| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 8.43 Billion |

| Market Size (2030) | USD 11.48 Billion |

| CAGR (2025 - 2030) | 6.38 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Chronic Venous Occlusions Treatment Market Analysis

The Chronic Venous Occlusions Treatment Market size is estimated at USD 8.43 billion in 2025, and is expected to reach USD 11.48 billion by 2030, at a CAGR of 6.38% during the forecast period (2025-2030).

The chronic venous occlusions treatment landscape is significantly influenced by global demographic shifts and aging populations, which are creating unprecedented healthcare demands. According to recent data from the Union for International Cancer Control, there are over 760 million people worldwide above the age of 65, representing over 9% of the global population, with this proportion projected to rise to 1.6 billion people by 2050. This demographic transition is particularly significant as approximately 53% of people who had cancer in 2022 were 65 or older, highlighting the increasing prevalence of conditions that can lead to venous thrombosis and other venous complications. The aging population's susceptibility to chronic diseases and cardiovascular conditions is reshaping treatment approaches and driving innovation in venous occlusion management.

The industry is witnessing a significant shift toward minimally invasive procedures and advanced therapeutic approaches, supported by technological innovations and improved treatment modalities. Recent statistics from the National Institutes of Health indicate that over 25 million individuals in the United States are affected by varicose veins, with more than six million suffering from severe venous disease. This substantial patient population has catalyzed the development of sophisticated treatment options, including advanced compression devices, novel stenting systems, and innovative therapeutic approaches that offer improved patient outcomes and reduced recovery times. These advancements are integral to the evolving landscape of vascular medicine.

The market is experiencing a transformation through strategic collaborations and technological advancements that are reshaping treatment paradigms. For instance, in June 2024, Philips launched its Duo Venous Stent System following FDA premarket approval, while InVera Medical introduced the world's first effective non-thermal medical device for treating chronic venous disease in March 2023. These innovations reflect the industry's commitment to developing more effective and patient-friendly treatment options, particularly focusing on minimally invasive approaches and improved clinical outcomes in venous therapy.

The sector is increasingly focusing on personalized medicine approaches and integrated care solutions, driven by advances in genetic testing and biomarker-guided therapies. According to the World Health Organization's March 2023 data, approximately 33% of adults aged 30-79 worldwide are affected by hypertension, a significant risk factor for vascular occlusion and venous occlusions. This high prevalence has spurred research into personalized treatment approaches, with healthcare providers increasingly adopting comprehensive care models that combine traditional treatments with innovative therapeutic options. The integration of telemedicine and remote monitoring technologies is further enhancing patient care and treatment accessibility, particularly in managing chronic conditions and post-treatment follow-up care.

Chronic Venous Occlusions Treatment Market Trends

Increasing Prevalence of Venous Occlusion Diseases

Chronic venous occlusions are primarily caused by conditions such as deep vein thrombosis, chronic inflammation, and venous insufficiency, which lead to the formation of blood clots, vein wall thickening, and impaired blood flow. The growing cases of diabetes, glaucoma, high blood pressure, and obesity are significantly driving the prevalence of venous occlusion diseases worldwide. According to the International Diabetes Federation (IDF) report of 2022, the number of individuals living with diabetes is projected to increase to 643 million by 2030 and 783 million by 2045. Similarly, according to data published by the National Institutes of Health (NIH) in April 2023, varicose veins affected over 25 million individuals in the United States, with more than six million suffering from severe venous disease, underscoring the significant prevalence of chronic venous disease as a major health condition.

The increasing prevalence of hypertension worldwide has led to a steep rise in the occurrence of venous occlusion disease. According to data published by the World Health Organization (WHO) in March 2023, hypertension affects approximately 33% of adults aged 30-79 worldwide. The most common signs of chronic venous diseases are telangiectasis, reticular veins, varicose veins, and venous ulcerations. Growing cases of diabetes, high blood pressure, and obesity, along with increasing pregnancy rates, are expected to increase the adoption of chronic venous occlusion treatments. The substantial burden of these underlying conditions creates a pressing need for effective venous occlusion management strategies and treatments, including venous compression therapy to alleviate symptoms and improve patient outcomes.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Availability of Advanced Treatments and Devices

