Civil Aerospace Training And Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

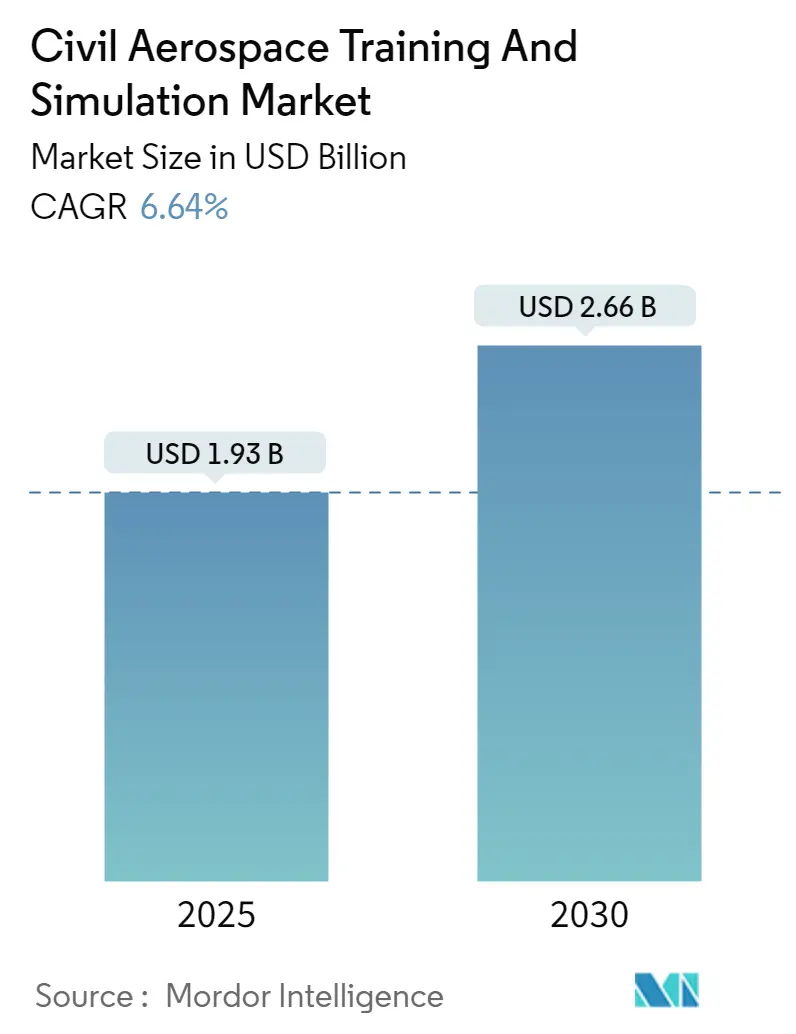

| Market Size (2025) | USD 1.93 Billion |

| Market Size (2030) | USD 2.66 Billion |

| Growth Rate (2025 - 2030) | 6.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Civil Aerospace Training And Simulation Market Analysis by Mordor Intelligence

The Civil Aerospace Training And Simulation Market size is estimated at USD 1.93 billion in 2025, and is expected to reach USD 2.66 billion by 2030, at a CAGR of 6.64% during the forecast period (2025-2030).

The civil aerospace simulation and training market is experiencing significant transformation driven by technological advancements and increasing air travel demand. According to IATA data, air passenger traffic demonstrated strong recovery, reaching 68.5% of pre-pandemic revenue passenger kilometers (RPKs) in 2022, indicating a robust industry revival. The integration of advanced technologies like virtual reality, augmented reality, and artificial intelligence into training systems has revolutionized pilot training methodologies, enabling more realistic and comprehensive training scenarios. Flight simulators now incorporate sophisticated features such as high-fidelity visual systems, motion platforms, and real-time weather simulation capabilities, enhancing the overall training experience.

The industry faces a critical challenge in addressing the growing demand for trained aviation professionals. Boeing's 2022 Pilot & Technician Outlook projects a requirement for 602,000 new civil aviation pilots over the next 20 years, highlighting the substantial need for expanded training infrastructure. Training providers are responding by modernizing their facilities and adopting innovative approaches, including standardized training requirements and digital learning platforms. Airlines and training centers are increasingly investing in state-of-the-art simulation technology to ensure efficient, cost-effective, and comprehensive pilot training programs.

