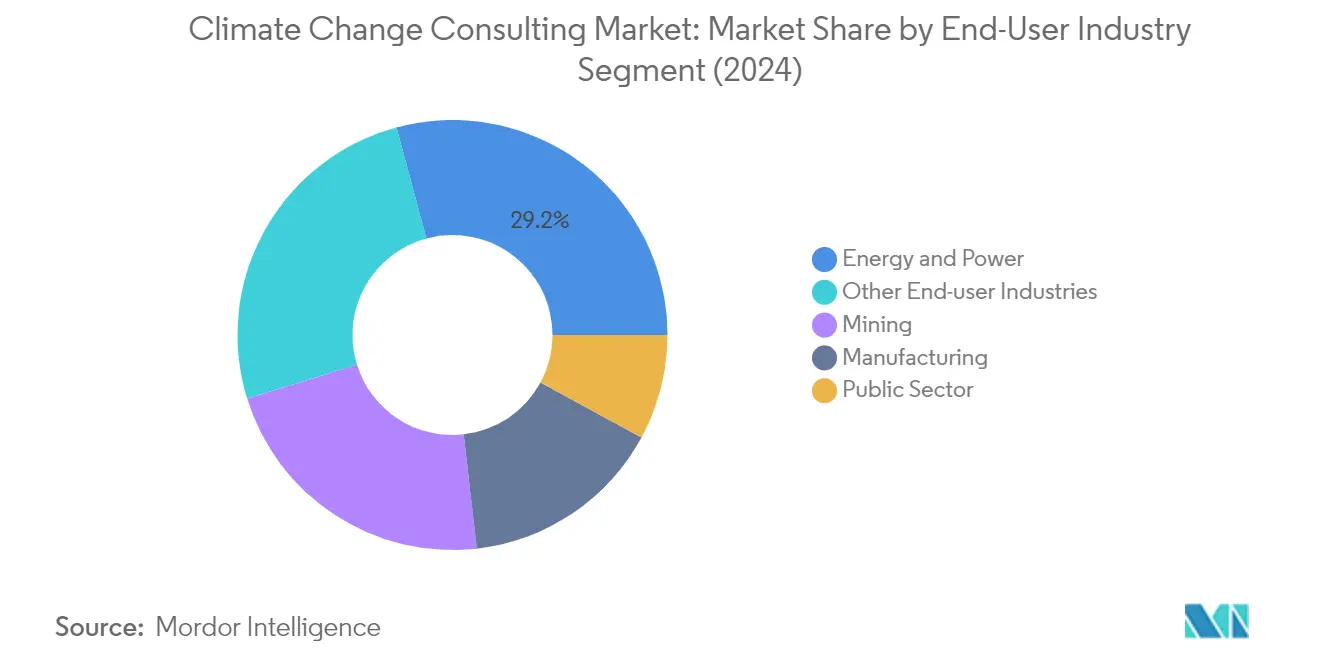

Segment Analysis: By End-User Industry

Energy and Power Segment in Climate Change Consulting Market

The Energy and Power segment maintains its dominant position in the climate change consulting market, commanding approximately 29% market share in 2024. This leadership position is driven by the sector's significant transformation toward cleaner and more sustainable energy sources, including solar, wind, and hydropower technologies. The segment's prominence is further reinforced by the increasing focus on renewable energy integration, decarbonization initiatives, plant digitalization, energy storage solutions, and the implementation of smart grids. Energy and power companies are actively seeking environmental management consulting services to minimize greenhouse gas emissions while navigating complex regulatory frameworks and designing comprehensive sustainability plans. The sector's substantial contribution to global emissions has made it a primary target for climate change initiatives, creating a strong demand for specialized consulting services in areas such as carbon footprint consulting, renewable energy planning, and energy efficiency optimization.

Public Sector Segment in Climate Change Consulting Market

The Public Sector segment has emerged as one of the fastest-growing segments in the climate change consulting market, with a projected growth rate of approximately 14% during 2024-2029. This remarkable growth is driven by increasing government initiatives to combat climate change and fulfill international commitments. Public sector organizations are increasingly seeking specialized guidance on climate change mitigation, adaptation strategies, and sustainability planning at various levels—local, regional, national, and global. The segment's growth is further accelerated by the need for expertise in developing and implementing successful climate action plans, policies, and initiatives. Consulting firms are playing a crucial role in helping public sector entities undertake greenhouse gas inventories, establish data collection methodologies, and develop reporting systems aligned with international protocols.