The emergence of minimally invasive devices for chronic venous treatment has significantly boosted market growth, offering several advantages over traditional surgeries such as shorter recovery times, reduced pain and discomfort, lower risk of complications, and outpatient procedures. Major players in the market are actively introducing novel technologies to address the rising demand for treating chronic venous occlusions. For instance, in June 2024, Philips launched its Duo Venous Stent System, an implantable medical device indicated to treat symptomatic venous outflow obstruction in patients with chronic venous insufficiency (CVI), following premarket approval from the US Food and Drug Administration. In the same month, Inari Medical's Venacore thrombectomy catheter was introduced at the Cardiovascular Institute of the South (CIS), Louisiana, becoming one of the first mechanical thrombectomy devices specifically designed for peripheral venous occlusions.

The industry continues to witness significant technological advancements and innovative product launches. In March 2023, InVera Medical Limited launched InVera, the world's first effective non-thermal medical device to treat chronic venous disease. Additionally, key players are adopting growth strategies such as collaborations to boost their market presence. For instance, in June 2022, ClexBio collaborated with the Swiss Center for Electronics and Microtechnology to develop the world's first machine to grow tissue-engineered human veins in the lab, receiving over CHF 2 million (USD 2.24 million) in funding from the Research Council of Norway. These technological advancements and strategic initiatives demonstrate the industry's commitment to developing more effective and patient-friendly treatment options for chronic venous occlusions. Furthermore, the introduction of venous diagnostic tools and venous compression therapy devices is expected to enhance patient care and treatment efficacy.