The space segment of the training and simulation market is witnessing unprecedented growth, driven by increased commercial space activities and government investments. In 2022, global government expenditure for space programs reached a record USD 103 billion, with significant investments in astronaut training and simulation technologies. The industry achieved a milestone with 186 successful rocket launches in 2022, representing a 28.27% increase in launch frequency, necessitating advanced training solutions for space personnel.

Recent industry developments demonstrate substantial investments in training infrastructure and capabilities. In February 2023, Emirates Airlines announced a USD 135 million investment in a new pilot training center, which will feature six Full Flight Simulator Bays (FFS) and boost the airline's pilot training capacity by 54% annually. Similarly, in April 2023, Boeing brought its B737 Max flight simulator to its Shanghai training center, enhancing regional training capabilities. These developments reflect the industry's commitment to expanding and upgrading training facilities to meet growing demand while incorporating the latest technological advancements in aerospace simulation and training systems.

Global Civil Aerospace Training And Simulation Market Trends and Insights

Airline Expansion Plans Driving Demand for Pilots

The aviation industry is witnessing an unprecedented surge in global pilot demand, driven by aggressive fleet expansion plans and the impending retirement of experienced pilots. According to Boeing's 2022 Pilot & Technician Outlook, the industry will require 602,000 new civil aerospace pilots, 610,000 new maintenance technicians, and 899,000 new cabin crew members to operate and maintain the global commercial fleet over the next 20 years. This substantial demand is further intensified by the latest disclosures from the International Air Transport Association (IATA), which reported that air passenger traffic recovered significantly, reaching 68.5% of 2019's revenue passenger kilometers (RPKs) in 2022, indicating a robust recovery in air travel demand.

Airlines worldwide are implementing various strategies to address the growing pilot shortage, which is already affecting their daily operations. Long-haul flights exceeding 12 hours typically require a team of four pilots, but several airlines are operating such routes with only three pilots due to staffing constraints. To combat this shortage, airlines are developing comprehensive pilot creation programs and establishing training academies through partnerships with professional institutions and universities. Some carriers are also revising their minimum requirements for captain qualification to expedite pilot progression, while others are offering substantial salary premiums of 10-15% compared to carriers in the Western Hemisphere to attract experienced pilots. These initiatives, coupled with Boeing's Commercial Market Outlook projecting the global commercial aviation fleet to double to 47,080 aircraft by 2041, underscore the critical need for expanded civil aerospace simulation and training capabilities.

Increase in Space Exploration Activities

The space sector is experiencing remarkable growth, with global government expenditure for space programs reaching a record USD 103 billion in 2022. This expansion is accompanied by an unprecedented increase in launch activities, with 186 successful rocket launches recorded in 2022, representing a 28.27% increase in launch frequency. These developments are driving the demand for sophisticated training solutions as space agencies and private companies prepare for increasingly complex missions. Notable upcoming missions include the September 2023 return of the OSIRIS-Rex mission with samples from asteroid Bennu, and NASA's launch of the Psyche spacecraft to explore the metallic asteroid 16 Psyche, demonstrating the diverse range of space exploration activities requiring specialized training.

The commercial space industry has emerged as a significant driver of growth, with companies like SpaceX, Blue Origin, and others investing heavily in space missions for various purposes, including satellite deployment, space tourism, and resource extraction. For instance, Pittsburgh-based Astrobotic's Peregrine Mission 1 (PM1) represents a milestone as the first commercial mission attempting to land on another planetary body. The mission will utilize United Launch Alliance's new Vulcan Centaur rocket, a sophisticated 82-meter-tall methane-fueled launcher powered by seven BE-4 engines. Additionally, SpaceX's ongoing Crew missions to the International Space Station, including the March 2023 launch of Crew 6 for a 180-day science expedition, highlight the increasing frequency and complexity of human spaceflight operations that require extensive aerospace simulation and virtual training and simulation market solutions.