Remaining Segments in End-User Industry

The Mining, Manufacturing, and Other End-user Industries segments collectively represent significant portions of the climate change consulting market, each addressing unique environmental challenges. The Mining sector focuses on sustainable practices and emission reduction in extraction operations, while the Manufacturing segment emphasizes energy efficiency and sustainable supply chain management. Other End-user Industries, including construction, agriculture, healthcare, and transportation, are increasingly adopting sustainability consulting services to address sector-specific environmental challenges. These segments are characterized by growing awareness of sustainability requirements, regulatory compliance needs, and the imperative to transition toward low-carbon operations. Each sector requires specialized consulting approaches, from developing adaptation strategies to implementing sustainable practices and managing climate-related risks.

Climate Change Consulting Market Geography Segment Analysis

Climate Change Consulting Market in North America

North America represents a dominant force in the global environmental consulting market, with the United States and Canada leading significant initiatives in sustainability and environmental protection. The region's market is characterized by robust regulatory frameworks, increasing corporate sustainability commitments, and growing awareness of climate-related risks. Both countries have demonstrated a strong commitment to reducing greenhouse gas emissions through various policy measures and corporate initiatives, with a particular focus on energy transition, sustainable infrastructure development, and carbon footprint reduction strategies.

Climate Change Consulting Market in United States

The United States stands as the largest market for climate change consulting services in North America, commanding approximately 82% of the regional market share in 2024. The country's market is driven by comprehensive climate action plans at federal, state, and local levels, with particular emphasis on renewable energy transition and sustainable infrastructure development. The Biden administration's commitment to addressing climate change has created additional momentum for consulting services, especially in areas of carbon reduction strategies and climate resilience planning. Various sectors, including energy, manufacturing, and public services, are actively seeking expertise to align their operations with national climate goals and environmental regulations.

Climate Change Consulting Market in Canada

Canada's sustainability consulting market demonstrates strong growth potential with a projected CAGR of approximately 11% from 2024 to 2029. The country's commitment to environmental protection and sustainable development has created significant opportunities for consulting services, particularly in regions facing rapid climate impacts. Canadian businesses and organizations are increasingly seeking expertise in climate resilience, carbon reduction strategies, and sustainable resource management. The country's focus on protecting its vast natural resources while transitioning to a low-carbon economy has created sustained demand for specialized consulting services across various sectors.

Climate Change Consulting Market in Europe

Europe maintains a strong position in the global environmental consulting market, with diverse initiatives across multiple countries including the United Kingdom, Germany, Spain, Italy, France, Benelux, and Poland. The region's commitment to the European Green Deal and various national climate policies has created a robust market for consulting services. Each country brings unique strengths and focus areas, from the UK's emphasis on corporate sustainability to Germany's energy transition initiatives, and France's climate resilience programs. The region's integrated approach to climate action, coupled with stringent regulatory requirements, continues to drive demand for specialized consulting services.

Climate Change Consulting Market in United Kingdom

The United Kingdom emerges as the largest market for climate strategy consulting services in Europe, holding approximately 30% of the regional market share in 2024. The country's leadership in climate action is reflected in its comprehensive net-zero strategy and corporate sustainability initiatives. British businesses and organizations are actively seeking consulting expertise to navigate complex environmental regulations and implement effective climate strategies. The country's focus on renewable energy development, sustainable urban planning, and green finance has created sustained demand for specialized consulting services.

Climate Change Consulting Market in Germany

Germany demonstrates the highest growth potential in Europe's sustainability consulting market, with a projected CAGR of approximately 14% from 2024 to 2029. The country's ambitious energy transition goals and strong industrial base create significant opportunities for consulting services. German organizations are increasingly seeking expertise in areas such as industrial decarbonization, renewable energy integration, and sustainable manufacturing practices. The country's commitment to achieving carbon neutrality has sparked increased demand for specialized consulting services across various sectors.

Climate Change Consulting Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for environmental consulting services, with China and Australia leading significant initiatives in sustainability and environmental protection. The region's rapid industrialization, coupled with increasing environmental awareness, has created substantial opportunities for consulting services. Both countries are implementing ambitious climate action plans, though their approaches and priorities differ based on their unique economic and environmental contexts.

Climate Change Consulting Market in China

China represents the largest market for climate change consulting services in the Asia-Pacific region, driven by its comprehensive national climate strategy and industrial transformation initiatives. The country's focus on sustainable development and environmental protection has created significant demand for consulting expertise. Chinese organizations across various sectors are actively seeking guidance on emission reduction strategies, clean energy transition, and sustainable industrial practices.

Climate Change Consulting Market in Rest of Asia-Pacific

The Rest of Asia-Pacific region demonstrates the highest growth potential in the environmental consulting market, driven by rapid industrialization and increasing environmental awareness. Countries in this region are actively implementing climate action plans and seeking expertise in areas such as renewable energy development, sustainable urban planning, and climate resilience strategies. The region's diverse economic landscape and varying environmental challenges create unique opportunities for specialized consulting services.