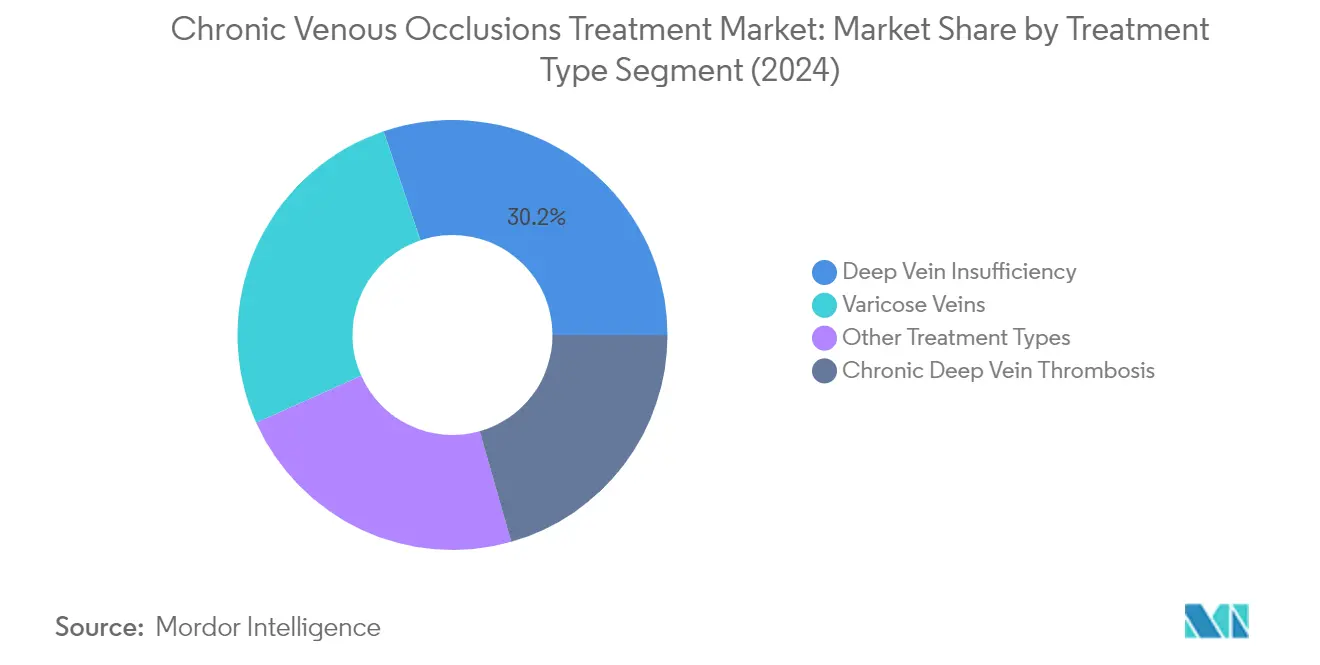

Segment Analysis: By Treatment Type

Deep Vein Insufficiency Segment in Chronic Venous Occlusions Treatment Market

Deep Vein Insufficiency represents the largest segment in the chronic venous occlusions treatment market, accounting for approximately 30% of the total market value in 2024. This dominant position is attributed to the increasing prevalence of deep vein insufficiency cases globally, particularly among aging populations and individuals with sedentary lifestyles. The segment's growth is further supported by technological advancements in treatment options, including the development of novel non-surgical replacement venous valves and minimally invasive procedures. For instance, enVeno Medical Corporation's accelerated development of enVVe, a transcatheter-based replacement venous valve, demonstrates the ongoing innovation in this segment. The rising adoption of these advanced treatment methods, coupled with growing awareness about early diagnosis and treatment of deep vein insufficiency, continues to strengthen this segment's market leadership.

Chronic Deep Vein Thrombosis Segment in Chronic Venous Occlusions Treatment Market

The Chronic Deep Vein Thrombosis segment is emerging as the fastest-growing segment in the market, projected to grow at approximately 7% CAGR from 2024 to 2029. This remarkable growth is driven by several factors, including the increasing adoption of advanced thrombectomy devices and innovative treatment approaches. The segment's expansion is supported by significant technological developments, such as SonoVascular Inc.'s strategic collaboration with Lantheus Holdings Inc. in 2024 to enhance DVT treatment through their SonoThrombectomy System. This system's innovative approach combines ultrasound, microbubbles, low-dose thrombolytic drugs, and mechanical retrieval in an integrated intravascular catheter system. Additionally, the growing focus on minimally invasive procedures and the development of more effective anticoagulation therapies are contributing to the segment's accelerated growth trajectory. The deep vein thrombosis market is expected to benefit significantly from these advancements.

Remaining Segments in Treatment Type

The Varicose Veins and Other Treatment Types segments continue to play vital roles in shaping the chronic venous occlusions treatment market. The Varicose Veins segment benefits from increasing awareness about aesthetic concerns and the availability of advanced treatment options like foam sclerotherapy and endovenous laser treatments. Meanwhile, the Other Treatment Types segment, which includes various emerging treatment modalities and specialized procedures, contributes to market diversity through continuous innovation and the development of alternative treatment approaches. Both segments are characterized by ongoing technological advancements and increasing patient preference for minimally invasive procedures, reflecting the market's overall trend toward more sophisticated and patient-friendly treatment options. The integration of venous compression therapy is also becoming more prevalent in these treatment strategies.

Segment Analysis: By Product Type

Devices Segment in Chronic Venous Occlusions Treatment Market

The devices segment dominates the chronic venous occlusions treatment market, holding approximately 55% of the market share in 2024. This significant market position is attributed to the increasing adoption of advanced medical devices such as thrombectomy devices, inferior vena cava (IVC) filters, peripheral vascular stents, and percutaneous transluminal angioplasty (PTA) balloon catheters. The segment's growth is further supported by technological advancements in minimally invasive procedures and the rising demand for compression devices and stockings. Key market players are actively launching innovative devices, such as Philips' Duo venous stent market System and Inari Medical's Venacore thrombectomy catheter in 2024, which has strengthened the segment's market position. Additionally, the growing preference for outpatient procedures and the increasing focus on improved patient outcomes have contributed to the sustained dominance of the devices segment.

Therapeutics Segment in Chronic Venous Occlusions Treatment Market

The therapeutics segment is emerging as the fastest-growing segment in the chronic venous occlusions treatment market, with a projected growth rate of approximately 7% from 2024 to 2029. This accelerated growth is primarily driven by the increasing adoption of novel oral anticoagulants and the emergence of cost-effective biosimilars. The segment's expansion is further supported by ongoing clinical trials and research activities, such as Bayer AG's Phase II clinical trial for BAY3018250, an innovative anti-α2 antiplasmin antibody, launched in February 2024. The rise of biosimilars is particularly significant, as demonstrated by Fresenius Kabi Canada's successful securing of public reimbursement for ELONOX, its enoxaparin biosimilar, across all Canadian provinces in 2023. Additionally, the development of new coagulation tests and the increasing focus on personalized medicine approaches are contributing to the segment's rapid growth trajectory. The deep vein thrombosis market is poised to benefit from these advancements in therapeutics.