Segment Analysis: Simulator Type

Full Flight Simulator Segment in Civil Aerospace Training and Simulation Market

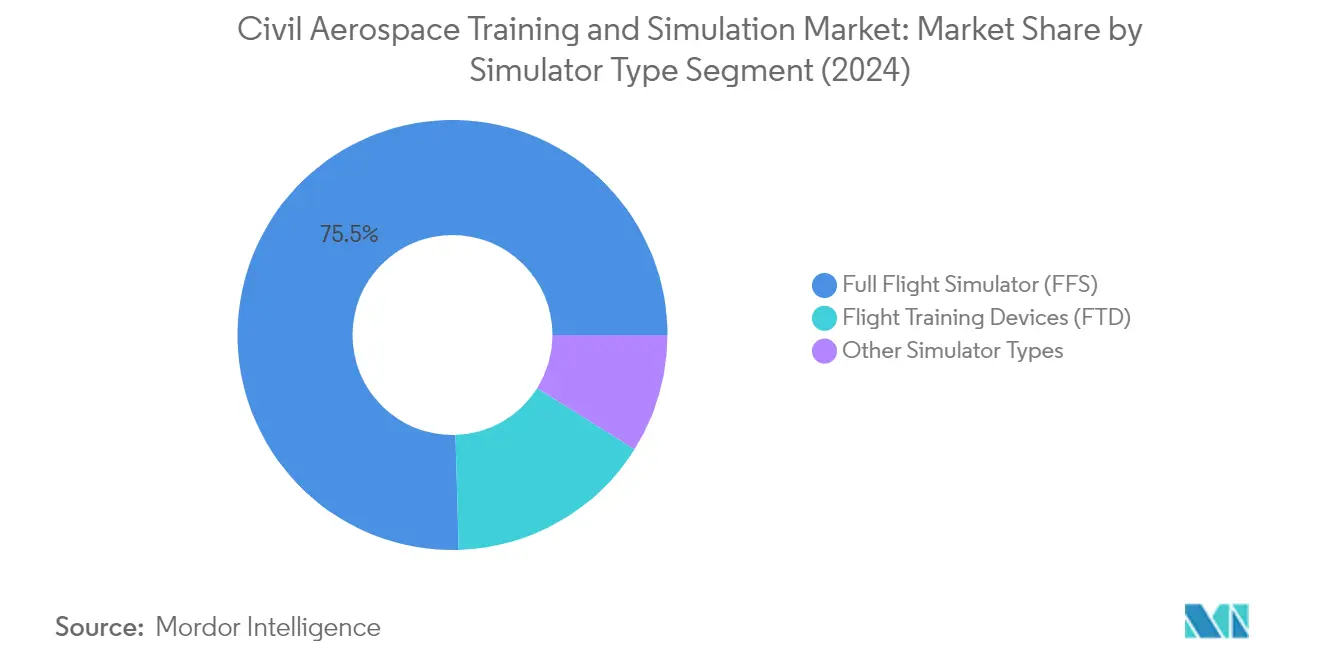

The Full Flight Simulator (FFS) segment continues to dominate the civil aerospace simulation and training market, commanding approximately 75% market share in 2024. This significant market position is attributed to the FFS's superior capability to replicate critical flight parameters such as movement and acoustics of modern aircraft and spacecraft by accurately simulating acceleration and G-forces acting on the platform. These sophisticated simulators provide an immersive training environment that closely mirrors real-world flying conditions, making them indispensable for commercial pilot training programs. The segment's dominance is further reinforced by stringent regulatory requirements that mandate specific hours of FFS training for pilot certification and type ratings across different aircraft categories.

Flight Training Devices Segment in Civil Aerospace Training and Simulation Market

The Flight Training Devices (FTD) segment is experiencing robust growth in the civil aerospace simulation and training market for the period 2024-2029. This growth is driven by the increasing adoption of FTDs as cost-effective complementary training tools alongside full flight simulators. FTDs are gaining popularity among flight schools and training organizations due to their versatility in providing procedural training, systems familiarization, and basic flight control practice. The segment's expansion is further supported by technological advancements in visual systems, computing power, and motion cuing, which have significantly enhanced the training experience while maintaining a lower cost structure compared to full flight simulators.

