Market Size of Civil Aerospace Training And Simulation Industry

| Study Period | 2019 - 2029 |

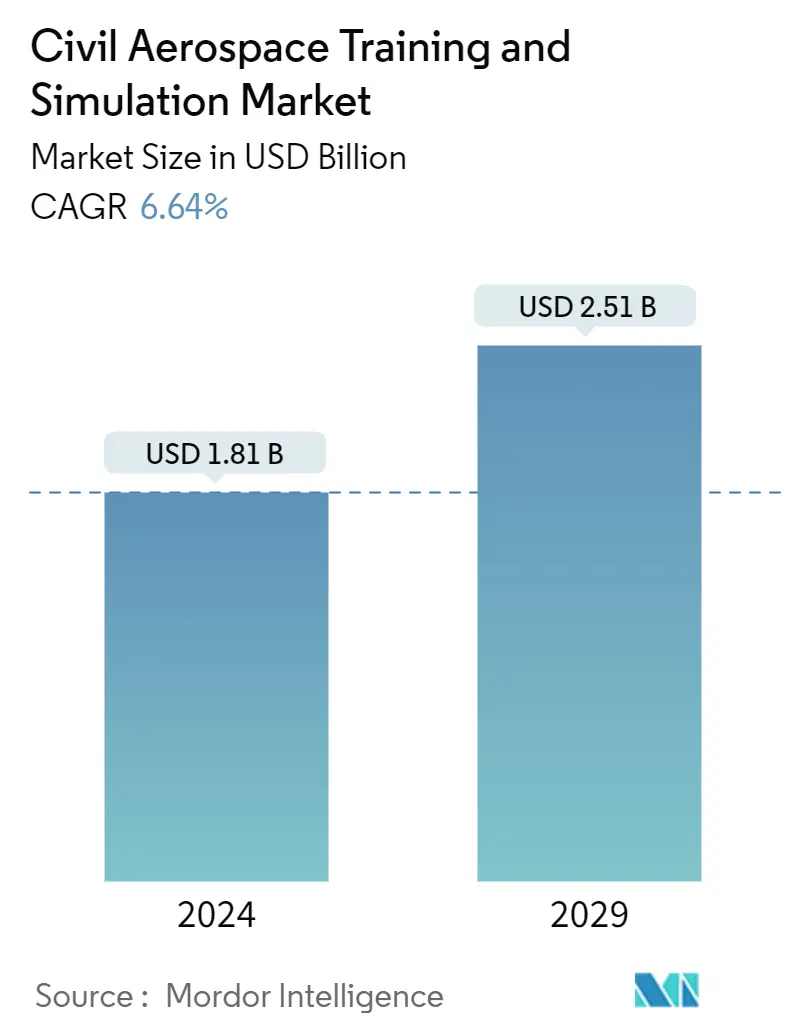

| Market Size (2024) | USD 1.81 Billion |

| Market Size (2029) | USD 2.51 Billion |

| CAGR (2024 - 2029) | 6.64 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Civil Aerospace Simulation and Training Market Analysis

The Civil Aerospace Training And Simulation Market size is estimated at USD 1.81 billion in 2024, and is expected to reach USD 2.51 billion by 2029, growing at a CAGR of 6.64% during the forecast period (2024-2029).

Airlines around the globe were aggressively pursuing fleet expansion and network expansion plans before the emergence of the COVID-19 pandemic. However, following the impact of the COVID-19 pandemic, the airlines have canceled and deferred aircraft orders as well as furloughed their pilots to mitigate the losses due to the impact felt by the pandemic. The aviation industry started recovering in 2022 and gradually returning to its pre-COVID-19 level. According to the latest updates from IATA, ICAO, the Airports Council International (ACI), the UN World Tourism Organization (UNWTO), the World Trade Organization (WTO), and the International Monetary Fund (IMF), the international air passenger traffic in 2022 has improved compared to that of 2021. With the recovery of the aviation industry in 2022, the orders and deliveries of commercial aircraft witnessed a gradual increase, which led to a simultaneous increase in demand for simulators and training devices.