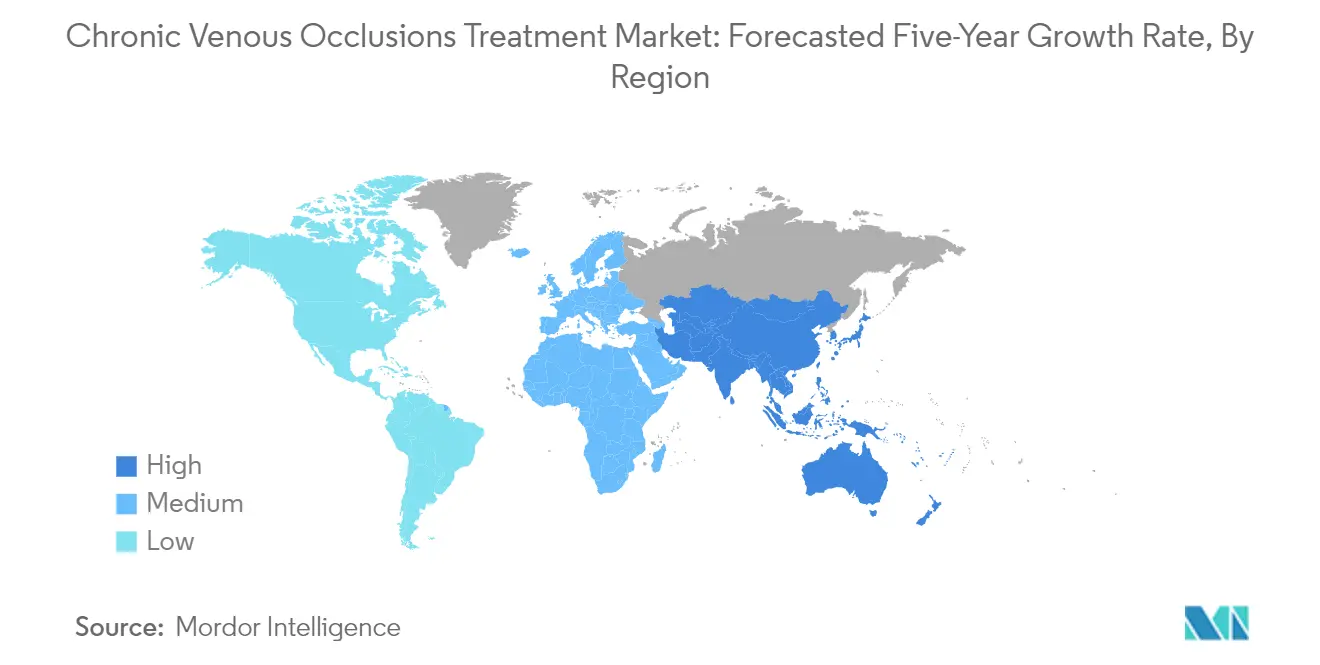

Chronic Venous Occlusions Treatment Market Geography Segment Analysis

Chronic Venous Occlusions Treatment Market in North America

North America represents a dominant force in the chronic venous occlusions treatment market, driven by advanced healthcare infrastructure and high adoption rates of innovative medical technologies. The region benefits from extensive insurance coverage, well-established healthcare systems, and increasing awareness about venous diseases. The United States, Canada, and Mexico collectively contribute to the market's growth through their respective healthcare initiatives and growing patient populations requiring treatment for chronic venous conditions. The region's focus on vascular medicine further enhances its market leadership.