Remaining Segments in Simulator Type

Other simulator types in the market include basic aviation training devices, flight navigation procedure trainers, and specialized task trainers. These segments play a crucial supporting role in the overall pilot training ecosystem by providing focused training for specific skills and procedures. While these simulators may not offer the same level of fidelity as FFS or FTDs, they serve essential functions in early-stage pilot training, procedure practice, and specialized operations training. The continued development of these complementary training devices contributes to a comprehensive and multi-layered approach to pilot training, ensuring that various training needs are met at different stages of a pilot's career development.

Segment Analysis: Application

Commercial Aviation Segment in Civil Aerospace Training and Simulation Market

The commercial aviation segment dominates the civil aerospace training and simulation market, holding approximately 73% market share in 2024. This significant market position is driven by the increasing global air traffic and subsequent need for skilled pilots across commercial airlines. Airlines, flight training academies, and aviation organizations heavily rely on simulators to train their pilots efficiently, cost-effectively, and safely. The segment's dominance is further reinforced by the growing adoption of advanced simulation technologies that provide highly realistic and immersive training experiences, incorporating sophisticated graphics, motion systems, and realistic flight dynamics. Additionally, the use of flight simulators for commercial aviation training results in substantial cost savings compared to traditional training methods by eliminating fuel costs, reducing aircraft wear and tear, and minimizing the need for expensive on-aircraft training hours.

Space Segment in Civil Aerospace Training and Simulation Market

The space segment is projected to exhibit the fastest growth in the civil aerospace training and simulation market, with an estimated CAGR of approximately 7% during 2024-2029. This accelerated growth is primarily attributed to the rapid increase in space sector activities, particularly manned missions that require extensive astronaut training. The segment's growth is driven by the increasing complexity of space missions, which necessitates comprehensive training on different operational, mission-critical, and emergency parameters for extended durations. The expansion is further supported by significant investments in advanced simulation technologies that can accurately replicate the unique challenges of space environments, including zero-gravity conditions and spacecraft operations. The rise in commercial space ventures and the growing number of countries developing space programs are also contributing to the increased demand for sophisticated space simulation and training solutions.

Civil Aerospace Training And Simulation Market Geography Segment Analysis

Civil Aerospace Training and Simulation Market in North America

The North American civil aerospace simulation and training market demonstrates robust growth driven by the presence of major simulator manufacturers, established flight training academies, and a mature aerospace sector. The United States and Canada form the key markets in this region, with both countries showing significant investments in advanced simulation technologies and training infrastructure. The region benefits from stringent regulatory frameworks that mandate comprehensive pilot training programs, creating sustained demand for simulation-based training solutions. The presence of leading airlines and their expanding fleet sizes continues to drive the need for more sophisticated training facilities and simulators across North America.

Civil Aerospace Training and Simulation Market in United States

The United States maintains its position as the dominant force in the North American market, holding approximately 87% of the regional civil aerospace market share in 2024. The country's leadership is supported by its extensive network of flight training facilities, the largest aircraft fleet, and numerous operational airports. Major airlines in the US are actively expanding their training capabilities through significant investments in simulator facilities. The presence of key industry players and continuous technological advancements in simulation technology further strengthens the US market position. The country's robust aviation infrastructure and growing demand for commercial pilots continue to drive market growth, supported by various pilot training programs and partnerships between airlines and training academies.