Climate Change Consulting Market in Latin America

Latin America's climate change consulting market is characterized by growing awareness of environmental challenges and increasing adoption of sustainable practices, with Brazil emerging as both the largest and fastest-growing market in the region. The region's rich biodiversity and natural resources create unique challenges and opportunities for climate consulting services. Countries across Latin America are implementing various initiatives to address climate change, particularly in areas of deforestation prevention, renewable energy development, and sustainable agriculture. The region's commitment to international climate agreements and increasing corporate sustainability awareness continues to drive demand for specialized consulting services.

Climate Change Consulting Market in Middle East & Africa

The Middle East & Africa region presents unique opportunities in the environmental consulting market, driven by increasing awareness of climate vulnerabilities and the need for sustainable development. The region faces distinct challenges related to water scarcity, extreme temperatures, and energy transition. Countries across the region are implementing various initiatives to diversify their economies and reduce dependence on fossil fuels, creating demand for specialized consulting services. The region's focus on sustainable urban development, renewable energy projects, and climate resilience strategies continues to drive market growth.

Get Analysis on Important Geographic Markets

Download PDF

Climate Change Consulting Industry Overview

Top Companies in Climate Change Consulting Market

The environmental consulting industry features prominent players like Jacobs Solutions, AECOM, WSP Global, Stantec, Ramboll Group, Tetra Tech, ERM International, and others who are actively shaping the industry landscape through various strategic initiatives. These companies are increasingly focused on expanding their service portfolios through technological innovation, particularly in areas like carbon footprint analysis, sustainability strategies, and climate resilience solutions. Market leaders are demonstrating strong operational agility by rapidly adapting their service offerings to meet evolving client needs across different sectors, from energy and power to public infrastructure. Strategic partnerships and collaborations with technology providers and research institutions have become a key trend as firms seek to enhance their capabilities in data analytics, artificial intelligence, and climate modeling. Geographic expansion remains a priority, with companies establishing new offices and strengthening their presence in emerging markets while simultaneously deepening their footprint in established regions.

Dynamic Market Structure Drives Industry Evolution

The sustainability consulting industry exhibits a moderately fragmented structure, characterized by a mix of global consulting conglomerates and specialized environmental advisory services firms. Large multinational players leverage their extensive resources, cross-sector expertise, and established client relationships to maintain market leadership, while specialized firms compete through deep technical knowledge and focused service offerings in specific areas like carbon management or climate resilience. The market has witnessed significant consolidation through mergers and acquisitions, as larger firms seek to acquire specialized capabilities and expand their geographic reach, while smaller firms join forces to achieve scale and enhance their service portfolios.

The competitive dynamics are further shaped by the increasing presence of new entrants, particularly technology-focused consulting firms and boutique sustainability advisories. Market consolidation continues to accelerate as established players pursue strategic acquisitions to strengthen their positions in key growth markets and acquire emerging technologies and specialized expertise. Regional players are increasingly forming strategic alliances and partnerships to compete more effectively with global firms, while also maintaining their local market advantages and specialized knowledge of regional regulatory environments and client needs.

Innovation and Adaptability Drive Market Success

Success in the climate change consulting market increasingly depends on firms' ability to combine technical expertise with innovative service delivery models and digital capabilities. Incumbent firms are focusing on developing proprietary tools and methodologies, investing in advanced analytics capabilities, and building specialized sector expertise to maintain their competitive advantage. The ability to offer integrated solutions that address both immediate climate challenges and long-term sustainability goals has become crucial, while maintaining strong relationships with regulatory bodies and industry stakeholders helps firms stay ahead of evolving compliance requirements and market trends.

Market contenders can gain ground by focusing on niche specializations, developing innovative service offerings, and leveraging technology to deliver more efficient and cost-effective solutions. The relatively low threat of substitution services provides opportunities for firms to differentiate themselves through specialized expertise and tailored solutions. However, success requires careful consideration of end-user concentration in key sectors and the ability to adapt to increasingly stringent regulatory requirements. Building strong client relationships, maintaining thought leadership in specific areas, and demonstrating a clear value proposition through measurable outcomes have become essential factors for gaining market share in this evolving environmental consulting industry.

Climate Change Consulting Market Leaders

-

Jacobs Solutions Inc.

-

AECOM

-

WSP Global Inc.

-

Stantec Inc.

-

Ramboll Group A/S

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Climate Change Consulting Market News

- March 2023 - Boston Consulting Group (BCG) launched its Global Center for Climate & Sustainability Policy & Regulation, a virtual platform designed to help clients navigate climate policy and align with global net-zero goals.

- March 2023 - Aurecon introduced a new sustainability advisory team in New Zealand, focusing on decarbonization and resilience, aimed at helping businesses reduce emissions and enhance climate resilience.