Chronic Venous Occlusions Treatment Market in the United States

The United States leads the North American market with its comprehensive treatment facilities and advanced healthcare infrastructure. The country accounts for approximately 82% of the North American market in 2024, supported by the presence of major market players and extensive research activities. The growing prevalence of venous diseases and chronic venous insufficiency (CVI) continues to drive market growth, alongside increasing demand for minimally invasive procedures. The country's healthcare system emphasizes early detection and treatment of venous disorders, supported by favorable reimbursement policies and continuous technological advancements in treatment options, including venous therapy and venous diagnostic techniques.

Chronic Venous Occlusions Treatment Market in Canada

Canada emerges as the fastest-growing market in North America, with an expected growth rate of approximately 7% from 2024 to 2029. The country's market expansion is driven by increasing strategic activities such as product launches and a rising prevalence of cardiovascular diseases. The Canadian healthcare system's focus on preventive care and treatment accessibility contributes significantly to market growth. The country has witnessed substantial developments in minimally invasive procedures and enhanced treatment protocols, supported by government initiatives to strengthen healthcare infrastructure and improve patient outcomes, particularly in the realm of vascular medicine.

Chronic Venous Occlusions Treatment Market in Europe

Europe maintains a significant position in the global chronic venous occlusions treatment market, characterized by its robust healthcare infrastructure and strong focus on medical innovation. The region encompasses key markets including Germany, the United Kingdom, France, Italy, and Spain, each contributing uniquely to the market's development. The European market benefits from extensive research and development activities, strong healthcare policies, and increasing adoption of advanced treatment methodologies, including venous therapy and venous diagnostic advancements.

Chronic Venous Occlusions Treatment Market in Germany

Germany stands as the largest market in Europe, commanding approximately 24% of the regional market share in 2024. The country's market leadership is attributed to its advanced healthcare system and high population suffering from cardiovascular diseases. The German healthcare landscape features extensive insurance coverage, state-of-the-art medical facilities, and a strong focus on innovative treatment approaches. The country's commitment to healthcare excellence is reflected in its continuous investment in research and development, particularly in minimally invasive treatment options and vascular medicine.

Chronic Venous Occlusions Treatment Market in France

France demonstrates the highest growth potential in Europe, with a projected growth rate of approximately 7% from 2024 to 2029. The country's market is characterized by its progressive healthcare policies and increasing focus on advanced treatment methodologies. French healthcare providers are increasingly adopting innovative technologies and treatment approaches, supported by government initiatives promoting novel treatment methods. The country's strong emphasis on research and development, coupled with rising awareness about venous diseases, positions it as a key growth market in the region, particularly in addressing venous thrombosis.

Chronic Venous Occlusions Treatment Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for chronic venous occlusions treatment, characterized by rapid healthcare infrastructure development and increasing awareness about venous diseases. The region encompasses diverse markets including China, Japan, India, Australia, and South Korea, each at different stages of healthcare development and market maturity. The market is driven by improving healthcare access, rising disposable incomes, and growing adoption of advanced medical technologies, including those targeting venous thrombosis.

Chronic Venous Occlusions Treatment Market in China

China emerges as the dominant market in the Asia-Pacific region, supported by its large patient population and rapidly evolving healthcare infrastructure. The country's market leadership is driven by increasing cardiovascular disease burden and growing adoption of innovative treatment technologies. The Chinese healthcare system's ongoing modernization, coupled with rising healthcare expenditure and improving access to advanced medical treatments, continues to drive market growth, particularly in the field of venous diagnostic.

Chronic Venous Occlusions Treatment Market in India

India demonstrates remarkable growth potential in the Asia-Pacific region, driven by its expanding healthcare infrastructure and increasing awareness about venous diseases. The country's market is characterized by rising adoption of advanced treatment methodologies and growing private healthcare sector participation. The emergence of specialized vascular centers and clinics, coupled with the country's strong position in medical tourism, contributes significantly to market expansion, especially in vascular medicine.

Chronic Venous Occlusions Treatment Market in Middle East & Africa

The Middle East & Africa region presents unique opportunities in the chronic venous occlusions treatment market, with varying healthcare infrastructure levels across different countries. The region, encompassing GCC countries and South Africa, shows increasing adoption of advanced treatment methodologies. The GCC countries lead the regional market, benefiting from well-developed healthcare infrastructure and high healthcare spending, while South Africa shows the fastest growth potential driven by improving healthcare access and rising awareness about venous diseases.