As the aviation industry is expected to return to pre-COVID levels and the fleet of commercial aircraft is expected to increase, the demand for pilots is also expected to increase. Also, currently, many airlines are facing the issue of a pilot shortage, which is affecting their daily operations. Generally, flights longer than 12 hours require a team of four pilots. However, several airlines are still operating such long-haul routes with three pilots due to a shortage of pilots. The shortage of pilots is expected to drive demand for new simulation and training solutions.Also, the planned investments in human space exploration programs during the forecast period are anticipated to generate demand for simulators for astronauts and training solutions in the coming years.

Civil Aerospace Simulation and Training Industry Segmentation

An aerospace simulator is a software or hardware system designed to simulate various aspects of aerospace operations. These simulators are used for training pilots, conducting research, testing aircraft systems, and exploring aerospace concepts. Aerospace simulators can range from simple desktop applications to full-motion flight simulators used by commercial airlines and military organizations. They typically incorporate realistic graphics, physics models, and control interfaces to provide an immersive and interactive experience.

The market is segmented by simulator type, application, and geography. By simulator type, the market is segmented into full flight simulators (FFS), flight training devices (FTD), and other training devices. The other training devices include advanced aviation training devices (AATDs), basic aviation training devices (BATDs), and other visual and training tools used for training spacecraft crew. By application, the market is segmented into commercial aviation and space. The report also covers the market sizes and forecasts for the civil aerospace simulation and training market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Simulator Type | |

| Full Flight Simulator (FFS) | |

| Flight Training Devices (FTD) | |

| Other Training Devices |

| Application | |

| Commercial Aviation | |

| Space |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Civil Aerospace Training And Simulation Market Size Summary

The civil aerospace simulation and training market is poised for significant growth as the aviation industry recovers from the impacts of the COVID-19 pandemic. The market is driven by the increasing demand for pilots due to fleet expansion and the ongoing pilot shortage, which has necessitated the adoption of advanced simulation and training solutions. The full flight simulator (FFS) segment, in particular, is expected to dominate the market, offering realistic training experiences that are crucial for addressing the shortage of trained pilots. Companies like CAE Inc. are actively expanding their training capabilities, as evidenced by their contracts with major airlines such as Qantas Group, to develop new pilot training centers and deploy advanced simulators. The integration of technologies like virtual reality into these simulators is further enhancing training efficiency, supporting the market's growth trajectory.

The Asia-Pacific region is a key area of growth, with major airlines in countries like China and India planning significant aircraft procurements and pilot training expansions. The demand for new pilots in this region is substantial, driven by the procurement of new aircraft and the acceleration of human space exploration programs. Companies such as Boeing and ALSIM are making strategic investments to enhance pilot training capacities in these regions. The market is semi-consolidated, with prominent players like L3Harris Technologies Inc., The Boeing Company, and CAE Inc. leading the way. These companies are focusing on developing new simulators with advanced features to capitalize on the growing demand for civil aerospace simulation and training solutions.

Civil Aerospace Training And Simulation Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Simulator Type

-

2.1.1 Full Flight Simulator (FFS)

-

2.1.2 Flight Training Devices (FTD)

-

2.1.3 Other Training Devices

-

-

2.2 Application

-

2.2.1 Commercial Aviation

-

2.2.2 Space

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 United Kingdom

-

2.3.2.2 Germany

-

2.3.2.3 France

-

2.3.2.4 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 India

-

2.3.3.3 Japan

-

2.3.3.4 South Korea

-

2.3.3.5 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Rest of Latin America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 United Arab Emirates

-

2.3.5.2 Saudi Arabia

-

2.3.5.3 Turkey

-

2.3.5.4 Rest of Middle East and Africa

-

-

-

Civil Aerospace Training And Simulation Market Size FAQs

How big is the Civil Aerospace Simulation And Training Market?

The Civil Aerospace Simulation And Training Market size is expected to reach USD 1.81 billion in 2024 and grow at a CAGR of 6.64% to reach USD 2.51 billion by 2029.

What is the current Civil Aerospace Simulation And Training Market size?

In 2024, the Civil Aerospace Simulation And Training Market size is expected to reach USD 1.81 billion.