Civil Aerospace Training and Simulation Market in Canada

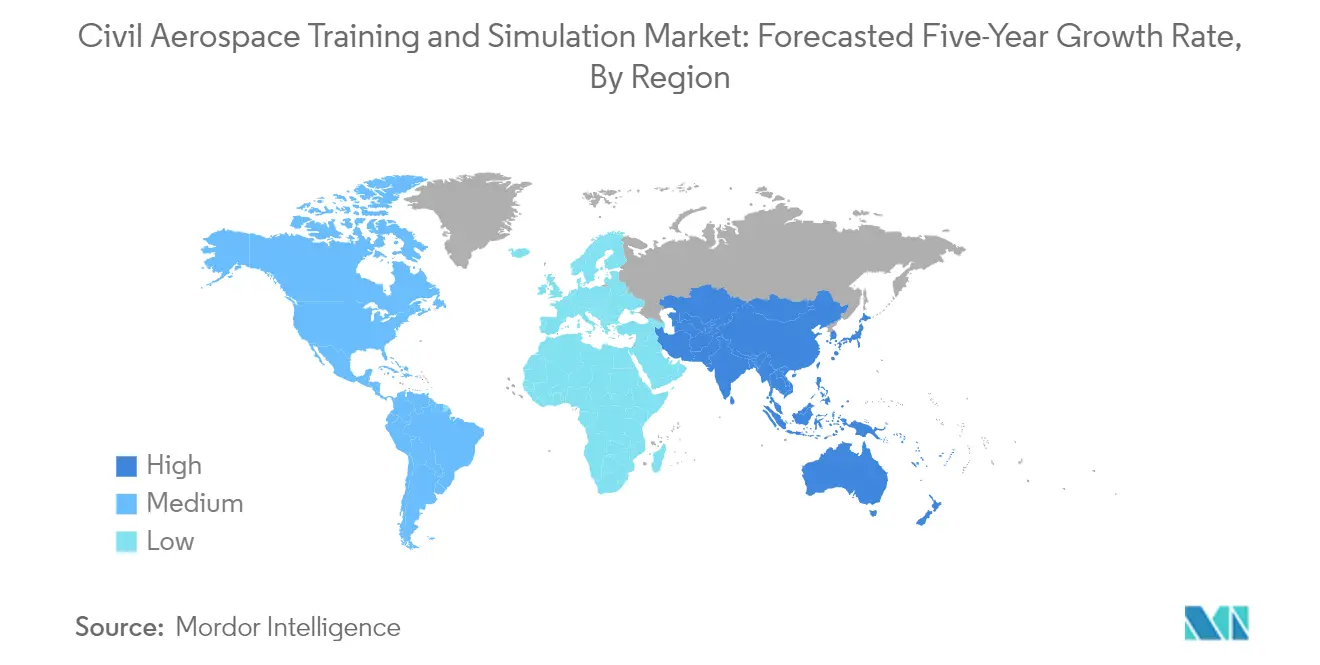

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 7% during 2024-2029. The country's aviation sector is experiencing increased demand for pilot training, driven by expanding commercial aviation activities and growing international student enrollment in Canadian flight schools. Canadian training facilities are increasingly adopting advanced simulation technologies and establishing partnerships with international aviation organizations. The country's focus on modernizing training infrastructure and implementing innovative training methodologies positions it well for sustained growth. Additionally, Canada's strategic initiatives to address pilot shortages and enhance training capabilities contribute to its rapid market expansion.

Civil Aerospace Training and Simulation Market in Europe

The European civil aerospace simulation and training market showcases strong growth potential, characterized by technological innovation and comprehensive training infrastructure. Key markets including the United Kingdom, France, and Germany demonstrate significant investments in advanced simulation technologies and training facilities. The region benefits from strong regulatory oversight by EASA and various national aviation authorities, ensuring high standards in pilot training. The presence of major aircraft manufacturers and their training centers, coupled with increasing air traffic demands, drives continuous innovation in simulation technology and training methodologies across Europe.

Civil Aerospace Training and Simulation Market in United Kingdom

The United Kingdom maintains its leadership position in the European market, commanding approximately 38% of the regional civil aerospace market share in 2024. The country's strong position is supported by its well-established aviation training infrastructure and the presence of major airlines with extensive training facilities. The UK's aviation sector benefits from advanced simulation technologies and comprehensive training programs that attract both domestic and international students. The country's focus on implementing innovative training methodologies and maintaining high safety standards continues to strengthen its market position.

Civil Aerospace Training and Simulation Market in France

France demonstrates remarkable growth potential with a projected growth rate of approximately 7% during 2024-2029, emerging as the fastest-growing market in Europe. The country's aviation sector is experiencing significant developments in simulation technology and training infrastructure. French aviation academies are increasingly adopting advanced training methodologies and expanding their simulator capabilities. The presence of major aerospace manufacturers and their training centers contributes to the market's rapid growth. France's strategic focus on modernizing its aviation training infrastructure and expanding international partnerships positions it well for continued expansion.