Chronic Venous Occlusions Treatment Market in South America

South America demonstrates growing potential in the chronic venous occlusions treatment market, with Brazil and Argentina as key contributors. The region's market is characterized by increasing healthcare infrastructure development and rising awareness about venous diseases. Brazil emerges as the largest market in the region, supported by its extensive healthcare network and growing adoption of advanced treatments, while Argentina shows the fastest growth potential driven by increasing healthcare investments and improving treatment accessibility.

Get Analysis on Important Geographic Markets

Download PDF

Chronic Venous Occlusions Treatment Industry Overview

Top Companies in Chronic Venous Occlusions Treatment Market

The chronic venous occlusions treatment market is characterized by intense innovation and strategic developments among key players, including Cardinal Health, Stryker Corp., Cook Medical, Boston Scientific Corporation, and Edwards Lifesciences. Companies are heavily investing in developing minimally invasive devices and advanced therapeutic solutions, particularly focusing on thrombectomy devices, venous stents, and compression systems. The market demonstrates strong operational agility through rapid product commercialization and regulatory approvals, especially in major markets like North America and Europe. Strategic collaborations and licensing agreements have become increasingly common as companies seek to expand their technological capabilities and geographic presence. Market leaders are also emphasizing the expansion of their distribution networks and strengthening their presence in emerging markets through local partnerships and the establishment of regional manufacturing facilities.