Climate Change Consulting Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Size Estimates and Forecasts for the Study Period

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the World to Combat Climate Change

- 5.1.3 Emerging Trends in Climate Change Consulting

-

5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

- 5.2.2 Barriers to adoption lead to Challenge of the market

- 5.3 Key Trend Analysis within Various Services

6. MARKET SEGMENTATION

-

6.1 By End-user Industry

- 6.1.1 Energy and Power

- 6.1.2 Mining

- 6.1.3 Public Sector

- 6.1.4 Manufacturing

- 6.1.5 Other End-user Industries

-

6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 Spain

- 6.2.2.4 Italy

- 6.2.2.5 France

- 6.2.2.6 Benelux

- 6.2.2.7 Poland

- 6.2.2.8 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 Australia

- 6.2.3.2 China

- 6.2.3.3 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Rest of Latin America

- 6.2.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Jacobs Solutions Inc.

- 7.1.2 AECOM

- 7.1.3 WSP Global Inc.

- 7.1.4 Stantec Inc.

- 7.1.5 Ramboll Group A/S

- 7.1.6 Tetra Tech Inc.

- 7.1.7 ERM International Group Limited

- 7.1.8 Ove Arup & Partners International Ltd

- 7.1.9 GHD Group Limited

- 7.1.10 Sweco AB

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Climate Change Consulting Industry Segmentation

Climate change consultation is a process in which people, organizations, or communities seek feedback and acquire information to address the difficulties and implications of climate change. It entails gathering opinions, thoughts, and suggestions on climate-related policies, strategies, and actions from a variety of stakeholders, including government agencies, experts, corporations, community people, and environmental organizations. Climate change consultation strives to promote collaboration, raise awareness, and enable inclusive decision-making, enabling educated and effective responses to climate change mitigation, adaptation, and resilience activities at the local, regional, and global levels.

The climate change consulting market study tracks the demand (regarding value) from various end-user industries, such as energy and power, mining, the public sector, manufacturing, and other end-user industries. The market has been tracked by analyzing the revenues generated by major global climate change consulting players. The impact of COVID-19, and other macroeconomic factors, are considered to arrive at the overall market projections.

The climate change consulting market is segmented by end-user industry (energy and power, mining, public sector, manufacturing, and other end-user industries), by geography (North America (United States and Canada), Europe (United Kingdom, Germany, Spain, Italy, France, Benelux, and Poland), Asia-Pacific (Australia, China, and rest of Asia-Pacific), Latin America (Brazil and rest of Latin America), and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the segments.

| By End-user Industry | Energy and Power | ||

| Mining | |||

| Public Sector | |||

| Manufacturing | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| Spain | |||

| Italy | |||

| France | |||

| Benelux | |||

| Poland | |||

| Rest of Europe | |||

| Asia-Pacific | Australia | ||

| China | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Climate Change Consulting Market Research Faqs

How big is the Climate Change Consulting Market?

The Climate Change Consulting Market size is expected to reach USD 6.13 billion in 2025 and grow at a CAGR of 10.79% to reach USD 10.23 billion by 2030.

What is the current Climate Change Consulting Market size?

In 2025, the Climate Change Consulting Market size is expected to reach USD 6.13 billion.

Who are the key players in Climate Change Consulting Market?

Jacobs Solutions Inc., AECOM, WSP Global Inc., Stantec Inc. and Ramboll Group A/S are the major companies operating in the Climate Change Consulting Market.

Which is the fastest growing region in Climate Change Consulting Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Climate Change Consulting Market?

In 2025, the North America accounts for the largest market share in Climate Change Consulting Market.

What years does this Climate Change Consulting Market cover, and what was the market size in 2024?

In 2024, the Climate Change Consulting Market size was estimated at USD 5.47 billion. The report covers the Climate Change Consulting Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Climate Change Consulting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Climate Change Consulting Market Research

Mordor Intelligence provides comprehensive insights into the rapidly evolving climate change consulting sector. We leverage our extensive experience in both environmental consulting and sustainability consulting. Our expert analysts offer detailed coverage of ESG consulting trends, environmental impact assessment methodologies, and environmental advisory services. The report examines key areas such as carbon consulting, greenhouse gas consulting, and climate strategy consulting. This offers stakeholders a thorough understanding of market dynamics and growth opportunities.

Our detailed analysis covers climate risk consulting, decarbonization consulting, and climate resilience consulting services. These are available in an easy-to-download report PDF format. The research provides valuable insights into carbon neutrality consulting practices, climate adaptation consulting strategies, and environmental management consulting approaches. Stakeholders benefit from our comprehensive evaluation of the sustainability consulting industry and the environmental consulting industry. This is supported by robust data on carbon footprint consulting services and emerging trends in the climate change advisory landscape.