Civil Aerospace Training and Simulation Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for civil aerospace simulation and training market analysis, characterized by rapid technological adoption and expanding aviation infrastructure. Countries including China, India, Japan, and South Korea are making significant investments in simulation technology and training facilities. The region's growing air passenger traffic and increasing demand for trained pilots drive substantial investments in training infrastructure. The market benefits from supportive government policies and increasing collaboration between international training providers and local institutions.

Civil Aerospace Training and Simulation Market in China

China maintains its position as the largest market in the Asia-Pacific region, driven by extensive investments in aviation infrastructure and training facilities. The country's aviation sector demonstrates strong growth through the establishment of new training centers and adoption of advanced simulation technologies. Chinese airlines' expanding fleet sizes and growing domestic air travel demand necessitate continuous investments in pilot training infrastructure. The country's focus on developing domestic simulation technology capabilities and establishing partnerships with international training providers further strengthens its market position.

Civil Aerospace Training and Simulation Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by rapid expansion in its aviation sector and increasing investments in training infrastructure. The country's aviation training landscape is transforming through the adoption of advanced simulation technologies and establishment of new training facilities. Indian airlines' fleet expansion plans and growing domestic air traffic create sustained demand for pilot training. The government's supportive policies and focus on developing domestic training capabilities contribute to the market's rapid growth trajectory.

Civil Aerospace Training and Simulation Market in Latin America

The Latin American civil aerospace simulation and training market demonstrates steady growth potential, with Brazil emerging as both the largest and fastest-growing market in the region. The market is characterized by increasing investments in simulation technology and training infrastructure across various countries. The region's growing air passenger traffic and modernization of aviation infrastructure drive demand for advanced training solutions. While facing some infrastructure challenges, the market benefits from increasing collaboration between international training providers and local institutions, supporting the development of comprehensive pilot training programs.

Civil Aerospace Training and Simulation Market in Middle East and Africa

The Middle East and Africa region showcases significant growth potential in the civil aerospace simulation and training market, with the United Arab Emirates leading as the largest market and Turkey emerging as the fastest-growing country. The region benefits from substantial investments in aviation infrastructure and training facilities, particularly in Gulf countries. The market is characterized by strong partnerships between international training providers and local institutions, supporting the development of advanced training capabilities. The region's strategic location and growing role as a global aviation hub drive continued investments in simulation technology and training infrastructure.

Competitive Landscape

Top Companies in Civil Aerospace Training and Simulation Market

The civil aerospace simulation and training market is characterized by continuous product innovation focused on enhancing training realism and effectiveness through advanced technologies. Companies are investing heavily in developing next-generation simulators with improved visual systems, motion capabilities, and integrated training solutions. Operational agility has become crucial as manufacturers adapt to changing industry requirements, particularly in areas of sustainable aviation and electric aircraft simulation. Strategic partnerships between simulator manufacturers and airlines have become increasingly common to develop customized training solutions. Market leaders are expanding their geographical presence through training center establishments and strategic acquisitions, particularly in high-growth regions like Asia-Pacific and the Middle East. The focus has shifted towards providing comprehensive training ecosystems rather than standalone simulator products, incorporating elements like mixed reality, artificial intelligence, and data analytics to enhance training effectiveness.