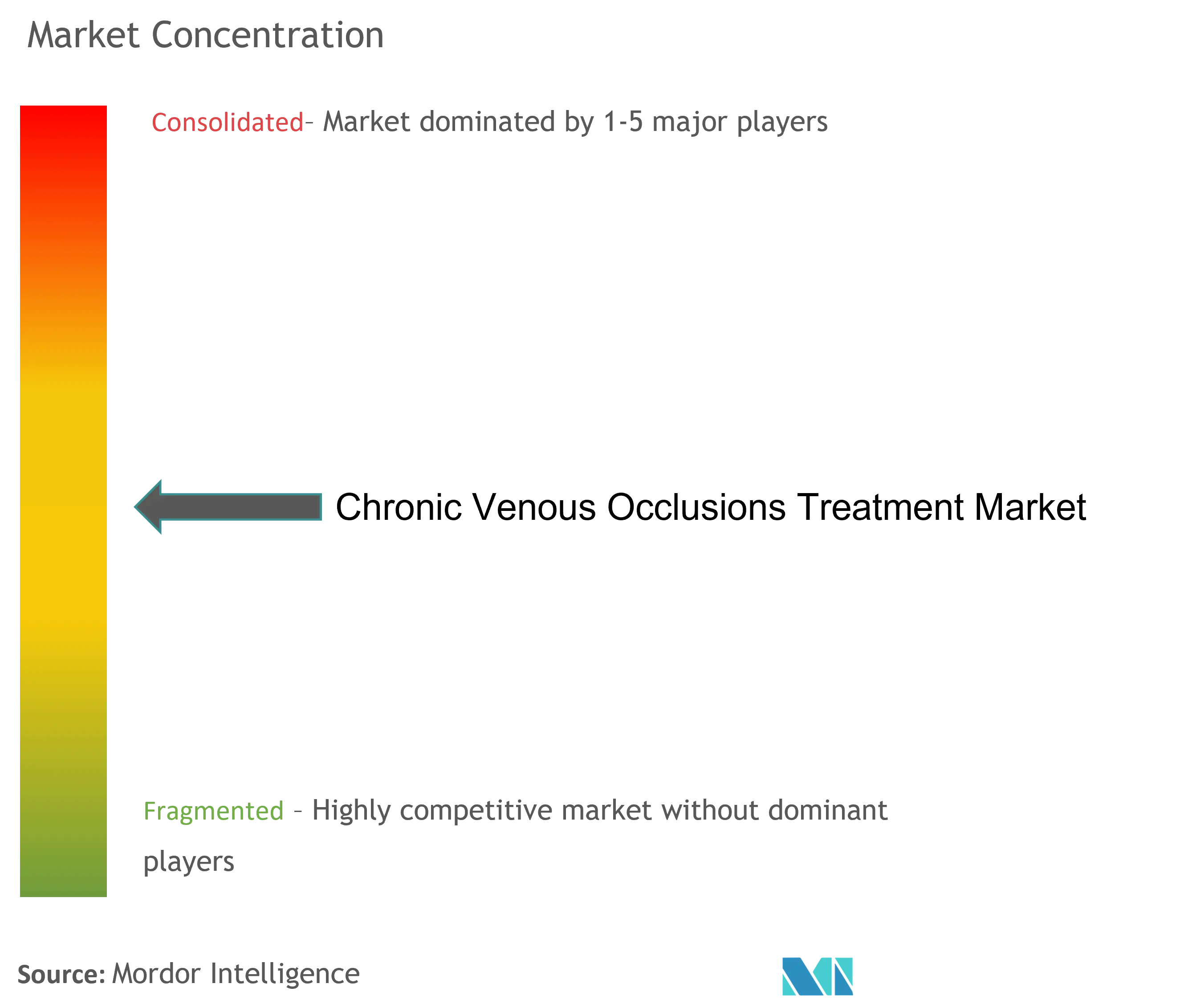

Consolidated Market with Strong Regional Players

The chronic venous occlusions treatment market exhibits a relatively consolidated structure dominated by large multinational medical device manufacturers and pharmaceutical companies with diverse product portfolios. These established players leverage their extensive research and development capabilities, robust distribution networks, and strong brand recognition to maintain their market positions. Regional players, particularly in Asia-Pacific and Europe, have carved out significant niches by focusing on specific product categories or geographic markets, often competing through cost leadership and local market knowledge.

The market has witnessed significant merger and acquisition activity as larger companies seek to expand their product offerings and strengthen their market presence. Companies are particularly targeting acquisitions of innovative startups and smaller firms with promising technologies in areas such as mechanical thrombectomy and venous stenting. This consolidation trend is driven by the need to achieve economies of scale, access new technologies, and expand geographic reach. Vertical integration strategies are also becoming more prevalent as companies seek to control key aspects of their supply chain and enhance their competitive advantage.

Innovation and Market Access Drive Success

Success in the chronic venous occlusions treatment market increasingly depends on companies' ability to innovate while maintaining cost competitiveness. Incumbent players must focus on continuous product innovation, particularly in developing minimally invasive solutions and improving patient outcomes. Building strong relationships with healthcare providers and maintaining robust clinical evidence for product efficacy are crucial for market share retention. Companies must also adapt to evolving reimbursement landscapes and strengthen their market access capabilities through strategic partnerships with healthcare providers and payers.

For new entrants and smaller players, success lies in identifying and exploiting specific market niches where they can differentiate themselves from larger competitors. This includes focusing on underserved geographic markets or developing specialized solutions for specific patient populations. The relatively low risk of substitution from alternative treatments provides stability, but companies must navigate complex regulatory requirements and maintain strong quality control systems. Future success will increasingly depend on the ability to demonstrate both clinical and economic value, particularly as healthcare systems globally focus on cost containment while maintaining quality of care. Additionally, advancements in venous imaging and vascular medicine are expected to play a pivotal role in enhancing treatment outcomes and expanding market opportunities.

Chronic Venous Occlusions Treatment Market Leaders

-

Cardinal Health

-

Stryker

-

Boston Scientific Corporation

-

Edward Lifesciences

-

AngioDynamics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Chronic Venous Occlusions Treatment Market News

- April 2024: Johnson & Johnson presented new findings from the PIONEER AF-PCI clinical trial, revealing that XARELTO (rivaroxaban) outperformed warfarin in reducing the risk of clinically significant bleeding (CSB) and net adverse clinical events (NACE) in patients with nonvalvular atrial fibrillation (AF) who underwent percutaneous coronary intervention (PCI). These results, unveiled at the American College of Cardiology's 73rd Annual Scientific Session & Expo in Atlanta, Georgia, highlight XARELTO's potential advantages for elderly and non-elderly patients.

- April 2024: AngioDynamics Inc. secured FDA clearance for its AlphaVac F1885 System, broadening its application to address pulmonary embolism (PE), a significant advancement in critical medical scenarios. This expanded FDA approval now specifically encompasses the non-surgical removal of thrombi or emboli from the venous vasculature.