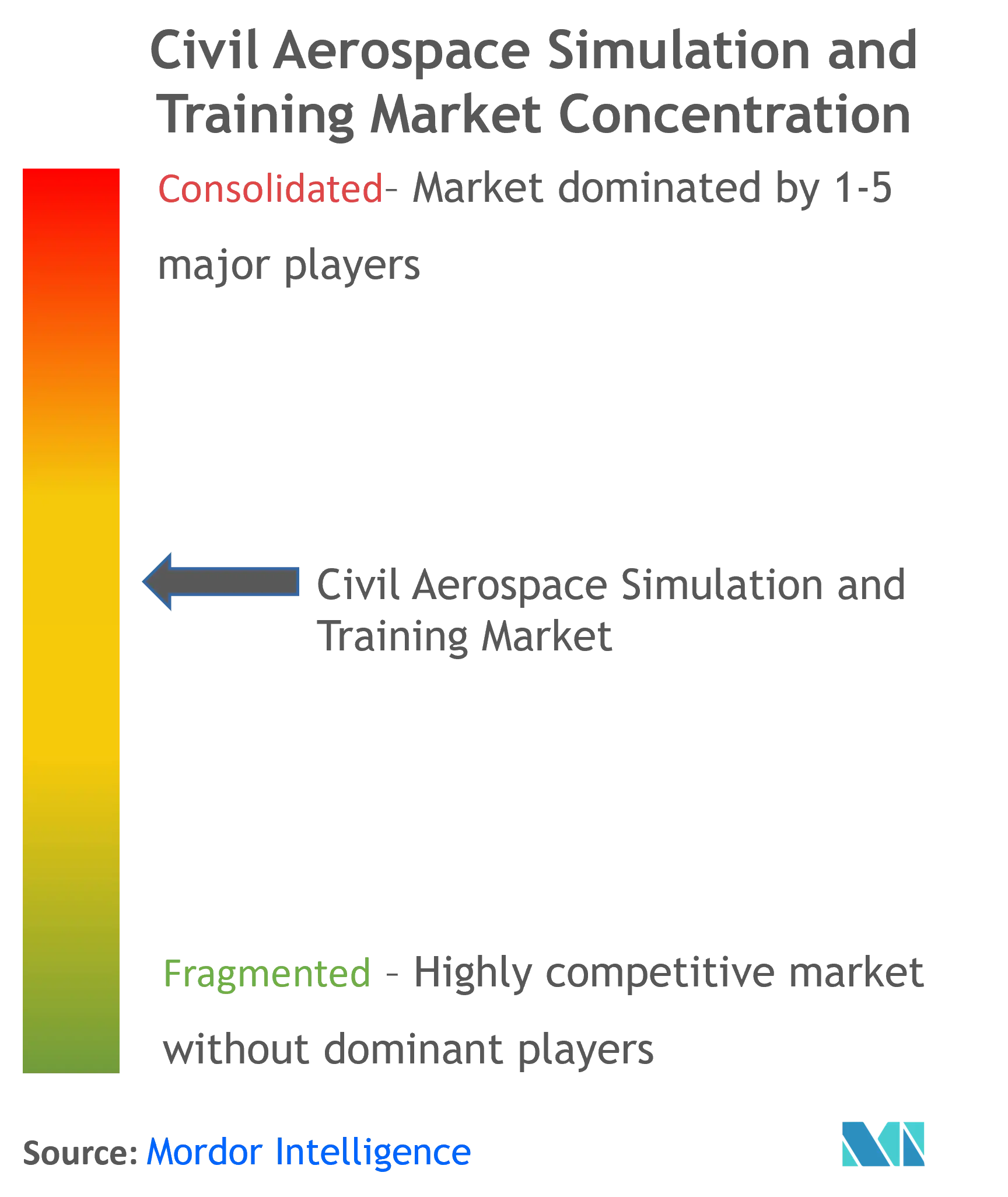

Consolidated Market Led By Global Players

The civil aerospace training and simulation market exhibits a relatively consolidated structure dominated by large global players with diverse aerospace portfolios. Companies like CAE, L3Harris Technologies, and Boeing maintain significant market presence through their established relationships with airlines, comprehensive product offerings, and extensive global training networks. These major players leverage their technological expertise and financial resources to maintain competitive advantages, while specialized simulator manufacturers focus on specific market niches or regional opportunities.

The market has witnessed notable merger and acquisition activities aimed at expanding capabilities and market reach. Large aerospace conglomerates have been actively acquiring smaller, specialized simulation technology companies to enhance their training portfolios and access new customer segments. This consolidation trend has been particularly evident in areas of advanced aerospace simulation technology, virtual reality training solutions, and regional training center operations. The industry structure favors established players due to high entry barriers, including substantial capital requirements, regulatory compliance needs, and the importance of long-term customer relationships.