Chronic Venous Occlusions Treatment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Availability of Advanced Treatments and Devices

- 4.2.2 Increasing Prevalence of Venous Occlusion Diseases

-

4.3 Market Restraints

- 4.3.1 Cost Consciousness Coupled with Risk and Complications Associated with Treatment

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Treatment Type

- 5.1.1 Chronic Deep Vein Thrombosis

- 5.1.2 Varicose Veins

- 5.1.3 Deep Vein Insufficiency

- 5.1.4 Other Treatment Types

-

5.2 By Product Type

- 5.2.1 Devices

- 5.2.2 Therapeutics

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Cardinal Health

- 6.1.2 Stryker

- 6.1.3 Cook Medical

- 6.1.4 Boston Scientific Corporation

- 6.1.5 Edward Lifesciences

- 6.1.6 AngioDynamics

- 6.1.7 SIGVARIS GROUP

- 6.1.8 Johnson & Johnson Inc. (Janssen Global Services LLC)

- 6.1.9 Penumbra Inc.

- 6.1.10 Becton, Dickinson and Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Chronic Venous Occlusions Treatment Industry Segmentation

As per the scope of the report, venous occlusion is a condition in which a vein becomes narrowed, blocked, or compressed by nearby structures such as clots, muscles, arteries, or other veins, which results in blood pooling and flowing backward, causing swelling and pain in the area. The introduction of new technology to treat venous occlusion is expected to emerge, and the market is likely to witness more vertical integration and joint ventures during the forecast period.

The chronic venous occlusion treatment market is segmented by treatment type, product type, and geography. The market is segmented by treatment type into chronic deep vein thrombosis, varicose veins, deep vein insufficiency, and other treatment types. By product type, the market is subsegmented into devices and therapeutics. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (in USD) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across the major regions globally.

| By Treatment Type | Chronic Deep Vein Thrombosis | ||

| Varicose Veins | |||

| Deep Vein Insufficiency | |||

| Other Treatment Types | |||

| By Product Type | Devices | ||

| Therapeutics | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Chronic Venous Occlusions Treatment Market Research Faqs

How big is the Chronic Venous Occlusions Treatment Market?

The Chronic Venous Occlusions Treatment Market size is expected to reach USD 8.43 billion in 2025 and grow at a CAGR of 6.38% to reach USD 11.48 billion by 2030.

What is the current Chronic Venous Occlusions Treatment Market size?

In 2025, the Chronic Venous Occlusions Treatment Market size is expected to reach USD 8.43 billion.

Who are the key players in Chronic Venous Occlusions Treatment Market?

Cardinal Health, Stryker, Boston Scientific Corporation, Edward Lifesciences and AngioDynamics are the major companies operating in the Chronic Venous Occlusions Treatment Market.

Which is the fastest growing region in Chronic Venous Occlusions Treatment Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Chronic Venous Occlusions Treatment Market?

In 2025, the North America accounts for the largest market share in Chronic Venous Occlusions Treatment Market.

What years does this Chronic Venous Occlusions Treatment Market cover, and what was the market size in 2024?

In 2024, the Chronic Venous Occlusions Treatment Market size was estimated at USD 7.89 billion. The report covers the Chronic Venous Occlusions Treatment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Chronic Venous Occlusions Treatment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Chronic Venous Occlusions Treatment Market Research

Mordor Intelligence offers extensive expertise in vascular medicine research. We deliver a comprehensive analysis of treatments for venous thrombosis and vascular occlusion conditions. Our research thoroughly examines various aspects, including venous catheter technologies, advanced venous therapy approaches, and emerging venous imaging techniques. The report provides detailed insights into the deep vein thrombosis market dynamics. This is supported by extensive clinical data and consultations with industry experts.

Stakeholders can access crucial information about venous compression therapy solutions and venous stent market developments. This information is available through our easy-to-download report PDF format. The analysis encompasses cutting-edge venous diagnostic methodologies. It offers healthcare providers, manufacturers, and investors a complete understanding of market dynamics and growth opportunities. Our research helps organizations make informed decisions about technology investments, treatment protocols, and strategic planning in the chronic venous occlusions treatment sector.