Innovation and Adaptability Drive Market Success

Success in the civil aerospace training and simulation market increasingly depends on companies' ability to innovate while maintaining cost-effectiveness. Incumbent players must focus on developing next-generation training solutions that address emerging industry needs, particularly in areas of sustainable aviation and electric aircraft operations. Companies need to balance investment in new technologies with maintaining competitive pricing structures, while also expanding their training center networks to capture growing demand in developing markets. The ability to provide flexible, scalable training solutions that can be customized to specific airline requirements has become a crucial differentiator.

Market contenders can gain ground by focusing on specialized market segments or innovative training approaches that address specific industry pain points. This includes developing cost-effective training solutions for regional airlines, creating specialized programs for new aircraft types, or offering innovative financing models for training services. The increasing regulatory focus on pilot training standards and safety requirements presents opportunities for companies that can effectively address compliance needs while maintaining operational efficiency. Success also depends on building strong relationships with aircraft manufacturers and airlines, as well as maintaining the agility to adapt to changing industry requirements and technological advances. The largest flight simulator companies are poised to capture significant civil aerospace market share by leveraging these strategies.

Civil Aerospace Training And Simulation Industry Leaders

-

CAE Inc.

-

L3Harris Technologies, Inc

-

The Boeing Company

-

FlightSafety International

-

Indra Sistemas SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

April 2023: Boeing announced that they have brought its B737 MAX flight simulator to its Shanghai training center to fulfill the promise of improving pilot training for the aircraft in China after two fatal crashes in 2018 and 2019, led to it being grounded worldwide. Moreover, the company installed the B737 MAX Flight Training Device at its training hub at Shanghai Pudong International Airport to better support the operations of Chinese airlines

August 2022: CAE Inc. announced that it had signed a 15-year contract with Qantas Group for the development and operation of a new pilot training center in Sydney. CAE will deploy a new A320 full-flight simulator and purchase B787, A330, and B737NG full-flight simulators from the Qantas Group.

Global Civil Aerospace Training And Simulation Market Report Scope

An aerospace simulator is a software or hardware system designed to simulate various aspects of aerospace operations. These simulators are used for training pilots, conducting research, testing aircraft systems, and exploring aerospace concepts. Aerospace simulators can range from simple desktop applications to full-motion flight simulators used by commercial airlines and military organizations. They typically incorporate realistic graphics, physics models, and control interfaces to provide an immersive and interactive experience.

The market is segmented by simulator type, application, and geography. By simulator type, the market is segmented into full flight simulators (FFS), flight training devices (FTD), and other training devices. The other training devices include advanced aviation training devices (AATDs), basic aviation training devices (BATDs), and other visual and training tools used for training spacecraft crew. By application, the market is segmented into commercial aviation and space. The report also covers the market sizes and forecasts for the civil aerospace simulation and training market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Full Flight Simulator (FFS) |

| Flight Training Devices (FTD) |

| Other Training Devices |

| Commercial Aviation |

| Space |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East and Africa |

| Simulator Type | Full Flight Simulator (FFS) | |

| Flight Training Devices (FTD) | ||

| Other Training Devices | ||

| Application | Commercial Aviation | |

| Space | ||

| Geography | North America | United States |

| Canada | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Rest of Latin America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Civil Aerospace Simulation And Training Market?

The Civil Aerospace Simulation And Training Market size is expected to reach USD 1.93 billion in 2025 and grow at a CAGR of 6.64% to reach USD 2.66 billion by 2030.

What is the current Civil Aerospace Simulation And Training Market size?

In 2025, the Civil Aerospace Simulation And Training Market size is expected to reach USD 1.93 billion.

Who are the key players in Civil Aerospace Simulation And Training Market?

CAE Inc., L3Harris Technologies, Inc, The Boeing Company, FlightSafety International and Indra Sistemas SA are the major companies operating in the Civil Aerospace Simulation And Training Market.

Which is the fastest growing region in Civil Aerospace Simulation And Training Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Civil Aerospace Simulation And Training Market?

In 2025, the North America accounts for the largest market share in Civil Aerospace Simulation And Training Market.

What years does this Civil Aerospace Simulation And Training Market cover, and what was the market size in 2024?

In 2024, the Civil Aerospace Simulation And Training Market size was estimated at USD 1.80 billion. The report covers the Civil Aerospace Simulation And Training Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Civil Aerospace Simulation And Training Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: